Update on $ATER (Aterian)

On April 29th, 2021 Mohawk ($MWK) changed their name to Aterian ($ATER)

Website: Aterian

Press release on name change [click here]

2021 Q1 Earnings Report [click here]

2021 Q1 Earnings Call [listen here]

2021 Q1 Investor Presentation [click here]

Form 10-Q, filed May 11th [click here]

Form 8-K, filed May 14th [click here]

INTRODUCTION:

Back on December 21st, 2020 I did a Substack writeup on $MWK at $12.50 because it was clear to me this company was extremely undervalued.

You can read that writeup here: https://jonahlupton.substack.com/p/jonahs-growth-stock-ideas-mwk

Over the next 2 months $MWK went up 4x from the $12 range all the way to $48 and then from late March until mid-May the stock dropped all the way about to $12. I’ve been around the investment industry for 2 decades and I can probably count on one hand how many times I’ve seen this happen. $MWK was undervalued at $12, overvalued at $48 and now undervalued again at $13.

Here’s my interview from mid-March with the Yaniv Sarig, Founder and CEO of $ATER (formerly $MWK)

OVERVIEW:

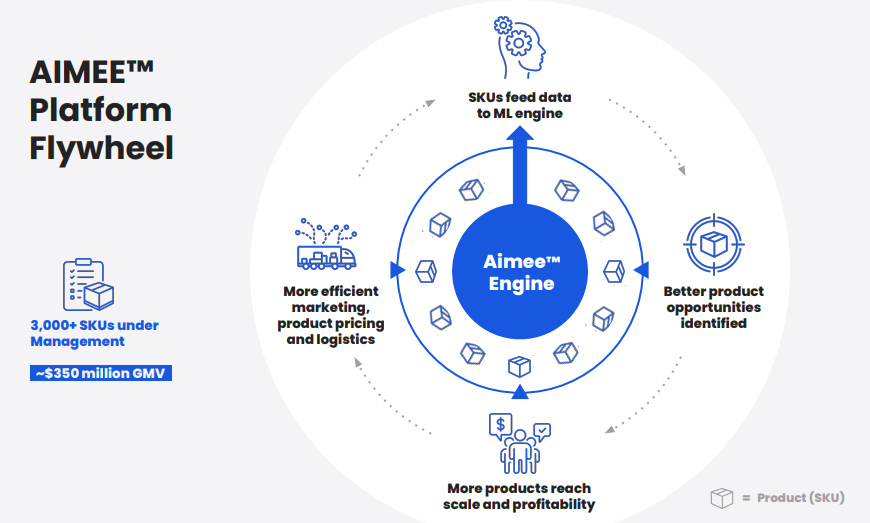

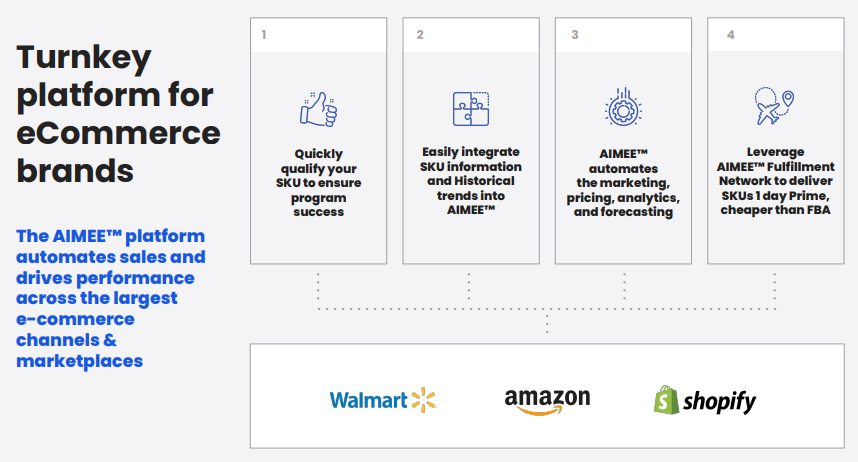

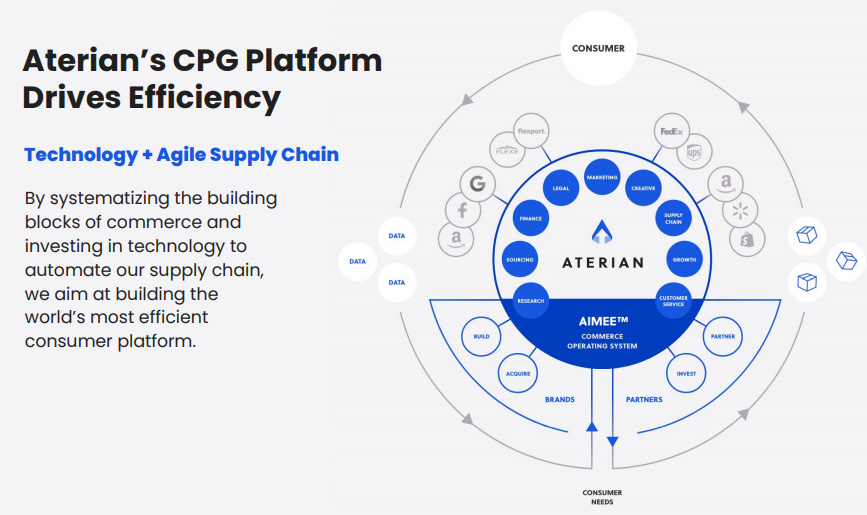

$ATER is a tech-enabled CPG company (consumer packaged goods) using their proprietary AI software called AIMEE (AI marketplace ecommerce engine) in 5 different ways:

BUILD: use AIMEE to maximize growth of existing brands across different marketplaces as well as identify category opportunities then leverage their agile supply chain to create and launch new brands

ACQUIRE: use AIMEE to identify acqusition targets, then acquire other brands with strong product portfolio and marketplace track record at accretive multiples

There’s also a great opportunity for $ATER to expand their existing brands and acquired brands across multiple marketplaces including international expansion opportunities.

PARTNER: generate revenues by allowing other ecommerce brands to use AIMEE as a SaaS product thus enabling them to better manage their supply chain, marketing channels, ad spend, inventory levels, etc.

2021 Q1 EARNINGS:

$ATER posted very strong Q1 numbers — revenues grew 88% YoY to $48.1 millions. The company has already stated they lost $6 million in revenues in Q1 from low inventories due to disrupted supply chains and backups at the shipping ports.

One of the most surprising numbers in the Q1 report was gross margins improved from 40.2% in 2020 Q1 to 54.1% in 2021 Q1. This is a massive increase in gross margins and goes to show how efficient the $ATER business model really is. One of the reasons that I want $ATER to continue doing acquisitions is because they are so good at eliminating costs and increasing operating margins. There aren’t many CPG companies with gross margins in the mid 50s, this is quite an accomplishment for $ATER.

Operating losses increased in Q1 however this was due to non-cash related expenses such as stock compensation, earn outs and warrants.

Contribution margin improved to 12.7% in 2021 Q1 from -2.9% in 2021 Q1.

My next favorite metric after the improvement in gross margins was that fixed operating expenses as a percentage of net revenues decreased from 22.3% in 2020 Q1 to 17.5% in 2021 Q1. Once again this goes to show the operational efficiencies coming out of $ATER and how they’re able to acquire proven ecommerce brands and eliminate 80% of the fixed costs. This is why accretive acquisitions make so much sense, especially if $ATER is able to lander a bigger cheaper credit facility from a Tier 1 bank — with cheaper debt they can keep buying companies at 5x earnings then chop out 80% of the fixed costs thus expanding their operating margins (EBITDA) and dropping more of those gross profits to the bottom line as free cash flow.

2021 FINANCIAL GUIDANCE:

Back a couple months when $ATER (then $MWK) reported Q4 earnings they issued full year 2021 guidance of $360 million in revenues and $31 million of EBITDA. Since the core business is still showing nice growth and $ATER announced the acquisition of Squatty Potty, they have raised 2021 guidance to $360-390 million and $30-34 million of EBITDA.

Assuming they come in at the midpoint of that revenue guidance, $375 million would be 102.5% YoY revenue growth from 2020 when they did $185 million. I know that $ATER has issued more shares for these recent acquisitions but after the recent selloff of $ATER from $48 to $12 and having this revenue guidance to work with it means $ATER is now trading at approximately 1.1x 2021 sales (using market cap) and approximately 1.3x 2021 EV/Sales. This is simply way too cheap for a company growing top line revenues at 100% YoY with 54% gross margins and $30-34 million of EBITDA.

In December 2020 $MWK (now $ATER) acquired SMASH which includes brands such as Mueller, Pursteam, Pohl and Schmitt, and Spiralizer [click here for more details]. Now, if you look at the recent 8-K filing [click here] from last week it’s clear these brands were growing at 127.6% YoY with 66.4% gross margins at the time of acquisition. These metrics are both better than anyone was expecting to see.

We can also see that operating margins at SMASH were on the high side (47.8%) and I believe $ATER will continue to reduce fixed costs, leading to an improvement in operating margins and therefore higher earnings going forward from this deal.

ANALYSTS:

Brian Nagel, the $ATER analyst from Oppenheimer reiterated his buy recommendation on May 11th with a $50 price target. Usually when a stock drops 50% or more you see the analysts all lowering their price targets but not with Brian and $ATER, he’s standing firm with his analysis which I love to see. Finally an analyst with a spine :)

SHORT SQUEEZE:

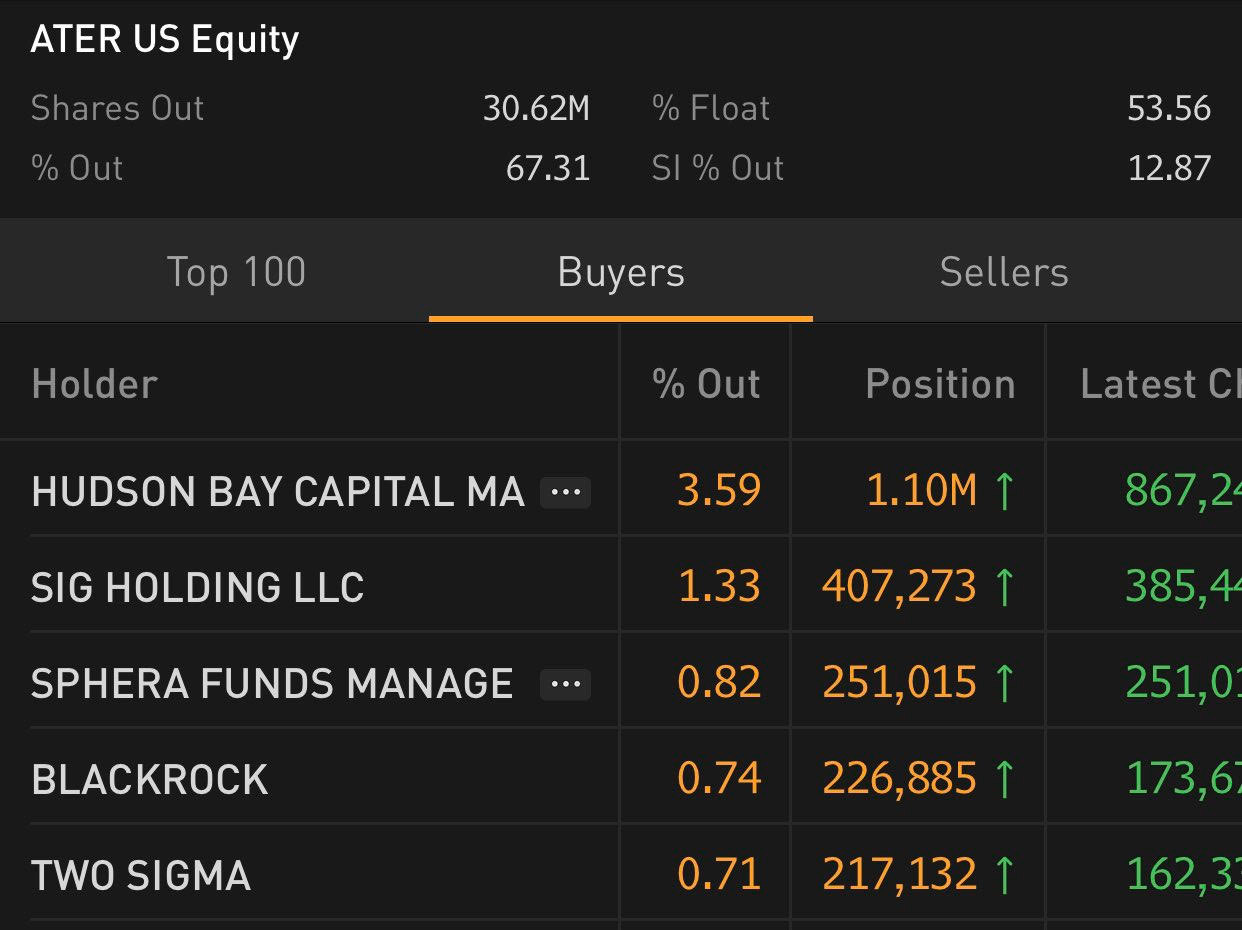

I’m not saying we’re going to get a short squeeze in $ATER but it’s always a possibility since when we know the float for $ATER is very low because so much stock is owned by founders, insiders and recent acquisition targets. I can also see the short interest for $ATER is around 20% depending on which data service I look at — I believe there’s 4-5 million shares now short with shares outstanding around 31 million and the float at least 30% lower which means it’s possible the short interest is 25-30%.

We also found out last week that Hudson Bay Capital (a very large hedge fund) has increased their position in $ATER by 373% which means they now own 1.1 million shares and 3.59% of the company. Clearly a hedge fund as large as Hudson bay could increase this stake at any time, drive the price higher and possibly force the shorts to start covering their positions.

This information was made public on Friday, May 14th which is probably why $ATER was trading up 30% in the after hours session on Friday afternoon. Not sure if this was funds buying or shorts covering but it shows that someone really wanted to buy some stock before this week.

I would love to see Hudson Bay continue buying $ATER shares and at these prices it would not surprise me.

Today we found out that several other hedge funds have also started acquiring shares in $ATER including Two Sigma which is one of the largest hedge funds on the planet. This is pretty big news for $ATER. I would not want to be a short in $ATER knowing that several of the largest hedge funds in the U.S. are starting to building positions in the company.

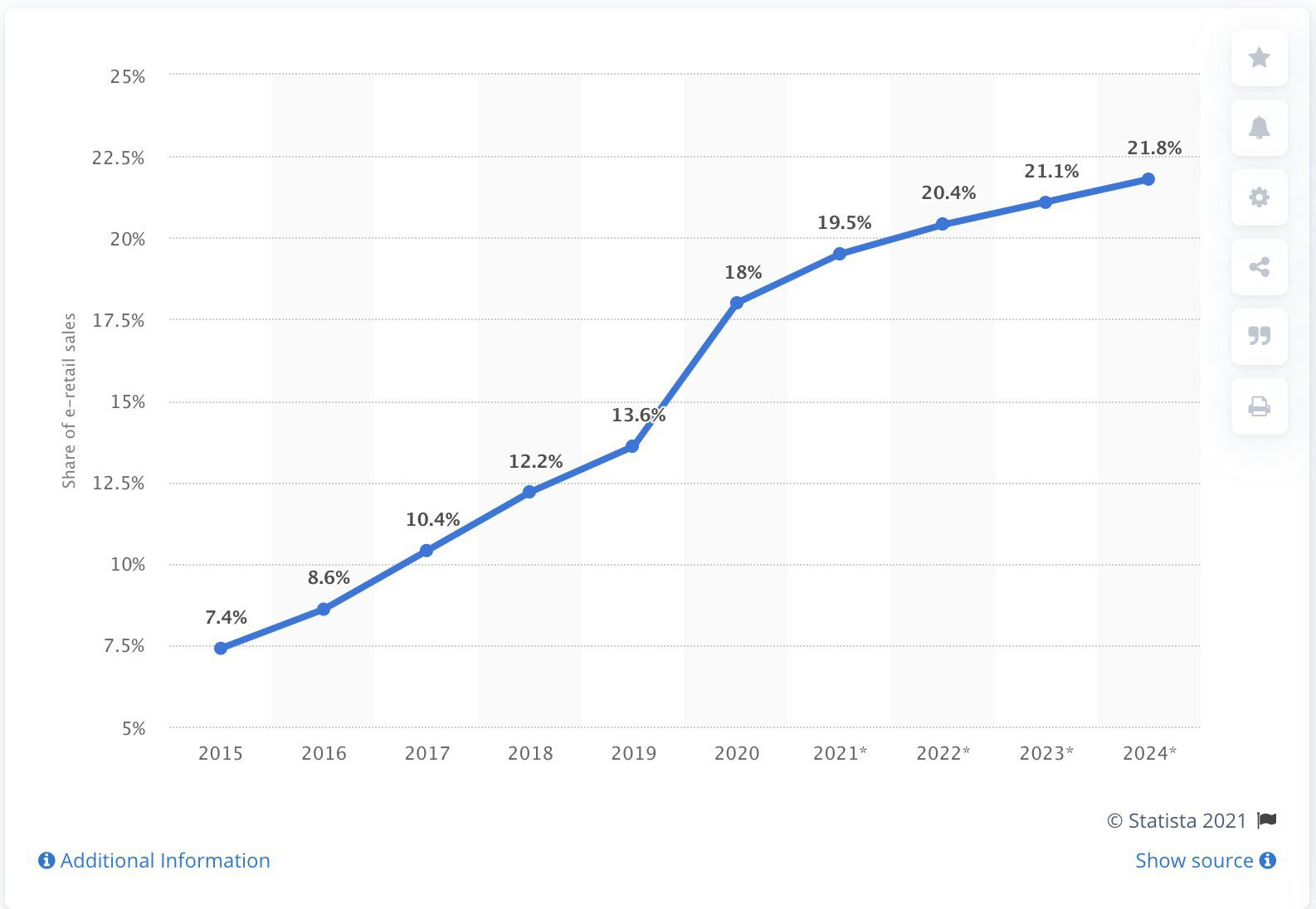

E-COMMERCE:

Even though the pandemic is coming to end, the ecommerce penetration is still accelerating which is one reason I remain bullish on $ATER. Even though the overwhelming majority of their revenues are coming from Amazon, they are expanding onto the Walmart and Target marketplaces as well as beginning international expansion. It sounds like Amazon Europe is where $ATER is headed next.

FINANCIALS:

I mentioned the financials earlier but here are the annual numbers first and the quarterly numbers second.

1st: I think the 2022 annual revenue/EBITDA estimates are way too low, I don’t see any chance that $ATER only grows 27.7%, that would require a tremendous slowdown in their existing brands plus no more acquisitions — both of which are very unlikely. If $ATER continues doing accretive acquisitions of ecommerce brands then I suspect next year we see 80-100% top line growth AGAIN with even better EBITDA margins, perhaps getting into double digits. Right now $ATER is sacrificing growth for profits and I’m fine with that, most of my portfolio companies are doing the same thing. If $ATER was a 30-year old mature CPG company like $PG and revenue growth was in the single digits then I’d expect profits, cash flow, dividends, buybacks, etc — $ATER is the opposite of this and that’s what I expect from my potential multibaggers

As you can see in the 3/31/21 column, gross margins for $ATER in Q1 jumped to 54%, there’s no reason to think this number should decline meaningful in the coming quarters so keeping this number in the 50s should lead to better EBITDA through 2021 especially as they continue to incorporate those SMASH assets where we learned the gross margins are even better at 66%. Since this acquisition took place in 2020 Q4, it makes sense that $ATER would be starting to benefit from those higher metrics and now we get to see how much fixed cost reduction $ATER can squeeze out of those assets. If Yaniv and his team are able to reduce the fixed costs at SMASH by 80% (which is always their goal) then we could see another $10+ million of EBITDA which would bring 2021 EBITDA from current guidance of $30-34 million up to $40-44 million. In this scenario $ATER would be trading currently at less than 12x 2022 EV/EBITDA with 102% revenue growth and 54% gross margins.

This might be a little unfair because they are such different companies (although both CPG) but $PG (Procter & Gamble) is currently trading at 17x 2022 EV/EBITDA with 3.4% growth.

This goes to show the operational efficiencies of $ATER’s business model. If you listened to the Q1 earnings call you’ll hear the CEO talk about revenues per employees, this is a metric they take alot of pride in. He estimated that right now the revenues per employees is around $1.2 million however their goal by year end is $1.4 million. This is incredible and proves how good they are at doing acquisitions and integrating all those new products while still reducing costs. Not to pick on $PG but they are around $700,000 revenues per employee and they’ve been around for 100 years.

CONCLUSION:

I will continue to reiterate that I’m looking for companies that can 5x within 5 years. After this pullback from $48 to $13 there’s no doubt in my mind that $ATER will accomplish this which means the market cap would only need to reach $2 billion over the next 5 years. This seems very feasible for a company that is operating in one of the largest TAM’s in the world (e-commerce) and doing a great job of executing on their triple-threat strategy: BUILD, ACQUIRE, PARTNER

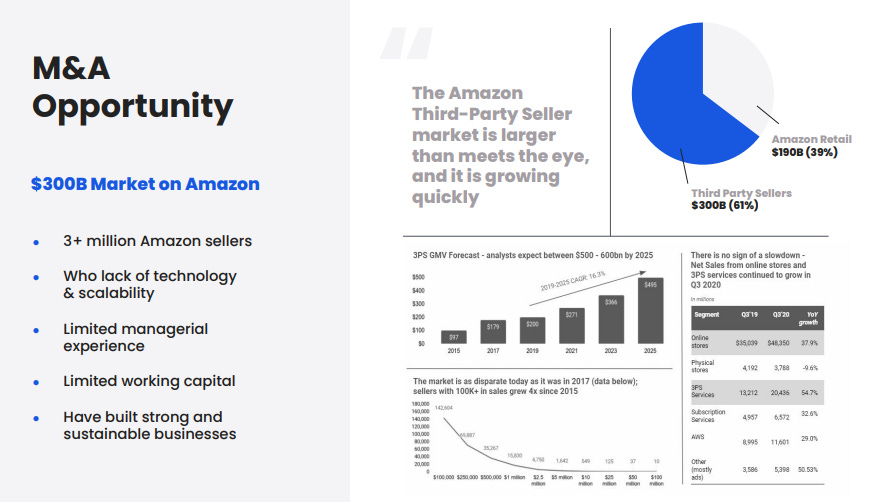

According to independent research there are approximately 6 million third-party sellers on Amazon. It’s true there are several companies now copying $ATER and doing a rollup of Amazon FBA brands but there’s literally millions of these e-commerce companies that could/should be acquired over the next decade.

As $ATER has shown us, many of these smaller ecommerce brands have great products with strong reviews but they are being run very inefficiently as they try to compete across multiple marketplaces. $ATER have become experts and scaling/managing brands so it just makes more sense for many of these small brands (most of which are owned by individuals, families, or friends) to finally sellout and get some liquidity.

One of the things that has hurt $ATER over the past couple months (besides a ridiculous short report full of lies) was when $ATER announced they were refinancing their existing debt at 8% plus warrants. This was a little expensive given the low rate environment we’re in and the cheaper rates that bigger companies are able to get.

On the Q1 earnings call Yaniv did disclose they are in discussions with multiple Tier 1 banks about a bigger, cheaper credit facility that would allow them to retire the existing debt and have a much cheaper cost of capital to go out and do accretive acquisitions with.

In the recent acquisition of Squatty Potty they are paying a total of approximately $28 million for $5 million of earnings however knowing that $ATER is so good at eliminating fixed costs, I believe $ATER can squeeze another $2 million of costs out of Squatty Potty thus increasing those earnings to $7 million. If we divide $28 million by $7 million we get an earnings yield of 25%. If $ATER is able to get a bigger, cheaper credit facility at 5-6% then it makes all the sense in the world to keep doing accretive acquisitions with a 20-30% earnings yield. This is exactly how companies should be using debt = ACCRETIVE GROWTH

I like to say that $ATER is a publicly traded CPG private equity fund because that’s definitely a big part of their current growth strategy and I like it. Throw in 30-40% annual growth from existing brands (proprietary & acquired) and some licensing/fee revenues from AIMEE and you have a company that should be able to sustain at least 50% revenue growth for the foreseeable future; perhaps the next decade or longer.

Before I wrap up I’m going to make a wild prediction knowing that I could very much be wrong but it’s fun to think about these things. I recently finished the book “100 Baggers” for a second time [click here to order the book on Amazon or audio book on Audible] and I’ve been trying to put together a list of 10 companies that I believe could be 100-baggers over the next 20, 30, 40 years. As hard as it is to find these companies, it’s probably even harder to hold them for that long without selling to lock in profits in a downturn.

Either way, I think $ATER is a potential 100-bagger. Of course a lot of things would have to go right but given the sustainable top line growth, expanding/enormous TAM, international expansion opportunities and extremely cheap valuation at the present time (which means possible multiple expansion in the future)… I do think there’s a remote possibility that $ATER could be a 100-bagger over the next 20+ years. If you run a formula in Google Sheets you’ll see that $ATER’s stock price would need to appreciate at a 26% CAGR over the next 20 years to become a 100-bagger from today’s prices. I know it’s unlikely since 100-baggers are almost impossible to find but it’s still something I felt the need to point out.

I hope this writeup on $ATER was helpful. I tried to include as much recent information as possible without overwhelming you. $ATER has definitely had a rough year however I remain very confident in this company for the next 3-5 years and maybe longer. I think they have a solid business model with multiple ways to drive growth and add shareholder value, now we just need to see if the team can continue executing at a high level. If they are able to deliver strong results then the stock price will take care of itself and shareholders will be very happy.

If you have any questions about $ATER please feel free to reach out.

Best regards,

Jonah Lupton