Deep dive on Uber ($UBER)

Deep dive on Uber ($UBER)

Company: Uber

Ticker: $UBER

Website: Uber.com

IPO date: May 9, 2019

IPO price: $45.00

Current stock price: $21.09

Outstanding shares: 1.963 billion

52 week high: $52.36 on June 28, 2021

52 week low: $20.89 on June 14, 2022

Market cap: $41.4 billion

Enterprise value: $43.7 billion

Headquarters: San Francisco, California, the United States

Number of employees: 29,000+

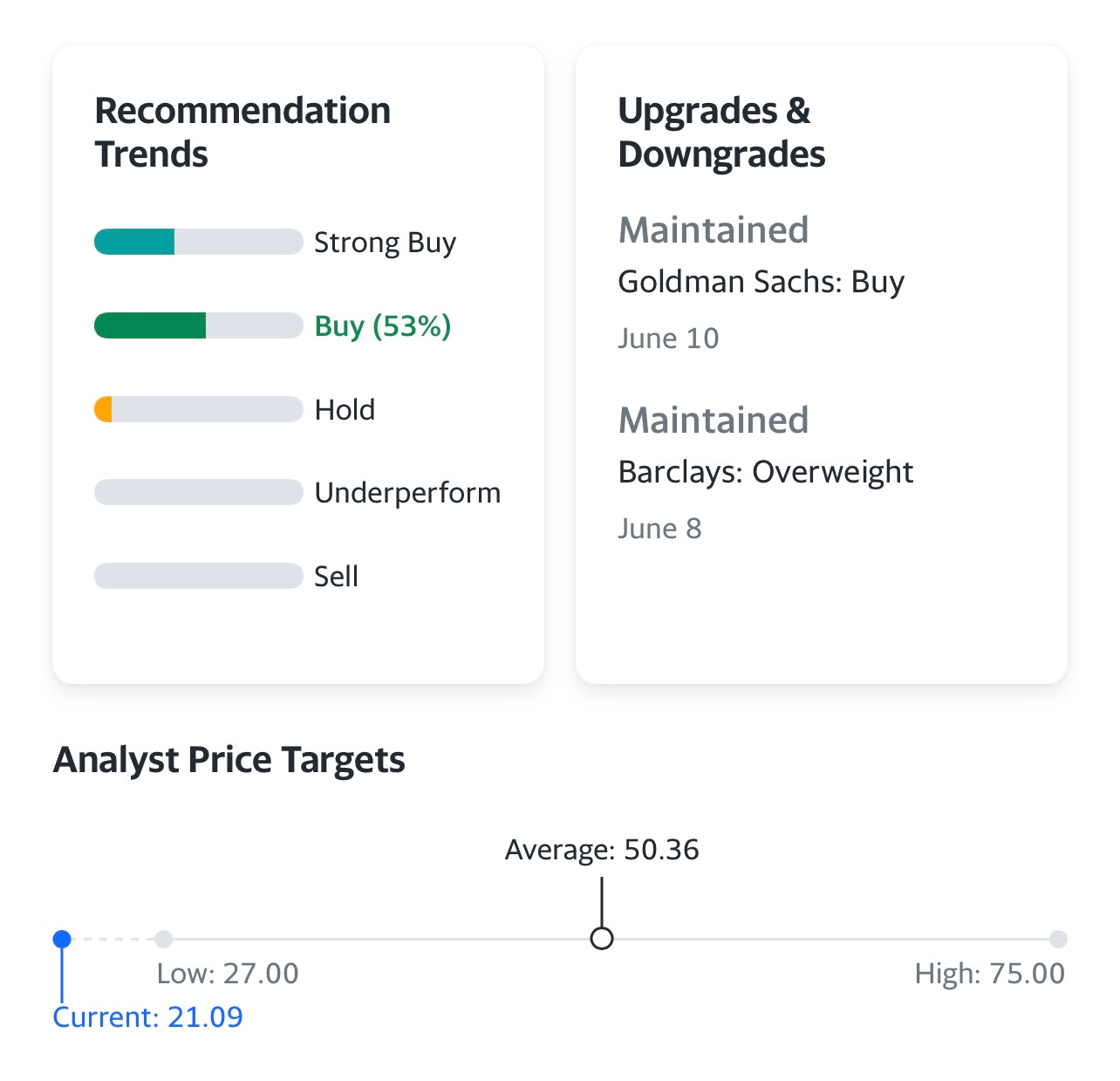

Average price target from analysts: $50.36

Investor Relations [click here]

2022 Q1 Earnings Report [click here]

2022 Q1 Earnings Call Transcript [click here]

2022 Q1 Earnings Call Presentation [click here]

Investor Day 2022 Report [click here]

2021 Annual Report [click here]

Outline

Introduction

Company Background

Opportunity / Technology / Customers

Business Model

Competitive Advantages

Management

Culture

Financials

Key Metrics

Risks

Ownership

Valuation

Investment Model

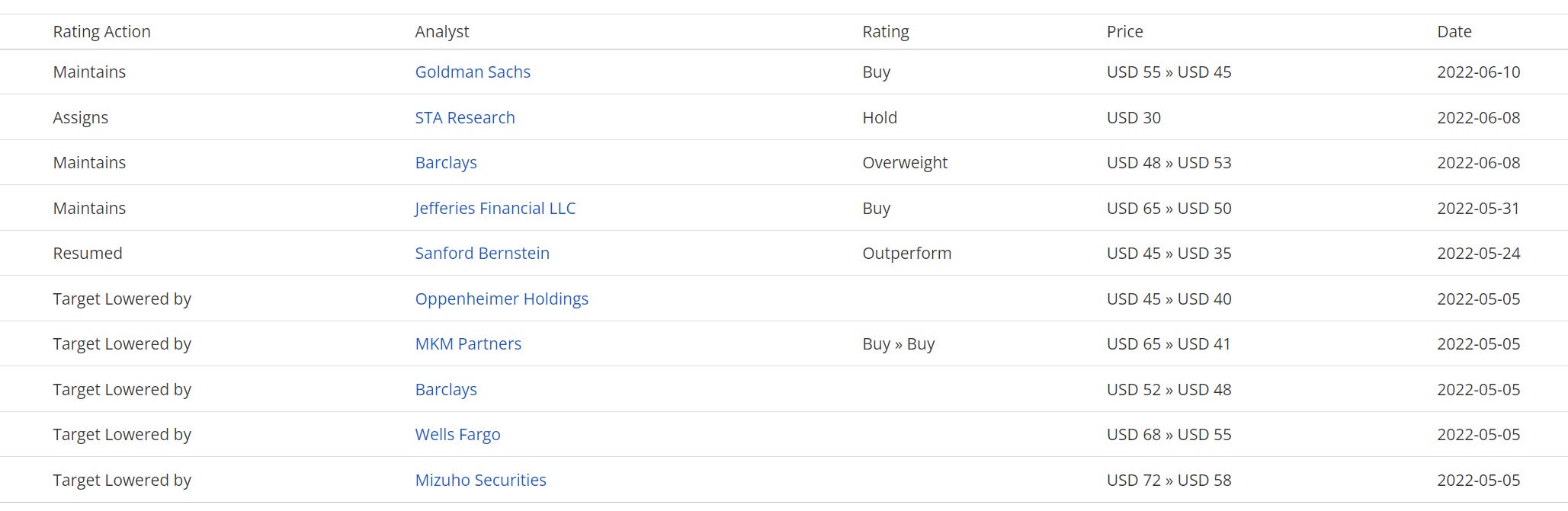

Analysts

Technicals

Conclusion

Introduction

Most of you reading this writeup are probably familiar with Uber as a company because you use their ridesharing or delivery services but now you’re going to learn about Uber, the publicly traded company which I believe has become a very attractive buying opportunity for investors.

In full disclosure I started buying Uber a couple months ago and was averaging down into the lows in early May and then we got a 25% rally in the stock so I setup some stop losses in case the technicals broke down which is exactly what happened so my position has been reduced from 4.25% to 3.0% but I’m planning to add to my position in the coming months once the broad markets find some stability which won’t be easy until Treasury yields stop going up and inflation starts coming down. Right now it’s macro that’s driving these markets, not the individual companies or their fundamentals — at least not until we get into Q2 earnings season.

As you’ll read in this writeup $UBER has really evolved over the past decade (but especially over the past 5 years) from a ridesharing company to a diversified global platform for mobility, delivery, freight, advertising, and much more. There are many reasons to be bullish on Uber for the next several years but several of the primary reasons for me are optionality, competitive advantages and the potential to generate massive amounts of free cash flow. Dara (the Uber CEO) certainly has a master plan and so far he’s done an impressive job of executing — even when the pandemic shut down their ridesharing business he was able to scale up their delivery business to help make up the difference and now two years later both business segments are crushing it.

There are growing fears that we’re heading into a recession which is supported by historical data meaning never before have we seen energy prices go up this much and inflation running this hot and not ended up with a recession. The bigger question is will it be a short, minor recession or a long, deep recession — I clearly don’t have the answer but I’m certainly voting for the first one. With that being said I do think Uber’s underlying business segments would hold up relatively well in a light recession assuming that travel demand (for personal and business) didn’t fall off a cliff since those rides to and from the airports are essential in more ways than one plus people on vacation are certainly high frequency riders unless they are renting a car which has gotten very expensive. I also think their delivery business would hold up relatively well in a light recession because it’s become a necessary convenience for many people that would not want to give up that luxury. On the other hand, if we end up with a long, deep recession then all bets are off and Uber will certainly suffer like many other companies that rely on the consumer and their spending habits.

Company Background

Uber's story began in late 2008 when two friends, Travis Kalanick and Garrett Camp, went to Paris to attend LeWeb, Europe's largest tech conference. Both were already successful entrepreneurs at that time, selling their respective companies for many millions (Kalanick sold Red Swoosh to Akamai Technologies for $19 million, and Camp sold StumbleUpon to eBay for $75 million).

As the story goes, the initial idea of Uber came on one snowy evening when the duo was trying to get a taxi after the conference. Back in the day, getting a cab on a snowy/rainy evening during the workweek was probably the most challenging time after Christmas and New Year. So entrepreneurs questioned themselves: "How does one get a cab on such evenings, and most importantly can you do it via your phone?"

At that time, there were various taxi services that one could call and request a car, but these services were slow and expensive, and for someone who does not speak the native language or does not know the city that well, if at all, it was hard and sometimes even impossible. Moreover, Kalanick and Camp were looking for not just a regular cab; they wanted to get a business type of car, a limo. That would require a special order in advance. So the initial idea was to create a mobile app for timeshare limo service.

After returning to San Francisco, the duo went in separate ways, but Camp decided to pursue this idea further as a side project. He called it UberCab. After working on the prototype for six months with two other friends, Camp decided to invite Kalanick to join him in getting this project to the next stage.

The first version of UberCab was soft-launched in early 2010 in New York with just three cars, and the official full launch of the service happened in May that year in San Francisco. Kalanick got so into this idea that he took over the CEO role in December 2010. That was the beginning of what is now known as Uber.

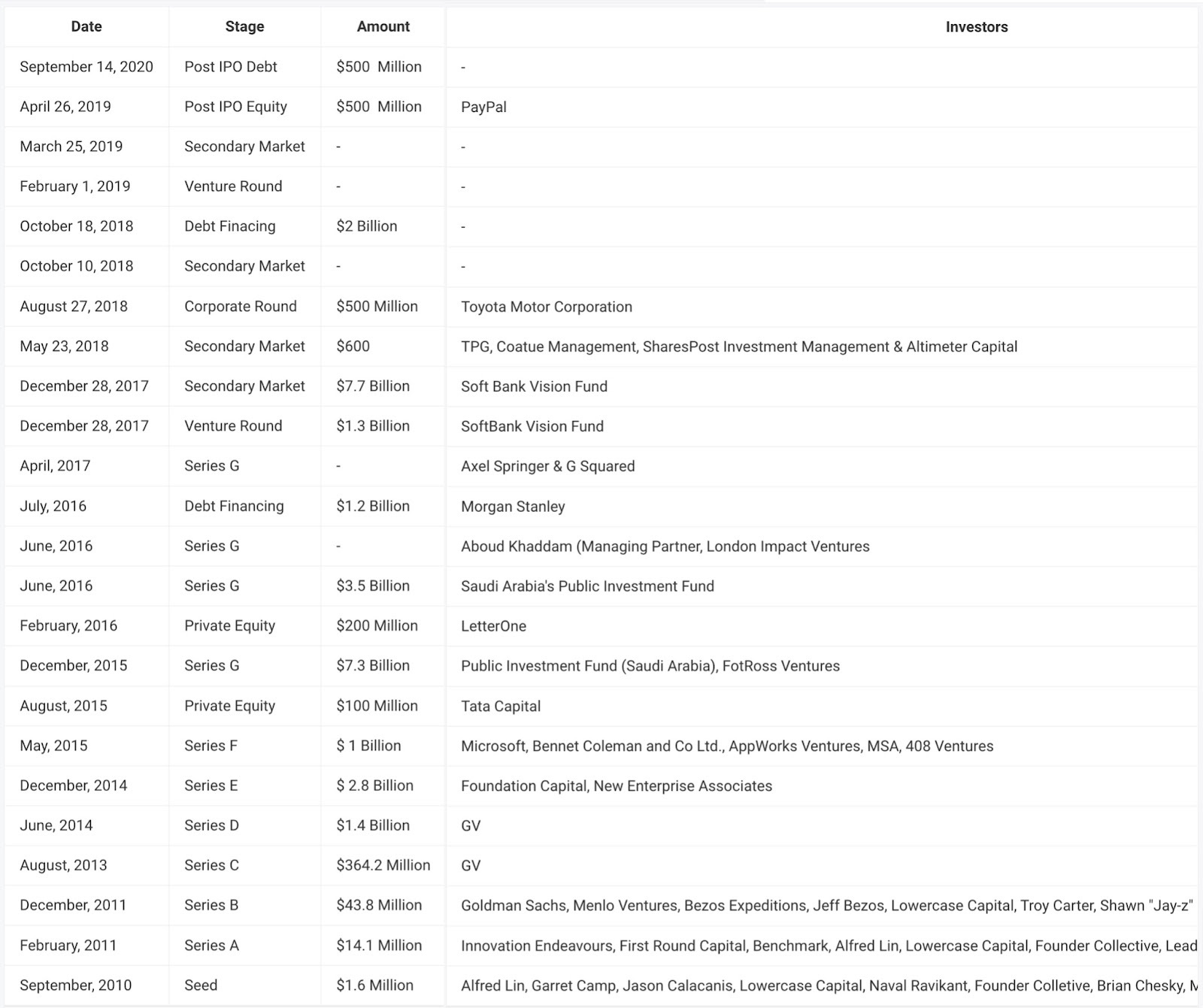

Uber started to gain traction with its easy-to-use interface, fast ordering, and convenient paying. The company very quickly attracted the attention of Silicon Valley's best investors. The very first investment the company received came straight after the launch: in September 2010, First Round Capital and a group of business angels, including Jason Calacanis, Naval Ravikant, and Brian Che sky, among others, invested $1.6 million in Uber. It was the beginning of one of many investment rounds. Looking a little bit ahead, in total, Uber raised a whopping 33 investment rounds, attracting $25.2 billion. Everyone wanted to have a piece of later to be the most valuable startup in the world.

Uber started to rapidly take not only the US but the rest of the world by storm. The company was revolutionizing (even disrupting) the way the world moves, and ‘Uber’ became a verb used by millions of people in different parts of the globe.

"This is the thing about changing the world. The world never wants to change. It's gonna dig in its heels and tell you no and try to crush you. Fortunately for us, we are in the world-changing business." – famously said Travis Kalanick.

Despite the monstrous growth and the status as one of the most disruptive companies of our generation, the company was constantly surrounded by various controversies, from surge price backlash to fair pay and drivers' benefits. But Uber, led by Kalanick, managed to get away with all of it… until February 2017.

A pivotal moment in the company's history happened on February 19, when the former employee published a blog post about Uber's culture. She alleged the company of having a corporate culture that was highly hostile, sexist, and offensive to most people. This blog post went viral overnight, and every media outlet was publishing excerpts from it.

As a result, a wave of resignation went through high-level Uber employees. The management was forced by the board of directors, led by now-famous Bill Gurley, a general partner at Benchmark, to start an internal investigation. The investigation resulted in almost 50 recommendations intended to improve the culture and work environment in the company, and additionally, another 20 employees were fired.

But that was just the beginning. More letters were released to the public, confirming that sexist attitudes came from the top down, including from Kalanick himself. He was also caught on the video arguing with one of the drivers about lowered fares. The board was fed and started to heavily pressure Kalanick, who eventually resigned on June 21, 2017.

Fixing the broken culture was given to Dara Khosrowshahi, who became the new CEO of Uber in August 2017. "The Board and the Executive Leadership Team are confident that Dara is the best person to lead Uber into the future, building world-class products, transforming cities, and adding value to the lives of drivers and riders around the world while continuously improving our culture and making Uber the best place to work." ~Uber PR team.

Dara Khosrowshahi came from Expedia, where he served as a CEO for a decade and under his leadership the company quadrupled their revenues.

Over the next 18 months, Khosrowshahi worked day and night to improve governance and board oversight, build a stronger and more cohesive management team, and make the changes necessary to ensure that the company culture rewards teamwork and encourages employees to commit for the long term.

Fixing most but not all problems, Khosrowshahi led the company to a blockbuster IPO, which eventually turned out to be a flop. The company went public on May 9, 2019, at an $82.4 billion valuation and an opening price of $45 per share. Everyone expected the price to skyrocket, but it closed down 7.6% from the IPO price. Nevertheless, the company raised over $8 billion from IPO proceeds and began the next chapter of its history, the one where the company has been actively working on becoming profitable.

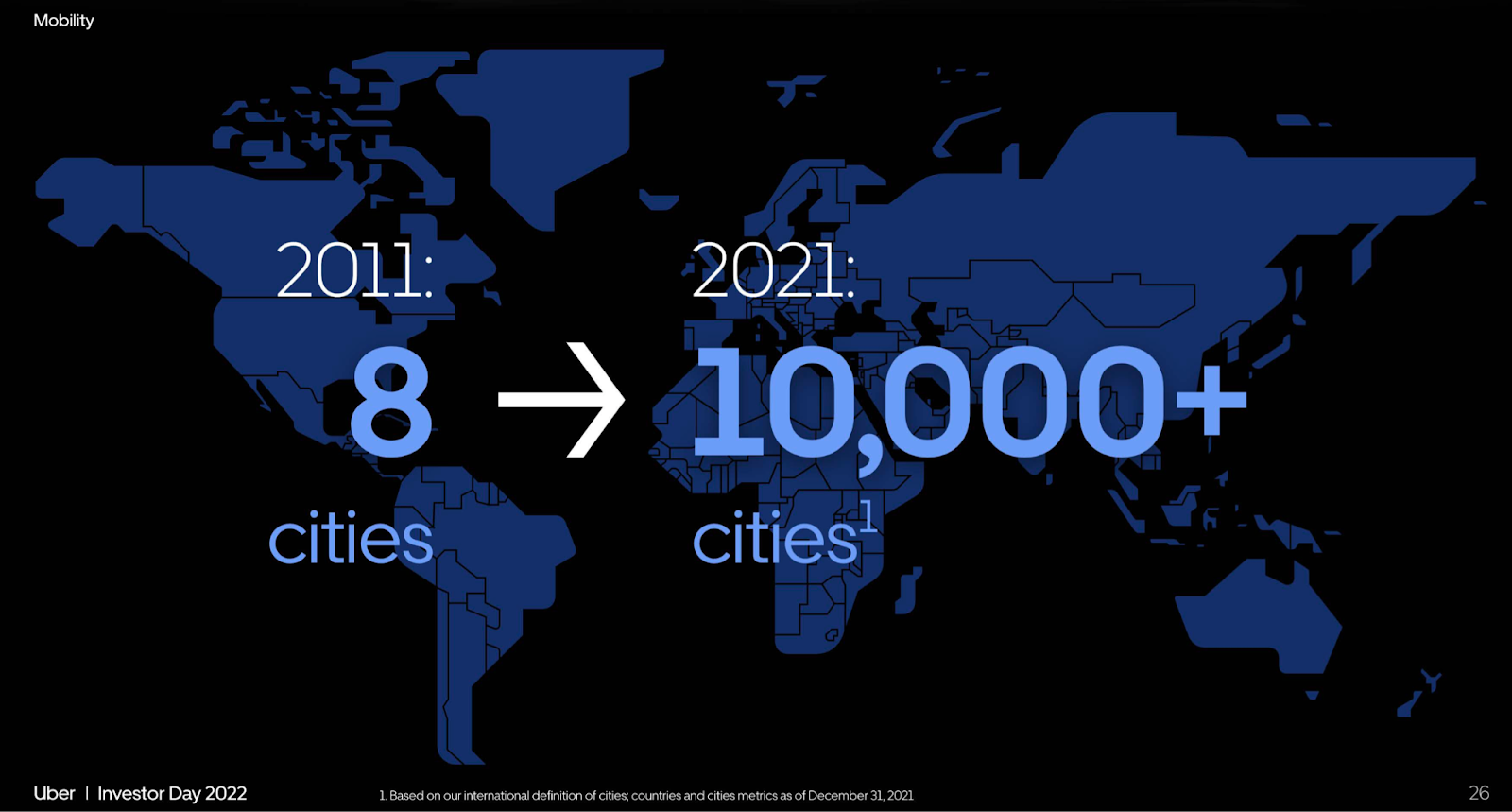

The company has come a long way since the early days, from a handful of cities to more than 10,000, with a global footprint and a leading position in the vast majority of the markets. Uber grew from black cars and SUVs to bikes, scooters, minibusses, and everything in between. Ridesharing has since been recognized and legitimized in almost every major market around the world — and since the pandemic the food delivery part of their business has become as large as mobility but that will change post-pandemic as consumers and business people return to their normal travel patterns.

"Ten years ago, Uber was born out of a watershed moment in technology. The rise of smartphones, the advent of app stores, and the desire for on-demand work supercharged Uber's growth and created an entirely new standard of consumer convenience. What began as "Tap a button, get a ride" has become something much more profound: ridesharing and carpooling; meal delivery and freight; electric bikes and scooters; and self-driving cars and urban aviation. Uber is a once-in-a-generation company, and the opportunity ahead of it is enormous." ~Dara Khosrowshahi on Investor Day 2022.

Opportunity / Technology / Customers

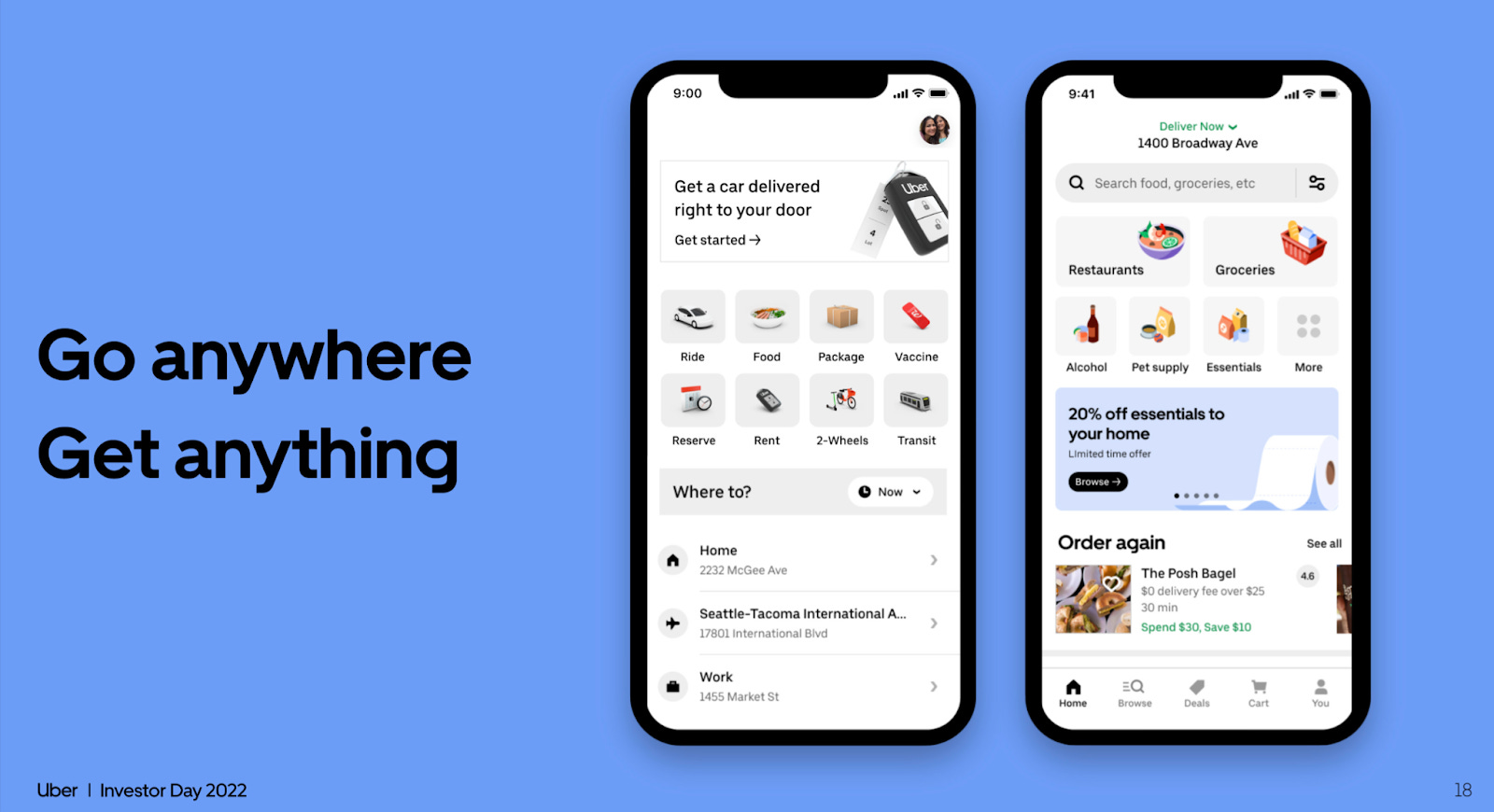

Today, Uber's network spans tens of millions of consumers and partners — it represents one of the world's largest platforms for independent work aka the “gig economy”. Uber still accounts for less than 1% of all miles driven globally but this could change over the next decade as more urban residents give up their cars and lean more heavily on public transportation and ridesharing. Uber has barely scratched the surface when it comes to food delivery and logistics. There is a lot of untapped potential in all segments in which the company operates, and these segments represent hundreds of billions of dollars in potential revenue every year.

Mobility

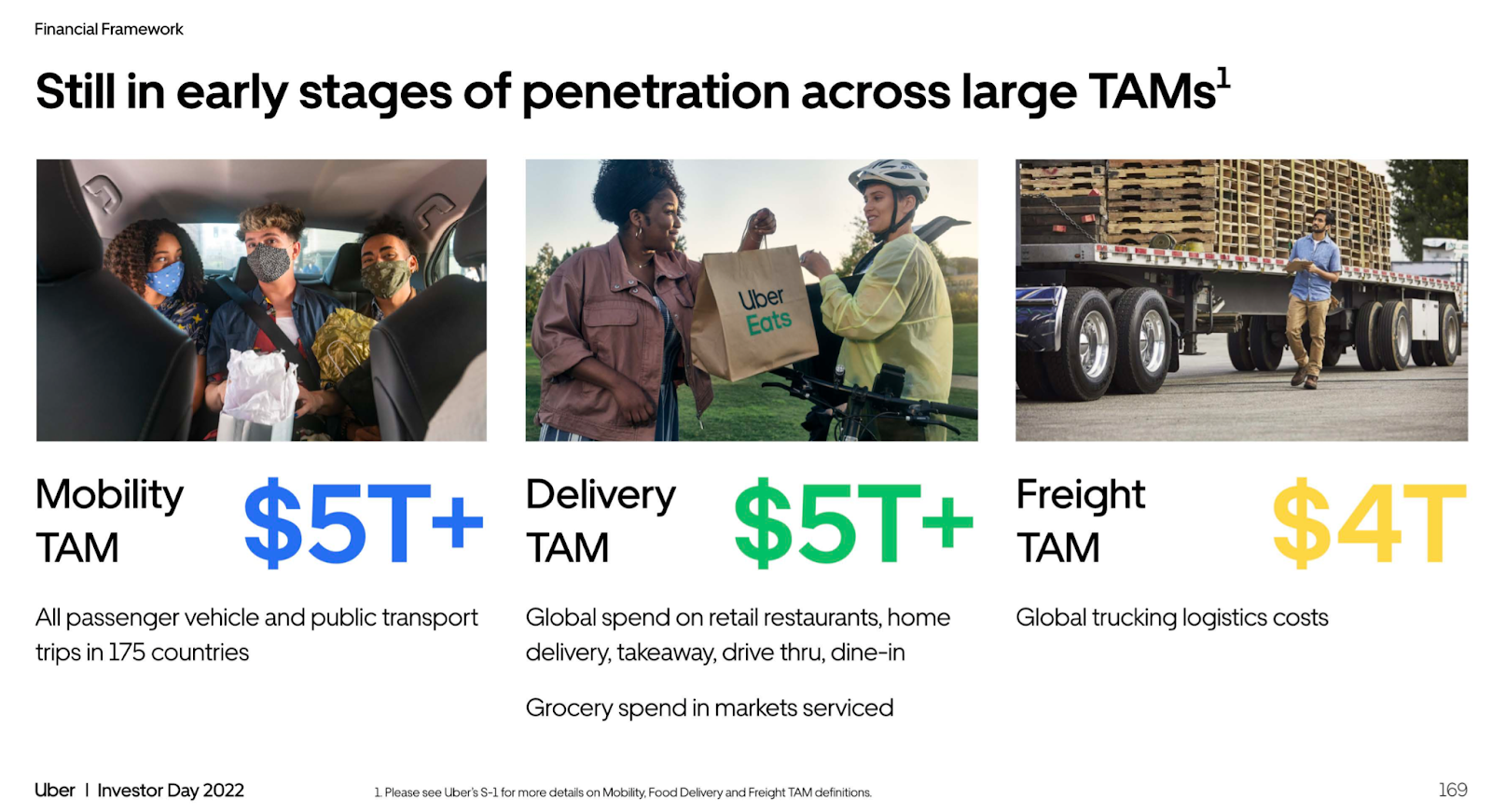

Uber helps people go anywhere they want — this is the core mission at Uber. The mobility segment (refers to products that connect consumers with drivers who provide rides in a variety of vehicles, such as cars, auto-rickshaws, motorbikes, minibuses, or taxis) is estimated to be a $5 trillion market worldwide.

This large market is highly fragmented, but Uber has a leading ridesharing category position in every major region of the world where the company operates. In some markets, for example, China, South East Asia, and Russia, Uber operates through minority owned affiliates, such as Didi, Grab, and Yandex.Taxi

Uber sold their operations in these countries to their competitors in exchange for equity stakes. These companies are the ridesharing leaders in their respective markets. Didi and Grab both came public in the past year but unfortunately for Uber both of those IPOs turned out to be massive disasters and the stock prices are down 60-70% from their highs.

Uber’s vision is to be a part of the trip every time a consumer leaves the house. Instead of monthly or weekly, it should become a daily use case. The company wants to achieve it by (i) deepening core rides penetration, (ii) expanding use cases, (iii) scaling sustainable, low-cost products, (iv) developing alternatives to individual car ownership, and (v) leading the transition to electric and autonomous vehicles.

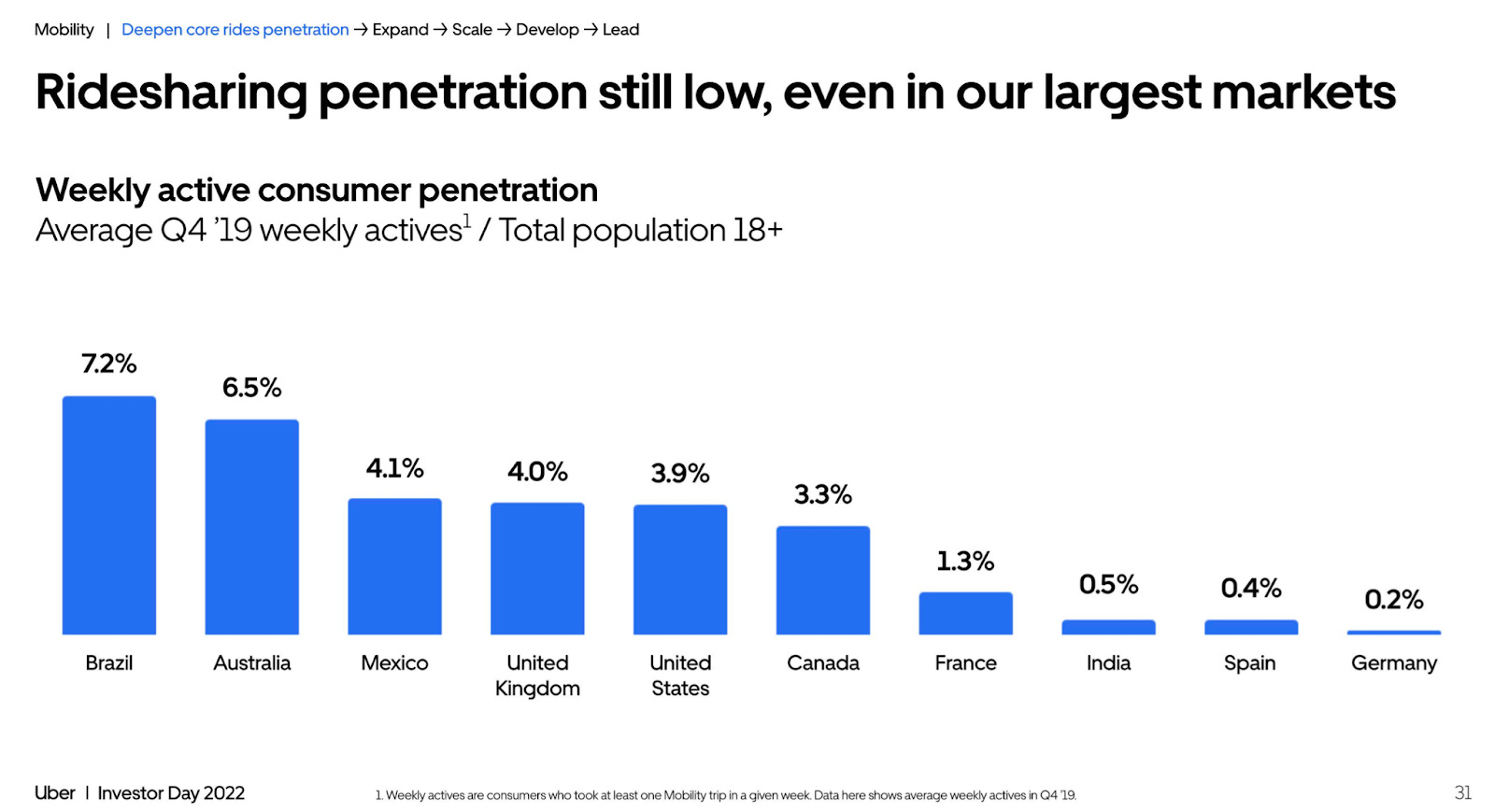

First off, despite Uber being a well-recognized brand in all markets where the company operates, there is still a considerable amount of untapped growth potential in each of these markets. For example, only 4% of the population uses Uber in a given week in the US or 7% in Brazil. It is true across all major markets where Uber is present.

"To put that in perspective, if the US reached the weekly saturation levels of Australia, that's an incremental $14 billion in gross bookings annually. If India reached the levels of Brazil, that would be 10X the number of weekly active users and $15 billion in gross bookings." ~Andrew Macdonald, SVP Mobility & Business Operations, on Investor Day 2022.

There are still a lot of large economies around the world where Uber is far from being a leader, for example, Spain, Germany, and South Korea. It was due to regulations that prohibited companies like Uber from operating in the country, protecting the traditional taxi industry and employees' rights. But that is slowly changing.

In Spain and Germany, the company operates by acquiring licenses for fleets that employ drivers. As a result, Uber's business in both countries is growing nicely (Spain has more than doubled since 2018, and Germany went from near zero in 2018 to $400 million in 2021).

In South Korea, the company took a different approach: they partnered with a local company, SK Telecom, and now jointly operate a joint venture, which goes after the $7 billion Korean mobility market. The company expects to increase the gross bookings by 60X in the next two years. A similar approach is now used in markets like Italy and Japan, where Uber is trying to get a local partner on board so they can unlock these markets together.

Today, most trips (90%) booked via the app are UberX, which is solo, on-demand, from point A to point B, a 4-door-car type of transportation. Less than 5% of remaining trips are shared among several people, 1% of trips are scheduled in advance, and just 4% are with traditional taxis. All these other types of trips represent tremendous opportunities for the company.

For instance, pre-booked transportation remains the preferred choice for most consumers worldwide. In the US alone, this market represents an additional $8 billion opportunity, and it has much higher margins for the company and also higher earnings for drivers. For Uber, the number of pre-booked trips is currently negligible — just 6% of gross bookings in the US and Canada and less than 1% globally.

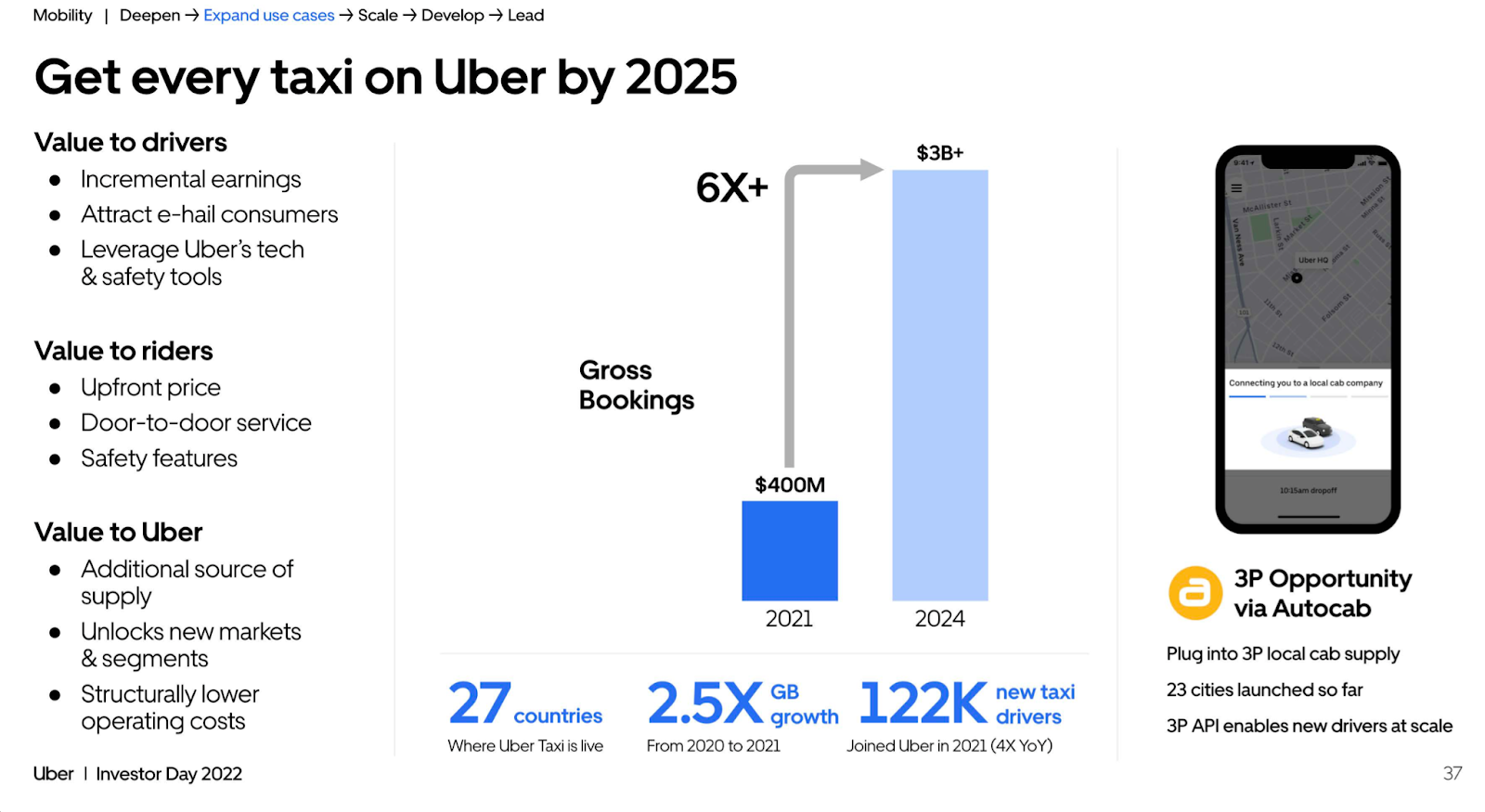

There is an even larger opportunity that Uber has not historically served well. Hail-able taxis represent a $120+ billion market worldwide, which is 2x larger than Uber's mobility business. There are over 20 million licensed vehicles on the streets. So what Uber is focusing on is getting as many licensed taxis on board as possible. Taxis open new markets for the company. For example, in Turkey and Hong Kong, the company primarily operates through licensed taxis. This subsegment grew 2.5X from 2020 to 2021.

Uber is continuously working on bringing more modes of transportation to its platform. It helps to onboard more customers but offering more choices and price points. As the company builds out new use cases, they are laser-focused on affordability since most of its TAM sits below UberX prices. In other words, the majority of customers cannot afford to use UberX on a frequent basis. So the priority is to make Uber more accessible to more people. It is what truly unlocks the massive opportunity in the mobility segment.

Lowering prices for individual car rides won't work. The only way is to introduce more affordable alternatives, from shared rides to micro-mobility to public transit, to leverage network density and create excess vehicle capacity. Uber tackles this problem with several initiatives.

First, they completely revamped what Uber Pool was. Now called UberX Share, there are no huge discounts anymore, just a fixed 5% discount and Uber Cashback to the rider only if one is matched with another rider. Something that was hugely unprofitable for the company now starts to have a much better core unit economics for them, riders, and drivers.

Next, comes the high capacity vehicles (HCV), like private buses. These are used daily by millions of people, especially in many emerging market cities, and they are 1/4 of the price of UberX. But these private buses are often slow, unsafe, overcrowded, and stressful. Uber is working on rebuilding this experience completely. The HCV business is growing rapidly, and most importantly, these trips are happening daily, increasing the usage of Uber's platform. The company also has a business opportunity here. They partner with other businesses in various parts of the world that offer their employees a better commute. For example, with Nissan in Egypt, Toyota in Brazil, and Tata Realty in India – all have private buses in place operated by Uber.

Finally, motorbikes and auto-rickshaws, which are really popular in some parts of the world, especially in the emerging economies, since they are low cost and small in size, help the company unlock a massive TAM by offering rides at a fraction of the UberX prices. Putting them on the platform solves major consumer pain points around reliability and price transparency. And these modes of transportation proved to be a great user acquisition lever too: 10% of all first-time riders on the platform in 2021 came through a two-wheeler or a three-wheeler trip.

So what Uber is essentially doing is it battles against car ownership. "So thinking a bit bigger, we believe we can gradually help displace personal car ownership by systematically finding ways to make it easier not to own a car." ~Andrew Macdonald, SVP Mobility & Business Operations, on Investor Day 2022.

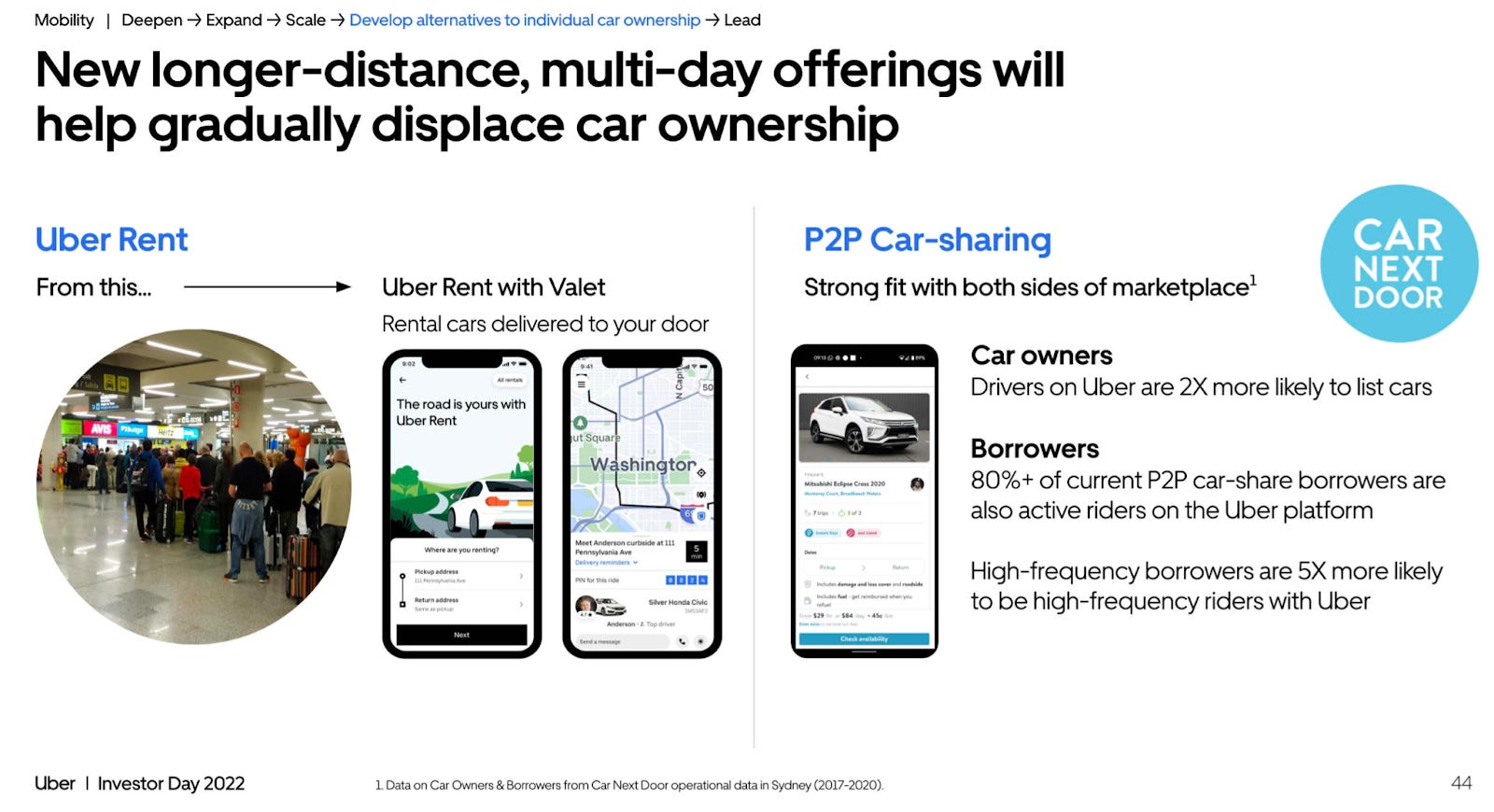

There are a few more initiatives the company is involved in to offer alternatives to car ownership. First is Uber Rent which opens up an additional $55 billion rental car TAM for the company. In partnership with Avis, one of the largest car rental companies in the world, Uber offers to get a car dropped off at the customer's location with a press of a button. This is still in the early days, currently only available in Washington DC, but the company plans to scale Uber Rent to other markets in the coming years.

The second initiative is P2P car sharing. Most cars sit unused for 95% of their useful life and could be rented from owners. Uber is currently testing this idea in Australia, where they recently acquired Car Next Door. They are now focused on scaling it in the local market, but it could be a global opportunity if successful. This is similar to the Turo and GetAround business models — which makes me wonder if we could see an acquisition of them by Uber prior to their anticipated upcoming IPOs.

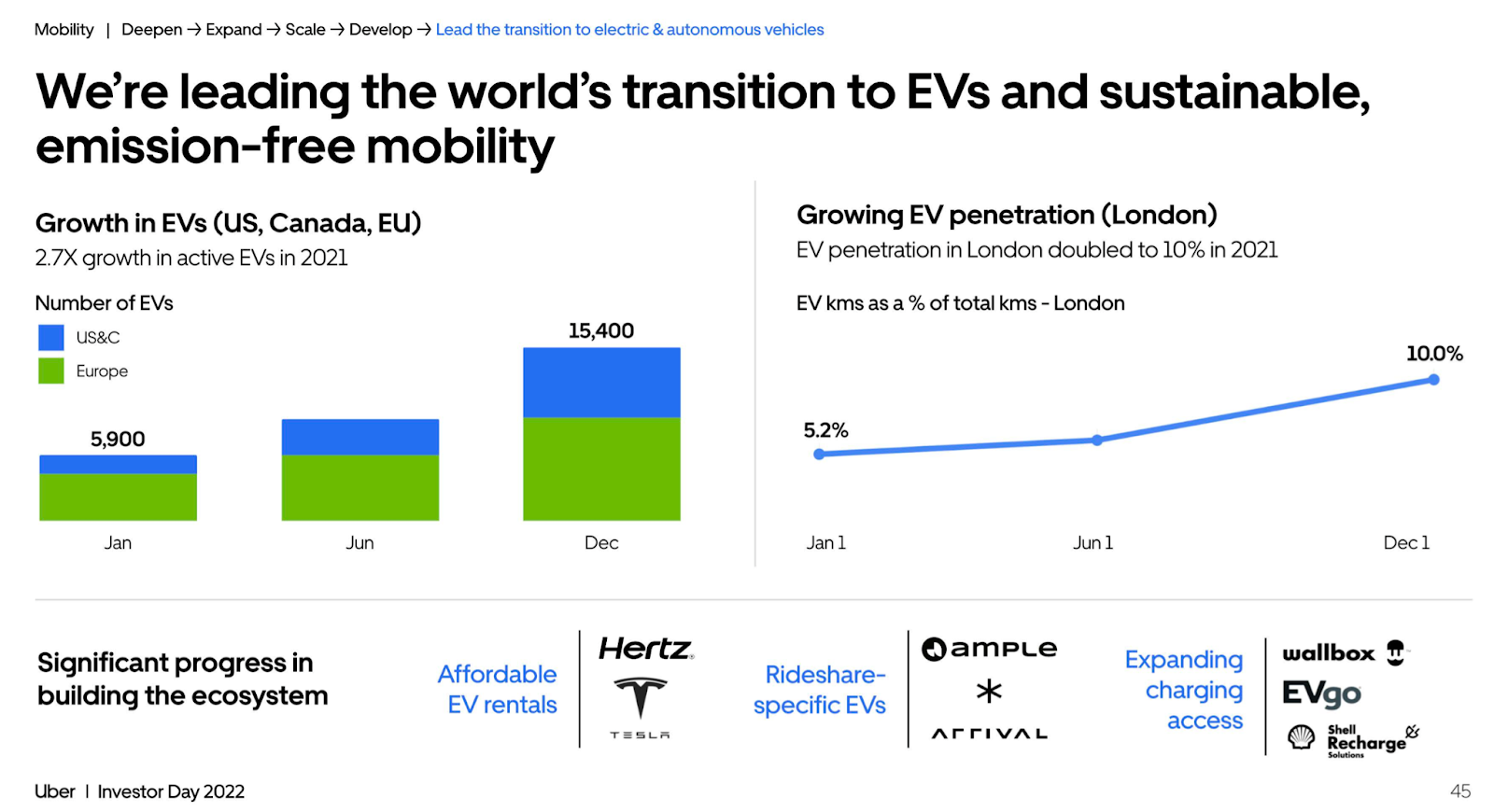

Mobility is rapidly evolving in all areas of the world. Electrification takes the lead in the next big change. It is clear by now that the future of transportation is electric. And Uber will play a crucial role in this switch. No wonder why the company has set an ambitious commitment to get to zero emissions by 2040. Today, riders can already choose hybrids or EVs in hundreds of cities around the world.

To achieve this goal further, Uber is actively developing various partnerships. The deal with Hertz, one of the largest rental companies and owners of car fleets, allows drivers on the Uber platform to get Teslas to drive. The waiting list right now is in the thousands — this is exciting for drivers, riders and shareholders of both $UBER and $TSLA

EVs like Tesla are not only cool to drive, they have lower operating costs, which means drivers can earn more. It is also a win-win situation for everyone: good for the planet, good for Uber, good for drivers and also the riders, as prices for rides should eventually decrease significantly. We also have to wonder how autonomous driving will play a role in the future of Uber’s different businesses from mobility to delivery.

Uber is also working with other companies on launching rideshare-specific EVs. One particular partnership looks very interesting. Uber and Arrival are working on a "super minimal" electric car. The plan is to create an electric fleet of such vehicles that can be used for ride-hailing. The production is still far away, but the idea is clear: Uber is working to build the ecosystem with many partners instead of building it themselves.

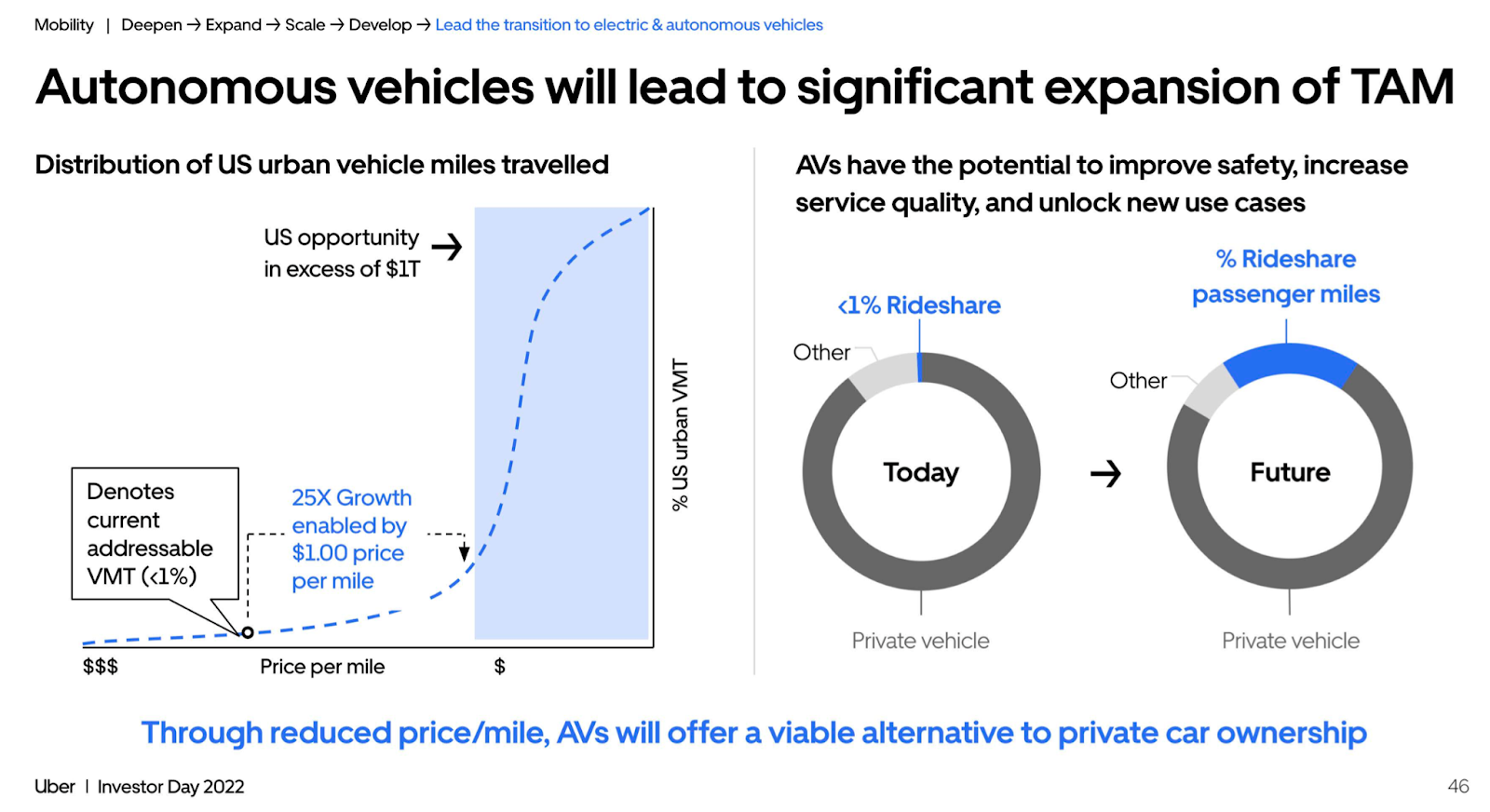

Perhaps, the next big thing in mobility after electrification would be autonomous vehicles (AV). While it is still quite far away from us, the AVs will lead to a significant TAM expansion. With the reduced price per mile, AVs could become a serious challenger to private car ownership.

Uber has recently changed its strategy, and instead of building AVs itself, management decided to partner with other AV developers. These developers will be able to launch AVs on Uber's mobility platform, the largest in the world.

There is so much going on in the mobility segment, and the company is best positioned to capitalize on these opportunities in 2022 and beyond.

Delivery

The second part of the Uber business is helping people get anything they need. The delivery business was launched over 6 years ago and has continued to evolve from restaurant delivery to “almost anything delivery”. In terms of restaurant delivery users were able to search for and discover local restaurants, order a meal, and either pick it up at the restaurant or have the meal home delivered by one of the Uber drivers. Since the pandemic began, Uber has started to offer grocery, convenience, alcohol, pharmacy, and other types of local commerce. Their alcohol delivery business (which I have used several times) came from the acquisition of Drizly, a Boston based startup that had raised $120 million from investors. Uber acquired Drizly for $1.1 billion in early 2021.

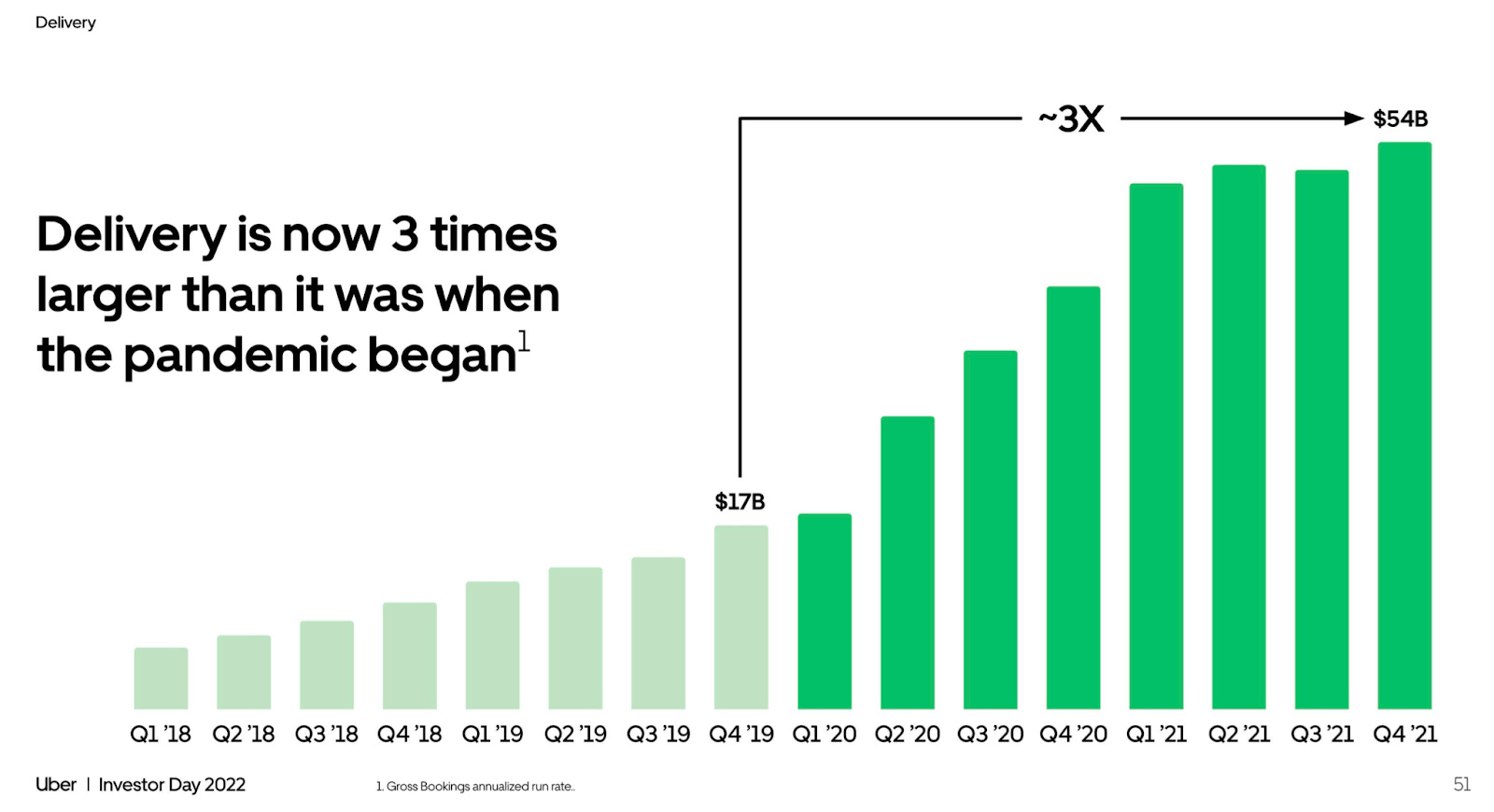

The COVID-19 pandemic has played a crucial role in developing and growing Uber’s delivery segments. At the end of 2019, delivery was a solid $17 billion annualized GV business for Uber and growing at healthy rates. But now, it is 3X larger than it was prior to the pandemic. Something that would normally take 3 to 5 years happened within 6-12 months as many consumers were forced into these delivery services but found them so convenient they have continued to use them even post-pandemic.

The delivery segment has become and remains larger than the mobility segment as of the first quarter of 2022. And even though the vast majority of economies have reopened, it keeps growing. Uber has built the largest food delivery platform outside China. It is active in 32 countries, and it has 7 leading positions in the top 10 markets. The overall TAM is absolutely massive, and Uber owns only a fraction of what is available.

"The delivery penetration, as you can see here, is still extremely low across the restaurant and the grocery categories, not even to mention retail. Capturing just a small fraction of this opportunity would actually double our delivery business today. So there is an enormous opportunity ahead of us." ~Pierre-Dimitri Gore-Coty, SVP of Delivery, on Investor Day 2022.

The company wants to achieve it by providing users instant access to all local commerce, not just food from restaurants. For example, if one needs a quick replacement of the iPhone charger or to pick up something from a grocery store, Uber Delivery would be able to get and deliver it. The opportunities are endless across the ecosystem they are building not to mention the delivery segment gives drivers the ability to generate more income during their shifts which is important for recruiting and retaining the best drivers.

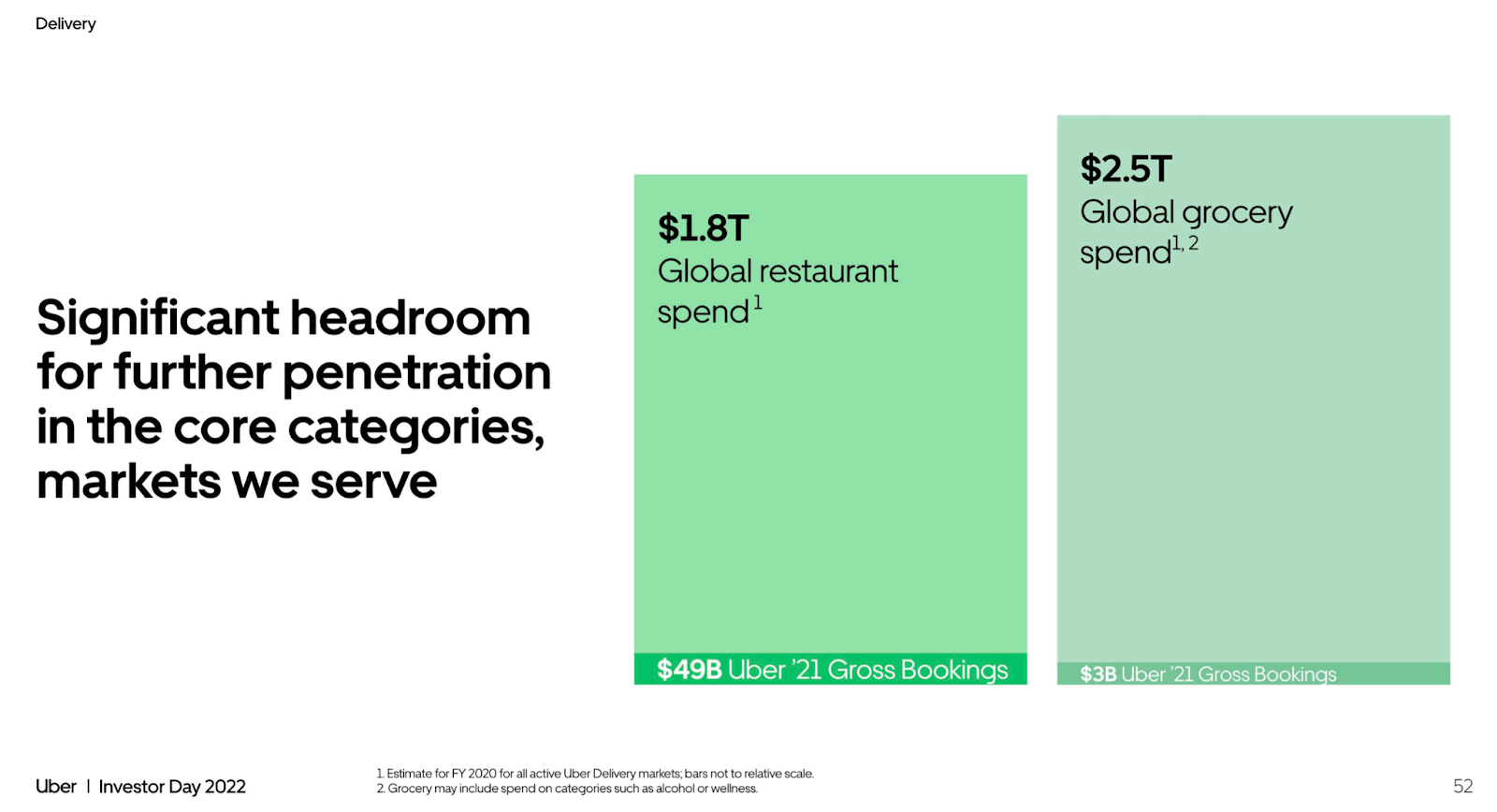

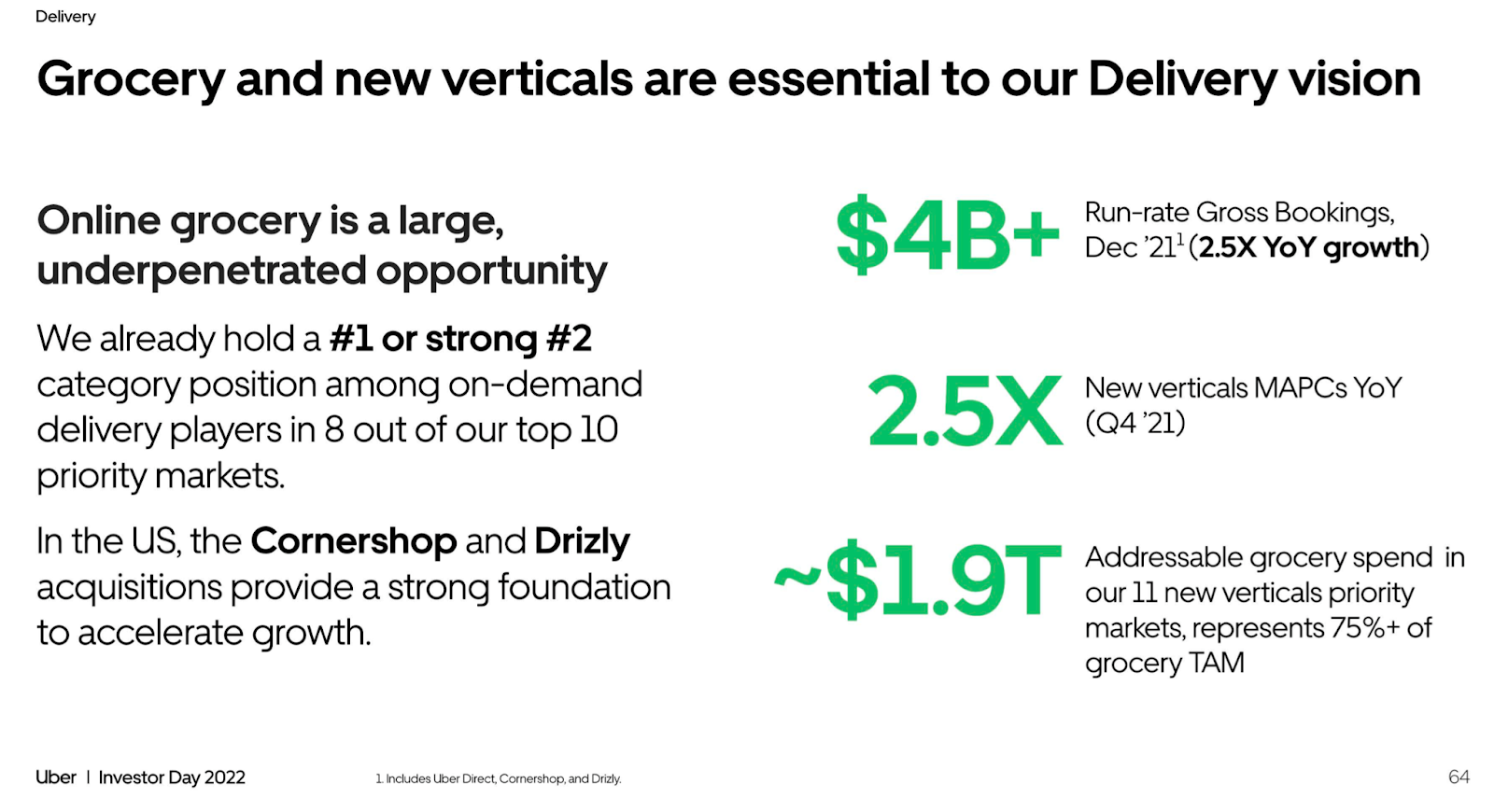

The grocery and other retail verticals represent an enormous, underpenetrated opportunity worth a whopping $1.9 trillion. The company wants to capitalize on this opportunity by increasing the use case from once a week to actually delivering whatever consumers need, whenever they need it, on a daily basis.

The grocery segment is a natural entry point to broader retail, and it does not require any behavior change from users. In addition, its massive spend and high-frequency repeat purchasing are what make grocery so interesting for Uber.

One part of the grocery segment stands out the most – quick commerce, which is sub-30 minute deliveries of everyday essentials. This subsegment is growing nicely and is currently available in selected cities. Uber takes a partnership approach for it and already works with the likes of GoPuff in the US and Carrefour in France. For example, the Carrefour Sprint (the partnership launched in October 2021) offers 15-min delivery of over 2,000 SKUs. Many users now use Uber as a primary service to order groceries, not just for quick delivery.

In other retail verticals, the company is actively developing delivery-as-a-service, called Uber Direct. First introduced in 2020 on the back of Postmates technology (acquired by Uber), it allows merchants and retailers to deliver orders that originate from their own apps and websites. The company already supports thousands of merchants around the world, from use cases like parking lot pickups with Walmart in the US to actually delivering orders from brands like Apple, Sephora, and Adidas.

To sum up, from the core restaurant delivery to a massive retail space, the delivery business is still in the very early stage and offers opportunities much larger than the opportunities offered by the mobility segment.

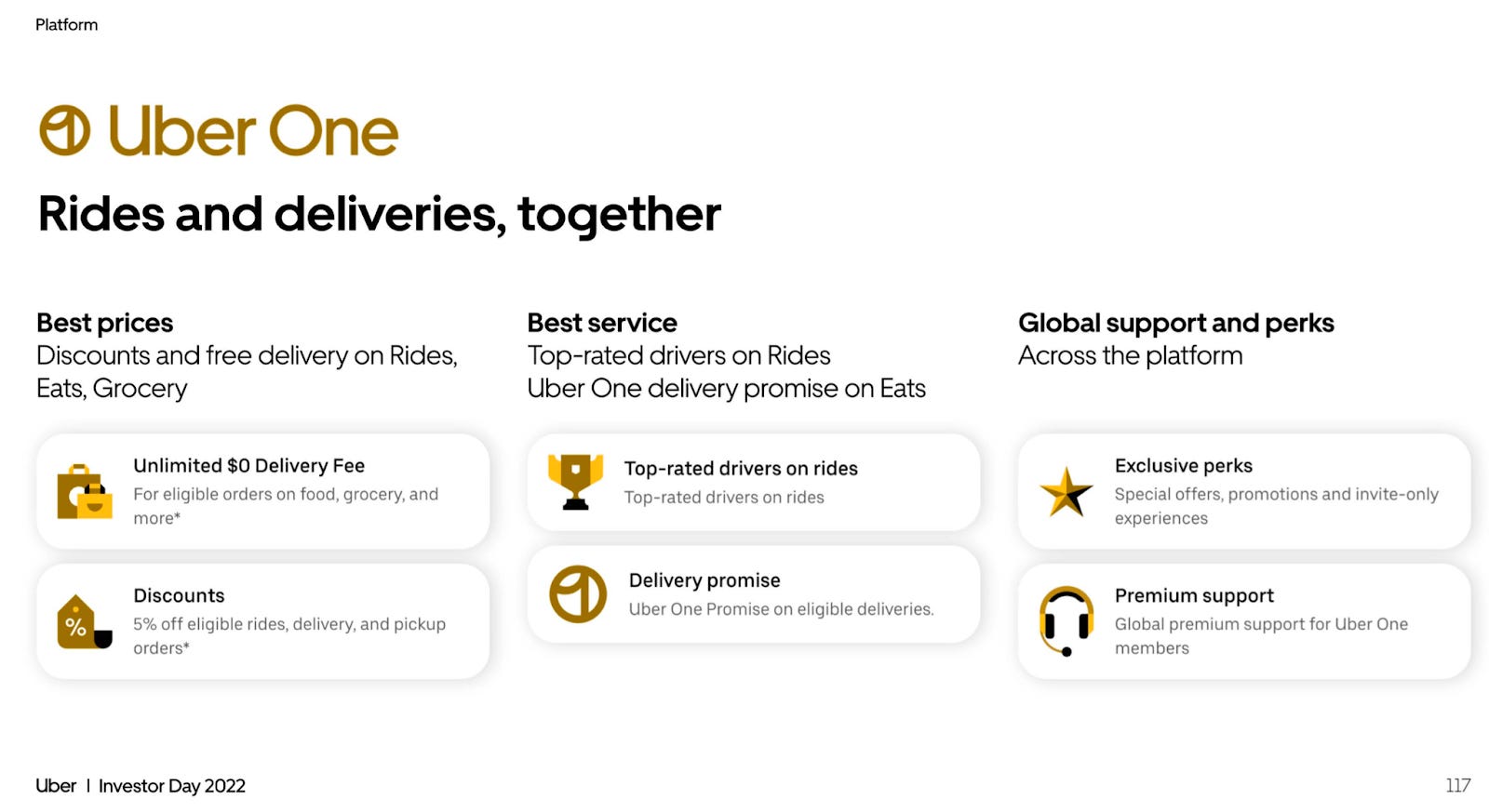

Uber One

One particular product, Uber One, launched in late 2021, should further help the company increase the usage of more of its products and more often.

Uber One is a membership program that brings together the best of Uber rides, delivery, and groceries. It is the only membership program that provides discounts and exclusive experiences across both rides and delivery. The membership price is $9.99 per month or $99.99 per year, and it can be activated inside any of Uber's apps.

As Uber helps customers go anywhere and get anything, Uber One provides members with savings and helps create an elevated experience

"We want our customers to experience firsthand how Uber can make their every day more effortless," said Awaneesh Verma, head of Membership at Uber. "Uber One offers elevated access to all of Uber: rides, delivery, and groceries. Members get preferred pricing, premium support, and surprise and delight perks that can make every day more fun."

As of Q4 2021, 17% of total gross bookings came from members, and these members are more valuable to Uber because they spend 2.7X versus non-members.

Membership is now available in selected countries and cities, but the company plans to significantly expand across geographies and across areas to increase the proportion of users that are members.

Freight

This is a segment that many investors are less familiar with because they don’t use the service on a daily or weekly basis like mobility (ridesharing) and Eats (food delivery) but freight could be a massive opportunity for Uber over the next decade.

Freight is a $4 trillion global market, with almost $1 trillion in the US alone — 70% of all goods are moved by trucks which makes it a critical component of the global economy.

But yet, the freight industry is broken which starts with the drivers that are aging out. Twenty years ago, an average truck driver's age was 35 years; now, it is 55. Most of these drivers (84% of all carriers) are small mom-and-pop shops with less than five trucks. It is practically impossible for them to connect with the big shippers or run their operations efficiently.

The ecosystem itself is vastly inefficient. On average, it takes 25 steps to just coordinate and move a truck, and coordination accounts for more than 10% of the cost of a truck. Moreover, because of various supply chain issues, shippers are forced to pay more and more for the logistics. Shipper costs in 2021 increased almost by 50% year-over-year and as a result of this increase, consumers have to pay more even for regular goods. To make the situation even worse, on average, 30% of all the trucks are driving empty at any given time which is clearly an inefficient scenario not to mention it unnecessarily increases the environmental impact. Those 30% empty trucks amount to more than 2% of global greenhouse emissions.

To combat these problems, Uber started to build out its logistics business in 2017. In 2018, it was spun off into a separate business unit and underwent an expansion. Before COVID-19 hit, it was doing relatively okay but still unprofitable. A significant breakthrough happened after. Today, Uber Freight is the largest digital freight marketplace, with $17 billion in freight under management. More than a million truck drivers (a quarter of all truck drivers in the US) have an Uber Freight app installed on their mobile phones. Uber Freight is now a vital part of America's supply chain.

Uber Freight does something that others don't. With artificial intelligence and data science it connects the right truck, at the right time, for the right shipper, for the right price, instantly. Uber Freight has become the most efficient way to procure freight in the market today.

The success of Uber Freight is not only due to its superior technology. Carriers are now paid for the shipments almost instantly versus an average of 45 days in the industry. It is a significant advantage for carriers as they can rely more on cash flow to grow their small businesses. They also can benefit from exclusive access to discounts on fuel, maintenance, insurance, and more. Combined, it helps them increase their earnings and reduce their costs.

Uber now serves not only thousands of small shippers but also more than 100 of Fortune 500 shippers, five out of the top five beverage companies, and nine out of the top 10 CPG companies. For many of those shippers, Uber Freight is now their biggest carrier. Just these enterprise shippers collectively represent more than $100 billion of freight opportunity and Uber is just getting started with them.

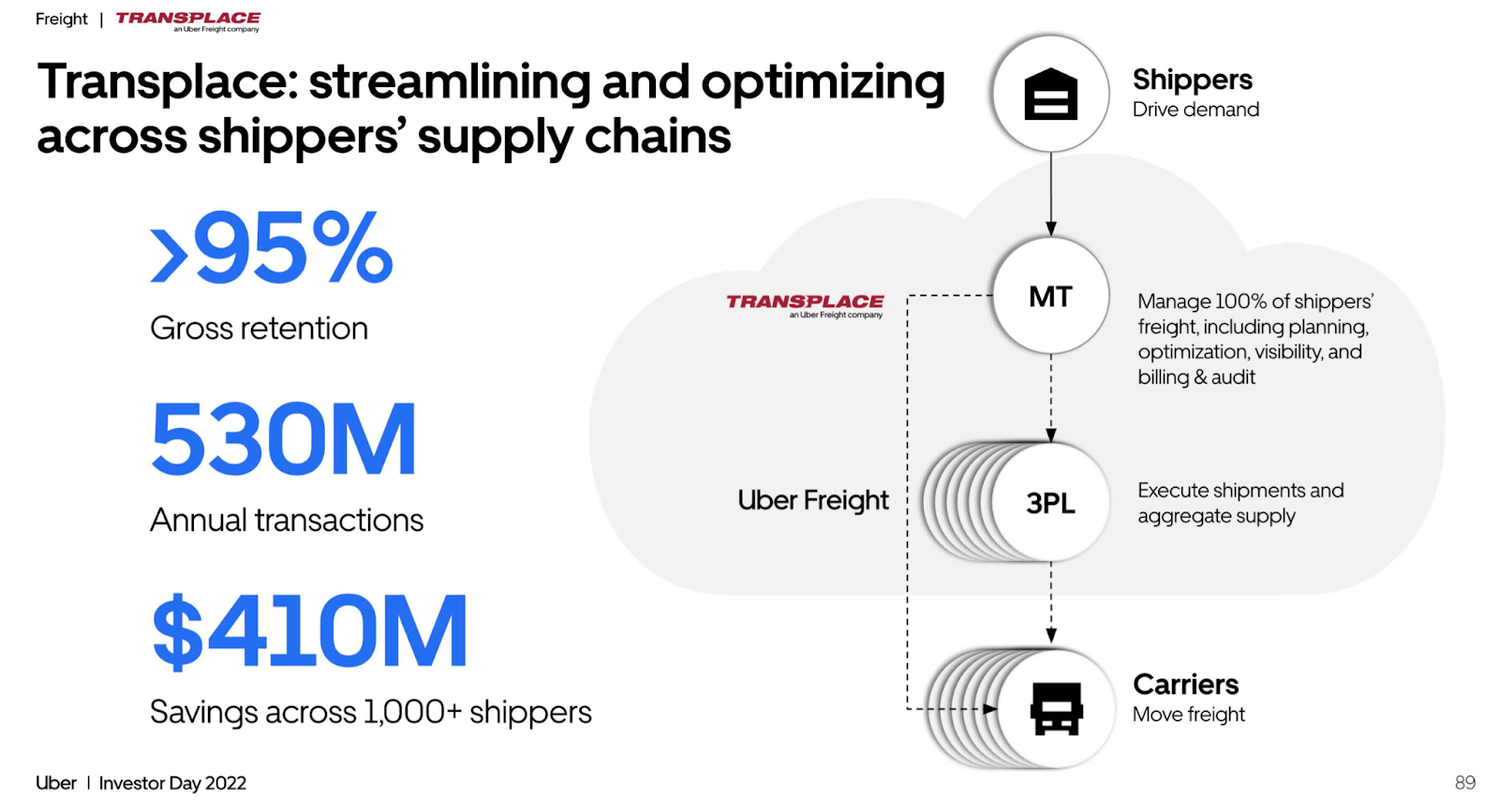

In 2021, Uber acquired a company called Transplace, the leading managed transportation provider in North America. Managed transportation is essentially a shipper deciding to fully outsource the logistics to a third party. "Because if you're a shipper, you need to manage hundreds of different brokers and carriers provider, do all of that with a large in-house team, deal with varying technology or the lack of technology by those providers, and even after all of that, you're not fully controlling your supply chain costs, because you're optimizing, to begin with on a subscale network. Compare that to the Transplace experience, it's magical. Transplace is the single point of contact across your logistics needs. They're managing all of your carrier relationships. Transplace software is integrated across their entire operation, from ELP to warehouse management, to customer service, audit, pay, and more. And this makes Transplace a trusted strategic partner, resulting in over 95% customer retention." ~Lior Ron, Head of Uber Freight.

Now the company combines Uber Freight, the number one digital broker, with Transplace, the number one managed transportation provider, and creates the largest logistics cloud platform ever built. This will significantly help Uber gain more market share in this massive segment.

One particular part of this business is especially exciting – the autonomous trucks. These trucks will fundamentally improve safety and reduce cost. While autonomous cars are pretty far away, autonomous trucks are already here. Last year, Uber announced the first pilot with Aurora, which is moving loads on self-driving trucks already, in Texas, between Dallas and Houston, every day. A little more time will pass, and we will see autonomous trucks on the roads all over the US and then around the world, and Uber, again, will be at the forefront.

Uber Business

With the growth of Uber in popularity among consumers, more and more businesses began to notice that Uber is one of the most costly items on the list of employees' expenses. The company got flooded by various companies asking for an expense solution. As a result, Uber Business was launched.

Uber Business is a platform for managing global rides, meals, and local deliveries for companies of any size. Companies can offer their employees integrated expense management for ordering rides or food on business travel, while Uber takes care of all receipts.

Uber also offers bill splitting, group ordering, and premium customer service. Because many companies are moving to hybrid ways of working, the company can deliver meals to employees' homes, which is something that only Uber can do.

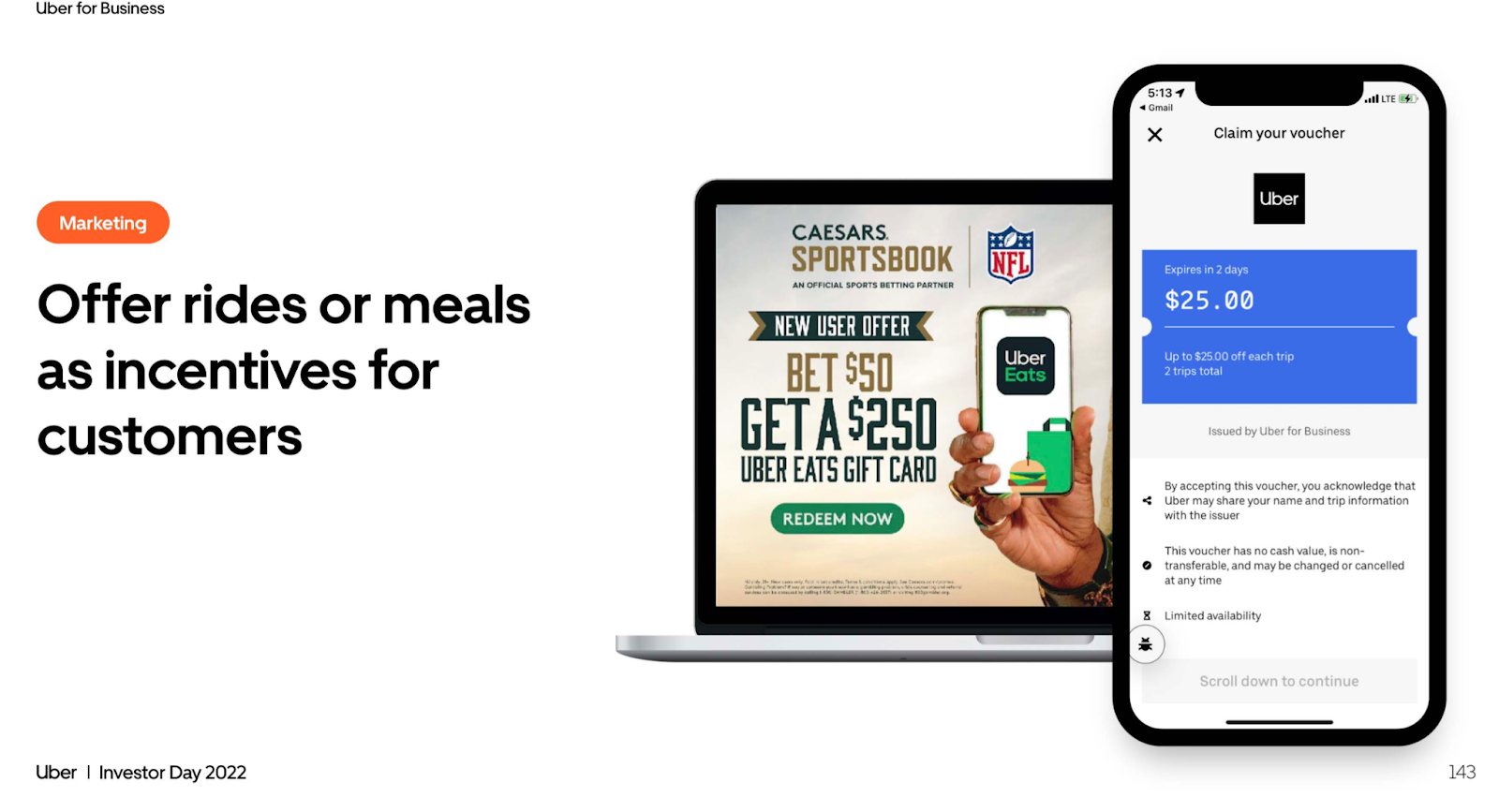

As part of the benefits package, many tech companies started to buy Uber One for their employees. There is also an option to distribute vouchers and corporate gift cards for both Uber rides and food delivery.

The functionality to issue and distribute vouchers and gift cards are also available for other purposes. For example, Uber has also secured multimillion-dollar deals with marketing agencies to provide Uber gift cards as a key part of their campaign. The potential here is enormous and is a powerful complement to the ads business.

There are other features that businesses can use on Uber Business. For example: companies can directly dispatch cars to their clients or VIPs who don't even need to have the Uber app downloaded or order food for executives or entire teams. In addition, there is a HIPAA-compliant offering providing non-emergency medical transportation that allows care teams to request rides to their medical appointments on behalf of their patients or to have prescriptions, food, or medical equipment delivered. It's just another example of how Uber can find a use case for its products.

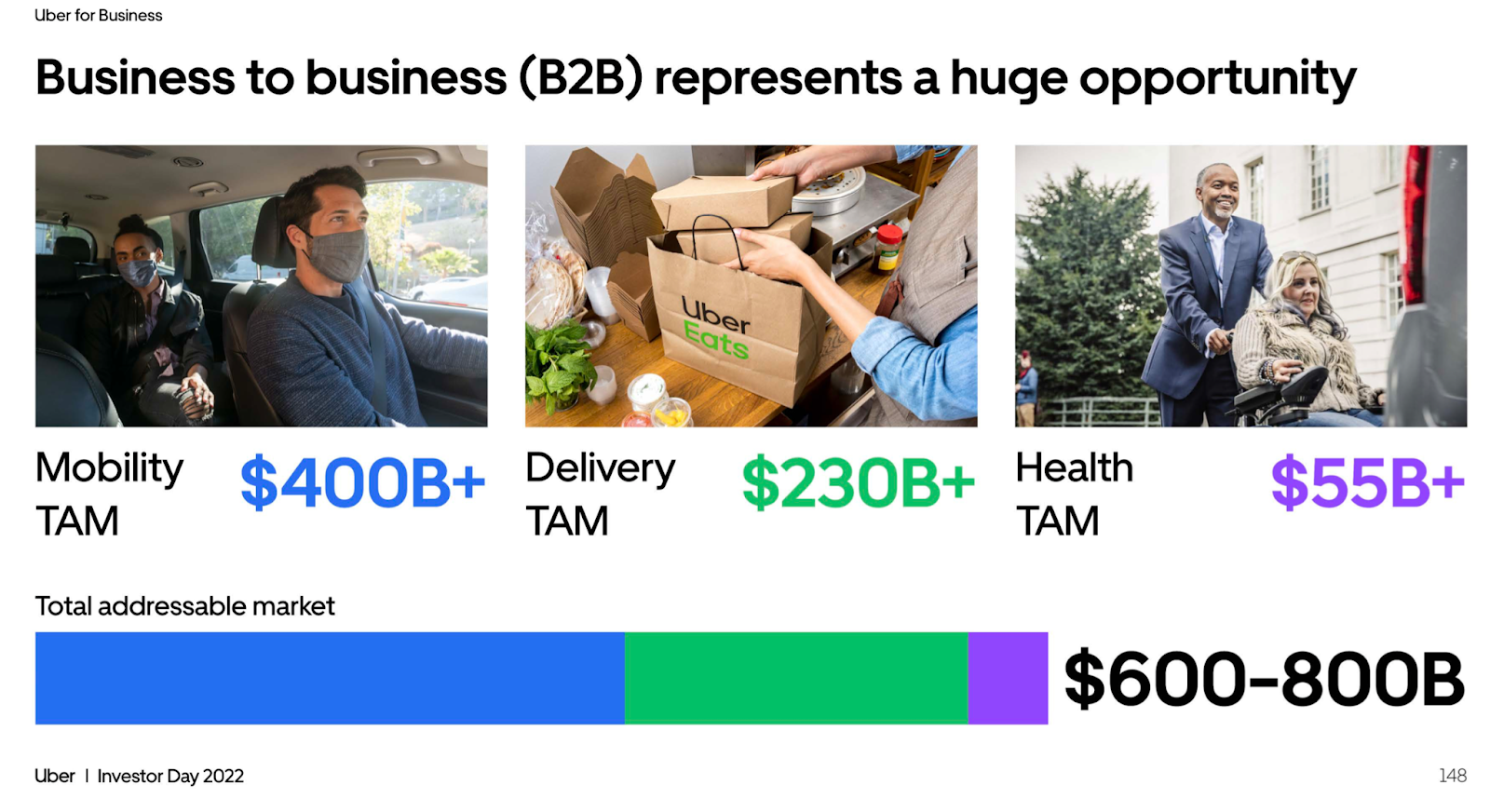

Uber Business is a top-rated service among companies with an NPS of 68. Uber currently has contracts with over 170,000 organizations worldwide, including over 60% of Fortune 500 companies. Uber Business is available in all markets where Uber operates. It is an additional $600 billion opportunity worldwide.

As of 2021, the gross bookings from the business segment were just $1.1 billion, a tiny fraction of the overall opportunity. Uber is aggressively investing to accelerate growth and achieve an annual run rate of well over $5 billion in 2024 (5X from now).

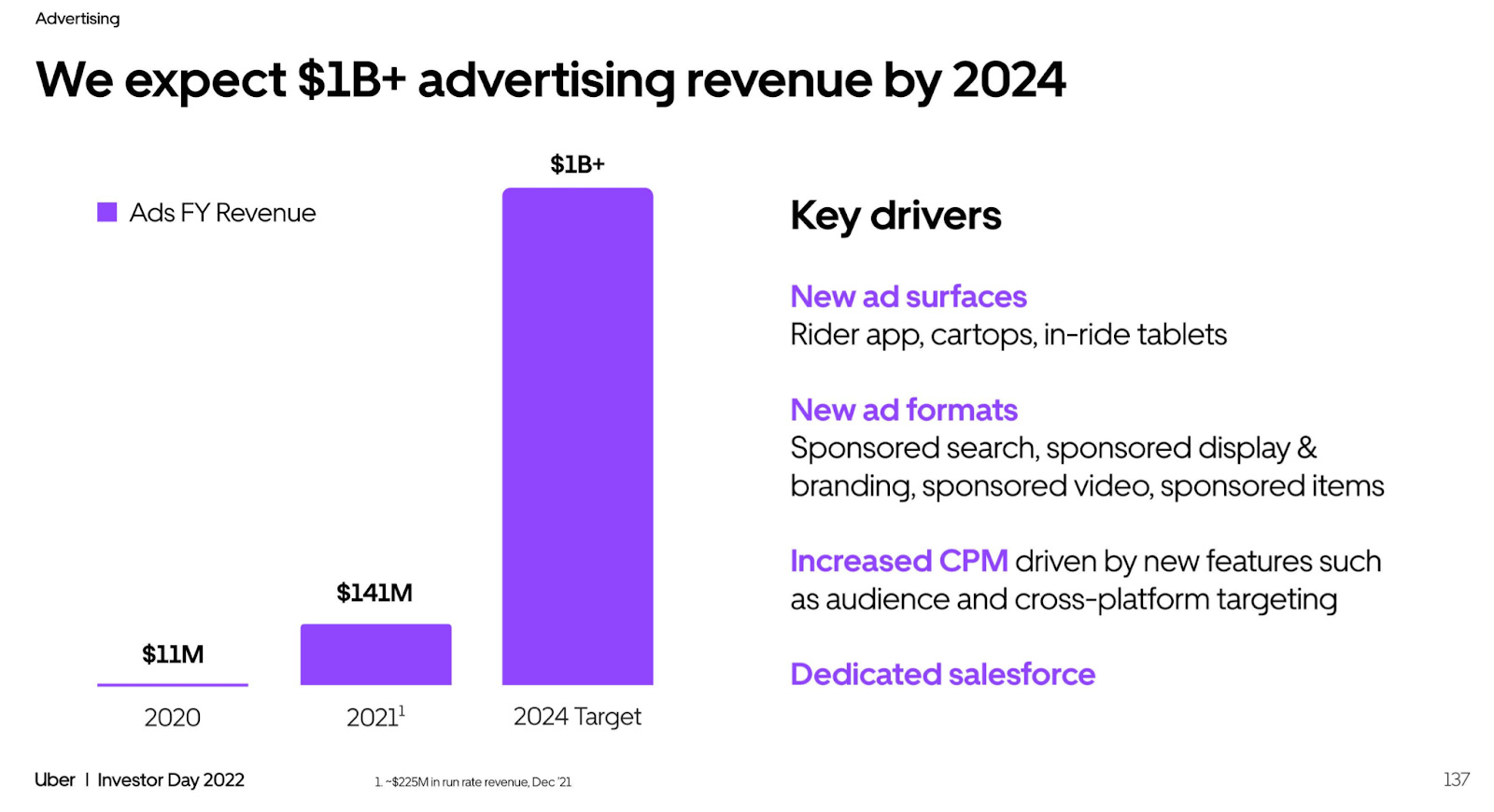

Advertising

There is one more, nascent but high potential business segment – advertising. Uber advertising brings together location-based and shopping data with closed-loop attribution across the mobility and delivery channels for performance and branding campaigns. So what Uber does is it enables advertisers to engage with the consumers on the entire marketing funnel: from awareness to consideration to conversion to retention.

To start with, Uber has a global audience of 180 million monthly consumers who engage with the platform. It translated into 1.8 billion trips in the fourth quarter of 2021 alone. On average, each consumer interacts with the platform about five times per month across the rides and eats services. That is a lot of interaction but still growing.

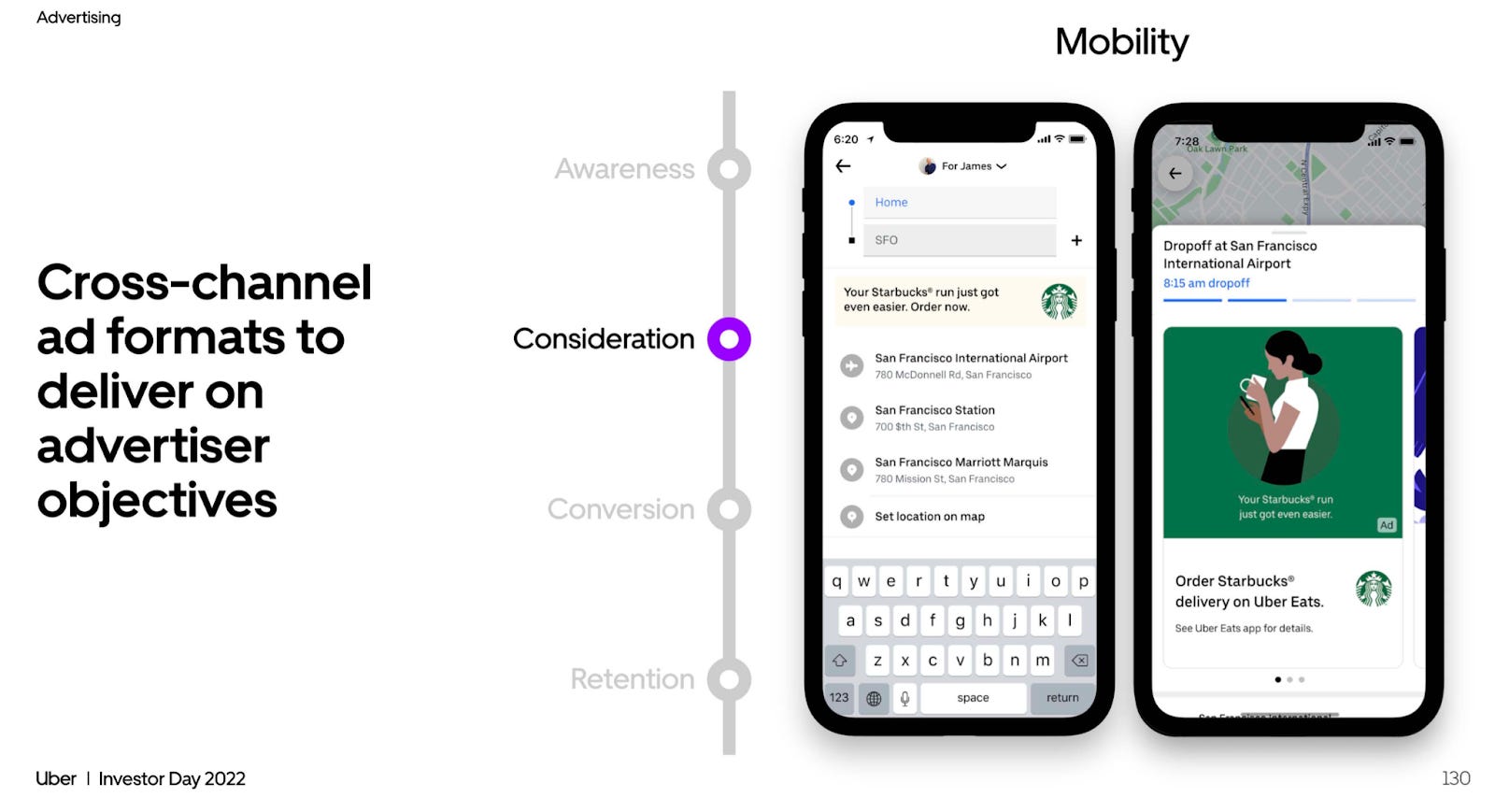

On each of the steps of the marketing funnel, Uber has various ad formats to deliver on advertisers' objectives. Imagine Starbucks has introduced a new holiday-themed drink. To achieve awareness, Starbucks can use cartop and in-car advertising spaces to promote this new drink, including video ads on the screen on the back of the front seat.

Uber can then target riders on the way to their offices by showcasing Starbucks ads inside the app in various formats, including text and banners.

And also target eaters inside the Uber Eats app by showcasing Starbucks sponsored ads in search and at the checkout.

And finally, Starbucks can interact with engaged, loyal customers who purchased the products by messaging them directly through the app. No other platform can reach consumers through such a targeted omnichannel marketing solution with transaction-based measurement on a global scale.

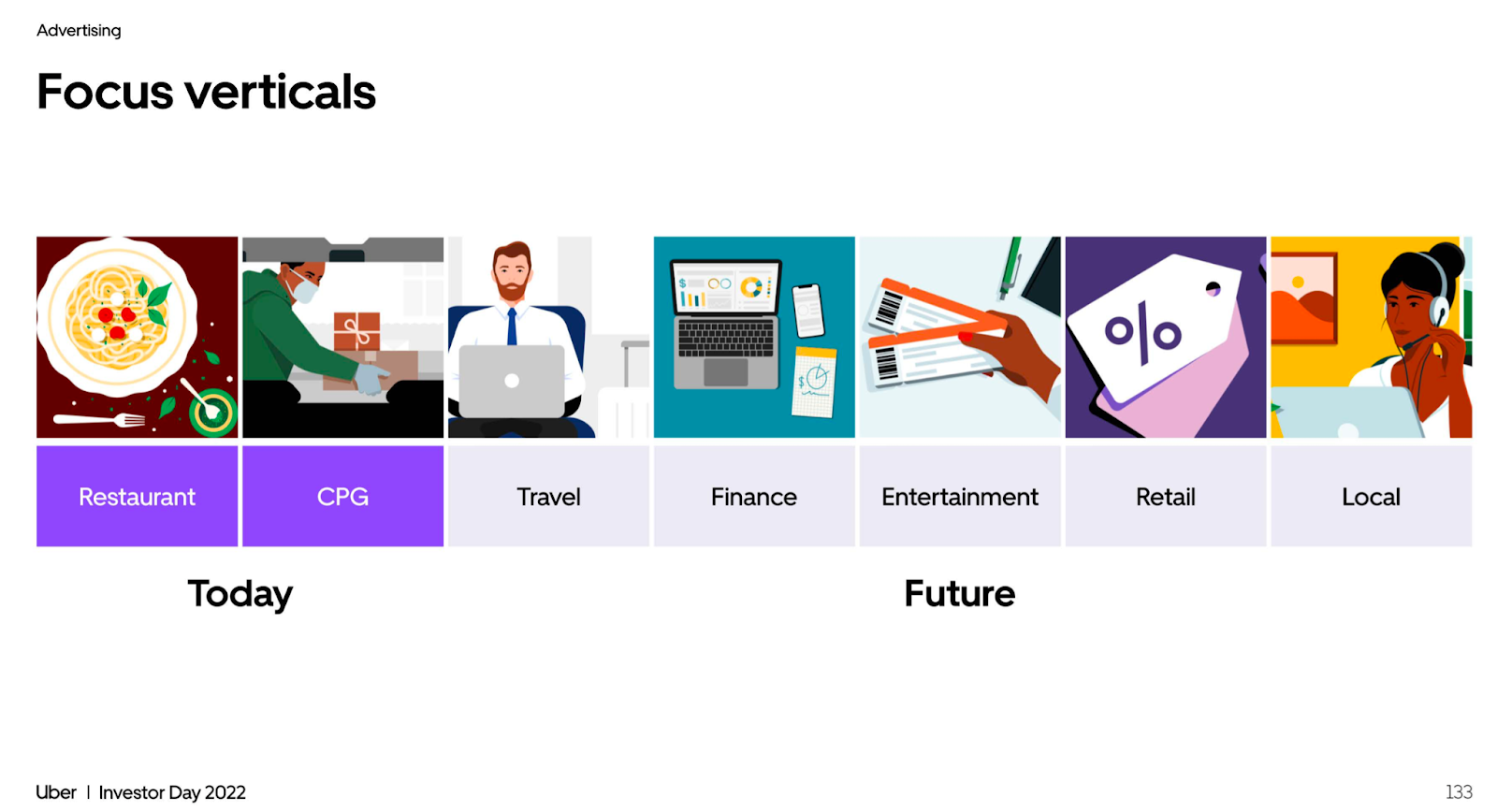

As of today, the advertising capabilities are available to more than 825,000 merchants worldwide, but Uber believes the value proposition will appeal to many verticals beyond restaurants and consumer packaged goods (CPG).

In the near future, it will be available to travel companies that can target business travelers frequently taking riders to the airport or to entertainment brands that can target those going out on a Friday evening. The opportunities are endless.

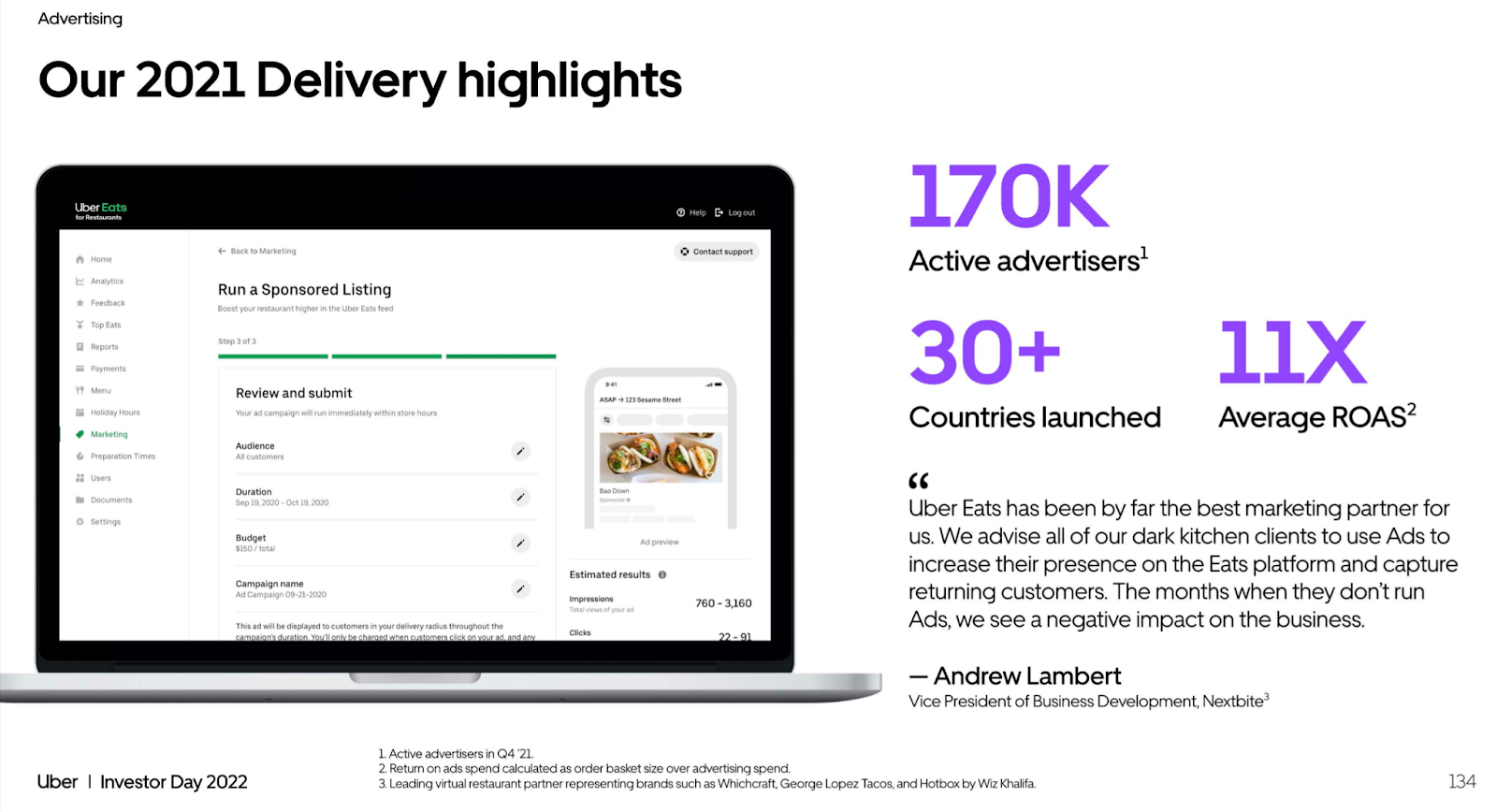

Uber Advertising was launched in 2021. The company first focused on creating a proprietary advertising platform for restaurants on the Uber Eats app. Over 170,000 advertisers from 30 countries used the platform to grow their business and saw a return of advertising spend of 11% in the fourth quarter of 2021.

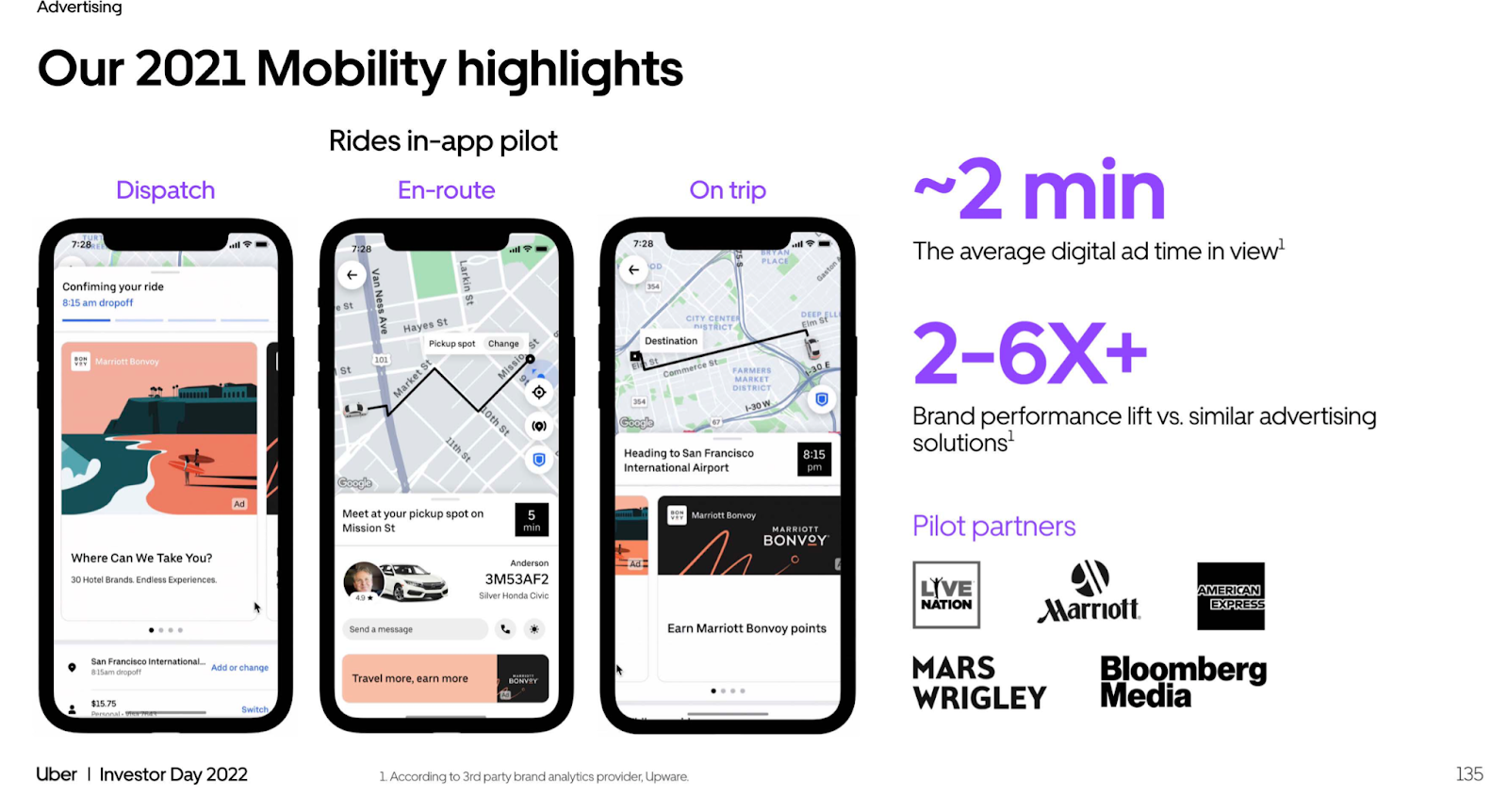

During the second half of 2021, Uber ran a pilot program on the riders' side of the advertising platform with five partners, including Marriott, American Express, Wrigley Mars, American Express, and Live Nation. The ads were placed in the app in three places: dispatch (when the ride is waiting for confirmation), en-route (before the car arrives), and on-trip (during the entire ride length).

The pilot results were fantastic: consumers were exposed to the ad content for approximately two minutes (significantly more than any other platform), resulting in a 2-6X brand performance lift.

In addition, the company launched a digital out-of-home advertising network with more than 3,000 car tops in seven US markets, delivering a hundred million daily impressions. This solution increased the driver's earnings by 20% on average.

Uber made $141 million in advertising revenue in 2021 with a run rate of $225 million for 2022. The company expects this segment to grow into a $1 billion+ revenue opportunity by 2024. This segment also has high margins that will help the company’s path to meaningful profitability in the years to come.

Business Model

Uber operates an asset-light business model whereby the company does not own a single car (or any other type of transportation), restaurant, or truck. It is one of the most disruptive business models (alongside Airbnb) out there, but at the same time, it is one of the hardest to execute which is why it’s taken them a decade-plus to build this massive ecosystem.

Uber generates substantially all of its revenue from fees paid by drivers and merchants for the use of the platform. Uber acts as an agent by connecting consumers to drivers or merchants to facilitate a trip or meal/grocery delivery service. Consumers (end-users of the services) are not customers.

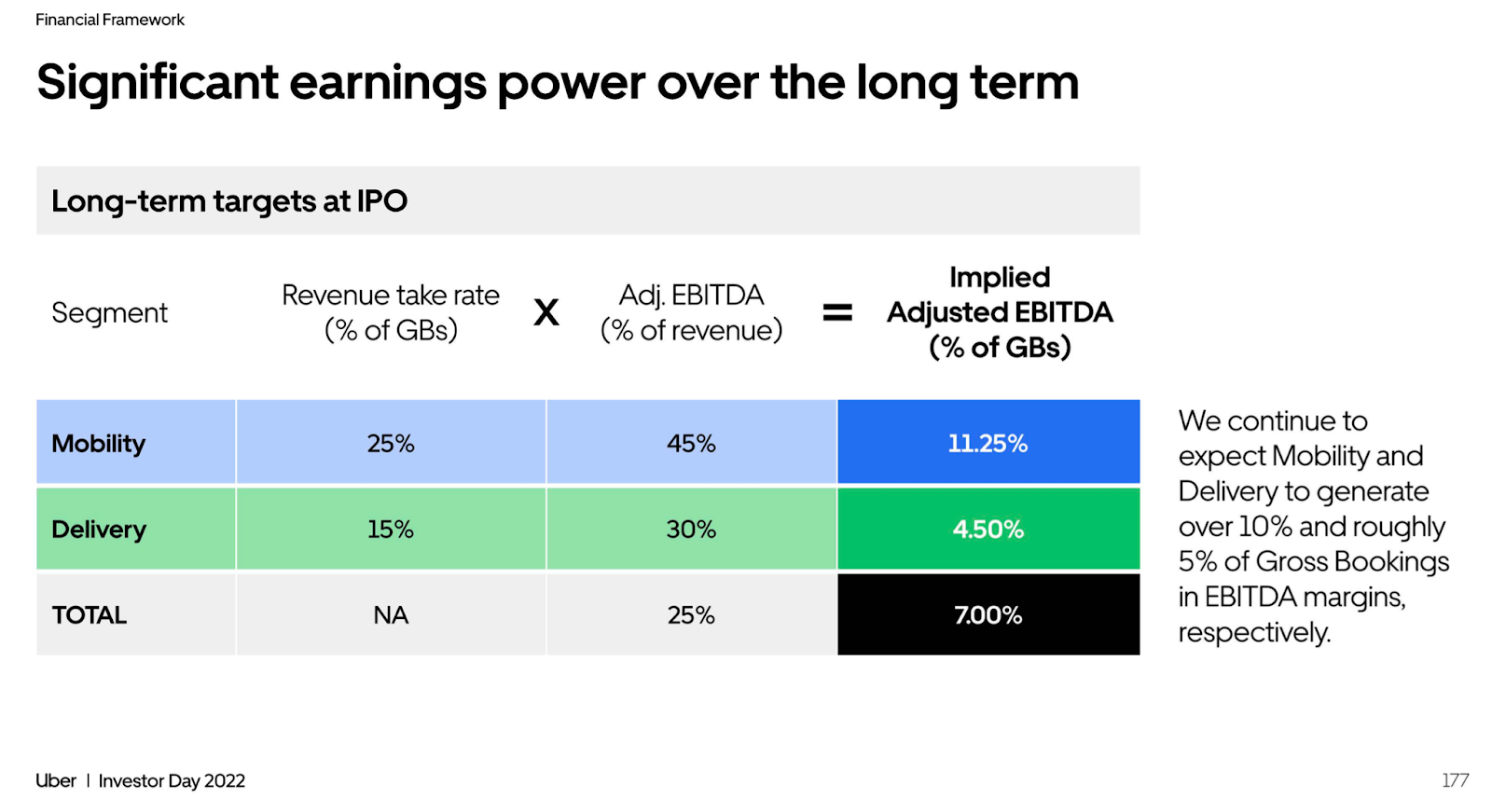

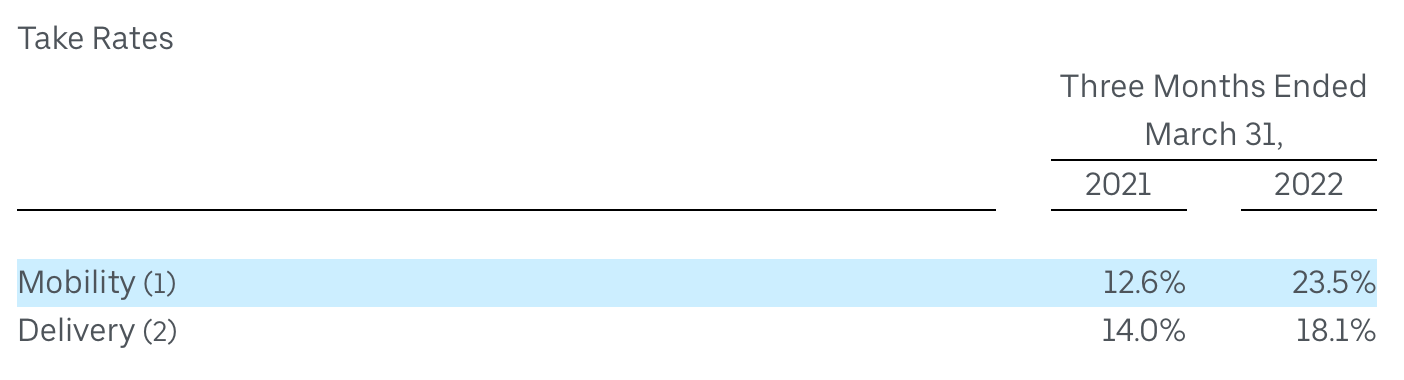

The company's revenue model is a classical representation of the commission-based revenue model. Uber charges a fixed fee for each transaction on the platform. The take rate for the mobility segment is currently 25%, and 15% for the delivery segment. The company wants to achieve a take rate of 27% for mobility and 18% for delivery in the long term.

In some markets, the company earns a fixed percentage of the end-user fare or the difference between the amount paid by an end-user and the amount earned by the driver. In such markets, the end-users are quoted a fixed upfront price for ridesharing services, while Uber pays drivers based on actual time and distance for the ridesharing services provided, calculated automatically. Therefore, the company can earn a variable amount and may realize a loss on the transaction.

Some part of the revenues come from the freight business. Uber derives this revenue from freight transportation services (fees based) provided to shippers and now also includes revenue from transportation management (fees based), which can consist of shipment planning, freight optimization, carrier assignment, load management, freight audit, payment processing, and other related transportation services. In both cases, Uber controls the service provided to customers and has obligations to transport the shipment from origin to destination. Therefore, the company is determined to be the principal in transactions instead of being an agent (like in mobility and delivery segments).

A tiny part of revenue comes from the advertising business. The company derives the majority of the advertising revenue from sponsored listing fees paid by merchants and brands in exchange for advertising on the platform. Advertising revenue is recognized when an end-user engages with the sponsored listing based on the number of clicks. Revenue is presented on a gross basis in the amount billed to merchants.

The cost of revenue (exclusive of depreciation and amortization) primarily consists of certain insurance costs related to the mobility and delivery offerings, credit card processing fees, bank fees, data center and networking expenses, mobile device and service costs, costs incurred for certain delivery transactions where the company is primarily responsible for delivery services and pay couriers for services provided, plus costs incurred with carriers for Uber Freight transportation services, amounts related to fare chargebacks and other credit card losses. The cost of revenue fluctuates on an absolute dollar basis in line with transaction volume changes on the platform.

So Uber's unit economics looks the following way: Gross Bookings (100%) – Payment to the Driver (100%-27%=73%) – Insurance and Payments (4%) – Tech Infrastructure, Support, and other Variable Costs (2%) – S&M Costs (5%) = Contribution (15%) – Fixed Costs (2%) = Adjusted EBITDA as % of Gross Bookings (13%).

"We encourage investors to assess the margin potential of our businesses as a percentage of gross bookings and set of revenues as it simplifies and improves the analysis of each segment relative to the other." – said Nelson Chai, Chief Financial Officer, on Investor Day 2022.

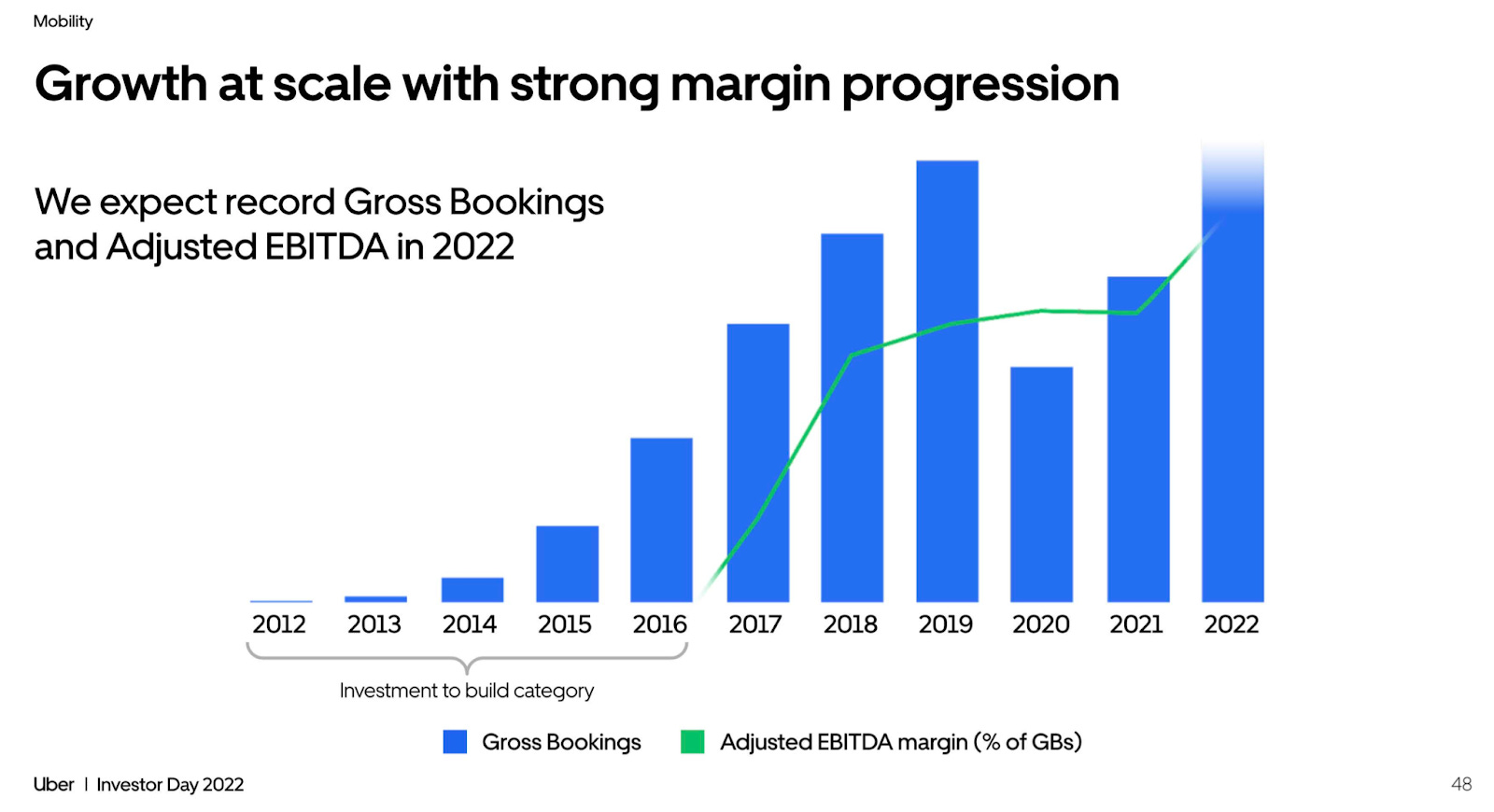

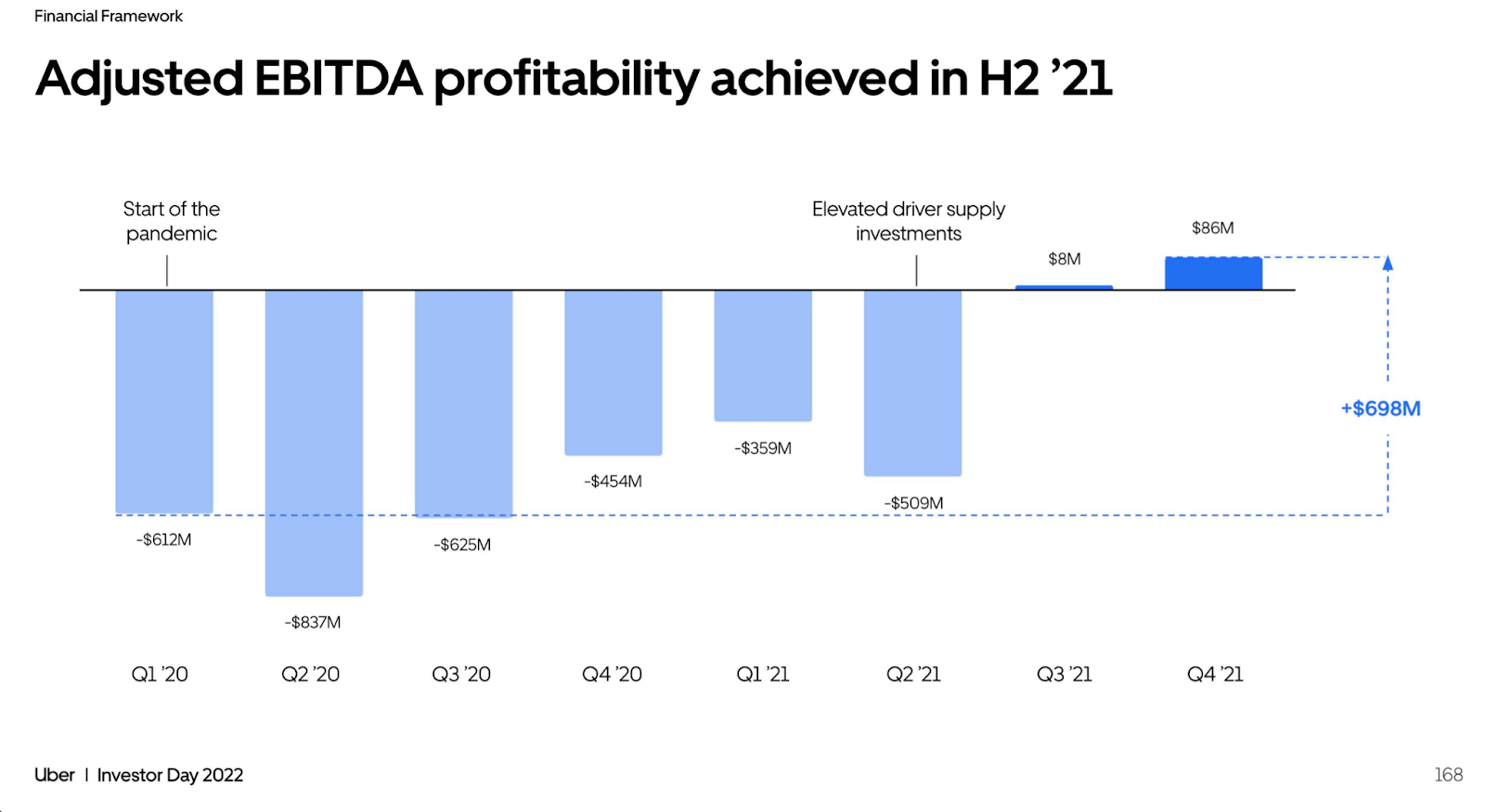

Until 2019, the business was generating deep losses (because of early and aggressive investments around the globe) before the management finally started to pivot towards profitability. The COVID-19 pandemic had a significant impact and slowed down the path to profitability. Still, the company managed to achieve a positive adjusted EBITDA in the second half of 2021, dramatically improving quarterly adjusted EBITDA by nearly $700 million since the pandemic began.

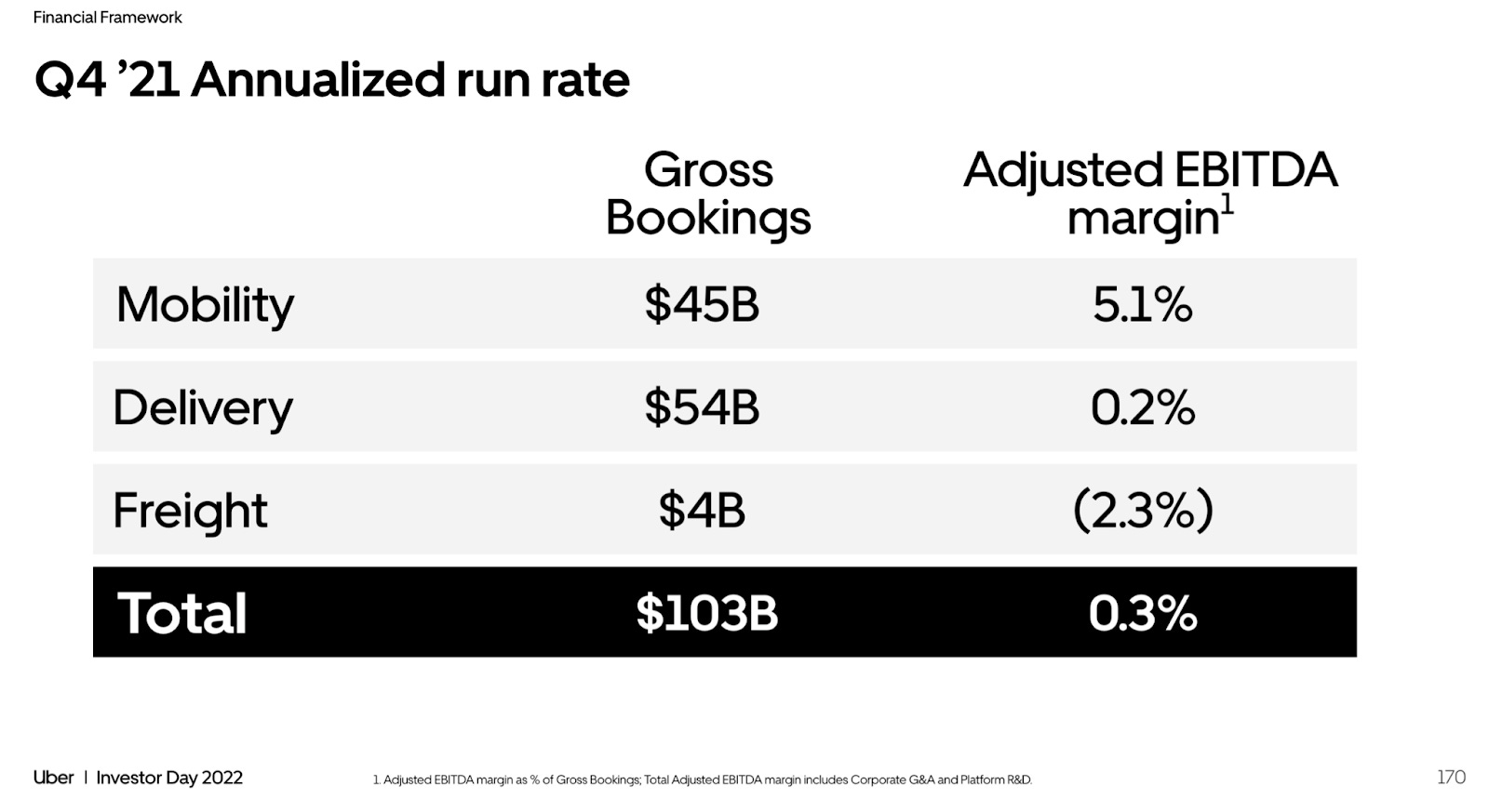

As of Q4 2021, the mobility segment was operating at a $45 billion gross bookings run rate and generating a healthy EBITDA margin of 5.1%. The delivery business reached a $54 billion gross bookings run rate in the fourth quarter and delivered its first positive EBITDA quarter ever. The freight business had a negative EBITDA, but it is on the way to becoming profitable somewhere in 2022.

The company markets its offerings through brand advertising and direct marketing. They use broad-based promotional campaigns, such as television and YouTube ads. Direct marketing primarily consists of consumer discounts, promotions, and referrals. The company attracts consumers through sponsored search, social networking sites, email marketing campaigns, and other similar initiatives. For certain products, the company engages a sales force that sells directly to businesses.

Competitive Advantages

Uber competes in several highly fragmented markets globally. The company faces significant competition in both the mobility and delivery industries globally and in the logistics industry in the United States and Canada from existing, well-established, and low-cost alternatives.

Uber focuses on global expansion and the introduction of new products and offerings across a range of industries simultaneously, while many of its competitors remain focused on a limited number of products and in a narrow geographic scope. This allows these competitors to develop specialized expertise and use resources to target specific markets better than Uber.

In the mobility segment, first and foremost, Uber competes with personal vehicle ownership and its usage, which accounts for the majority of passenger miles in the markets where Uber operates, as well as traditional transportation services, such as taxicab companies, taxi-hailing services, car hire, and other car services. Public transportation is considered to be a superior substitute to the mobility offering, and it offers a faster and lower-cost travel option in many, if not all, cities.

The company faces the following competition in each of its segments:

Apart from the competition with car ownership, traditional transportation services, and public transportation, Uber competes with other ridesharing companies such as Lyft (the primary competitor in the US and Canada), Ola (India, Australia, New Zealand, and the UK), Bolt and FreeNow (largely in Europe) as well as certain of its minority-owned affiliates such as Didi (mainly China), Grab (South East Asia), and Yandex.Taxi (Russia and CIS countries).

In the delivery segment, there is severe competition with numerous companies in the meal, grocery, and other delivery space in various regions for drivers, consumers, and merchants. Uber competes with the likes of DoorDash (US), Deliveroo (Europe), Glovo (Southern and Eastern Europe), Instacart (US), Gopuff (US, UK), Rappi (South America), iFood (South America), Delivery Hero (various countries), Just Eat Takeaway (mainly in Europe) and Amazon (various countries).

The freight business competes with global and North American freight brokers such as C.H. Robinson, Total Quality Logistics, XPO Logistics, Convoy, Echo Global Logistics, Coyote, Transfix, DHL, and NEXT Trucking.

Despite the severe competition in each of these segments and in every market where the company operates, Uber has built several competitive advantages thanks to its aggressive moves in its early days and laser focus on technology.

As a result, the company was able to build a massive ecosystem. Dara Khosrowshahi has described it perfectly: "Increasingly, it doesn't matter if your first interaction with Uber is a rideshare trip, a car rental, a scooter ride, or a grocery delivery. Once a consumer starts to use one of our services, we're able to quickly show them everything else that we can do for them. Because of this unique multi-product advantage, we can acquire customers at a lower cost and generate higher lifetime value than our competitors. People who use multiple products also spend more and retain at better rates than our own single product users. And we've really started to lean in here."

This ecosystem (when using one product, leads to using the whole suite of products that maximizes customer retention and the lifetime value of a customer) is a significant competitive advantage. There is simply no other company that can provide one-stop access to a global marketplace across mobility and delivery.

"The complementary nature between mobility and delivery that sustained us throughout the pandemic has become a powerful synergistic platform. Relative to other players that only have one line of business, our platform is giving us an advantage that's compounding over time and is getting bigger and bigger. The strategy here is pretty simple. Bring in as many new customers as we can throughout our mobility and delivery front ends, then we convert them into active cross-platform consumers and tie everything together with a first-class membership program." – Dara Khosrowshahi on the ecosystem advantage.

The technology is what makes this ecosystem thrive and another competitive advantage that Uber has. The company has built a state-of-the-art, proprietary marketplace, routing, and payment technologies. Marketplace technologies are the core of the deep technology advantage and include demand prediction, matching, dispatching, and pricing technologies. The significance of technology, or better to say innovation, is expressed in how many engineers work in the company (over 3000 people) and how much the company spends on research and development (11% of total revenue and 20% of total operating expenses in 2021). Consequently, the company can faster ramp up new offerings, grow the core, and eventually have better margins.

Technology also makes it extremely efficient to launch new businesses and operate the existing ones. Another strong competitive advantage of Uber is in launching new products and scaling them efficiently and globally. The data that comes from the marketplace help go to market faster than anyone else. Uber is the only player with this kind of a breath of data on a global scale. So Uber is best-positioned than any other company to gain the biggest slice of indeed colossal opportunity.

While it may sound controversial, Uber's brand will play a crucial role in helping the company gain more market share worldwide, and hence is another competitive advantage. This brand name became a household name in all countries where the company operates, despite lots of controversies surrounding it since its inception. When it comes to ride-hailing, Uber is the first thing that comes to mind for most consumers. The brand is becoming more trusted every year around the world, and the current management does a fantastic job rebuilding the brand image.

As a result of a strong brand name, the company can build strong partnerships with other companies that will enable new business opportunities. "We are prioritizing a partnership approach. We are convinced that partnerships are a more effective way to scale, both quicker time to market and more cost-efficient." – from the Investor Day 2022 presentation.

Finally, what makes Uber genuinely unique and may count as one more competitive advantage is that, unlike all of its competitors, which are highly unprofitable businesses, Uber is now profitable (at least on the Adjusted EBITDA basis) and on the path to generating exceptional growth and profitability (net income) in the years to come. The company expects to make $5 billion in Adjusted EBITDA in 2024 with significant free cash flow generation and net income, while most competitors likely will stay unprofitable for years, if forever.

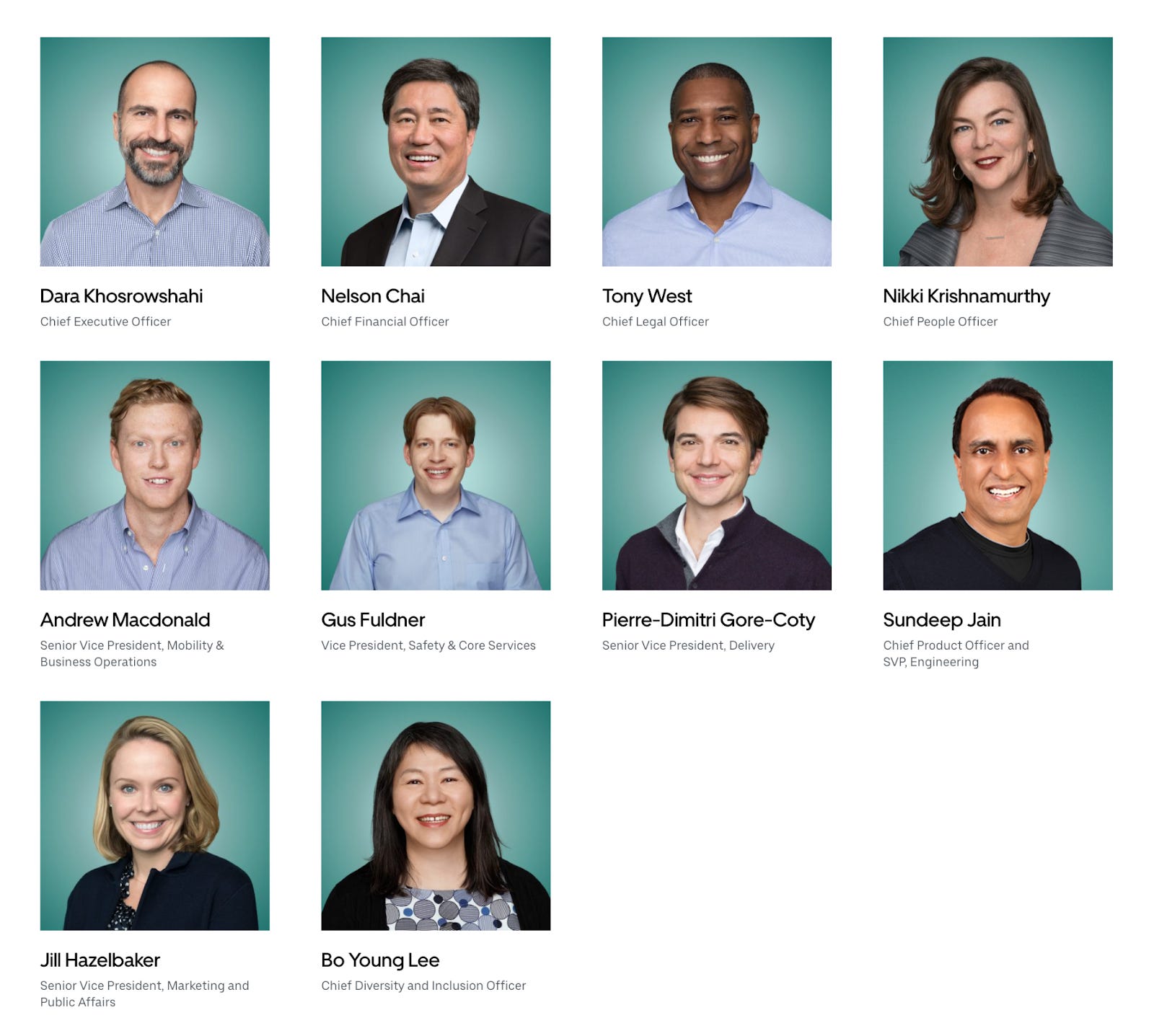

Management

Uber co-founders are no longer with the company, including the board of directors. Travis Kalanick left in 2017 and sold his last share of the company back in 2019, while Garrett Camp left the board only in March 2020 but still holds a significant amount of shares (approximately 2.5% of the entire company).

Camp backed replacing Kalanick as CEO in 2017 after being extremely upset with the company's culture and values Kalanick created and helped bring in Dara Khosrowshahi, the current CEO. "I will continue to work with Dara and the product and technology leadership teams to brainstorm new ideas, iterate on plans and designs, and continue to innovate at scale. I am looking forward to brainstorming the next big idea," said Camp at the time of leaving the board of directors.

Dara Khosrowshahi has built the leadership team from the ground, replacing all previous executives and appointing new ones. In total, the company has just five executive officers, including Dara Khosrowshahi.

Nelson Chai (CFO) Mr. Chai has served as the Chief Financial Officer since September 2018. Nelson brings more than a decade of experience in senior positions at some of the world's leading publicly traded financial services and insurance companies. He joined Uber from the Chicago-based Warranty Group, an insurance and warranty provider, where he was CEO. Previously, he spent more than 5 years at CIT Group, where he most recently served as President. Before that, he was Chief Financial Officer of Merrill Lynch & Co.; NYSE Euronext, the parent company of the New York Stock Exchange; and Archipelago Holdings, the first fully electronic stock exchange in the United States. He earned a Bachelor of Arts in economics from the University of Pennsylvania and a Master of Business Administration from the Harvard Business School.

Jill Hazelbaker (Senior Vice President, Marketing and Public Affairs) Ms. Hazelbaker has served as the Senior Vice President, Marketing and Public Affairs since June 2019. She was Senior Vice President, Communications and Public Policy from 2017 to 2019. From 2015 to 2017, Ms. Hazelbaker served as Uber's Vice President, Communications and Public Policy. Before joining Uber, Jill led communications and public policy at Snap Inc. Before Snap, Jill worked for Google, where she led communications across Europe, the Middle East, and Africa, as well as government relations in Europe. Jill began her career in US politics, having held leadership roles on many local, state, and federal election campaigns. In 2009, Jill served as Press Secretary to New York City Mayor Michael Bloomberg during his successful re-election campaign. In 2008, Jill was the National Communications Director and Chief Spokesperson for the late Senator John McCain's presidential campaign.

In 2020, Jill was named in both Fortune and AdAge's 40 Under 40 lists, recognizing her as a prominent female leader in the technology industry.

Nikki Krishnamurthy (Chief People Officer) Ms. Krishnamurthy has served as the Chief People Officer since October 2018, leading Uber's human resources, recruiting, workplace, and diversity and inclusion teams who support the company's 22,000 employees around the world. Prior to joining Uber, Ms. Krishnamurthy served as Chief People Officer of Expedia from 2016 to 2018. From 2013 to 2016, Ms. Krishnamurthy was Vice President of Expedia Local Expert, a branch of Expedia that provides online concierge services, and prior to that, she held the role of Vice President of Human Resources for Expedia from 2009 to 2013. Previously, Ms. Krishnamurthy was Principal HR Consultant for Washington Mutual Card Services from September 2007 to September 2009. She has a BA in psychology from Rutgers University.

Tony West (Chief Legal Officer) Mr. West has served as the Senior Vice President, Chief Legal Officer, and Corporate Secretary since November 2017, where he leads a global team of more than 600 in the company's Legal, Compliance and Ethics, and Security functions. Prior to joining Uber, Mr. West was Executive Vice President, Government Affairs, General Counsel, and Corporate Secretary from 2014 to 2017 at PepsiCo Inc., a food and beverage company. Tony has more than 20 years of experience in the public and private sectors. Prior to joining PepsiCo, Mr. West served as Associate Attorney General of the United States from 2012 to 2014, after previously serving as the Assistant Attorney General for the Civil Division in the US Department of Justice from 2009 to 2012. As Associate Attorney General, Tony pursued several financial institutions for their roles in precipitating the 2009 financial crisis, securing nearly $37 billion in fines and restitution for Americans who were harmed. When Tony left the Obama administration in 2014, Attorney General Eric Holder presented him with the Edmund J. Randolph Award, the Department of Justice's highest honor. From 2001 to 2009, Mr. West was a partner at Morrison & Foerster LLP. He also served as Special Assistant Attorney General at the California Department of Justice from 1999 to 2001 and, prior to that, as an Assistant United States Attorney in the Northern District of California. Tony graduated with honors from Harvard College, where he served as publisher of the Harvard Political Review, and received his law degree from Stanford Law School, where he was President of the Stanford Law Review.

Other notable members of Uber's team:

Sundeep Jain (Chief Product Officer and SVP Engineering) Mr. Jain has served as Chief Product Officer and SVP Engineering since 2018. He is responsible for the company's global Mobility and Delivery products, including engineering, product management, design, data science, and product operations. Before joining Uber, Sundeep was Vice President of Product Management at Google within the Search Ads group, where he worked on connecting users' commercial intent with advertisers, including quality, pricing, and user experience. Sundeep also worked on enabling local commerce by connecting users with local advertisers across both maps and search. Earlier in his career, Sundeep was Vice President at Zynga and a founder of a tech startup that was acquired by FIS, a public company with a $100 billion enterprise value. Sundeep earned a Bachelor of Science in Computer Engineering from UC Berkeley with the highest honors and a Masters of Business Administration from Harvard Business School, where he was a Baker Scholar.

Pierre-Dimitri Gore-Coty (Senior Vice President, Delivery) Mr. Gore-Coty has been with Uber since 2012, when he joined the company as the General Manager of France, launching Paris, Uber's first international city. As one of the earliest team members, he scaled Uber across Europe before taking on the challenge of international expansion. He now brings his experience and expertise to Uber Eats and the company's grocery and other on-demand delivery offerings. He oversees business strategy and operations in more than 6,000 cities across 45+ countries. Prior to this role, he served as the Vice President of Uber's ride-hailing business outside of North America.

Andrew Macdonald (Senior Vice President, Mobility & Business Operations) Mr. Macdonald has also been with Uber since 2012, starting as a general manager in Toronto, Canada. He is now responsible for the company's global ridesharing operations and other mobility businesses, including public transit partnerships and micro-mobility. Andrew also oversees core business functions, including business development and corporate (B2B) offerings. Uber is a continuation of Andrew's startup ambitions, as he founded two startups in the years before his time at Uber. Prior to entrepreneurial pursuits, Andrew was a management consultant with Bain & Company.

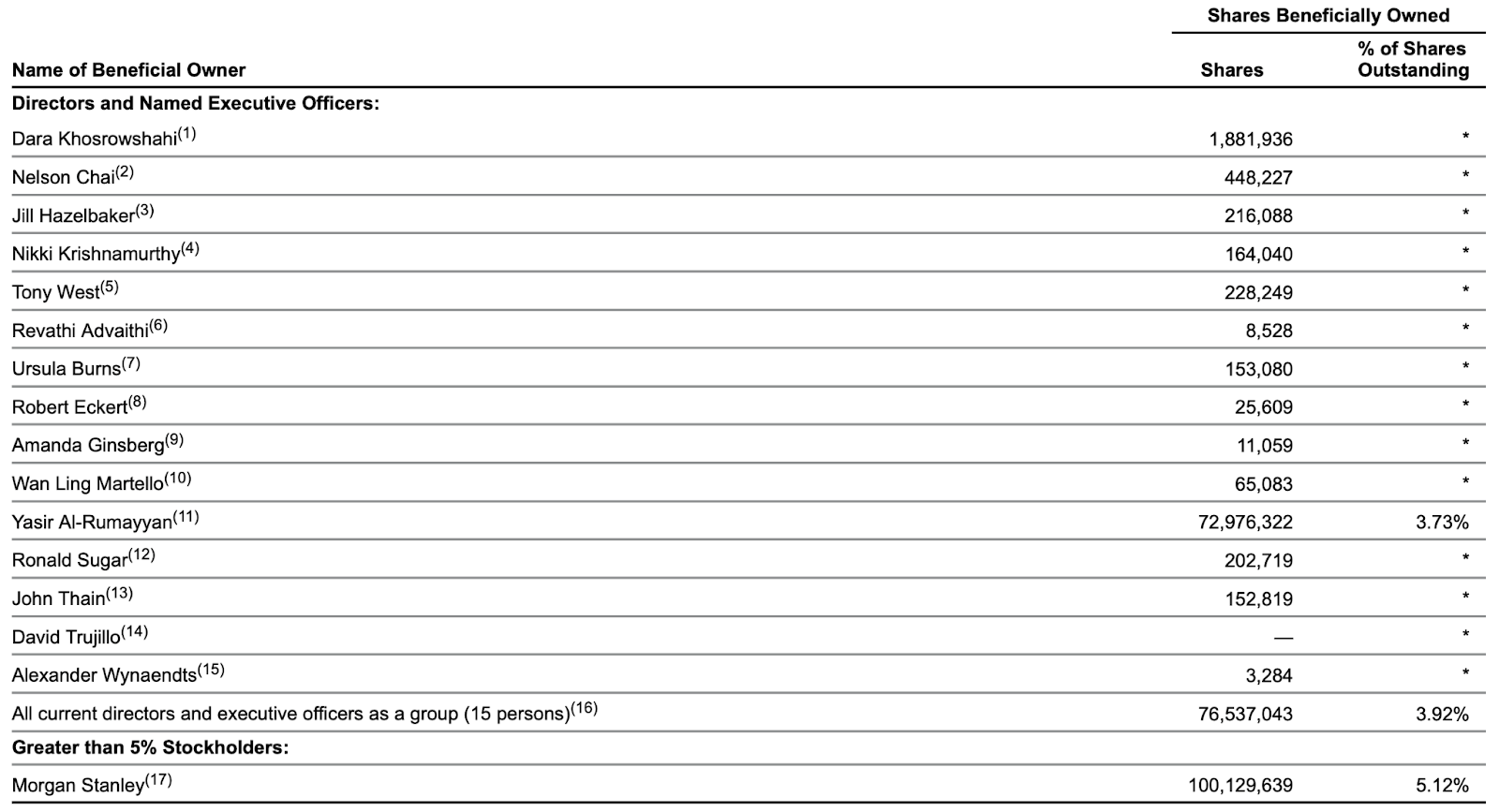

The board of directors has also changed since Dara Khosrowshahi took over, except for one member – Yasir Al-Rumayyan, a Governor of the Public Investment Fund, a sovereign wealth fund of the Kingdom of Saudi Arabia, who is a large investor in Uber. The company brought independent directors, who, unlike the previous group that was brought and supported by Kalanick, could not influence any decisions in the company.

The company also divided the roles of Chairperson and Chief Executive Officer and appointed Dr. Sugar as independent Chairperson. Furthermore, the company replaced the supervoting structure with a one-share, one-vote structure.

Uber's board is well-diversified and owner-oriented, as all members except one hold shares directly or indirectly.

Culture

Uber is most likely the best example of a company that had neglected the culture for so many years, which eventually turned into a disgrace and led to substantial changes in the company afterward.

Fast forward to today, Uber is most likely the best example of a company that cares about the culture so much that they even have a leadership role of a Chief Diversity and Inclusion Officer in the company.

Bo Young Lee leads Uber's diversity and inclusion efforts in the company. She partners with senior leadership, including Dara Khosrowshahi, to build a work culture where radically diverse and inclusive teams drive innovation, accelerate growth, and build a work culture and systems where all employees have the opportunity to excel and grow to their highest potential.

The leadership team has sought to reform the culture fundamentally by improving the governance structure, strengthening the compliance program, creating and embracing new cultural norms, committing to diversity and inclusion, and rebuilding the relationships with employees, drivers, consumers, cities, and regulators.

The new leadership committed to building a best-in-class compliance program and, since then, made tremendous progress in creating a program that is designed to prevent and detect violations of corporate policy, culture, law, and regulations.

Uber's mission has evolved over these years to reflect the changes the new management made and how the business itself advanced.

"We reimagine the way the world moves for the better" is the company's mission today. Uber employees call themselves go-getters, the kind of people who are relentless about the mission to help people go anywhere and get anything and earn their way.

The company works towards this mission based on eight cultural norms. These values reflect who the Uber employees are and where they are going. They guide their decision-making, unite and define Uber's culture, and tell a story to the world about Uber's corporate purpose.

We do the right thing. Period.

Go get it. Bring the mindset of a champion. Our ambition is what drives us to achieve our mission. How we define a champion mindset isn't based on how we perform on our best days, it's how we respond on our worst days. We hustle, embrace the grind, overcome adversity, and play to win for the people we serve. Because it matters.

Trip obsessed. Make magic in the marketplace. The trip is where the marketplace comes to life. The earner, rider, eater, carrier, and merchant are the people who connect in our marketplace - and we see every side. This requires judgment to make difficult trade-offs, blending algorithms with human ingenuity and the ability to create simplicity from complexity. When we get the balance right for everyone, Uber magic happens.

Build with heart. We care. We work at Uber because our products profoundly affect lives, and we care deeply about our impact. Putting ourselves in the shoes of people who connect in our marketplace helps us build better products that positively impact our communities and partners. Our care drives us to perfect our craft.

Stand for safety. Safety never stops. We embed safety into everything we do. Our relentless pursuit to make Uber safer for everyone using our platform will continue to make us the industry leader in safety. We know the work of safety never stops, yet we can and will challenge ourselves to always be better for the communities we serve.

See the forest and the trees. Know the details that matter. Building for the intersection of the physical and digital worlds at a global scale requires seeing the big picture and the details. Knowing the important details can change the approach, and small improvements can compound into enormous impact over time.

One Uber. Bet on something bigger. It's powerful to be a part of something bigger than any one of us or anyone team. That's why we work together to do what's best for Uber, not the individual or team. We actively support our teammates, and they support us - especially when we hit the inevitable bumps in the road. We say what we mean, disagree and commit, and celebrate our progress, together.

Great minds don't think alike. Diversity makes us stronger. We seek out diversity. Diversity of ideas. Identity. Ethnicity. Experience. Education. The more diverse we become, the more we can adapt and ultimately achieve our mission. When we reflect on the incredible diversity of the people who connect on our platform, we make better decisions that benefit the world.

One more change in Uber's public image worth mentioning came when the company announced its commitment to become a fully zero-emission platform by 2040, with 100% of rides taking place in zero-emission vehicles, on public transit, or with micro-mobility. The management has set an earlier goal to have 100% of rides in electric vehicles (EVs) in US, Canadian, and European cities by 2030. It is a very ambitious target that speaks for how drastically the company is different from what it was a few years ago under Kalanick's helm. In addition to the platform goals, new management committed to reaching net-zero emissions from the corporate operations also by 2030.

"As the largest mobility platform in the world, we know that our impact goes beyond our technology. We want to do our part to build back better and support a green recovery in our cities and communities." – Dara Khosrowshahi, CEO of Uber.

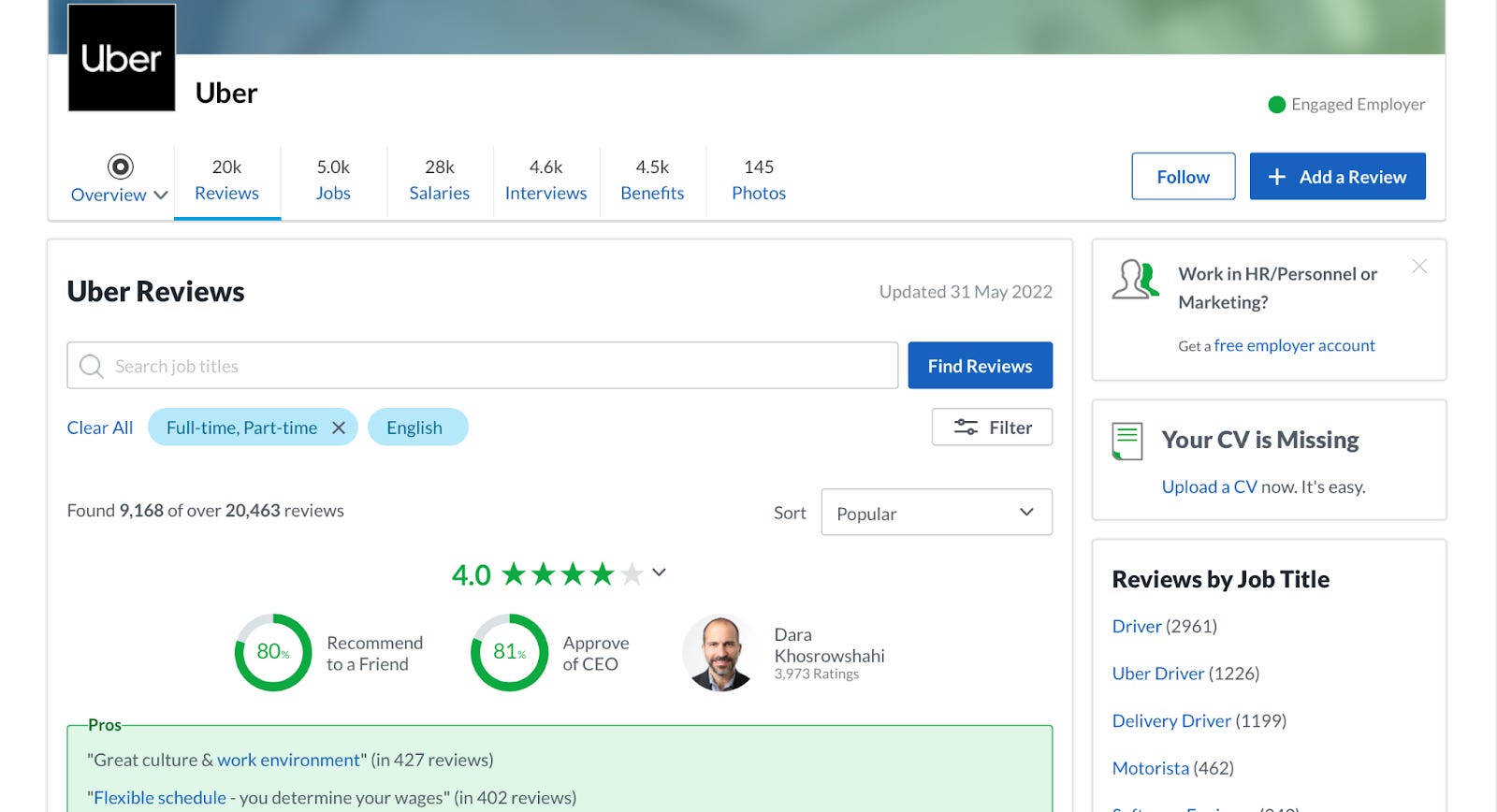

Uber as a company has transformed beyond recognition. Something that was really hard even to imagine a few years back. No wonder why the company and the new CEO have very high ratings both on Glassdoor and Comparably.

The company has a solid 4.0 / 5 rating on Glassdoor based on more than 20,000 reviews (the highest number I have seen so far). Dara Khosrowshahi has a high CEO approval rating of 81% based on almost 4000 reviews. Recommend to a Friend metric is also considerably high. To confirm the words about the culture, notice how many times the words 'great culture' and 'work environment' are included in the reviews.

An even greater picture is on Comparably. Uber has an outstanding rating of 4.7 / 5 (A+) based on more than 11,000 ratings. Dara Khosrowshahi has a rating of 88 / 100, putting him in the top 5% of 1338 similar sized companies on Comparably. Uber has won 4 awards in 2022 and 10 awards in 2021: from Best HR Team 2022 and Best Global Culture 2022 to Best Company Outlook 2022 and Best CEO 2021.

Uber also won rewards from other sources: BuiltIn (100 Best Large Companies to Work 2022, SF Best Places to Work 2022, Chicago Best Places to Work 2022) and Human Rights Campaign (Best Places to Work for LGBTQ Equality 2022).

Headquartered in San Francisco, California, the United States, the company and its subsidiaries employ approximately 29,300 employees globally.

Financials

All information in this section is based on the financial performance of Uber in its most recent quarter (Q1 2022), reported on May 4, 2022.

"Our results demonstrate just how much progress we've made navigating out of the pandemic and how the power of our platform is differentiating our business performance," said Dara Khosrowshahi, CEO of Uber. "In April, Mobility Gross Bookings exceeded 2019 levels across all regions and use cases. There's never been a more exciting time to innovate at Uber and we're focused on executing our strategy to grow our platform profitably."

"We are pleased with our Q1 results, with the outperformance of our quarterly guidance and strong incremental margins," said Nelson Chai, CFO of Uber. "With free cash flow approaching breakeven in Q1, we now expect to generate meaningful positive free cash flows for full-year 2022."

Income Statement

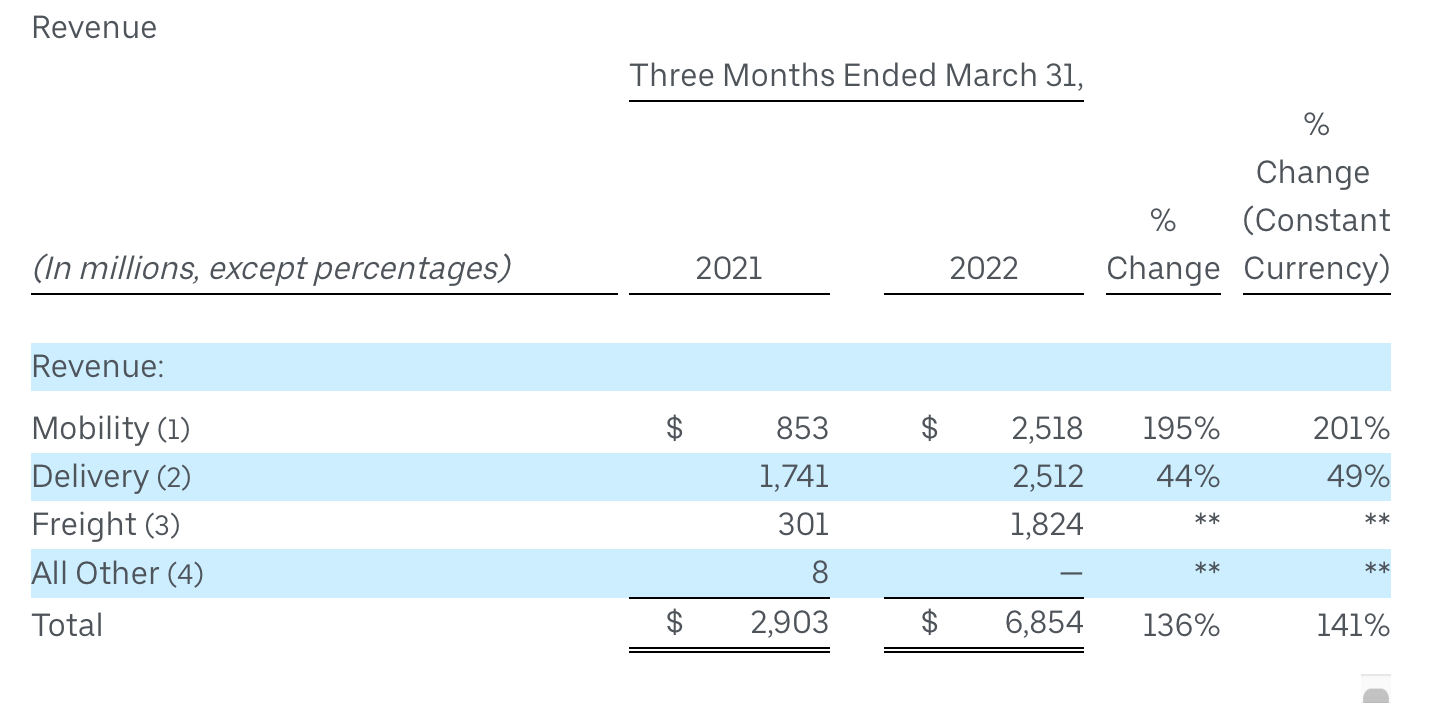

Revenue

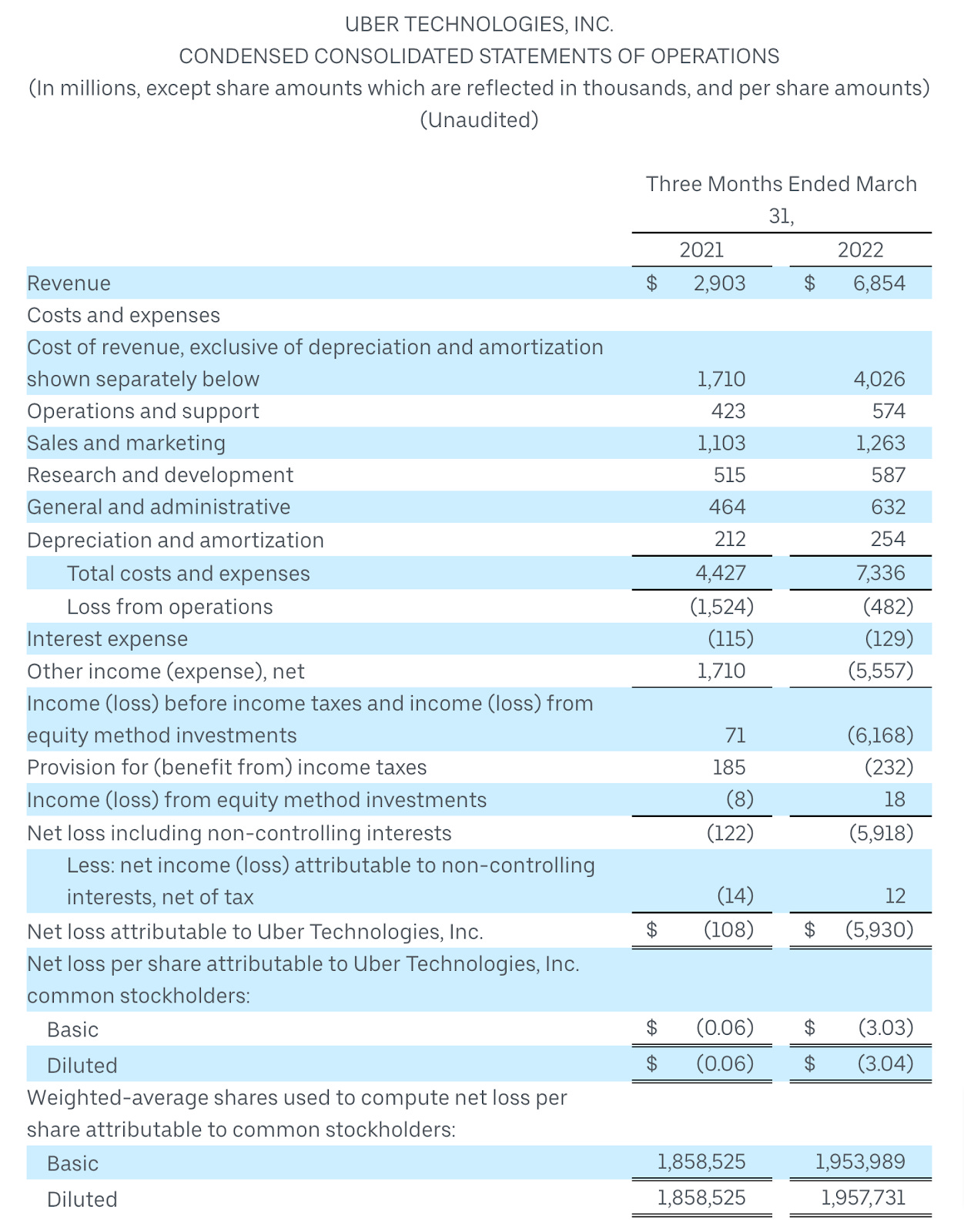

Revenue grew 136% YoY to $6.9 billion, with revenue growth significantly outpacing Gross Bookings growth primarily due to the acquisition of Transplace by freight, a change in the business model for the UK mobility business, and an easier comparison in Q1 2021 due to the accrual for historical claims in the UK.

Mobility revenue grew to $2.5 billion, an 11% QoQ and 195% YoY increase.

Delivery revenue grew to $2.5 billion, a 4% QoQ and 44% YoY increase.

Freight revenue grew to $1.8 billion, a 69% QoQ and 506% YoY increase (attributable to combined Uber Freight and Transplace performance).

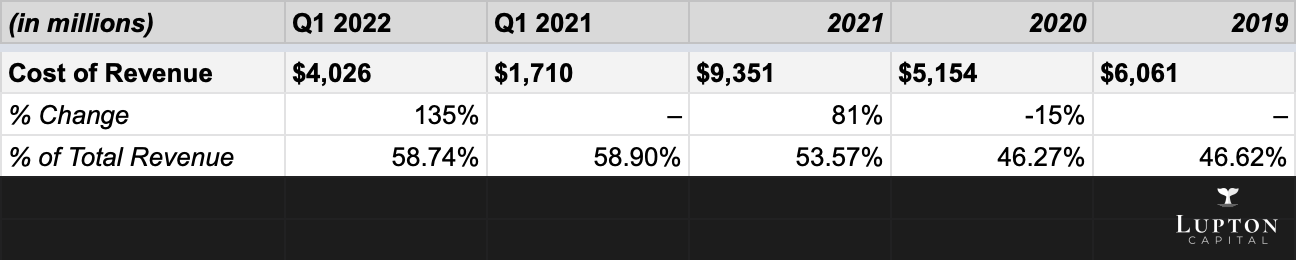

Cost of Revenue

The cost of revenue in Q1 2022 increased by 135% compared to the quarter a year prior, but this growth is in line with the revenue growth.

As a percentage of total revenue, it remains at the same level.

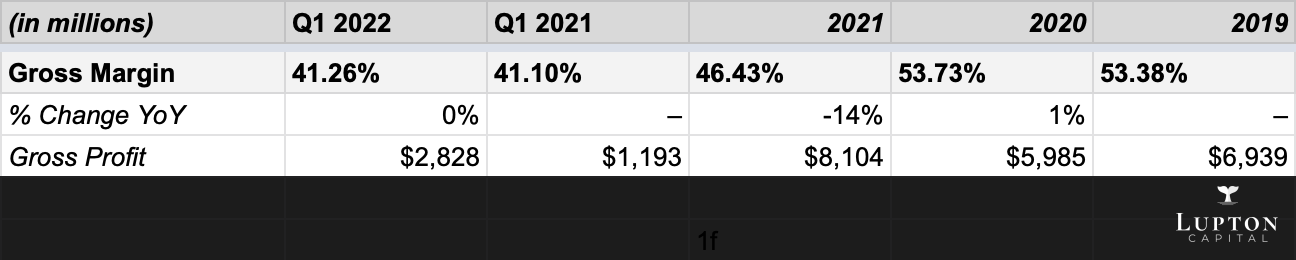

Gross Margin

The gross margin in Q1 2022 stayed flat (41%) compared to Q1 2021.

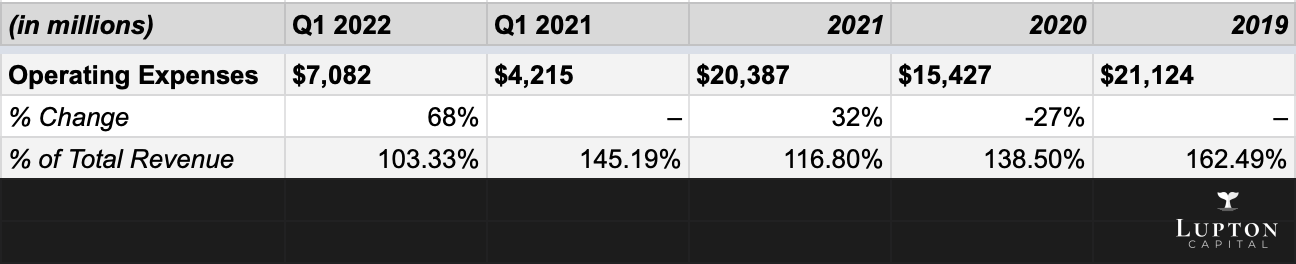

Operating Expenses

In Q1 2022, operating expenses grew 68% to $7 billion and represented 103% of total revenue. It is a significant improvement of 4200 basis points compared to Q1 2021.

Sales and marketing expenses as a percentage of Gross Bookings decreased due to improved cost leverage, with Gross Bookings growth outpacing sales and marketing expense growth. Additionally, the Gross Bookings mix shifted towards mobility, which carries lower associated sales and marketing costs.

General and administrative expenses as a percentage of Gross Bookings also decreased due to improved fixed cost leverage.

Guidance

The company provided guidance for Q2 2022:

Gross Bookings of $28.5 billion to $29.5 billion

Adjusted EBITDA of $240 million to $270 million

The company does not provide guidance for the entire year.

Profitability

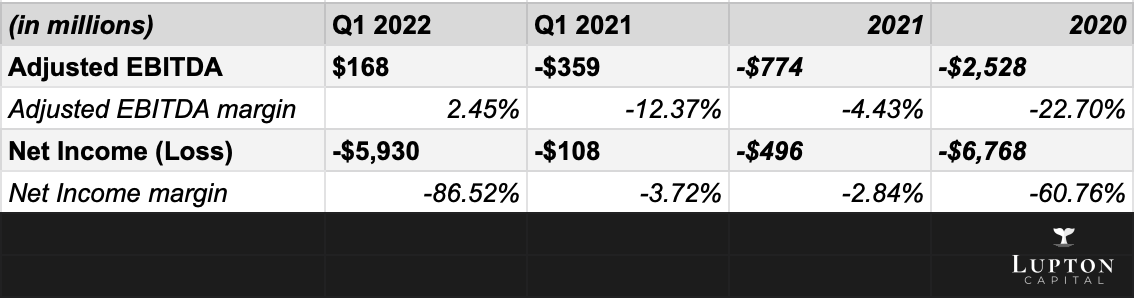

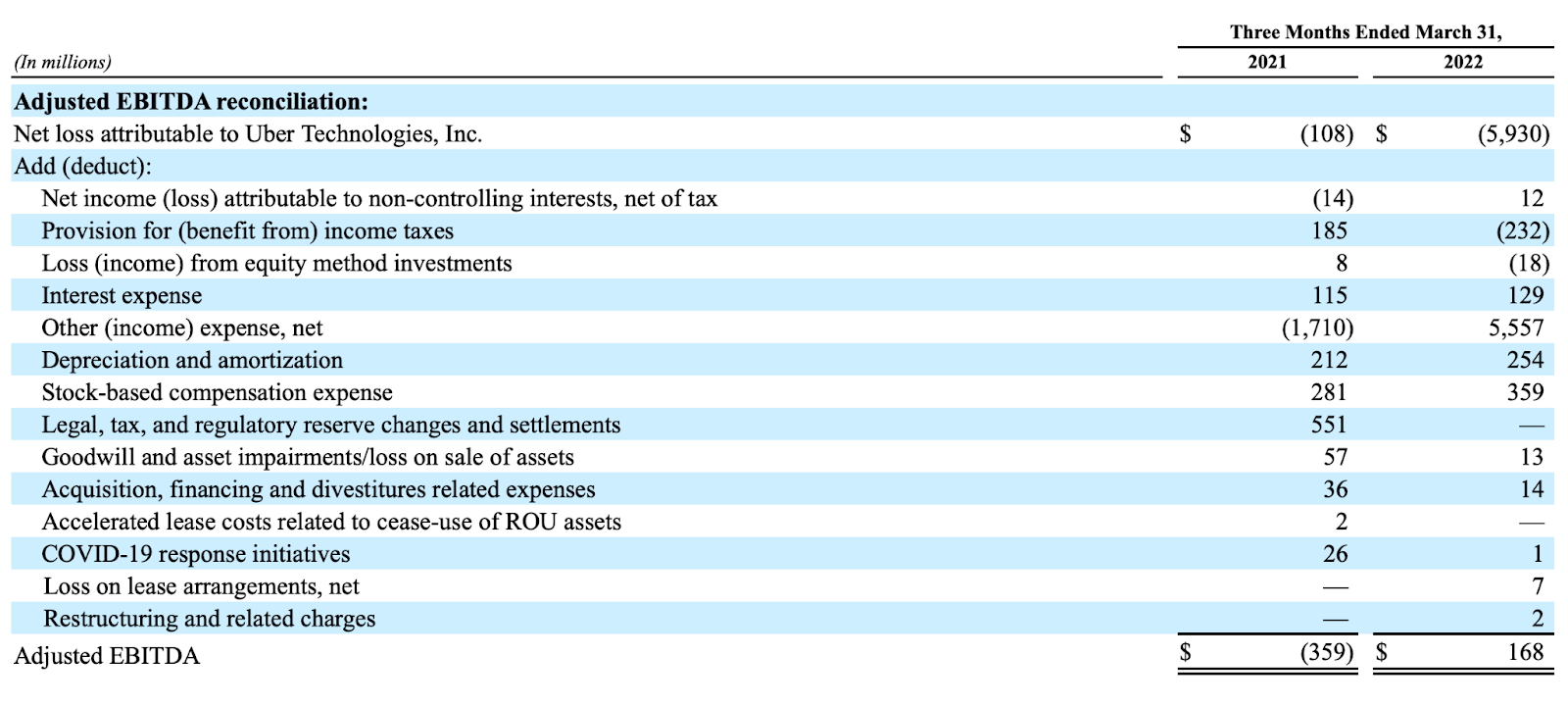

Adjusted EBITDA in Q1 2022 was $168 million, up $527 million year-over-year. Adjusted EBITDA margin as a percentage of Gross Bookings was 0.6%, up from (1.8)% in Q1 2021.

Net loss was $5.9 billion, which includes a $5.6 billion headwind (pre-tax) relating to Uber's equity investments, primarily due to aggregate unrealized losses related to the revaluation of Uber's Grab, Aurora, and Didi stakes. Additionally, the net loss includes $359 million in stock-based compensation expenses.

The company became profitable on an Adjusted EBITDA basis but is still deep in losses on Net Income (Loss) basis.

Balance Sheet

The company ended Q1 2022 with $4.2 billion in unrestricted cash and cash equivalents.

There is a long-term debt of $9.2 billion on the balance sheet. "We are taking every opportunity to improve our debt in terms of the amount of both extending and reducing the debt." – said Nelson Chai, CFO of Uber, on the Q1 2022 earnings call.

Cash Flow

Cash flow from operations was $15 million, up $626 million YoY.

Cash flow from investing in Q1 2022 came in as an outflow of $135 million, mainly due to the purchase of property and equipment and the acquisition of other businesses.

Cash flow from financing in Q1 2022 came in as an outflow of $113 million, mainly due to the principal payments on finance leases.

Free cash flow, defined as net cash flows from operating activities less capital expenditures, was an outflow of $47 million, improving $635 million YoY.

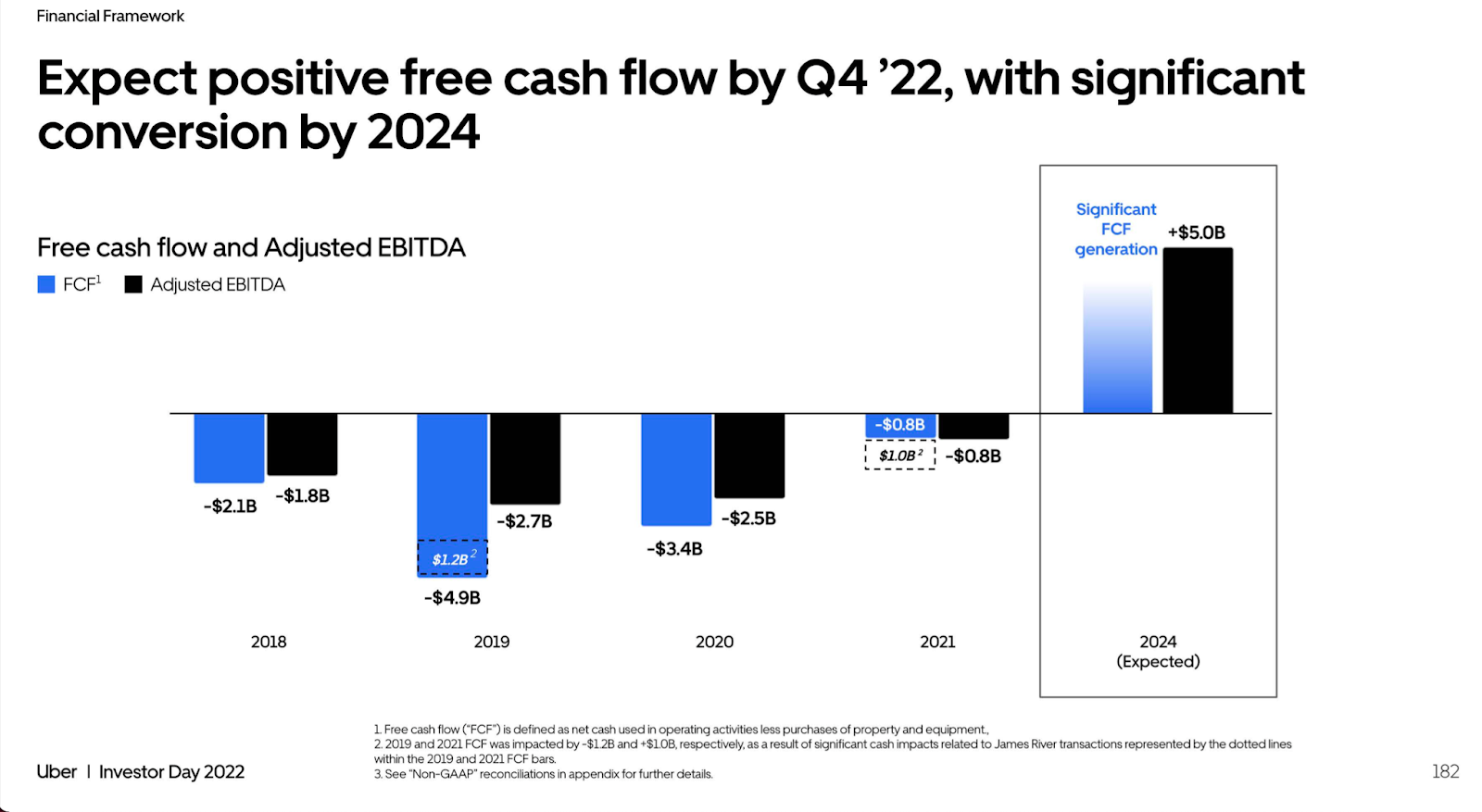

"In 2022, we expect to generate meaningful EBITDA. As such, we expect to turn free cash flow positive by the end of this year. By 2024, we expect strong free cash flow generation. So this brings us to a new chapter in Uber's history." – said Nelson Chai, CFO of Uber, on Investor Day 2022.

Key Metrics

The company tracks certain key metrics and non-GAAP financial measures to evaluate the business's health and assess its performance.

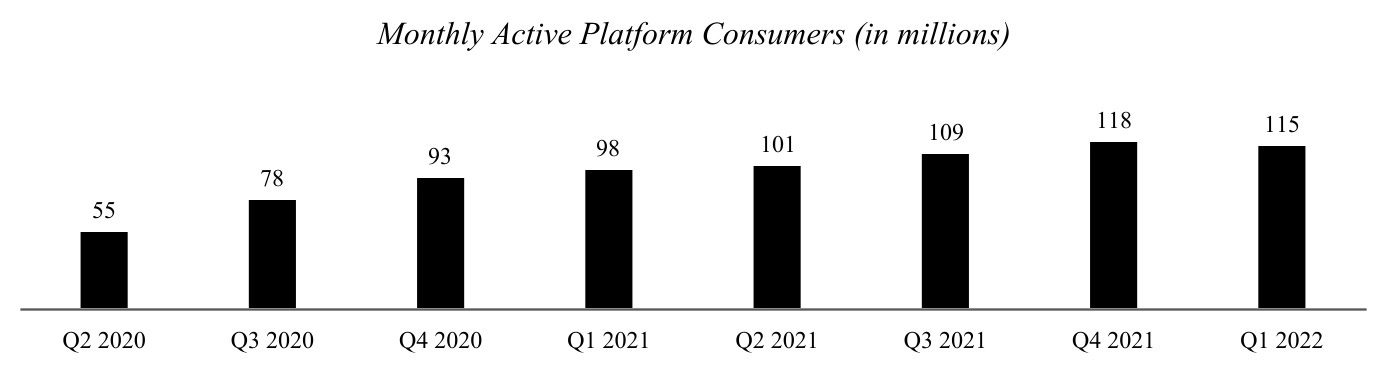

Monthly Active Platform Consumers (MAPC)

MAPCs is the number of unique consumers who completed a mobility or new mobility ride or received a delivery order on the platform at least once in a given month, averaged over each month in the quarter.

While a unique consumer can use multiple product offerings on the platform in a given month, that unique consumer is counted as only one MAPC.

Management uses MAPCs to assess the platform's adoption and frequency of transactions, which are key factors in the penetration of the countries in which the company operates.

MAPCs increased 17% YoY to 115 million, reaching 121 million in March 2022 with rapidly increasing consumer activity, compared to 118 million in Q4 2021. However, MAPCs declined 3% QoQ related to a slower start to the quarter due to Omicron impacts.

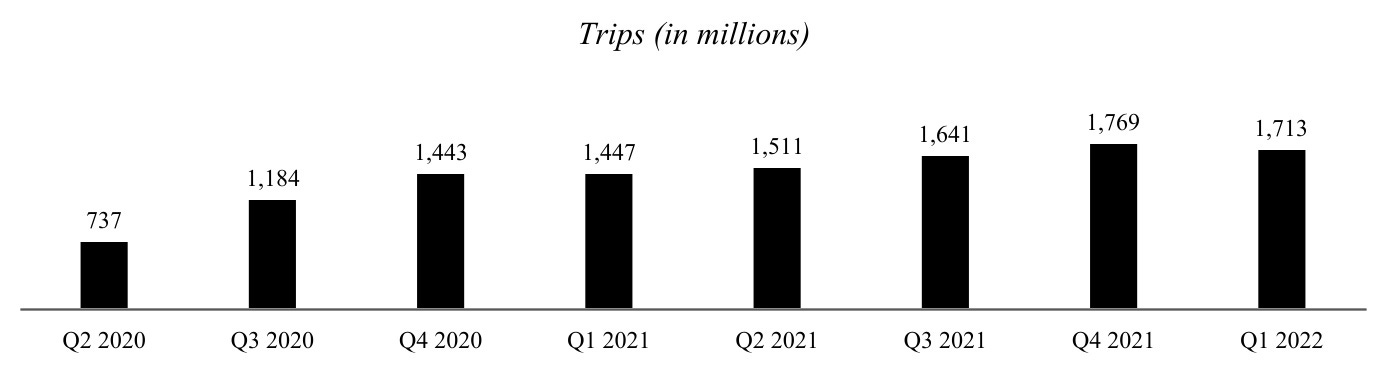

Trips

Trips is the number of completed consumer mobility or new mobility rides and delivery orders in a given period.

For example, an UberX Share ride with three paying consumers represents three unique Trips, whereas an UberX ride with three passengers represents one Trip.

Management believes that Trips are a useful metric to measure the scale and usage of the platform.

Trips on the platform grew to 1.7 billion in Q1 2022 (18% YoY). However, Trips declined 3% QoQ due to Omicron's impacts on mobility demand early in the quarter.

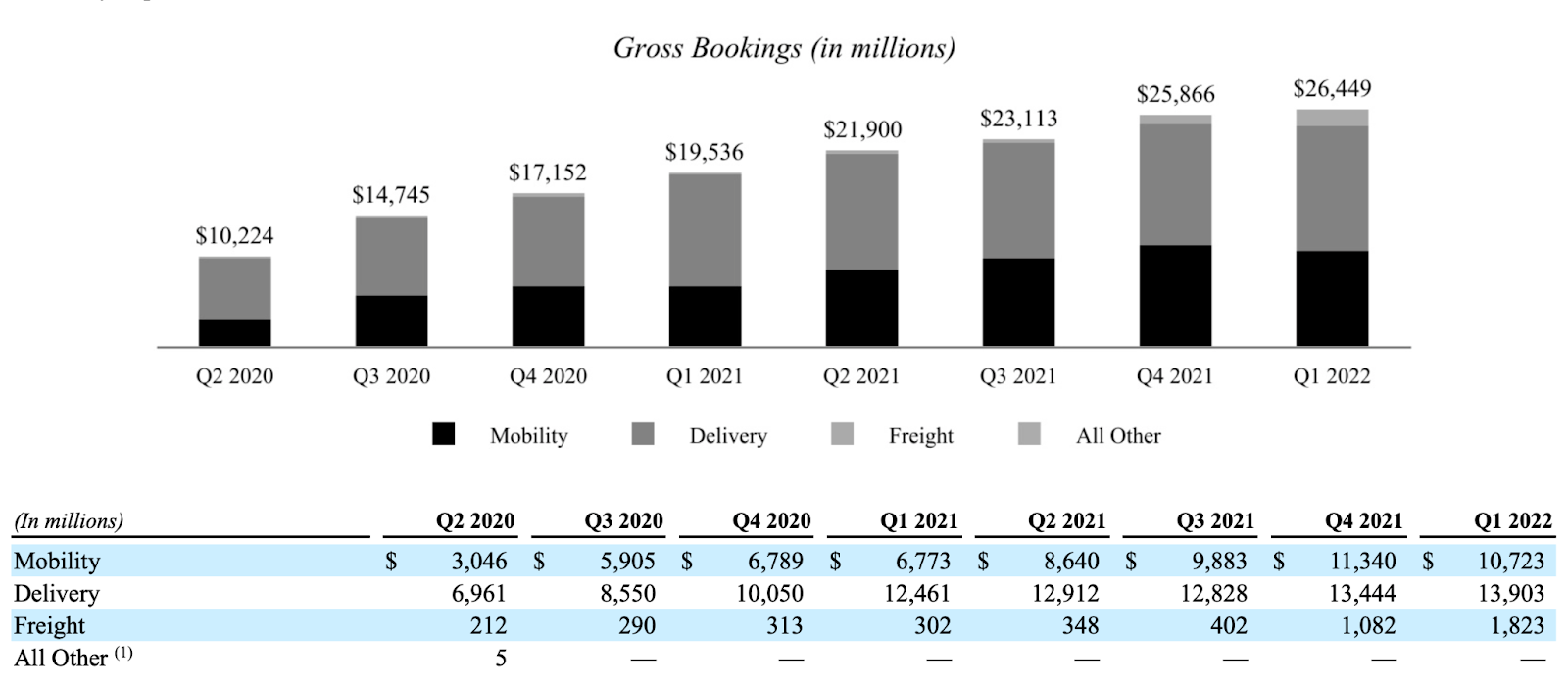

Gross Bookings

Gross Bookings is the total dollar value, including any applicable taxes, tolls, and fees, of:

Mobility and new mobility rides;

Delivery orders (in each case without any adjustment for consumer discounts and refunds);

Driver and merchant earnings;

Driver incentives;

Freight revenue.

Gross Bookings do not include tips earned by drivers. Gross Bookings indicate the scale of the current platform, which ultimately impacts revenue.

Gross Bookings grew 35% year-over-year to $26.4 billion, with Mobility Gross Bookings of $10.7 billion (+58% YoY) and Delivery Gross Bookings of $13.9 billion (+12% YoY).

Take Rate

Take Rate is an operating metric and defined as revenue as a percentage of Gross Bookings.

Mobility Take Rate of 23.5% increased 340 bps QoQ and 10.9 percentage points YoY.

Delivery Take Rate of 18.1% grew 10 bps QoQ and 410 bps YoY.

Adjusted EBITDA

The company defines Adjusted EBITDA as net income (loss), excluding

income (loss) from discontinued operations, net of income taxes;

net income (loss) attributable to non-controlling interests, net of tax;

provision for (benefit from) income taxes;

income (loss) from equity method investments;

interest expense;

other income (expense), net;

depreciation and amortization;

stock-based compensation expense;

certain legal, tax, and regulatory reserve changes and settlements;

goodwill and asset impairments/loss on sale of assets;

acquisition, financing, and divestitures related expenses;

restructuring and related charges;

other items not indicative of our ongoing operating performance, including COVID-19 response initiatives.

Adjusted EBITDA is a key measure used by the management team to evaluate the operating performance, generate future operating plans, and make strategic decisions, including those relating to operating expenses.

"We believe that Adjusted EBITDA provides useful information to investors and others in understanding and evaluating our operating results in the same manner as our management team and board of directors. In addition, it provides a useful measure for period-to-period comparisons of our business, as it removes the effect of certain non-cash expenses and certain variable charges." – from the latest 10-Q report.

However, Adjusted EBITDA has a number of limitations that have to be taken into consideration when accessing the real financial performance of the company.

Risks

The company has some critical risks related to business, legal and regulatory risks, and some other risks.

COVID-19

The coronavirus pandemic has adversely impacted and could continue to adversely impact the business, financial condition, and results of operations.

When the pandemic hit, the demand for mobility offerings had been drastically reduced. Furthermore, the company experienced and expects to continue to experience driver supply constraints. In some regions, the shared rides offering continues to be temporarily suspended.

The COVID-19 pandemic has adversely affected the near-term financial results and may adversely impact the long-term financial results, which has required and may continue to require significant actions in response, including additional reductions in the workforce (happened in Q1 2022) and certain changes to pricing models of the offerings, all in an effort to mitigate such impacts.

Any future "waves" or resurgences of the outbreak or variants of the virus, both globally and within the United States, will further impact the company and slow down its growth.

Drivers classification

The business would be adversely affected if drivers were classified as employees, workers, or quasi-employees. The classification of drivers is currently being challenged in courts, legislators, and government agencies in the United States and abroad.

The company is currently involved in numerous legal proceedings globally. The company may not successfully defend drivers' classification in some or all jurisdictions.

The company has already paid approximately $372 million for individual settlement agreements to more than 150,000 drivers in the United States who have entered into arbitration agreements with the company.

If the company is required to classify drivers as employees, workers, or quasi-employees, this may impact the current financial statement presentation, including revenue, cost of revenue, incentives, and promotions.

Competition

The mobility, delivery, and logistics industries are highly competitive, with well-established and low-cost alternatives that have been available for decades, as well as low barriers to entry, low switching costs, and well-capitalized competitors in nearly every major geographic region.

If the company is unable to compete effectively in these industries, the business and financial prospects would be adversely impacted.

In addition, to remain competitive in certain markets, the company needs to continue to lower fares or service fees and offer significant driver incentives and consumer discounts and promotions, which has adversely affected and may continue to adversely affect the financial performance.

Profitability

The company has incurred significant losses since its inception. They are still losing money on a Net Loss basis despite announcing reaching profitability on an Adjusted EBITDA basis.

The company will continue to incur losses in the near term as a result of substantial increases in operating expenses as the company continues to heavily invest across all segments.

The real profitability is several years away and may move further than 2024, as expected by the company.

Debt

As of December 31, 2021, the total outstanding indebtedness is $9.4 billion. In addition, up to approximately $238 million of Careem Convertible Notes remain subject to future issuance to Careem stockholders.