Update on $DMTK (DermTech)

Update on $DMTK (DermTech)

In full disclosure $DMTK is still one of my largest positions and I remain extremely bullish on this company for the next 5-10 years. I was not expecting any blowout numbers when $DMTK reported 2021 Q1 earnings last Thursday but they were better than expected plus the CEO had some very positive comments on the earnings call which I’ll discuss in this writeup.

Website: DermTech.com

$DMTK Investor Relations [click here]

2021 Q1 Earnings Report [click here]

2021 Q1 Earnings Call [click here]

2021 Q1 Earnings Call Transcript [click here]

2021 Q1 Form 10-Q | Quarterly Report [click here]

2021 Q1 Investor Presentation [click here]

DermTech patient handout [click here]

DermTech sample collection [watch here]

$DMTK to present at UBS Global Healthcare Conference on May 24th [click here]

My writeup on $DMTK from January: https://jonahlupton.substack.com/p/dmtk-dermtech-ee2

My interview with $DMTK’s CEO John Dobak in March 2021

OVERVIEW:

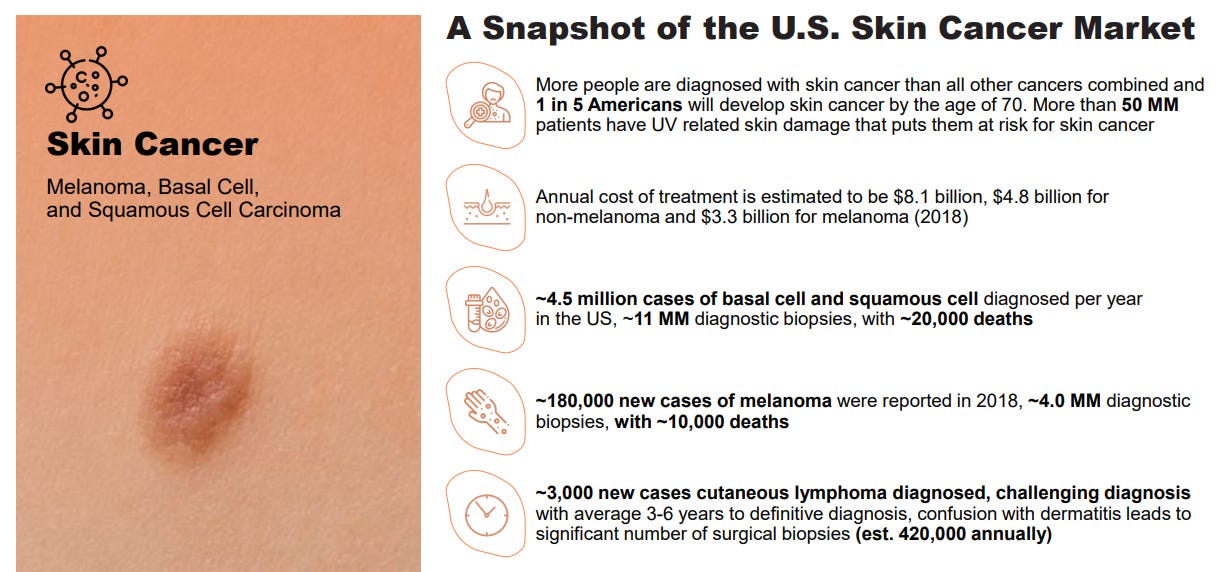

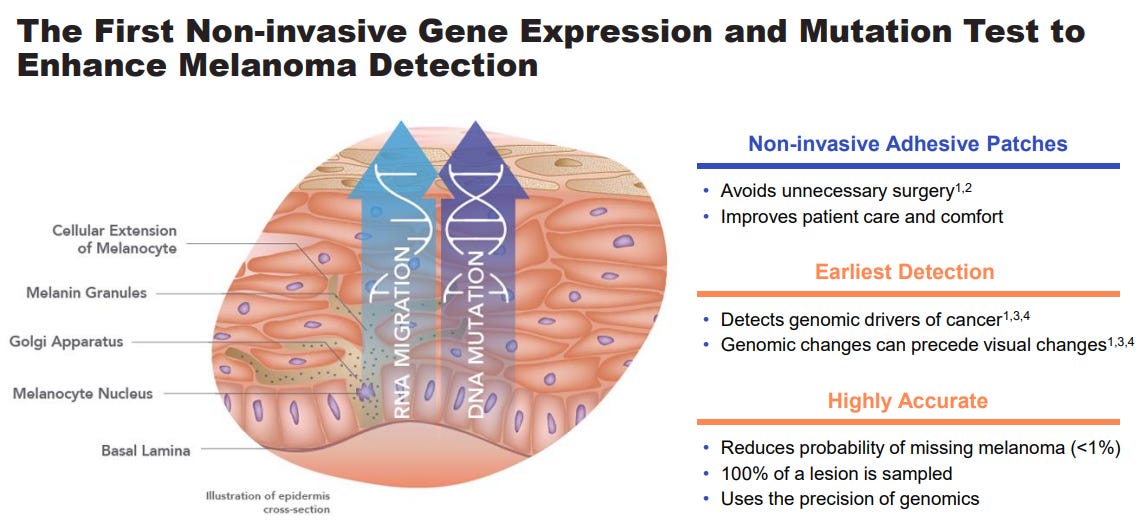

$DMTK is a precision dermatology company that created a genomics based non-invasive smart patch/sticker for early melanoma detection.

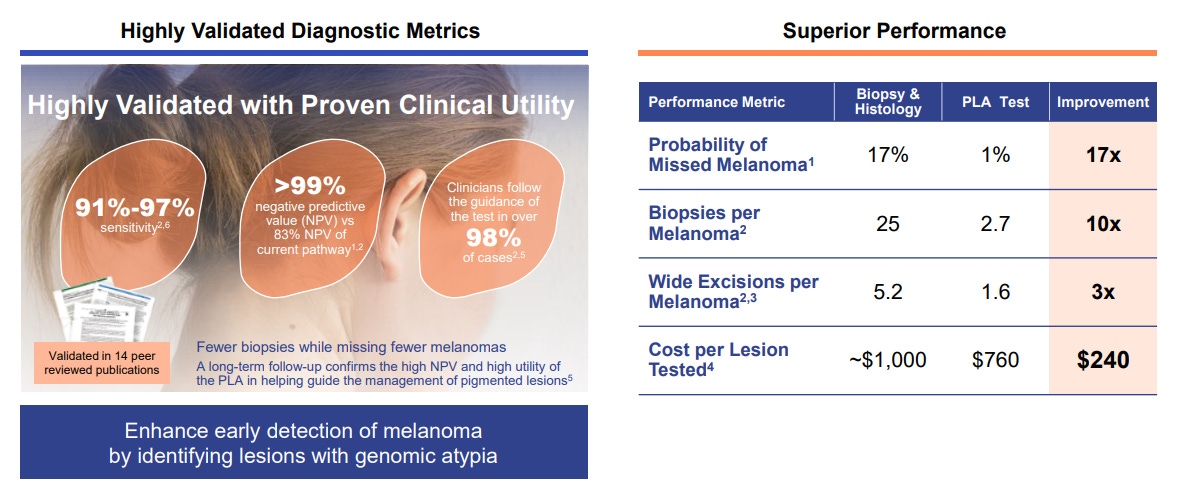

Skin cancer is the most common form of cancer and melanoma is the most deadly however the survival rate when caught early is close to 99%. This is why it’s so important for people to take care of their skin, get regular checkups and for the Dermatology industry adopt new technologies and standards like the $DMTK smart patch/sticker.

Every year there are 4+ million biopsies for potential melanoma and 15+ million for basal and squamous cell cancer. Since more than 90% of these biopsies come back negative it’s fair to say they turned out to be unnecessary and this is where $DMTK can play an important role for Dermatologists and patients. Let’s use the sticker before the scalpel.

Q1 RESULTS:

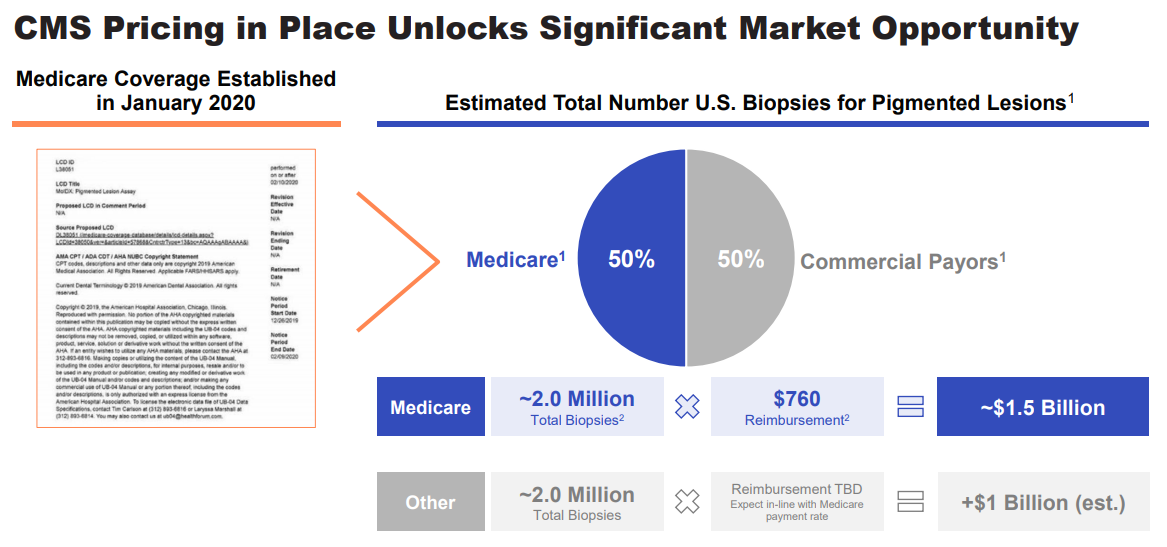

$DMTK reported strong Q1 numbers despite all the headwinds of the pandemic. Billable sample volume was up 62% YoY which was great but the more important number, assay revenue was up 175% YoY and 40% QoQ. The assay revenue is the PLA product that we’re all familiar with now for early Melanoma detection. Assay revenues were $2.2 million and sample volume was 9,400 for an ASP (average selling price) of $234. As more commercial payors ie private health insurance companies begin to support $DMTK’s patches we should see ASP continue to increase.

Q1 also included commercial payor contracts with Blue Cross Blue Shield of California, Texas and Illinois. There are 36 different BCBS organizations representing 106 million Americans and I think it’s only a matter of time before many of them begin supporting $DMTK [click here for more facts about BCBS]

Total revenues for the quarter were $2.5 million which were higher than expectations. We didn’t get any 2021 guidance which isn’t surprising.

Gross margins for Q1 were 21% however assay gross margins were only 10%. Both sound low (and they are) but these gross margins will increase dramatically over the next couple years with more volumes. I like to compare $DMTK right now to $EXAS (Exact Sciences) in the early days when their gross margins were also very low and today they are around 75% — this is where I think $DMTK can get to within 5-6 years.

During Q1 $DMTK raised $213 million from a secondary offering plus the exercise of outstanding warrants so the company’s cash balance is now $258 million. I believe this puts them in a very strong financial position so we probably should not see any new stock offerings anytime soon despite the quarterly operating losses. Right now these losses are justified and attributed to everything from hiring to sales & marketing to research & development. $DMTK has an opportunity to build a $10+ billion company over the next 5-6 years so they should be investing in growth every chance they get. They need to be moving as quickly as possible to build a category leading company and defend against any potential competitors.

PIPELINE:

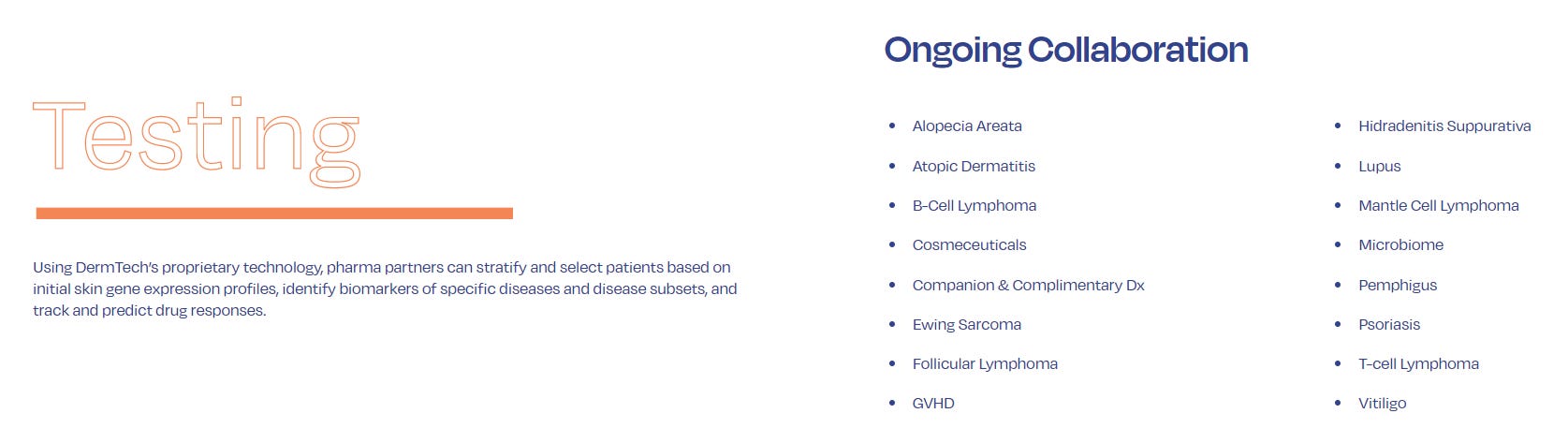

The first half of 2021 is all about PLA and PLA+ at $DMTK however as we get into the second half of this year we’ll start to focus on the next two products coming to market. PLA+ launched recently and contains an extra bio-marker that makes the patch even more accurate at detecting melanoma.

Based on Dr. Dobak’s (CEO of $DMTK) comments on the Q1 earnings call it sounds like Luminate should be coming in Q4 and Carcinome should be coming in the first half of 2022. Both of these products have tremendous upside for $DMTK as well as Dermatologists, PCP’s (primary care physicians) and the patients.

$DMTK still believes Luminate and Carcinome are the two biggest drivers for tapping into this $10 billion market opportunity called “precision dermatology”. I’m also hearing more and more about $DMTK testing tele-medicine which might be the ideal way to launch Luminate along with PCP’s. I suspect will hear more about $DMTK tele-medicine plans in the coming months.

Right now your dermatologist can order the $DMTK PLA test through a telehealth visit but I wonder if $DMTK will take it a step further. I just don’t want to make any guesses until we get more guidance from $DMTK.

RESEARCH PARTNERSHIPS:

In my interview with Dr. Dobak he explained that $DMTK was building a skin genomics platform which would include massive amounts of valuable data that biotech, pharmaceutical, healthcare and skincare companies would love to use to develop better drugs, products and topicals.

I suspect we’ll start to hear more about these partnerships in the coming months.

There are dozens of skin diseases besides cancer that $DMTK could address in the future with their genomics patches. PLA/PLA+ is just the first one. This is why I like to say the $DMTK story for shareholders is still in the top of the first inning. We need to be patient and allow this story to unfold in the coming years. If we are correct in our thesis around precision dermatology and the numerous uses for non-invasive patches then there’s no reason why $DMTK can’t be a $30 or $40 billion company by the end of this decade. Unfortunately skin cancer is not going away and there’s a good chance the # of annual cases worldwide will just continue to increase which means the opportunity for $DMTK and shareholders is quite large.

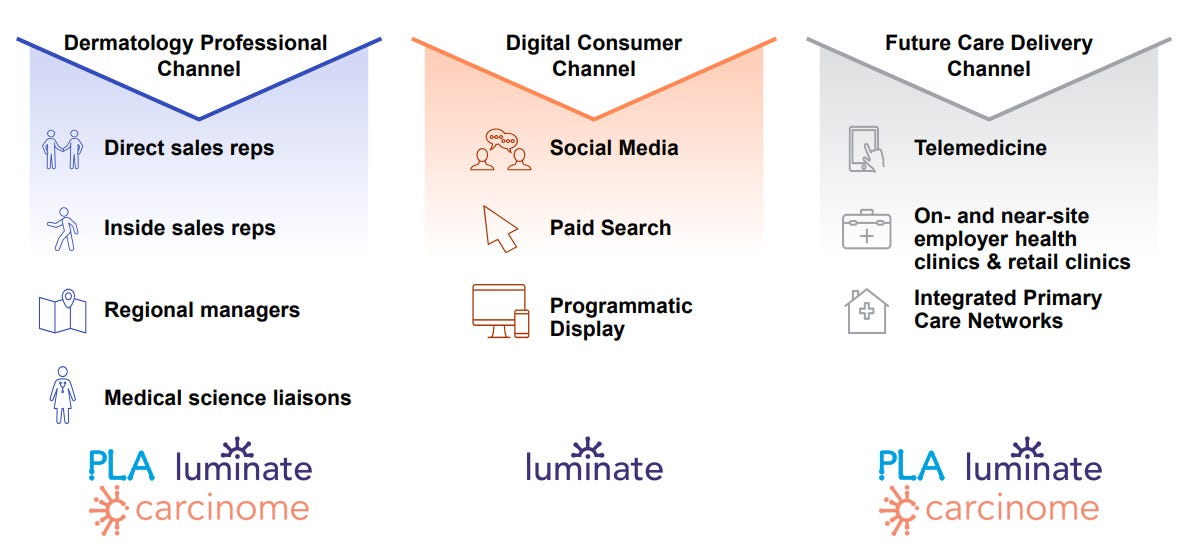

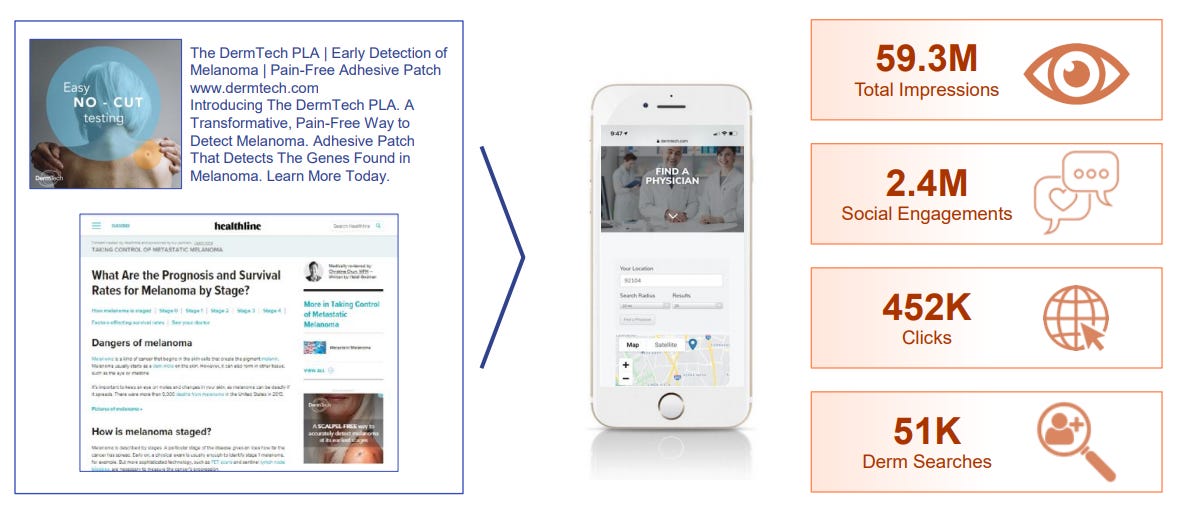

SALES & MARKETING:

$DMTK continues to expand the sales team in order to target the largest and most active Dermatology offices/centers in the country.

Based on recent comments from the CFO on the earnings call, it sounds like their marketing/branding efforts have been going well, especially when driving traffic to “Find a Specialist” on their website.

I believe we’ll see a large increase in marketing spend in Q3 as we approach the launch of Luminate.

FINANCIALS:

The chart below shows the current estimates from analyst for $DMTK revenues for both quarterly and annual.

I believe these estimates are too low and full year 2021 revenues will be closer to 200% YoY growth (especially if Luminate launches in Q4) but more importantly I believe 2022 estimates are way too low because next year we’ll have PLA + Luminate + Carcinome.

Based on my 5-year financial projections I have $DMTK doing $18 million in 2021, $45 million in 2022 and $750+ million by 2026. These are aggressive projections and only time will tell but that’s why I included the chart below which is the revenue numbers from $EXAS over the past 6+ years where you can see they went from $1.8 million in 2014 to $1.49 billion in 2021.

CHARTS:

As you can see from this chart, the past few months for $DMTK since my original writeup have been very volatile. The stock zoomed from $40 up to $80+ and now over the past 10 weeks the stock has pulled back more than 50%. Last Thursday $DMTK actually dipped below $30 which was painful for long term investors like me but I continued to add to my position. Then on Friday, as the stock bounced off the 200 day moving average plus the strong Q1 earnings report $DMTK was up more than 15% on Friday. Not only is this a strong bounce off the 200d but I think there’s a lot of enthusiasm for $DMTK based on the CEO’s comments from the Q1 earnings call with regards to commercial payors plus the pipeline plus some strategic partnerships. I think investors are regaining confidence in what $DMTK could be someday.

This chart below is $EXAS over the past 5 years. As you can see the stock was up 30x over the past 5 years before the recent pullback but even with the recent 35% pullback $EXAS is still up 20x over the past 5 years. This gives you an idea of what is possible for $DMTK if they continue to live up to our expectations and gain significant traction with Luminate and Carcinome.

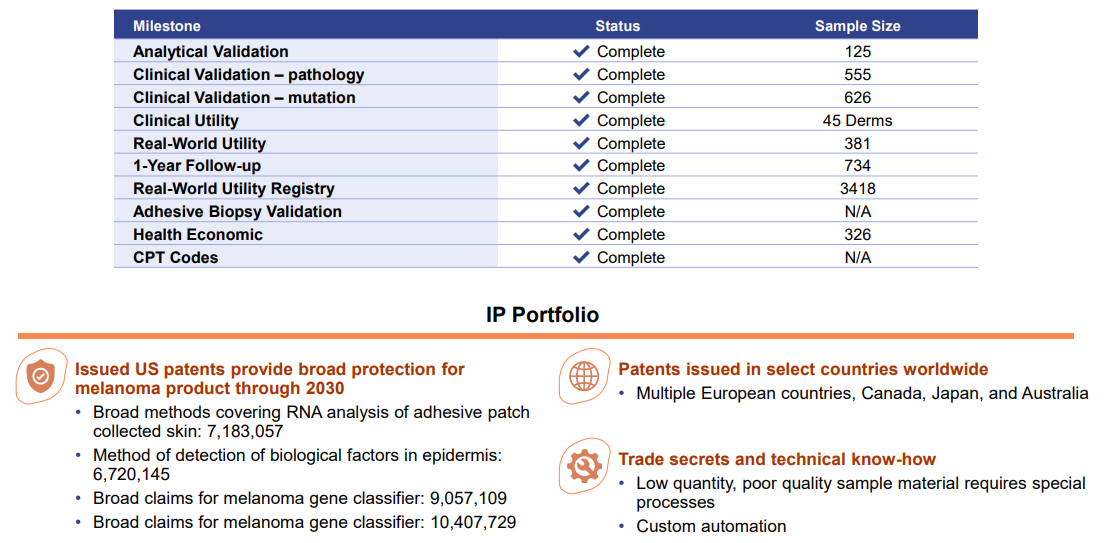

INTELLECTUAL PROPERTY:

$DMTK continues to expand their IP portfolio as they increase their R&D efforts and build their product pipeline.

Here are all the $DMTK patents issued [click here]

Here are all the $DMTK patents filed [click here]

MANAGEMENT:

Management team still very strong, there’s been a couple insiders selling shares but they were mostly minor sales and nothing that concerns me. Given all the headwinds of the pandemic, the $DMTK team has executed very well and I believe that will continue to do so.

CONCLUSION:

$DMTK continues to be one of my favorite companies for the next 5+ years. I’m assuming most of my subscribers know by now that I’m focused on finding companies that I believe can 5x over the next 5 years (38% annualized return) and then owning 15-30 of them.

I am very confident that $DMTK will be one of my companies that will 5x over the next 5 years and if they’re able to reach $750+ million by 2026 then I think there’s a good chance $DMTK becomes a 10-bagger over the next 5 years.

I have no idea where $DMTK’s stock price goes in the short term but I’m not worried. If the stock stays in the $30s I’ll continue to increase my position.

I was bullish about $DMTK back in January when I first heard about the company and TBH I’m ever more bullish now especially after listening to the Q1 earnings call three times.

I highly recommend everyone listen to the call or read the transcript because it’s clear the CEO is very excited about what his team is doing and the opportunity in front of them.

Investing is growth companies can be hard but it gets a little easier when you find a company like $DMTK that is not only trying to save/improve lives but has the potential to deliver insane returns for shareholders.

I hope you enjoyed this update on $DMTK — feel free to reach out with any questions.

Regards,

Jonah Lupton