Update on $FUTU (Futu Holdings)

Update on $FUTU (Futu Holdings)

$FUTU — FUTU HOLDINGS

Website: www.FutuHoldings.com

Investor Relations: www.IR.FutuHoldings.com

Company Profile [click here]

Stock price: $124.00

Market cap: $18.2 billion

Enterprise value: $16.8 billion

2021 Q1 Earnings Report [click here]

2021 Q1 Earnings Call Webcast [click here]

2021 Q1 Earnings Call Transcript [click here]

2020 Annual Report [click here]

$FUTU to start offering crypto services in second half of 2021 [click here]

$FUTU to be added to the MSCI Hong Kong Index [click here]

INTRODUCTION:

Back on December 31st, I did my original writeup on $FUTU when the stock was trading in the low $40s: https://jonahlupton.substack.com/p/futu-futu-holdings

Please read that writeup so you understand what $FUTU does and how they make money. It doesn’t make sense for me to rewrite that entire analysis when the core business has not changed at all over the past 4+ months — however the stock price and the fundamentals have changed quite meaningful which is why I’m doing this update.

Below is how $FUTU describes themselves…

I often say that $FUTU is the “Robinhood of China” but that’s not completely accurate because given the different layers to their business model and their growth strategy including international expansion plans I’d say $FUTU is closer to the “Robinhood / WeBull / eTrade / Interactive Brokers / Charles Schwab of China” — $FUTU has similarities to each of these companies.

Q1 EARNINGS REPORT:

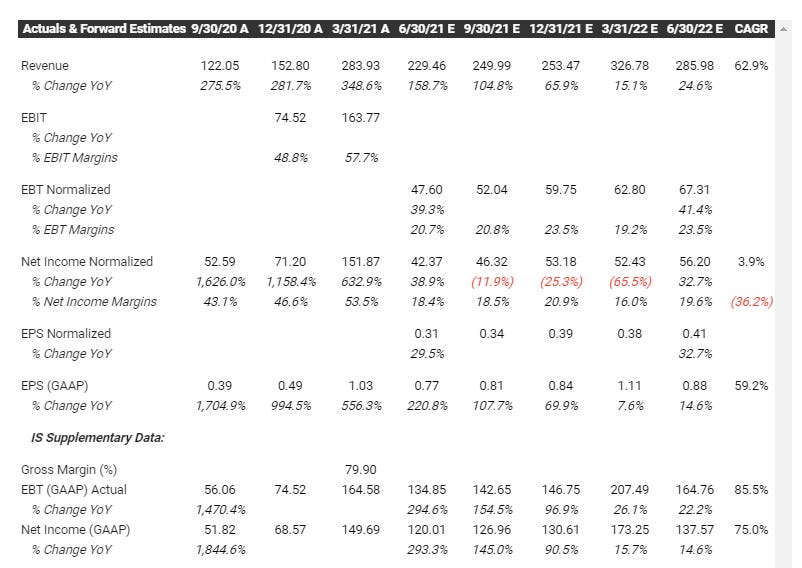

Let me start off by saying that $FUTU’s Q1 earnings report might have been the strongest I have ever seen, at least from a company that I owned. I was expecting great numbers but my jaw dropped when I saw the actual reported numbers.

The fact that the stock price has not moved since the blowout Q1 numbers makes me think there’s still a great opportunity to get into $FUTU before it starts heading back to $200+ which is where I believe it’s going in the next 3-6 months.

I’m hoping everyone read the Q1 earnings report [click here] but I’ll recap the numbers just to be sure:

Total revenues increased 349.4% YoY to $283.6 million

Total gross profit increased 372.6% YoY to $226.6 million

Net income was up 550% YoY to $149.5 million

Non-GAAP adjusted net income was up 530% YoY to $151.7 million

Total number of paying clients increased 231.0% YoY

Total number of registered clients increased 140.2% YoY

Total number of users increased 69.7% YoY to 14.2 million

Total client assets increased 367.6% YoY

Daily average client assets increased 303.7% YoY

Total trading volume increased 277.5% YoY

Daily average revenue trades (DARTs) increased 321.0% YoY

Margin financing and securities lending balance increased 469.5% YoY

These numbers above are just insane — which makes it really hard to value a company like $FUTU because we don’t have any good comparisons. We also don’t know how long this growth can continue at this pace.

Coming into the Q1 report, the analyst estimates for 2021 revenues were $930 million however since these blowout numbers the analyst estimates are now up to $1,052 million which is probably still too low.

In April, $FUTU completed a stock offering at $120/share with net proceeds of approximately $1.4 billion. The proceeds will be used to support a larger margin financing balances, international market expansion, new licensing applications, potential investment and acquisition opportunities and other general corporate purpose.

$FUTU said on the Q1 earnings call that 25% of new client additions came from Singapore and the U.S. with the other 75% coming from Hong Kong and mainland China. Organic growth continues to contribute more than 50% of new paying clients and the quarterly client churn rate is under 2%.

$FUTU is seeing early success with their wealth management business which includes strategic partnerships with firms like Well Fargo, Aberdeen and BNY Mellon as well as mutual fund companies looking for distribution to Chinese investors.

$FUTU is also doing a phenomenal job at growing their social investment community and convincing companies/enterprises to setup profiles, chat with retail investors, host webinars and livestream earnings calls. $FUTU is then able to convert these passionate retail investors into $FUTU clients through one or many of their brokerage/trading/wealth management services.

Robin Xu, SVP of $FUTU said from March 1st until May 16th, despite volatility in the global equity markets they saw positive inflows of net new assets every single trading day except for a couple days. This should be a good signal that Q2 is going well however I doubt we see the fundamentals in Q2 quite as strong as numbers in Q1.

This chart below is from the 2020 annual report but gives you a rough idea of where the revenues and costs are coming from. $FUTU said on the Q1 call that margin financing now accounts for 60-65% of the interest income which is one reason why they did that stock offering a month ago — so they could offer more margin to more customers — because more margin means more trading commissions and margin interest earned.

FINANCIALS:

Clearly this is where $FUTU really shines, as I showed you above, the financials for $FUTU in Q1 were just insane.

Putting up 348% YoY revenue growth with 52% net income margins is hard to comprehend because I’ve never seen it before. There’s definitely no other company on the planet with fundamentals this strong — I know because I’ve looked.

The analysts continue to raise their full year 2021 revenue estimates however I still think $1.052 billion is too low given what we just saw in Q1 and knowing how quickly $FUTU is expanding in their different markets.

Based on my own financial models I believe $FUTU can do closer to $1.2 billion in 2021 and stay around 50% net income margins which is also much higher than current estimates (42.9% net income margins).

Quarterly Financials/Estimates:

Annual Financials/Estimates:

VALUATION:

As I already mentioned it’s difficult to value a company like $FUTU because their fundamentals are so much stronger than any other publicly traded company. It’s possible that once we get the Robinhood S-1 (in preparation of their upcoming IPO) we’ll finally have a good comparison however I doubt Robinhood is growing revenues at 348% with 52% net income margins.

If I’m correct and $FUTU does $1.2 billion of revenues in 2021 with 50% net income margins it means the stock is currently trading at

Right now we have software companies trading at 14x 2021 EV/Sales and 28x 2021 EV/Earnings. Yup you read that correctly, $FUTU is growing revenues at 348% YoY with 52% net income margins and only trading at 28x earnings. WTF!!!!!!!

In full disclosure, I don’t expect $FUTU to maintain 348% YoY growth through the remainder of the year. If we know that $FUTU did $426 million in revenues in 2020 and I’m forecasting $1.2 billion in revenues for 2021 then it means I’m expecting 182% YoY growth for $FUTU.

However the P/E or EV/E multiple does not change, based on my forecasts $FUTU is trading at 28x earnings (using EV) with 182% revenue growth and 243% net income growth. Sorry but even with the “China discount” this stock is way too cheap.

Even if you used the low-ball analyst estimates of $1.052 billion in revenues and $451 million of net income $FUTU is still trading at just 16x 2021 EV/Sales or 37x earnings, both of which are still too low for a company growing this fast.

If you want to do some comparisons, let’s look at $IBKR (Interactive Brokers) which has a current market cap of $28 billion and is projected to do $2.8 billion in revenues in 2021. That means $IBKR is only trading at 10x 2021 sales/revenues which looks cheaper than $FUTU on the surface but when you take into account that $IBKR is only growing at 24% (or 1/8th of $FUTU’s growth rate).

Now, if you want to compare the two on P/E or EV/E the discrepancy is even bigger. $IBKR is expected to earn approximately $300 million in net income in 2021 which means that $IBKR is trading at 93x earnings. Based on everything I just laid out above, we already know that $FUTU is trading at 28-37x earnings depending on whether you trust my model (since I update regularly) or the analysts models (they seem to update quarterly). I know that $FUTU is always going to trade at a discount because the company is based in Hong Kong and there’s a China risk premium despite using very reputable law firms and auditors and early investors that include Tencent, Sequoia, Matrix and General Atlantic however even with the China risk premium it just makes no sense that a stock like $FUTU is trading at a massive discount to $IBKR despite growing revenues 8x faster and earnings 5x faster.

Why should $IBKR trade at 10x sales with 24% revenue growth when $FUTU trades at 14x sales with 182% revenue growth and net income margins of 50% versus 10% for $IBKR.

$IBKR is a great company (I actually use them as my primary trading platform) but the discount that $FUTU is currently getting in the market is absurd. Obviously I’m expecting growth to slow down for $FUTU (otherwise I’d be looking for 300-400% YoY growth instead of 182% YoY growth) but even if growth ticks down a little bit over the next three quarters it won’t have a meaningful impact on $FUTU’s 80% gross margins or 52% net income margins.

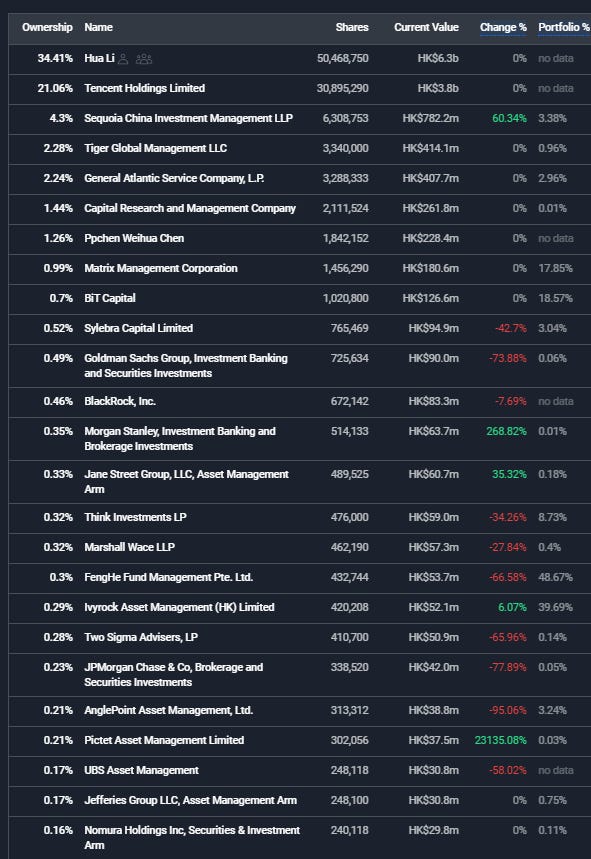

As you can see $FUTU still has strong ownership from early investors and institutions:

It’s also worth noting that “fund ownership” has increased nearly 10x over the past year including a very meaningful increase over the past two quarters.

TECHNICALS:

$FUTU tested the 100d EMA this morning and bounced off. Over the past few months $FUTU has bounce off $100 a couple times. I’d love to see $FUTU close above the 50d MA’s because then we should have clear skies until we get into the high $170s and run into potential resistance from the April highs.

Over the next 4-6 months I think $FUTU has 20% downside ($100 support) and 80-100% upside ($225-250 price target). $FUTU actually rallied to $205 back in February however the fundamentals, business model and balance sheet are even stronger now than they were three months ago so I am very confident $FUTU goes back to $200+ in the next 6 months and I think there’s a good chance we see $FUTU at $250-300 in the next 12-18 months especially after we see the numbers from Robinhood which should make the current valuation of $FUTU look even more compelling for investors.

CONCLUSION:

I do think investors are somewhat nervous about owning Chinese companies which is understandable. We’ve seen some frauds over the years however US companies have also had their fair share. Right now $FUTU is the only Chinese company that I own, partly because I want to limit my risk to Chinese companies but also because there’s no other company in China with numbers even remotely as strong as $FUTU. I also feel better owning $FUTU knowing they are audited by PricewaterhouseCoopers plus their largest outside investor is Tencent and several of the highest quality VC firms are their early investors and several well known mutual funds and hedge funds are building positions in the company after weeks or even months of due diligence and calls/meetings with management.

I’ve actually spoken to $FUTU SVP of Marketing to learn more about their international expansion plans and early next month I’m interviewing the CFO of $FUTU for my YouTube channel.

$FUTU remains one of my largest positions and highest conviction stocks for the next 6-12 months. There’s no doubt if $FUTU was a U.S. based company reporting these insane metrics the market cap would be at least $50-60 billion.

I do believe $FUTU deserves a “China risk premium” but not a 70% discount based on where it could be trading on the fundamentals alone. Despite being up 170% YTD, I believe $124 is an attractive entry price for investors so if you missed $FUTU at $42 after my first writeup, I believe you still have a chance to get in and make some money.

If I’m right and $FUTU finally gets the credit they deserve for putting up these insane growth numbers while maintaining incredible profit margins then $FUTU could have tremendous upside in the coming months.

I hope you enjoyed this update on $FUTU — if you have any questions on $FUTU please let me know.

Regards,

Jonah Lupton