$SOFI - SoFi Technologies

Below is the writeup that I sent to paid subscribers on July 16th — I have not changed anything.

This newsletter is sponsored by Interactive Brokers which is the only investing/trading platform that I currently use. Interactive Brokers doesn’t have the glitz and glamour of other platforms but I like the simplicity, user interface and speed of execution. Putting in orders is quick and easy which is important for me. Learn more at InteractiveBrokers.com

1) Follow me on Twitter where I share some daily investment content [click here]

2) Signup for my Stocktwits room [click here]

3) Signup for Fintrics to help with valuations and price targets [click here]

4) Subscribe to my YouTube channel where I post my CEO interviews [click here]

5) Signup for the “FinTwit Conference” in October [click here]

$SOFI - SoFi Technologies

Stock symbol: $SOFI

Prior SPAC symbol: $IPOE

Website: SoFi.com

Stock price: $15.99

Market cap: $13.8 billion

Enterprise value: $16.0 billion

Sector: Financial Services

Founders: Daniel Macklin, Ian Brady, James Finnigan, Michael Cagney

CEO: Anthony Noto [click here]

CFO: Chris Lapointe [click here]

CMO: Lauren Stafford Webb [click here]

Founded: August 2011

VC Funding: $3 billion [click here]

SPAC merger announced: January 2021 [click here]

First day as public company: June 2021 [click here]

Headquarters: San Francisco, California

Employees: 2,000+

Phone: 855-456-7634

Investor relations: ir@sofi.com

Investor presentation [click here]

2021 Q1 earnings presentation [click here]

2020 Q4 earnings presentation [click here]

Form S-1 [click here]

Form 10-K [click here]

Form 10-Q [click here]

$IPOE announces plans to merge with SoFi [click here]

$SOFI completes SPAC merger with $IPOE [click here]

CEO speaking at Piper Sandler Global Exchange & FinTech Conference [watch here]

SoFi announces acquisition of Golden Pacific Bancorp [click here]

CEO interview on CNBC talking about the $SOFI platform [watch here]

SoFi launches credit cards [click here]

SoFi announces early access to IPOs for members [click here]

Signup for the daily $SOFI podcast [click here]:

$SOFI - SoFi Technologies

INTRODUCTION:

$SOFI is a relatively new position for me because I waited until after the SPAC merger with $IPOE was finalized in early June and then $SOFI started trading under it’s own ticker. The second day $SOFI was trading on it’s own it rallied up to $24.95 and then it’s been tumbling downhill ever since as you can see from this chart — in fact 14 of the past 18 days have been red days (ie traded down).

I started buying $SOFI when it pulled back to $21 thinking we had found some support and the stock did bounce for a few days but then the sellers came in and it’s been ugly every since — including lockup expiration.

Given the past 3 weeks of horrible price action I believe the stock now looks extremely compelling on a risk/reward basis. I don’t see much more downside (although anything is possible) yet I do see the potential for 100% upside over the next 18 months if the company continues to execute really well, grow the customer base, get the national bank charter, launch new products, increase the ARPU and so on.

As the stock has been sliding the past few weeks I’ve continued to build my position (currently at 6.5%) while lowering my cost basis which now sits at $17 per share. In full disclosure if we do get a rally in $SOFI over the next few weeks going into Q2 earnings which is set for August 12th, I’ll probably trim back my position to a 5% weighting in my portfolio. I’m a little overweight in $SOFI right now because I think the stock is oversold and therefore due for a bounce (it was up 3% yesterday).

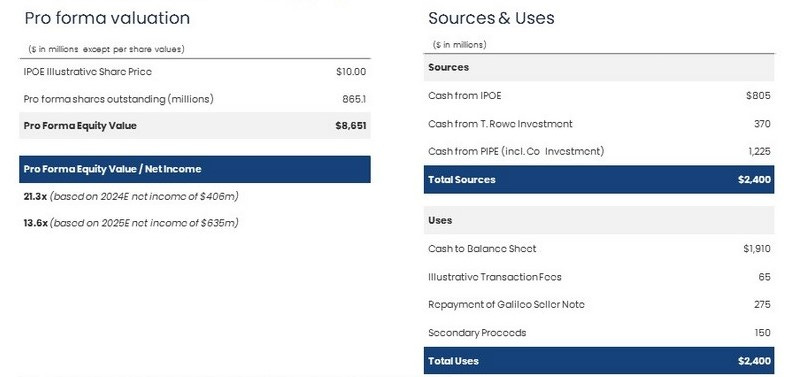

SPAC TRANSACTION:

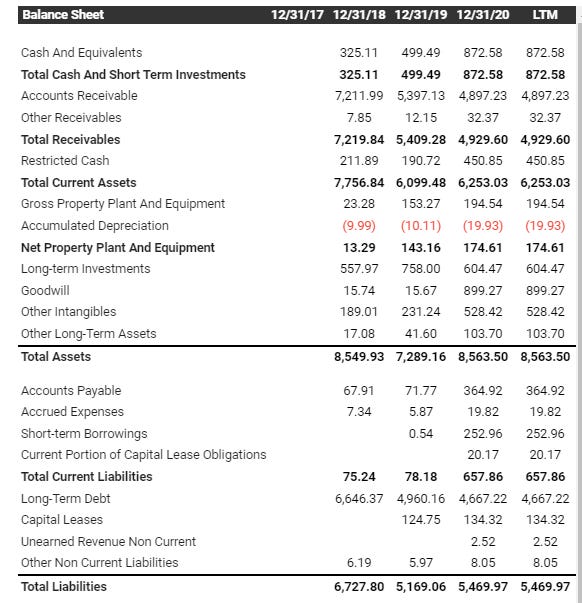

Since I already mentioned that $SOFI came public via SPAC ($IPOE) let’s get the transaction details out of the way. When the deal was announced earlier this year the market cap (not including cash) was $8.6 billion with 865 million shares outstanding. With the stock now trading at $15.99 it puts the current market cap at $13.8 billion. Between cash in the SPAC trust and the PIPE it added approximately $2.4 billion to the balance sheet however $SOFI has $4.6 billion in long term debt as you can see from the chart below so this puts the current enterprise value at $16.0 billion.

MARKET OPPORTUNITY:

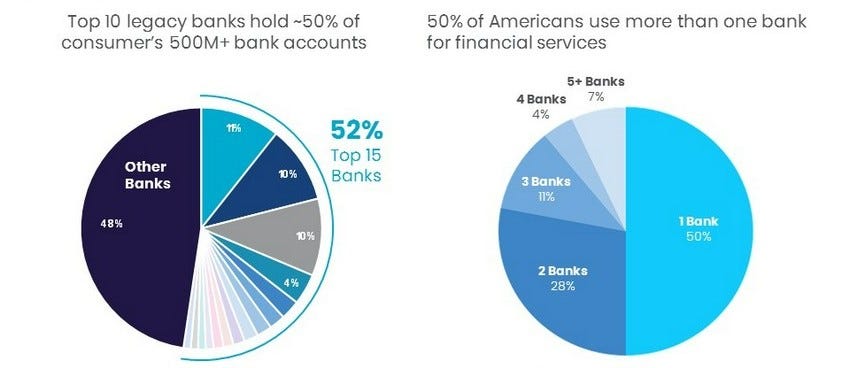

Normally I would start off by giving an overview of the company but before I do that I want to discuss the size of banking industry where $SOFI wants to compete.

According to $SOFI’s investor presentation the top 10 banks like JP Morgan ($JPM), Citigroup ($C), Bank of America ($BAC), Wells Fargo ($WFC) hold 50% of the accounts however 50% of American’s use more than one bank. This tells me that consumers can’t get everything they need from their primary bank so they are forced to have multiple relationships — $SOFI is trying to change this by creating a “one stop shop” for financial products and services so they can build long-lasting relationships with their customers (they actually call them members).

Here’s a chart showing the top 15 US banks and their total assets (which is typically based on deposits/loans)

50 largest US banks [click here]

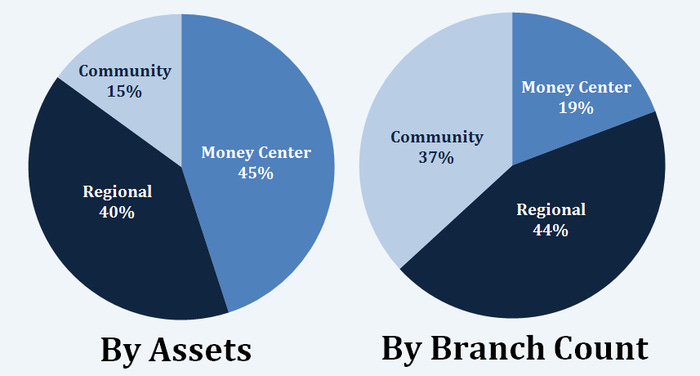

If you breakdown the banking industry into 3 segments this is what it looks like — money center banks (thousands of branches) are large national banks like JP Morgan and Bank of America, regional banks (hundreds of branches) are smaller like Huntington Bank and M&T Bank and then community banks are the smallest (dozens of branches) which typically serve rural towns and counties.

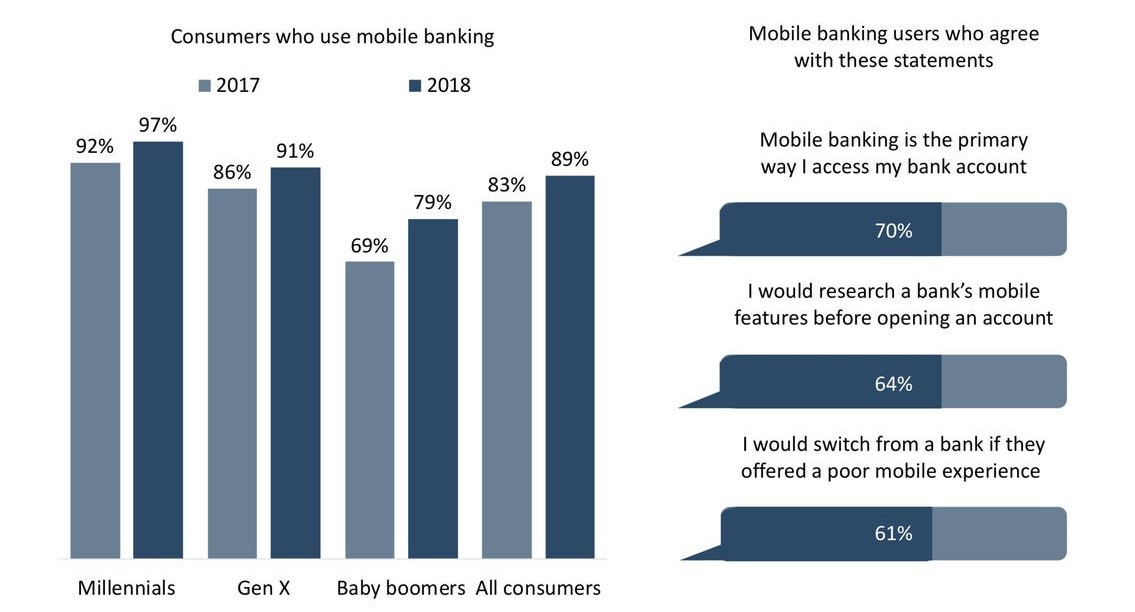

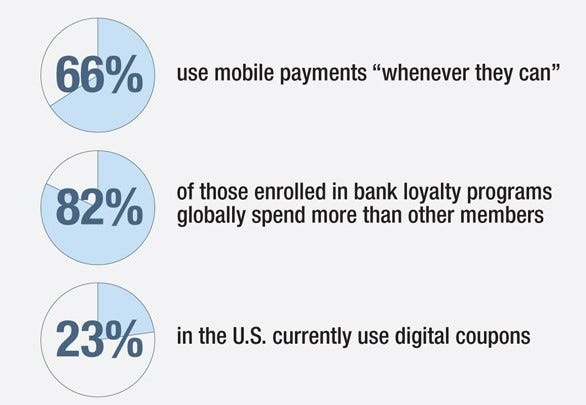

As you can see from this chart, based on data from 2019, there are just under 77,000 bank branches in the U.S. however this number has been declining for the past decade as “neobanks” like $SOFI have been taking market share thus making it too expensive for traditional brick & mortar banks to keep operating all of their branches.

Even though the data below is few years old (so the numbers are even higher now), it just proves the overwhelming majority of US adults (even the baby boomers) have adapted to mobile banking which means the companies like $SOFI that are able to build a digital-first banking company will be well positioned in the future. They won’t be strapped down with expensive real estate and limited by the locations of their bank branches.

OVERVIEW:

In the section above shared some large numbers in terms of the US banking industry but that was just to tease you because as we’ll get into very soon $SOFI isn’t a real banking company (yet) however they’ve applied for their national bank charter license so this could be a nice catalyst on the horizon.

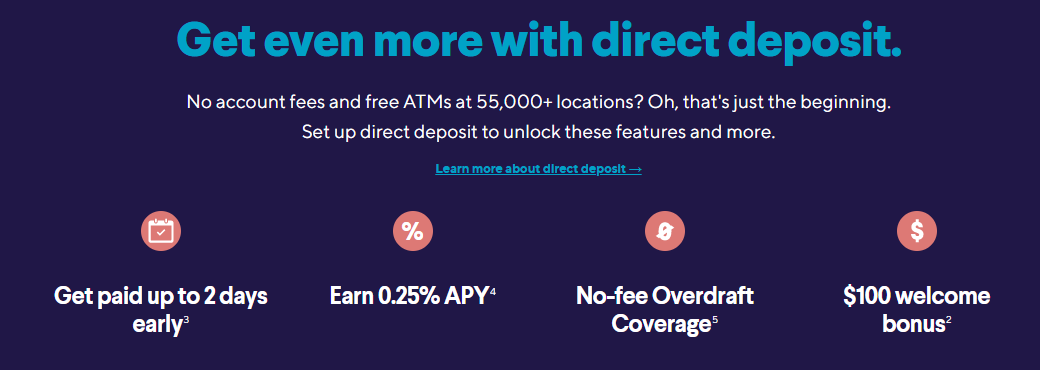

$SOFI does have SoFi Money but it’s technically a brokerage product offered by SoFi Securities — I bet 99% of $SOFI customers don’t even know the difference. SoFi Money is a cash management account that offers competitive rates, no account fees, no ATM fees, direct deposit, early access to paychecks and overdraft protection. Learn more about SoFi Money [click here]

The fact that $SOFI is not a bank is mostly irrelevant to customers — however it matters to $SOFI because once they get their national bank charter they’ll have the ability to do lending (underwrite loans) off customer deposits.

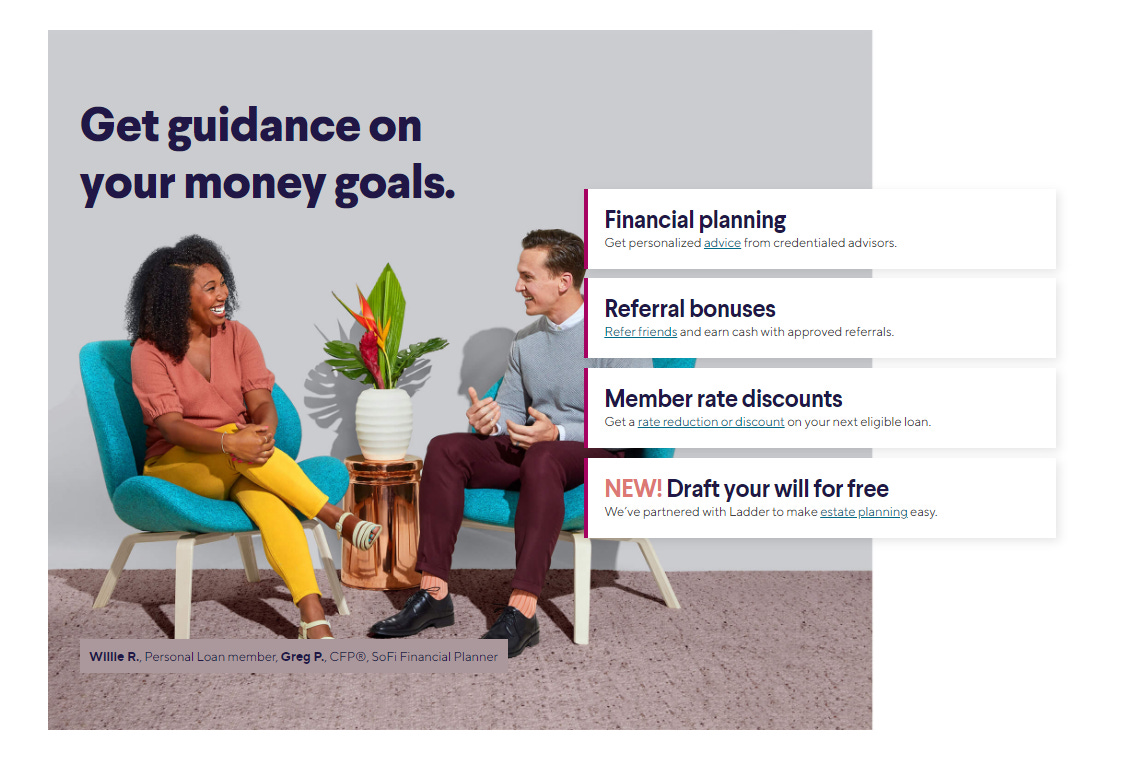

Even thought $SOFI is not a bank, they are still a “one-stop-shop” financial services company doing everything including cash management, lending, credit cards, credit building, investing and much more. As a matter of fact, $SOFI even provides free access to Certified Financial Planners — because they want all of their customers/members to have access to high-quality financial advice.

Once $SOFI gets their national bank charter license they will be the ideal prototype “digital bank of the future” meaning they’ll be able to offer dozens of different financial products and services to their millions of members without the need for physical branches. The other term used to describe “digital banks” is neobanks or challenger banks.

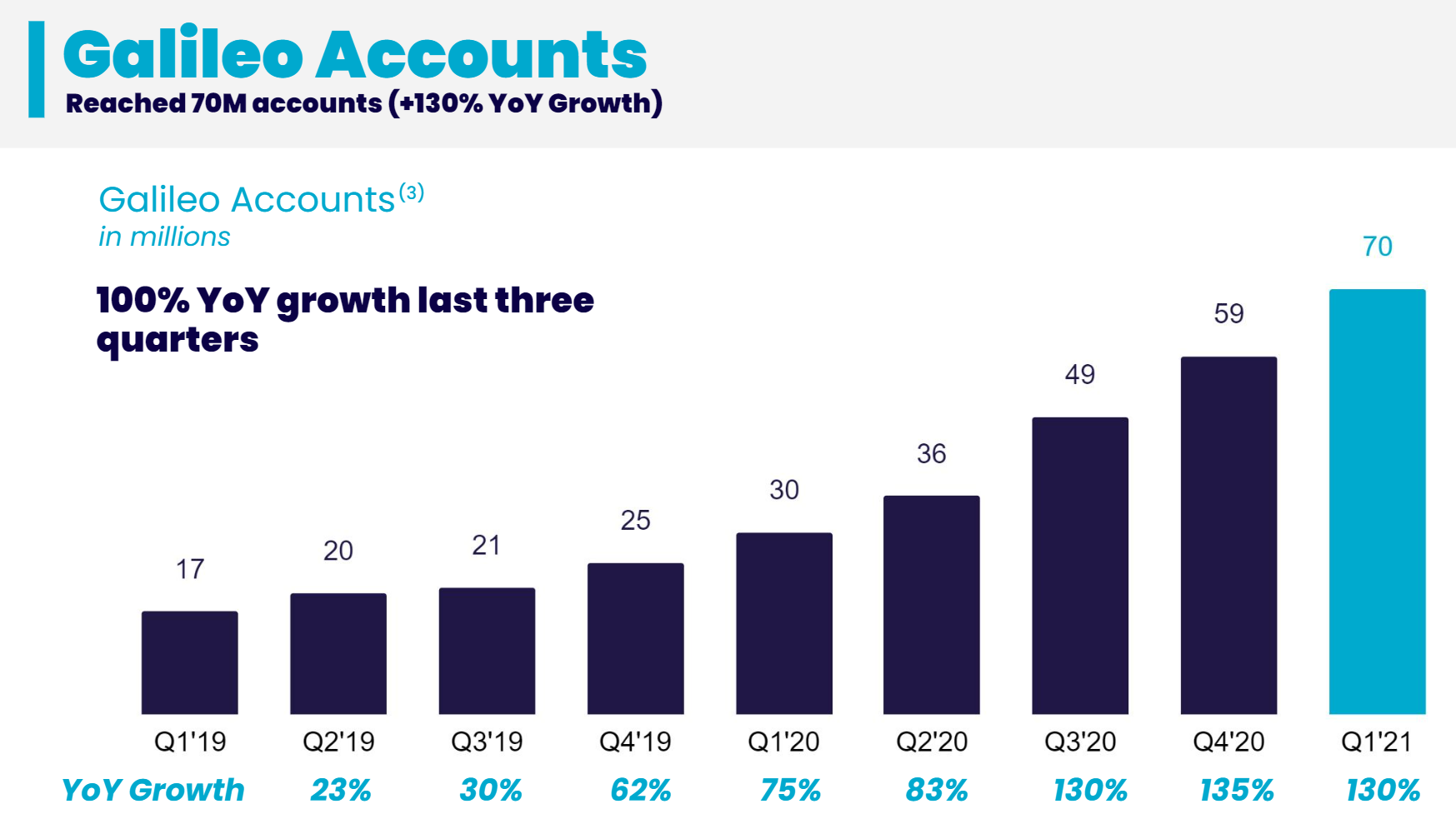

Speaking of neobanks, the other side of $SOFI’s business model which I’m extremely excited about is called Galileo. $SOFI acquired Galileo in April 2020 for approximately $1.2 billion [click here and click here to read more about the deal].

I believe this was an extremely smart acquisition that will help drive growth for many years to come. I’m going to talk more about Galileo a little later because this an important component to my $SOFI investment thesis.

Before we start digging into $SOFI’s product mix, business model, etc I wanted to share a little more data to help explain the acceleration in digital banking as well as why this business model is so much stickier than the old traditional banking models.

If companies like $SOFI don’t have to worry about brick & mortar locations, it keeps their overhead lower and profit margins higher which means not only should they be valued like a fin-tech company but it also allows them to build better products, offer better rates, reduce/eliminate fees and provide an overall better experience to their customers.

I’m not sure about you but I never go into a bank branch unless it’s to deal with a problem — I love being able to do all of my banking and investing through websites and mobile apps. In my opinion, assuming we see the continued growth in neobanks, I think 30-40% of all current bank branches could be gone in the next 10 years.

BUSINESS MODEL / GROWTH CATALYSTS:

Rather than waste your time drilling down on every single financial product that $SOFI offers or has in the pipeline (because I’m pretty sure we all understand the basics behind cash accounts, lending, credit cards, investing, etc)… I do want to cover the basics and explain why it’s so important that $SOFI is building a comprehensive suite of financial products and services as well as why this model will keep driving growth.

In terms of the business model, $SOFI should be looked at and valued in two different ways: 1) they are a FinTech, 2) they are powering other FinTechs

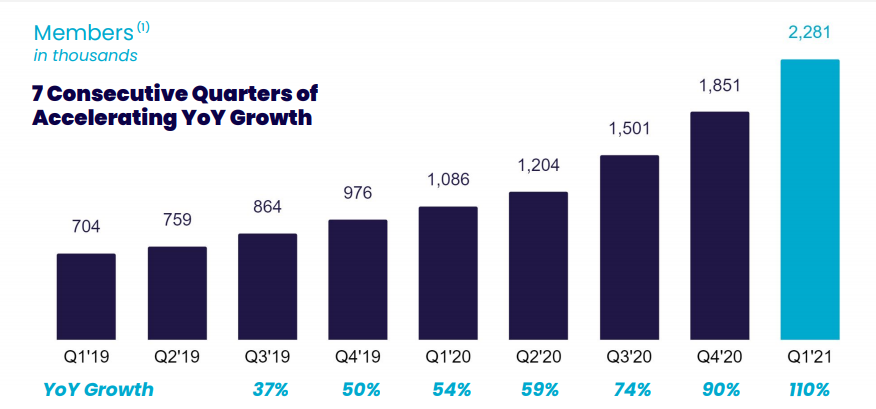

1) Member growth is exploding as you can see from the chart below, up 110% YoY in Q1 which can be attributable to multiple factors including:

$SOFI benefiting from the accelerated adoption of digital banking during Covid

$SOFI benefiting from the trading meltdown at Robinhood in Q1 because of the meme stocks which infuriated many customers thus allowing their competitors like $SOFI to grab thousands of new accounts

$SOFI going public and becoming a more recognizable name in the financial services industry

$SOFI getting into crypto which appeals to a large number of people

$SOFI launches first credit card that lets you redeem points in crypto [click here]

$SOFI benefiting from a 50% customer referral rate and an NPS score of 90 (this is insanely higher for a financial services company [click here] — the average NPS score for money-center banks is in the 20s and 30s [click here]

Another reason that $SOFI is growing so quickly is because of the value-added services they offer their members like access to Financial Planners, help with drafting your Will (for estate planning purposes), referral bonuses and special member discounts.

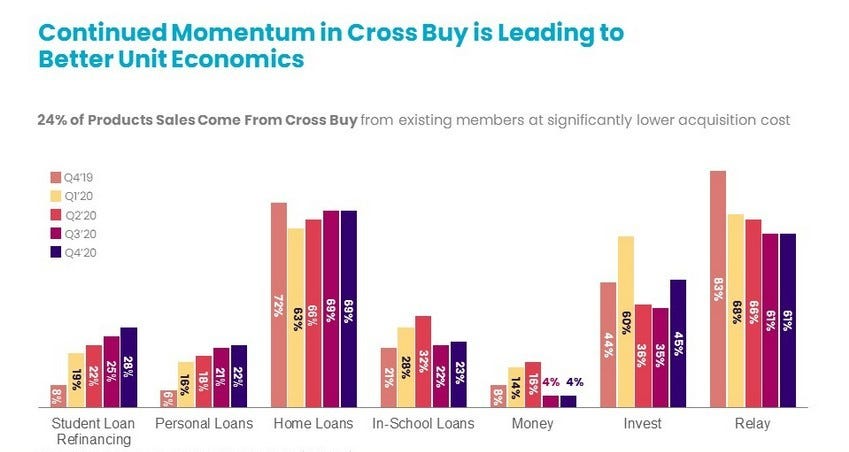

2) The retention rate of members goes up dramatically when they are using multiple products. If you get a customer to use 3-4 of your products then this customer is probably locked in for a long time because switching to other financial providers is just too big of a hassle — look at the Apple ecosystem as an example. We’ll talk about the revenue growth a little later but $SOFI is growing revenues very fast which should not be a surprise when you see customer growth up 110% YoY, total product growth up 121% YoY and financial services product growth up 273% YoY.

This is another reason why I’m excited about $SOFI getting that national bank charter because it will open up an entire new suite of products to not only attract new customers with the stickiest product in the industry (savings/checking accounts) but also because $SOFI taking deposits means they’ll have a larger and cheapest capital base to lend off which will help drive revenues higher higher and profit margins wider.

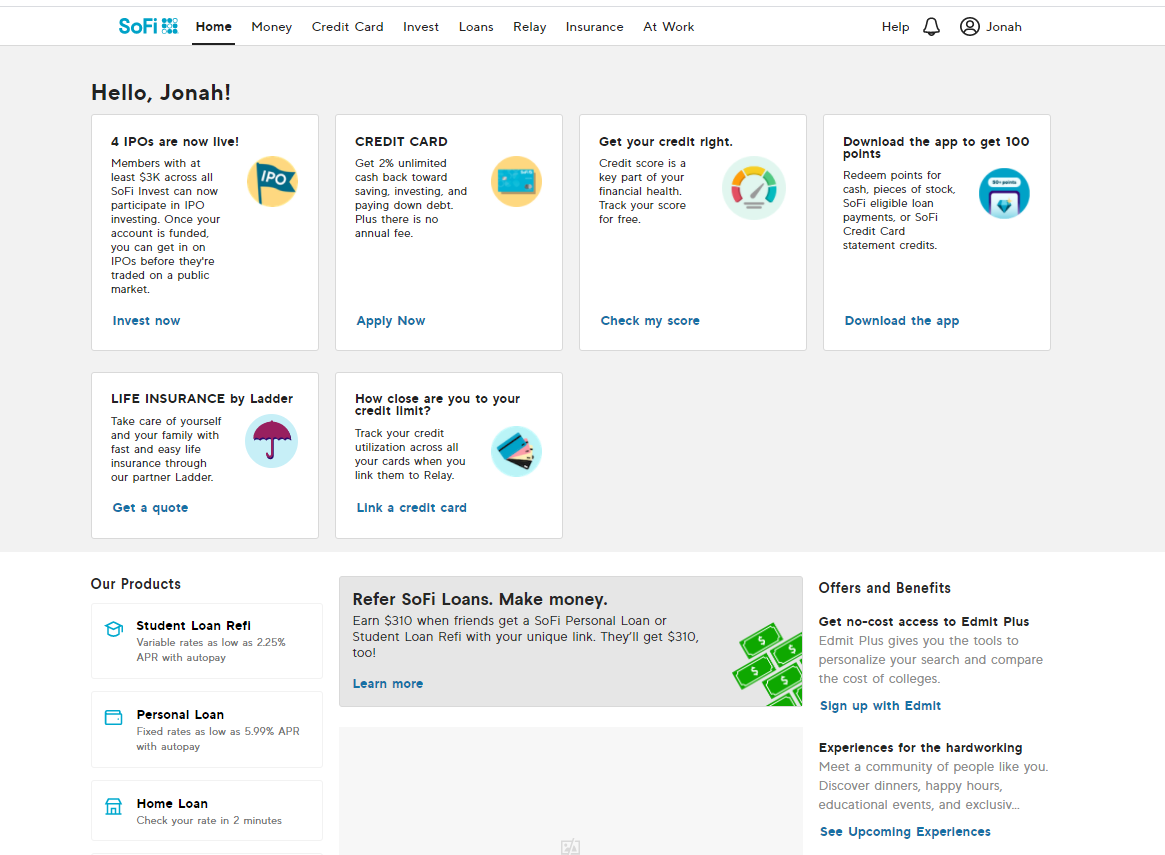

As an example when you log into your $SOFI account you see a dashboard with all of the possible products and services available to you — this is a constant cross-selling opportunity for $SOFI.

In full disclosure I am not a $SOFI customer yet — I created my account a couple weeks ago to help with my research. I am tempted to open a cash management account or signup for the SoFi credit card. Both of which look like great products with lots of perks.

3) The ARPU (average revenue per user) goes up dramatically when customers are using multiple products however your CAC (customer acquisition cost) does not go up so adding new products to each customer relationship becomes extremely profitable. This is the value in being a digital first bank when customers are conditioned to log into your website or mobile app every single day to check their different accounts. This daily engagement gives $SOFI unlimited opportunities to upsell new products and increase that ARPU. I saw a stat recently (can’t remember where) that $SOFI’s CAC was only $50/customer whereas the CAC for traditional money-center banks is closer to $1,000/customer.

This chart below shows how $SOFI is thinking about their different product segments (lending, financial services and Galileo), what growth will look like over the next 5 years (through 2025) and the margins within those different segments. I’m assuming that “financial services” includes everything outside of lending like cash management, investing, credit cards, etc. — I have no idea if $SOFI can maintain 153% CAGR in their financial services segment but if they can then this stock is way undervalued.

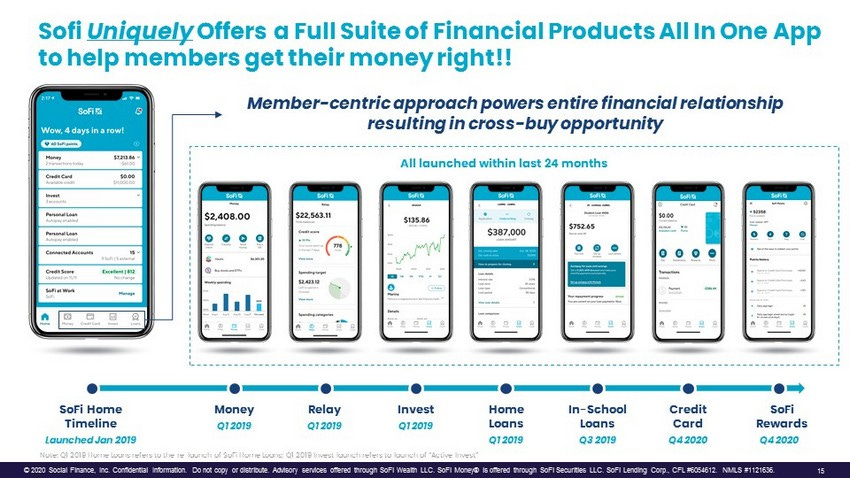

4) $SOFI started out in student loans which is still a part of their business — this allows $SOFI to establish relationships with younger people (under the age of 25) so as that customer graduates college, gets a job, begins making money, needs a mortgage, wants to open an investment accounts, needs life insurance, needs credit cards, etc — $SOFI is right there to grow with them and be their “one stop shop” provider.

As you can see from this timeline below, $SOFI has been very aggressive at introducing new products in order to enhance those customer relationships and make sure their members don’t need to look around at other providers.

GALILEO:

As I mentioned above, Galileo comes from an acqusition, not something that was developed internally and grown organically although given the surge in digital banking over the past year I’d argue that $SOFI got a great deal on Galileo which might be worth 2-3x in just the past 15 months. Galileo is a payment processing platform that allows other fintech’s and neobanks to create their own banking card programs and digital banking solutions.

Galileo is powering the next generation of FinTechs!!!!!

I look at Galileo’s importance to the fintech/neobank industry similar to Shopify’s importance to the ecommerce/retail industry. If you create a product and want to sell it online you don’t hire a developer to build you a customized ecommerce store, you simply turn to Shopify because they have already created the framework, tools, plugins, features, etc that you will need to launch that website as quickly, smoothly and inexpensively as possible.

In the same context, if you want to launch a digital banking service or card program you’d be crazy to try to build it from scratch so instead you turn to Galileo as your plug and play FinTech provider.

I think it’s important to note that a large number of Galileo’s customers are outside of the U.S. so owning $SOFI and getting Galileo as part of it means you are investing in the growth of FinTech around the world — including emerging markets where the adoption of digital banking is happening even faster than in the U.S.

Looking at the chart above I think you can understand why I’m so bullish on Galileo as a major growth catalyst for $SOFI — this growth is massive and most industry experts still believe that “fintech” and the growth of neobanks is just getting started.

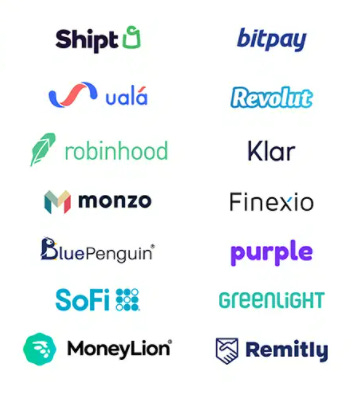

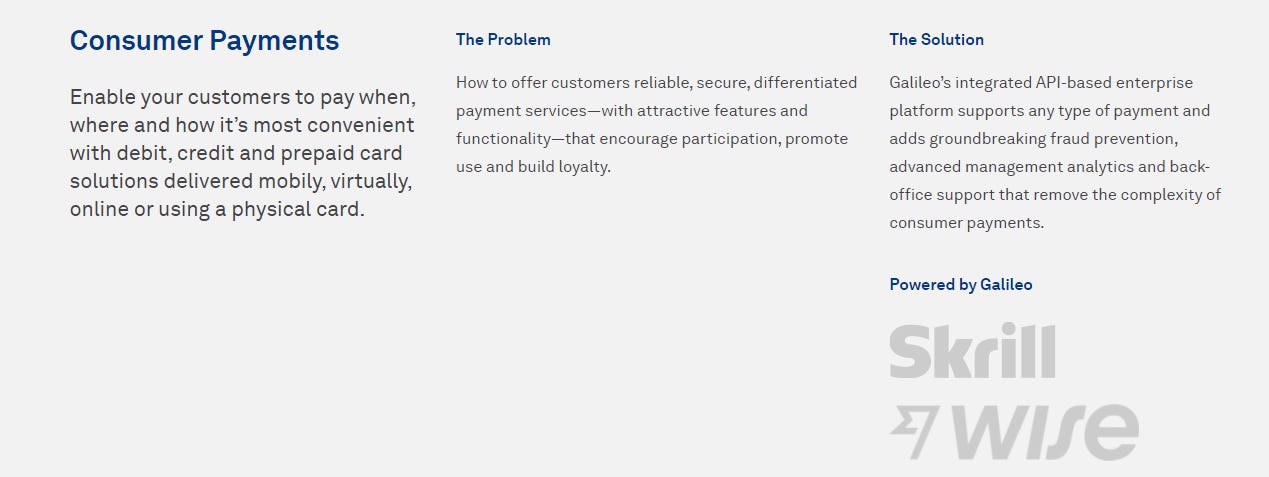

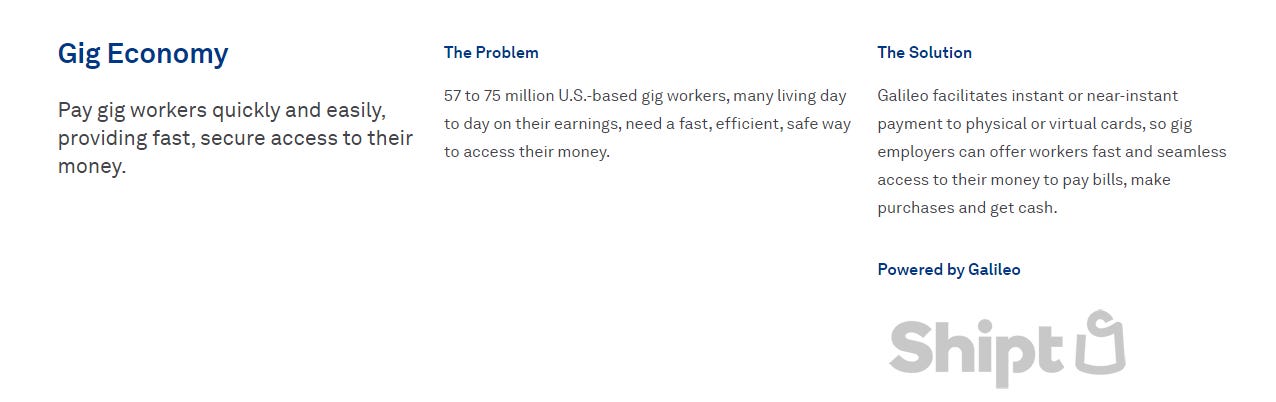

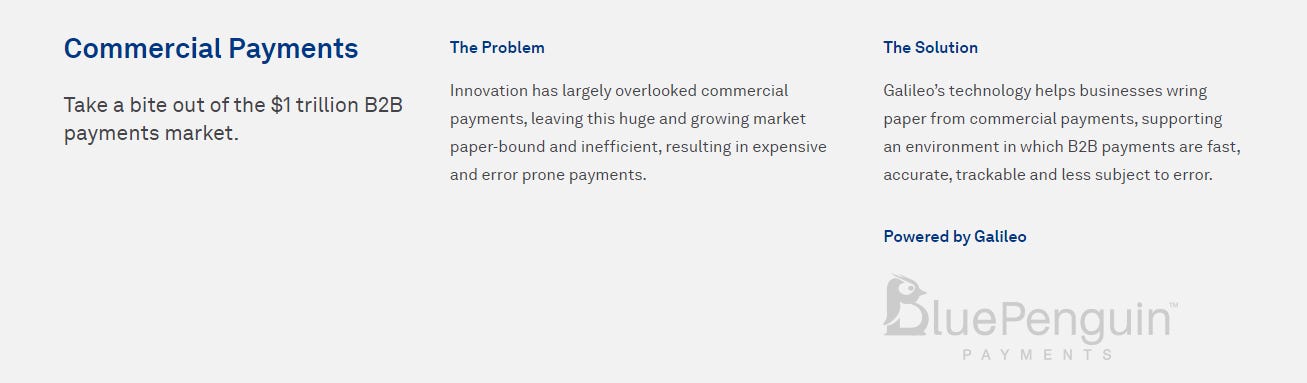

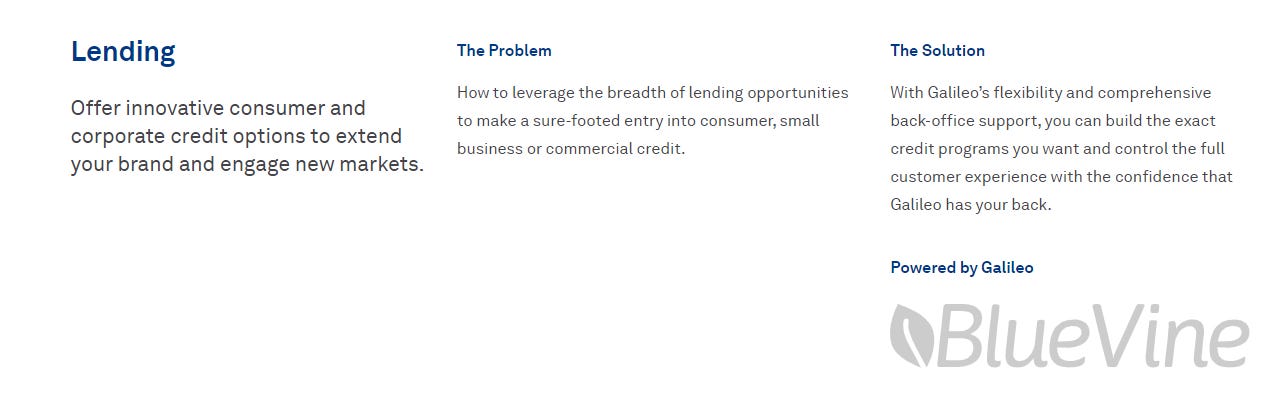

To help explain some of the massive growth in Galileo look no further than their rapidly growth customer list which includes some of the world’s largest fintech’s like Robinhood ($50+ billion upcoming IPO) and Revolut ($33 billion fintech from the UK). Other customers not listed below include big names like Wise, Dave, Current, BlueVine, Greenlight, Koho, Varo, Remitly, Lower.com, Aspiration, Blue Penguin, Interactive Brokers and even Verizon [click here about recent $VZ announcement]

The best place to see more of the Galileo customers is the Newsroom [click here]

Over the past few weeks as I continued doing my research on $SOFI I’ve come to the conclusion that I might be more bullish on Galileo for future growth than I am $SOFI’s core business given the competitive nature of the financial services industry. I feel like Galileo has become a dominant player in their category (empowering FinTechs) and therefore will be a significant portion $SOFI’s future success. Not sure how many of you remember when eBay bought PayPal in 2002 for $1.5 billion — then 13 years later eBay spun off $PYPL into what is now a $350 billion standalone company.

Not that I expect Galileo to follow this exact path but I think it’s very possible in 5-6 years that $SOFI is an $80+ billion company and half of that market cap is coming from Galileo.

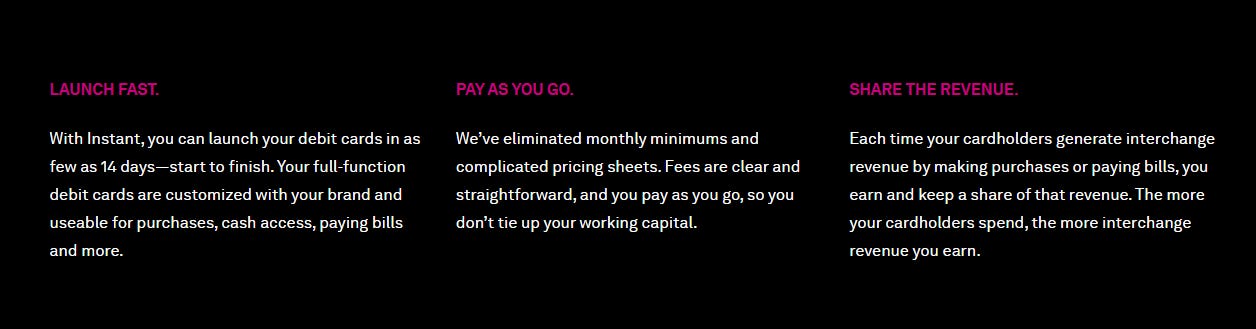

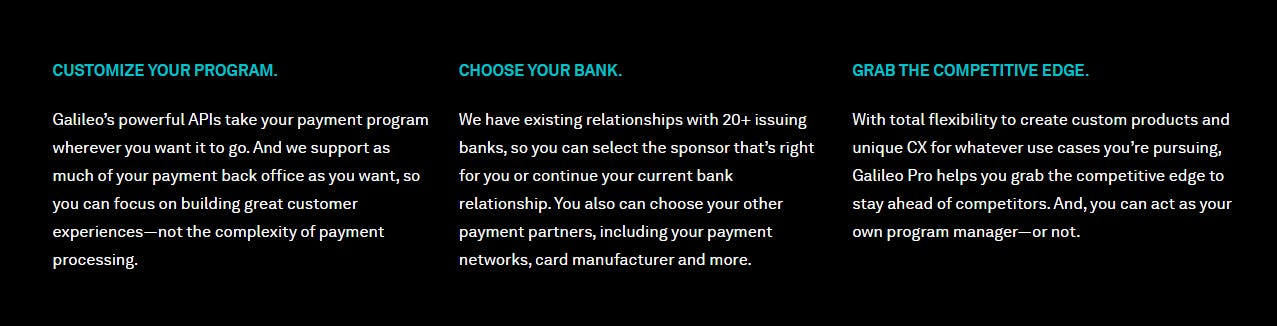

Here are five use cases describing how Galileo’s customers are using their technology applications:

FINANCIALS:

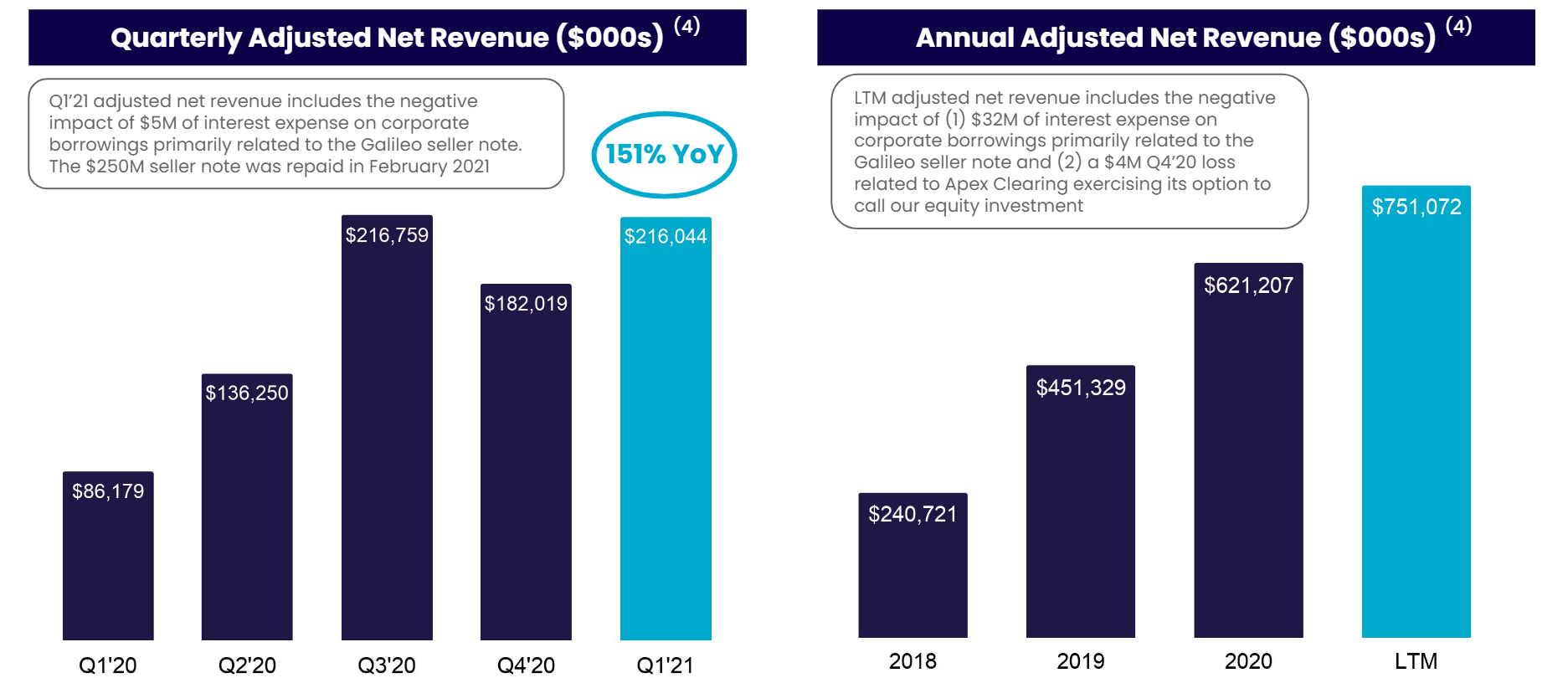

Hopefully by now you have a better understanding of $SOFI and their two core business segments: financial services and Galileo — now let’s dive into the financials. According to the S-1 (page 76) $SOFI’s net revenues in 2020 were $602 million so looking at estimates for 2021, we should be expecting at least 63% revenue growth this year.

With regards to next year (2022) all of the estimates I’m seeing are $1.5 billion to $1.6 billion, so 50-60% revenue growth (no too shabby) however I’m not going to put much credibility into these estimates until I see Q2 and Q3 earnings — we need to know if $SOFI is keeping up with the insane Q1 growth or are we coming back to some normalcy (pre-pandemic growth). It seems like the analysts are assuming the latter however if $SOFI keeps reporting these monster quarters then everyone will need to raise their guidance/estimates for 2021 and 2022.

However it’s very possible the current 2021 estimates are too low after seeing what $SOFI did in Q1 (net revenues up 151% YoY). I’ve seen at least one analyst that is looking for $1+ billion in 2021.

I do think Q1 was a semi-anomaly thanks to the final stages of Covid plus the Robinhood debacle however those customers are most likely still with $SOFI, we might not see the same customer growth rates going forward but even if growth normalizes back to 50-60% (pre-pandemic levels) we should still see $SOFI growing net revenues by 60-80% thanks to ARPU (plus new products), the national banking charter/license) and of course Galileo.

$SOFI is still in the early days of their growth so I’m not going to get hung up on the short term losses, I think most analysts are expecting them to be profitable by 2023. For now the company is profitable on an adjusted EBITDA basis — it’s a start and shows strong improvement from a year ago. Hopefully when $SOFI reports Q2 earnings on August 12th we’ll see continued progression and operating leverage in their financials.

According to $SOFI’s S-1 filing, they are projecting $3.7 billion of net revenues in 2025 however I’m going off the assumption that they’re being conservative plus I doubt this number includes the successful approval of a national bank charter or any future M&A so my own financial projections have $SOFI at $5.4 billion which would be a 52.5% CAGR assuming they do $1 billion in 2021. Obviously my numbers could be too conservative or too optimistic, only time will tell. Right now lending is a big portion of $SOFI’s net revenues however this should change over time as they introduce new products and continue their cross-selling efforts.

VALUATION:

Valuation on $SOFI is a little tricky because they’re somewhere between a banking/lending company and a technology company — especially when you consider Galileo. In my eyes $SOFI is a blend between the big banks like $BAC and $JPM and then the FinTech’s like $SQ and $PYPL however their business model is not identical to any of them, just pieces from each.

I’m going to provide to different price targets, one based on 2022 numbers and one based on 2026 numbers:

For 2022, if $SOFI comes in at $1.65 billion in revenues (might be too conservative), after doing $1.0 billion in 2022 then we’re looking at 65% top line growth. Since they’re still losing money we can’t use P/E multiples and even using EV/gross profit or EV/EBITDA is tough in these early days of growth when operating margins have not normalized yet so we’re stuck using P/S multiples. Based on 2022 estimates (I know this is not perfect), $PYPL trades at 10x EV/sales with 21% revenue growth and 51% gross margins while $SQ trades at 5x EV/sales with 11% revenue growth and 28% gross margins. $SOFI is likely to grow 60-70% with 28-30% gross margins, so a higher EV/sales multiple compared to $PYPL and $SQ would be justified but hard to know by how much. If we stick with $1.65 billion in revenues for 2022 and give them a 16x EV/sales multiple (assuming 865M shares) then we’re looking at a $25.6B / 865M = $29.6 per share by end of 2022

Based on my personal 5-year projections I have $SOFI doing $7.5 billion in revenues in 2026 at which point they should be profitable with normalized operating margins so we can probably use some P/E multiples this time. Let’s assume 20% net income margins (this might be a little high but I think they’ll get there eventually) that would be $1.5 billion in earnings in 2026 x 48 P/E (assuming 40-45% rev growth and 50-60% earnings growth) = $72B / 865M shares (assuming no more dilution which is unlikely) = $83.20 per share in 2026 or 5.2x from current prices ($16/share). Obviously there are a hundred factors that will impact this outcome one way or the other but this gives you a rough idea of how I think $SOFI becomes a 5x investment over the next 5 years.

CHARTS:

After several miserable weeks of owning $SOFI and adding on the pullback we finally had a decent GREEN day yesterday — the stock was up 3% — so perhaps we finally found some support at that $15.56 level which is my trendline going back to January.

As you can see we’re below all of the moving averages so it’s hard to know where we bounce to but bouncing off the trendline Wednesday and then moving higher yesterday was a great first step to getting this stock back into the $20s. I think we have a decent shot at getting back to that $24.95 level by end of year however that will depend on the Q2 and Q3 earnings reports. If $SOFI continues to show anything close to triple-digit top-line growth then we should be in great shape.

If you look at the 1-minute candle chart from yesterday (below) you can see there was some decent buying at the end of day. Hopefully that momentum carries forward into the next few days of trading.

MANAGEMENT:

Very solid management team at $SOFI with tons of experience from inside the financial services industry as well as other large technology companies like Amazon, Microsoft and Twitter.

In terms of Anthony Noto, he is the former COO of Twitter, CFO of the NFL and Partner at Goldman Sachs from their investment banking group.

I like that Clay Wilkes is still running Galileo post-acqusition. It’s always a good thing to keep the founders involved for as long as possible.

I see no weaknesses on the team and I’m sure they’ll continue to add more talent as the company grows.

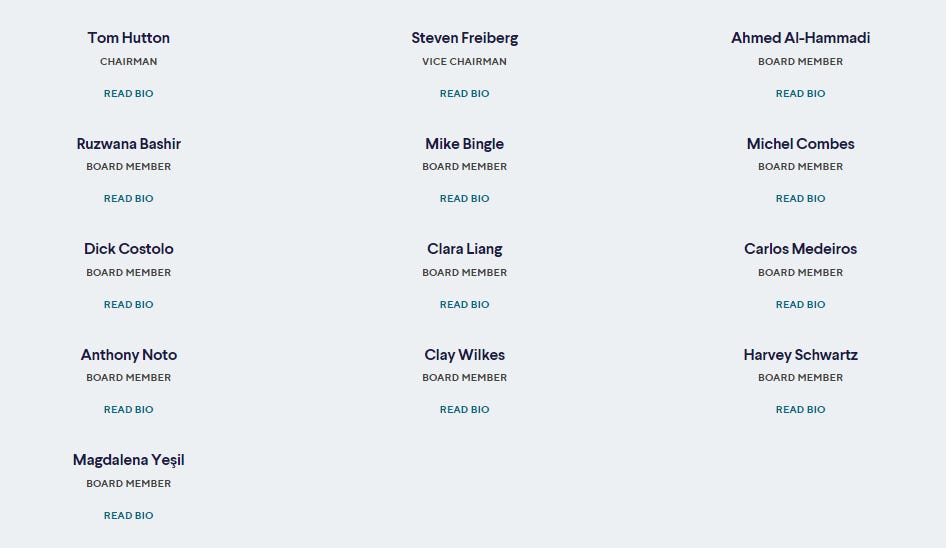

BOARD OF DIRECTORS:

Very strong Board of Directors with a wealth of experience from financial services and technology. Some of these Board Members are also large investors as you’ll see below in the “ownership” section.

Tom Hutton is CEO of Thompson Hutton

Steven Freiberg is the former Chairman of Citigroup

Dick Costolo is the former CEO of Twitter and now runs a VC firm

Clay Wilkes is the founder of Galileo

Harvey Schwartz is the former President of Goldman Sachs

Carlos Medeiros is a Partner at Softbank Group

Ciara Liang is a VP at Airbnb

Mike Bingle is Vice Chairman of Silver Lake Partners

Michael Combes is President of Softbank Group International

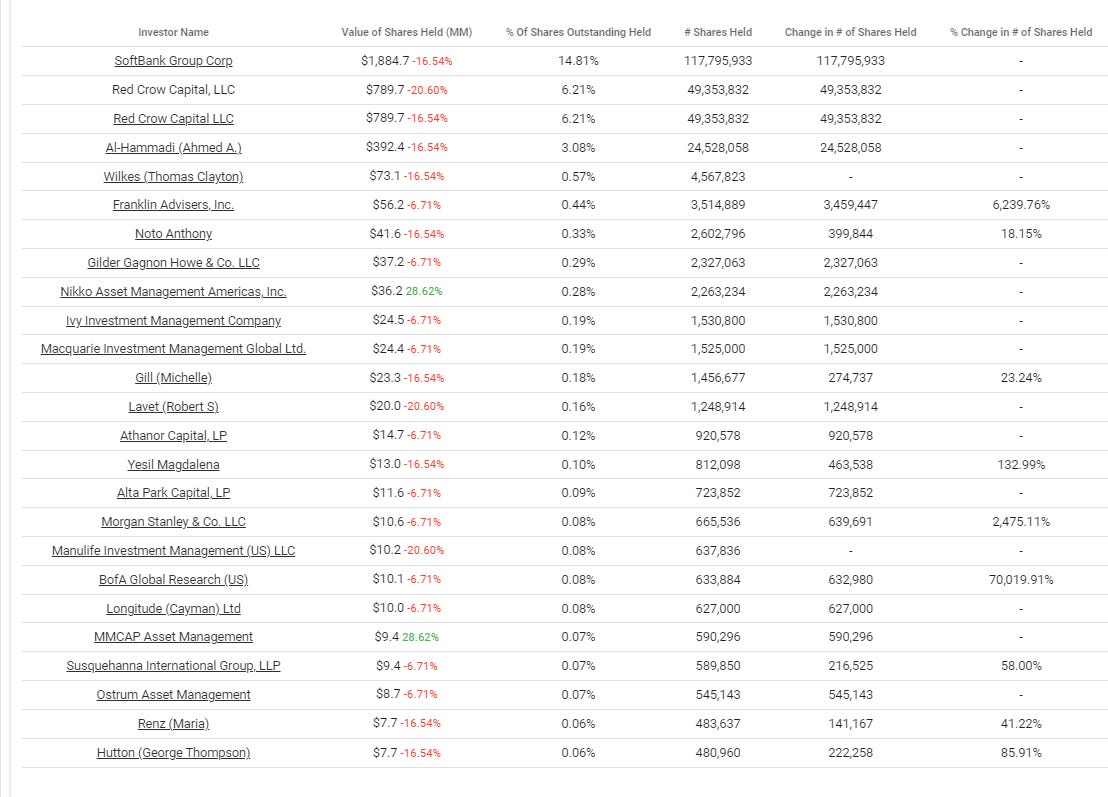

OWNERSHIP:

No big surprises on the shareholder table — nice to see that Anthony Noto (even though he’s not a founder) has a sizeable chunk of the business (ie skin in the game) and then Clay Wilkes (via the acquisition of Galileo) obviously owns a big chunk of $SOFI stock. I doubt either of them have plans to sell their shares anytime soon. If I was going to raise any concerns about this list it would be this… how long is Softbank planning to hold their shares? Hopefully a very long time but we have no idea. I doubt they have any interest selling those shares at current prices however if the stock got back into the mid $20s would they start selling? Obviously I have no clue.

ANALYSTS:

Overall analysts are bullish on $SOFI with price targets ranging from $25 to $30. If you go into Yahoo Finance the estimates for 2021 and 2022 are from 3 analysts however when I pull up this data from StockTargetAdvisor.com it only gives me two of them. I rarely care what the analysts provide in terms of future estimates or price targets however sometimes their reports contain some valuable nuggets of information.

CONCLUSION:

I’m obviously bullish on $SOFI in the short-term and long-term. In full transparency I don’t see $SOFI being a 10-bagger or 20-bagger anytime soon (maybe never) but that doesn’t mean $SOFI can’t be a core position in your portfolio because I expect good returns over the next 3-5 years assuming the company continues to put up strong revenue/member growth numbers, gets the bank charter (thus allowing them to lend off their own balance sheet), keeps launching innovative financial products, continues growing the investment and wealth management side of the business (including the robo-advisor) and most importantly keeps Galileo as a dominant player in the FinTech ecosystem.

Just based on NPS scores, it seems that very few people love their bank however lots of people love $SOFI so they must be doing something right. I think it’s fair to say the older segment of our population (let’s call them boomers) don’t really care about $SOFI or digital banking (as much) or neobanks in general however there’s a massive segment of the population (gen x, gen y, gen z) that do care about these things and actually prefer them.

When I do visit my local bank branch because I have to send a wire or get a new debit card, there’s never anyone under the age of 50 in the bank — this is why I said earlier that 30-40% of bank branches will be gone within 10 years. These neobanks are going to play a major role in our banking system and $SOFI will be at the middle of this, both as a financial services/products provider and as an enabler of other FinTech’s like Robinhood, Wise, Dave, MoneyLion and thousands of others around the world.

$SOFI will be reporting Q2 earnings on August 12th so I’ll do an update after we see those numbers. I’m also interviewing the CEO Anthony Noto in mid-August, most likely the week of August 16th so I’ll be sure to share that interview once we finish recording.

If you have any thoughts, questions or comments about $SOFI please feel free to reach out. I’m sure there are plenty of things I missed or was forced to leave out due to length restrictions but hopefully you have a better understanding of $SOFI after reading this writeup.

Have a great weekend.

Regards,

Jonah Lupton

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Stocks mentioned in this newsletter should only end up in your own portfolio after you conduct your own research and due diligence. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletter. Please manage your own portfolio and position sizes in accordance with your own risk tolerance and investment objectives.