Update on $UPST (Upstart)

Update on $UPST (Upstart)

One of my favorite stocks and largest holdings is Upstart aka $UPST

I did my original writeup on $UPST on December 28th, 2020 when the stock was at $38.50

You can read that writeup here: https://jonahlupton.substack.com/p/upst-upstart

$UPST closed today at $84.05 so the stock is still up nicely since my writeup and currently up 106% year to date but the stock has been very volatile and currently 49% off the highs from March 22nd.

This chart below shows how wild the past few months have been.

RESOURCES:

2021 Q1 earnings press release [click here]

2021 Q1 earnings presentation [click here]

2021 Q1 earnings conference call [click here]

OVERVIEW:

$UPST came public in December but wasn’t one of the overly hyped IPOs like DoorDash, Snowflake or Airbnb so the company was flying under the radar when I began doing my due diligence in late December. As I read more about the company, looked through their investor presentation and listened to some interviews I became very excited about what the company was doing.

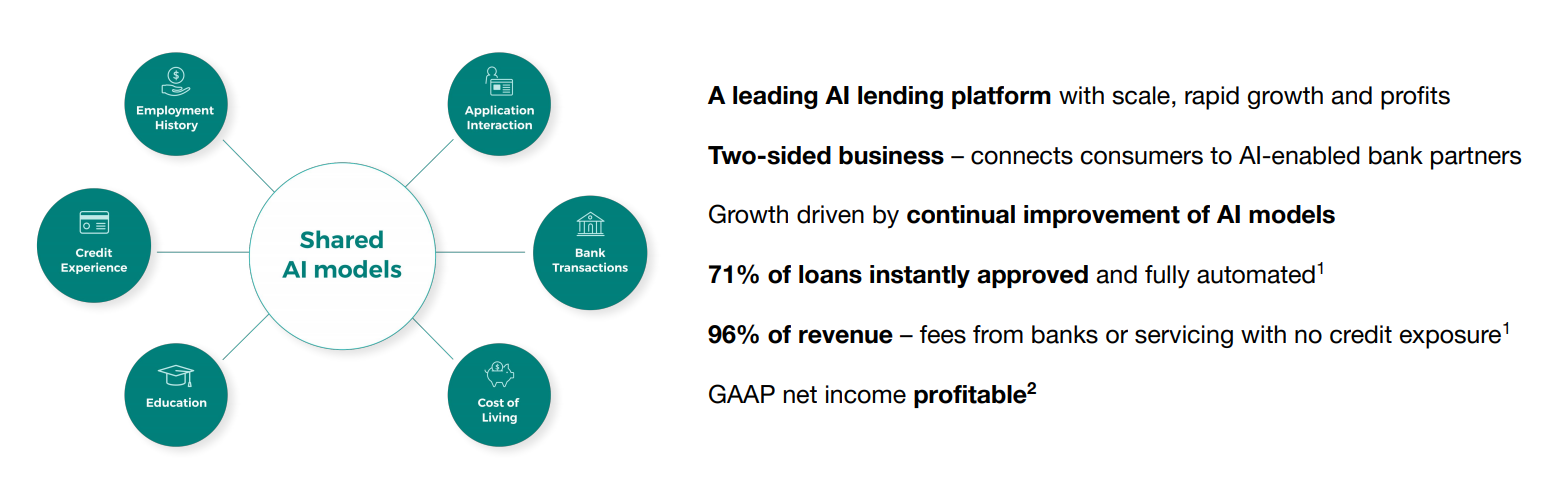

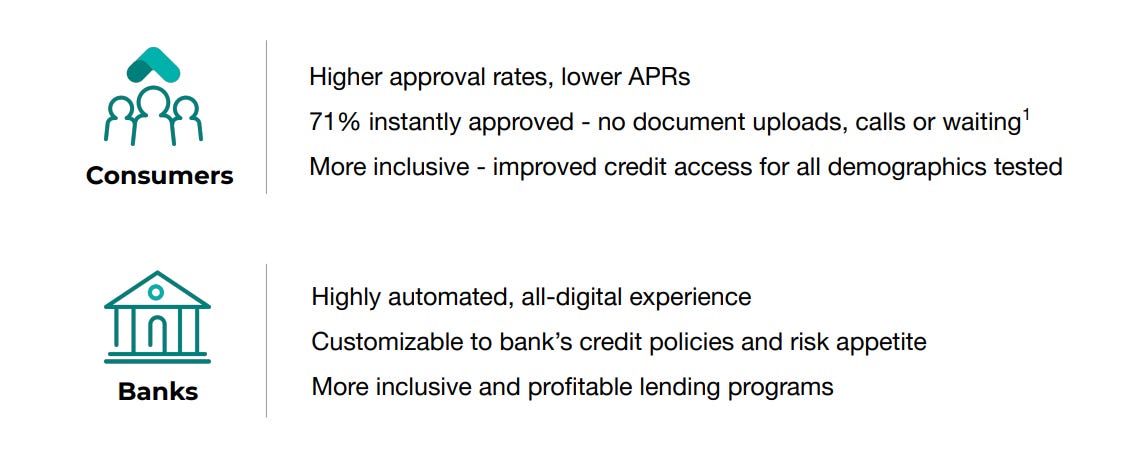

$UPST had developed a proprietary AI (artificial intelligence) model to improve the underwriting process of banks. As you may know most loans are approved based on FICO scores however this is very limited in terms of the data being considered to determine whether or not the applicant is approved.

$UPST’s model uses approximately 1600 data points and variables on the loan applicant which includes typical credit history stuff but adds things like education, job experience, geography, cost of living expenses, and so much more. Having all of these extra variables has enabled $UPST to build a better underwriting model which more accurately determines the credit worthiness of the applicant therefore more accurately predicting that person’s ability to pay back the loan. This is important because it means the banks underwriting these loans can issues more loans without increasing their risk (aka default rates).

$UPST started out doing personal loans but has since expanded into auto loans and recently acquired a company called Prodigy [click here] to help accelerate that growth. $UPST’s CEO says Prodigy is like “Shopify for car dealers” which will enable them to deliver a better digital experience to their customers. This is exciting for $UPST because selling this software to auto dealers will allow them to become one of the options for car buyers since most of them also need a loan at the time of purchase.

The auto loans market is almost 7x bigger than the personal loans market so this expansion is very exciting for $UPST shareholders. As you can see from the slide below I think $UPST is hinting that mortgages and credit cards might also be coming someday soon.

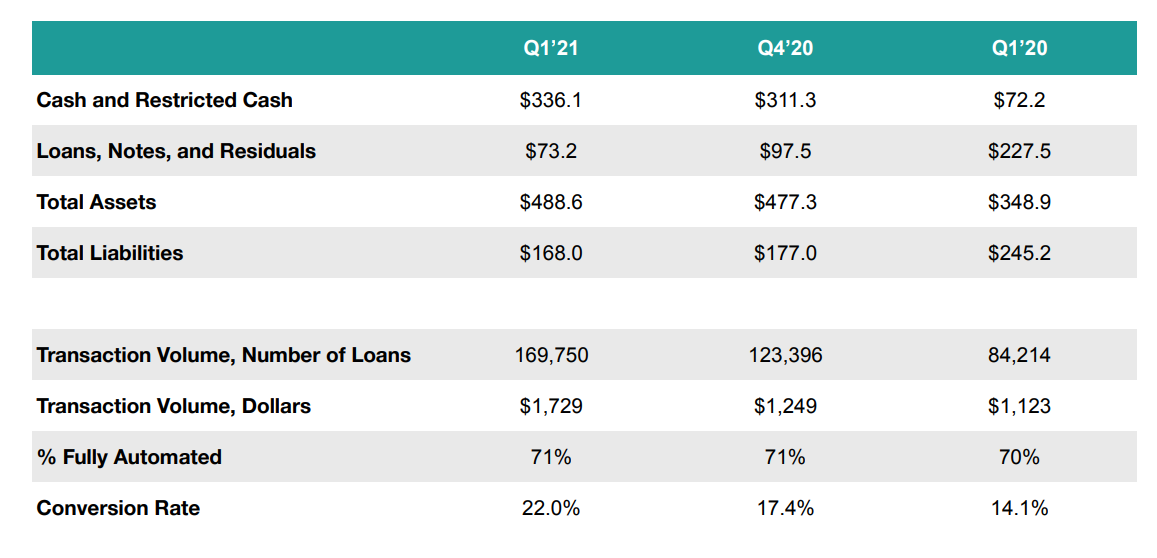

Q1 FINANCIAL RESULTS:

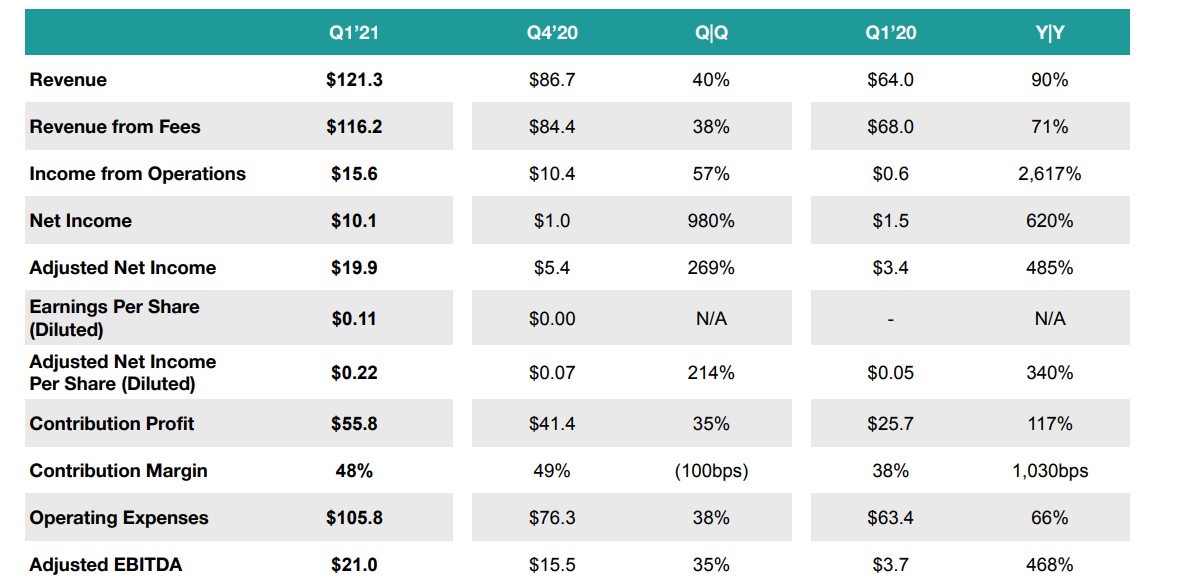

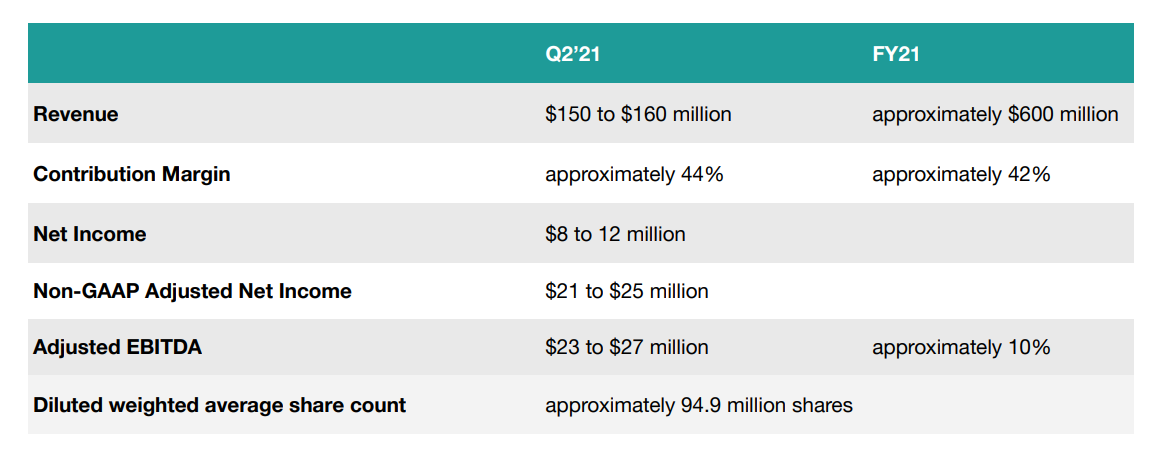

Seeing Q1 revenues of $121 million which was up 90% YoY was great since the estimates were for $115 million but clearly the exciting surprise from this report was raising Q2 guidance from $117 million to $155 million (technically they gave a $150M to $160M range). This is a monster raise and would have been enough to get me excited but then I read the company was raising full year 2021 guidance from $500 million to $600 million. Back in December when the company went public they were forecasting 2021 revenues of $360 million so the fact that guidance has gone from $360 million to $600 million in less than 6 months means the business is doing phenomenal.

I have a feeling that $600 million guidance for 2021 might be conservative but that number alone represents 158% YoY revenue growth for $UPST.

This is incredible growth but the most impressive part is that the company is growing this rapidly while remaining profitable and to be honest they’ve only scratched the surface for what is possible in terms of using AI and ML (machine learning) to improve the underwriting process.

$UPST has proven over the past 8 years, while collecting 16+ billion data points and processing hundreds of thousands of loans that their models are faster, cheaper, more accurate and better at assessing risks which is what the banks ultimately care about.

$UPST still has an incredible opportunity to not only expand into more credit markets but bring on more bank partners and referral partners to help generate more demand for loans. With conversion rates up from 14.1% last year to 22.0% in Q1 of this year it means they can justify spending more money on sales and marketing to fill the top of the funnel. This was mentioned on the recent earnings call.

VALUATION:

With $UPST pulling back over the past couple days since reporting Q1 earnings to $84.05 it means the current market cap (using the fully diluted share count as seen above) is $7.97 billion then you take out the cash and we get an enterprise value of $7.64 billion.

If we assume that $UPST does at least $600 million in revenues this year (probably conservative) it means that $UPST is currently trading at 12.7x EV/Sales. I challenge everyone reading this writeup to find me another company that is growing revenues at over 150% while trading at less than 13x EV/Sales and is already profitable. I bet you can’t because I’ve tried and couldn’t find one.

$UPST is my version of a unicorn and there’s no doubt in my mind this stock is going much higher.

I have 5-year financial models on all of my top holdings and I believe $UPST can get to $4-5 billion in revenues in 2025.

Since $UPST has a very high margin, asset light business model I believe they can get to 25-30% net income margins by 2025.

If we use the low end of these assumptions it means $UPST would generate at least $1 billion of earnings in 2025. At that time I believe they’d still be growing revenues in the 50% range which means a 50 P/E would be justified although I’ll discount that down to a 40 P/E for all you ball busters.

$1 billion of earnings x 40 P/E = $40 billion market cap in 2025

Using the current enterprise value of $7.64 billion, if $UPST gets to a $40 billion market cap in 2025 based on my estimates you’d have a 51.5% annualized return on your $UPST shares from current prices.

This is a simplified financial model but I wanted to give you an idea of where I think $UPST could go over the next 4+ years. I believe the future is very bright for this company assuming they continue to execute really well, bring on more bank partners and expand into more credit markets.

Of course there are risks such as:

What if we run into a recession (very unlikely in my opinion) = these AI models are so advanced they already have built in variables and calculations for a million different scenarios, this is why AI is the future of underwriting

What if other companies begin to develop similar AI models = they might try but $UPST has an 8 year head start, they continue to hire the smartest PhDs, engineers, computer scientists, AI experts, etc. — the $UPST CEO has already stated that no other company is even remotely close to them and when they’re hiring for talent they are not competing with banks or other FinTech’s, they are competing against Google, IBM, etc. — personally I don’t see any bank spending the time and resources to develop their own AI models when they can just use $UPST’s for a fee.

What about the concentration risk amongst their bank partners and referral partners = this is a valid concern but the company acknowledges this issue and is already showing signs of diversifying which includes doing more DTC advertising rather than relying on third party marketing channels like Credit Karma. This is only a concern for loan applicants that are coming through Upstart.com or one of their referral partners where all of their bank partners are competing for that business. When the applicants come through a bank partner’s website this is not an issue because those loans are not getting fished around so there is less concern about bank concentration risk. Many of the recent banks that have come onto the $UPST platform have $25-50 billion of assets/loans so they are decent sized banks. I believe this is the sweet spot for $UPST right now. The total number of commercial banks in the U.S. is around 5,000 so there are plenty of banks that $UPST can still partner with.

CONCLUSION:

In closing I want to share my interview with David Girouard, CEO of $UPST — we recorded this conversation right after the company reported 2020 Q4 earnings in March so it’s a couple months old but the story/strategy is still the same.

I don’t think I’m going to get a new writeup out this week — to be honest I’m having a hard time finding any new growth companies that get me really excited. There are still some that I own and have not written about yet but I decided these updates might be more helpful given we’re in the middle of earnings season.

Over the next few days I’m planning to do similar updates for some of my other favorite companies, many of which have pulled back from their 2021 highs and now present great buying opportunities.

Once we get through earnings season I’ll feel more comfortable digging into the stocks on my watchlist and picking which ones to do writeups on. It will be beneficial to use recent Q1 earnings reports and conference calls in my writeups.

If you have any questions about $UPST feel free to send me an email. I didn’t want this writeup to be too long — my goal was to provide an overview of the company, highlight the Q1 earnings numbers and explain why I’m still super bullish on the company.