Part 1: Deep dive on Schrodinger ($SDGR)

Part 1: Deep dive on Schrodinger ($SDGR)

In addition to my Substack newsletter, I also run a Stocktwits room where I post my current holdings, buys & sells, investment models, technical analysis and market commentary for both my Investment Portfolio (long term, strong fundamentals, 20-30 holdings) and my Trading Portfolio (short term, strong technicals, 0-10 holdings). The two options are $15/month for the monthly plan [click here] or $150/year for the annual plan [click here].

You can now signup for my new Substack called Jonah’s Trading Charts which is focused exclusively on the technicals — every day (usually pre-market) I’ll send out an email with my favorite trading charts/setups. You’ll also have access to my trading portfolio with current positions/sizes, entry/exit prices, profits/losses and much more. I’m also doing live charting and live trading 3-4 times per week.

Company: Schrödinger

Ticker: (SDGR)

Website: Schrodinger.com

IPO date: February 05, 2020

IPO price: $17.00

Current stock price: $23.81

Outstanding shares: 71.24 million

52 week high: $37.25 on March 23, 2022

52 week low: $15.85 on December 06, 2022

All time high: $117.00 on March 01, 2021

Market cap: $1.696 billion

Net cash/debt: +$378 million

Enterprise value: $1.318 billion

Headquarters: New York City, United States

Number of employees: 800+

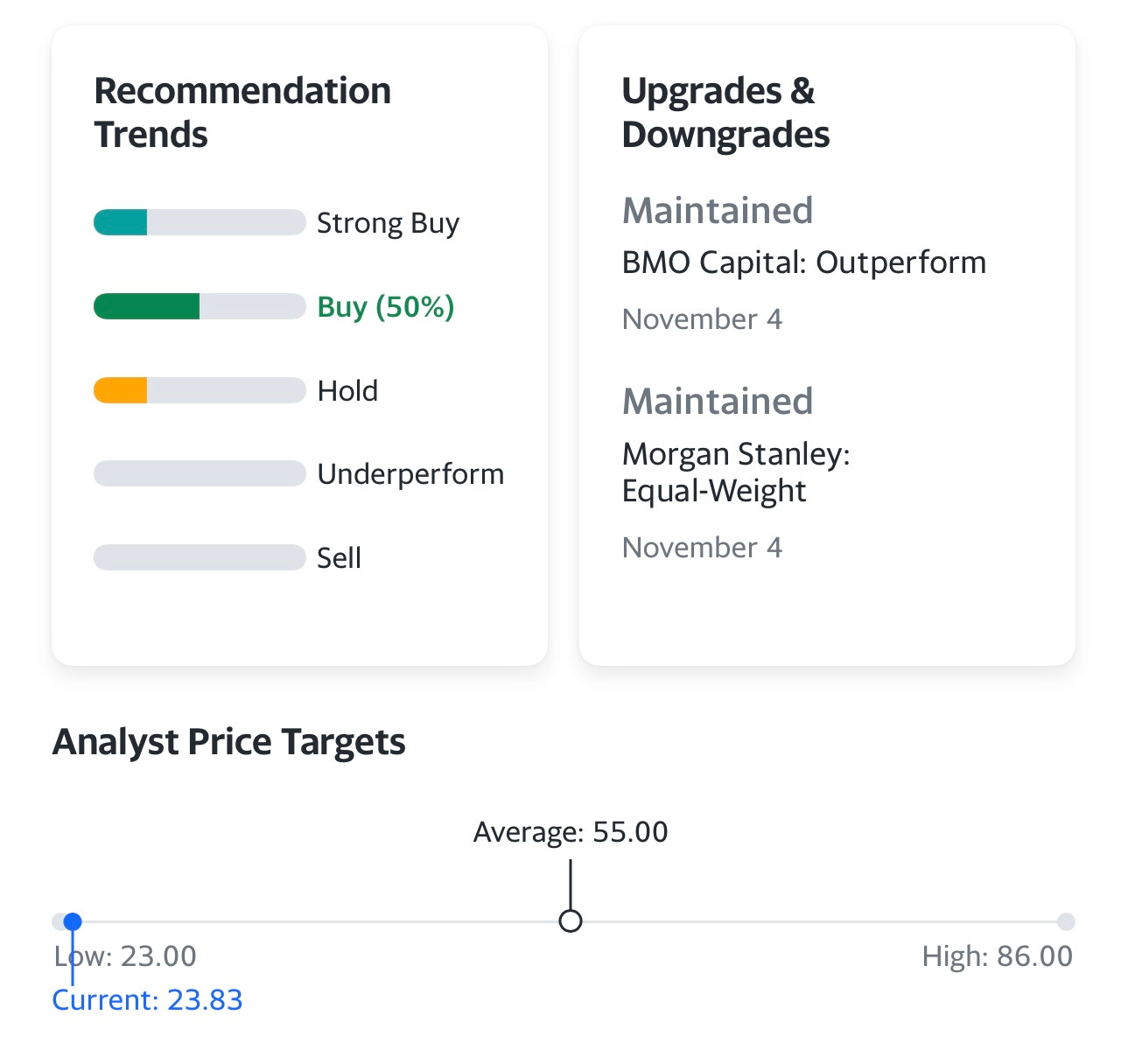

Average price target from analysts: $55.00

Investor Relations [click here]

2023 Update Note [click here]

Q3 2022 Earnings Report [click here]

Q3 2022 Earnings Call [click here]

Q3 2022 Earnings Presentation [click here]

Schrodinger Platform Day 2022 [click here]

Next earnings call (Q4 2022) will be February 28th

Outline

Introduction (part 1)

Company Background (part 1)

Opportunity (part 1)

Technology (part 1)

Business Model (part 1)

Customers (part 1)

Competitive Advantages (part 1)

Management (part 2)

Culture (part 2)

Financials (part 2)

Risk (part 2)

Ownership (part 2)

Valuation (part 2)

Investment Model (part 2)

Analysts (part 2)

Technicals (part 2)

Conclusion (part 2)

Introduction

First off, in full disclosure I do have a 2% position in SDGR which I started on January 6th at $18.00 per share. I had been looking at SDGR in late 2022 but wanted to wait until the tax loss selling ended before starting a position. I’m planning to hold this stock for at least 12+ months unless something material changes with the company or the stock runs up too fast in which case I’d be more likely to trim back my position.

SDGR is still unprofitable and might not be profitable (net income) until 2025 however there are lots of reasons why I finally started a position in this company. First off, SDGR is not only expected to grow revenues by 55% in 2023 (this is consensus amongst 9 analysts that cover the company) but there’s a good chance SDGR will continue growing revenues by an average of 30-35% from 2024 through 2026 so this is definitely a growth stock which should be able to sustain that growth for the foreseeable future. Whereas many cloud/software stocks benefited from massive revenue acceleration during the pandemic, they’re not suffering from massive deceleration which is leading to falling stock prices, margin compression and now massive layoffs across the tech industry. Even though SDGR is kind of a software company, they are very different because they cater to more resilient industries such as pharma and biotech. They also do some stuff with energy, materials and chemical companies given what their software is capable of doing ie accelerating innovation and the R7D process.

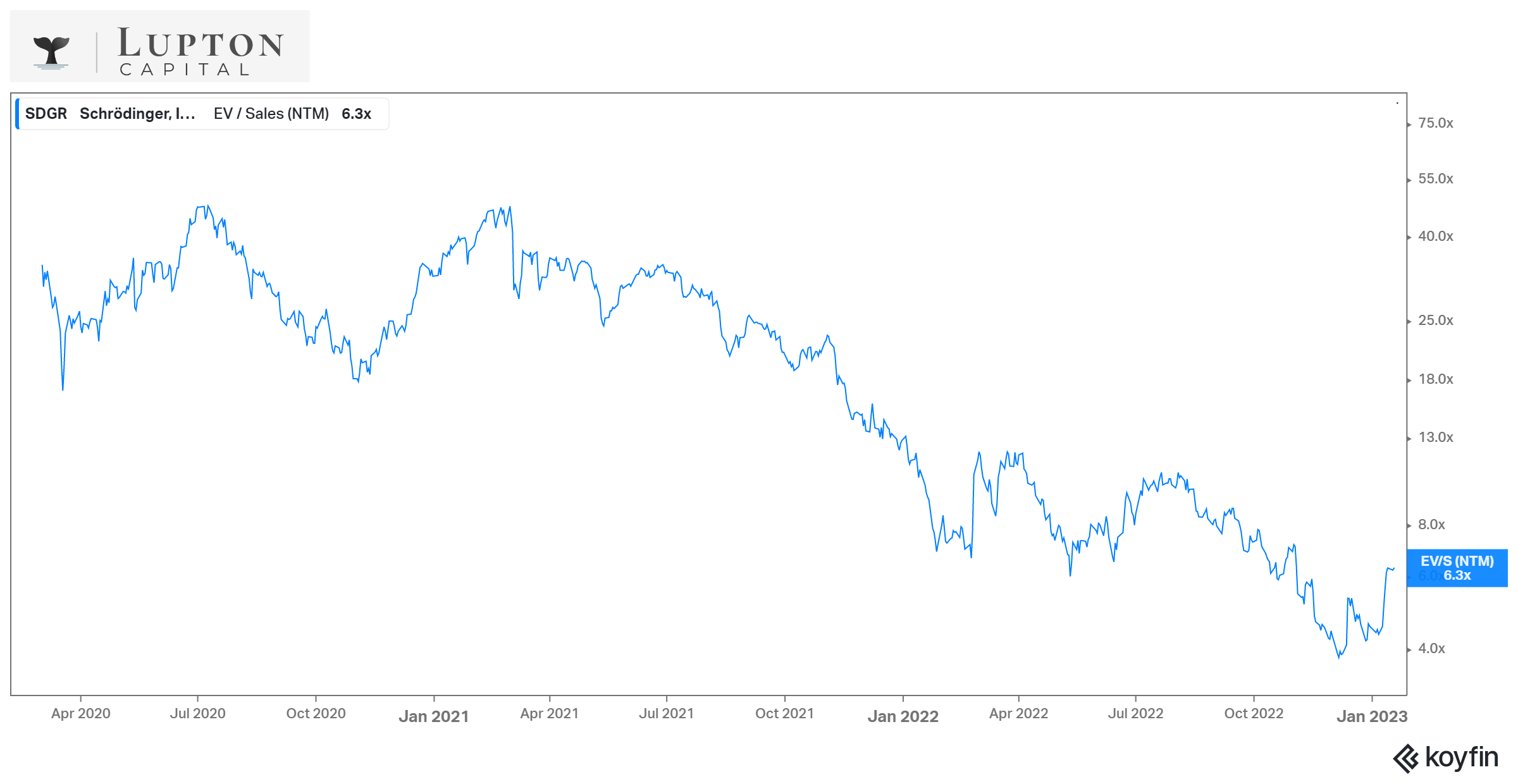

Another reason I really like SDGR at the current price is because the valuation finally makes sense. SDGR is now trading at less than 5x NTM EV/Sales (the Koyfin chart below is slightly off) versus where the stock was trading just a couple years ago at the all time high, almost 55x NTM EV/Sales in early 2021 so the EV/Sales multiple has contracted by 90% over the past 2 years. I’m getting 5x NTM EV/Sales because the current EV is $1.318B and the expected sales/revenues for 2023 is $267 million.

As a result of the multiple contracting, the stock (SDGR) is down 79.6%, from $117 in February 2021 to $23.81 as of today’s close. We’ll get into the technicals in more detail in part 2 of this writeup but SDGR had a strong DTL (downtrend line) breakout a couple weeks ago (right after I started a position — that’s another reason I got into SDGR when I did) and now SDGR is approaching the 200d ema and 200d sma. Reclaiming those moving averages would likely bring more investors into the stock.

Another reason I really like SDGR right now and see more opportunity in the future is because of what happened back in mid-December which was the announcement that Takeda is paying $4 billion for Nimbus plus another $2 billion in potential milestone payments [click here for more details]. Turns out that SDGR has a 5.5% stake in Nimbus so once this deal is finalized they’re looking at $220+ million of cash payments which they could use for stock buybacks, acquisitions, or anything else they want. Even though SDGR is expected to lose money in 2023 and 2024, they already have plenty of cash on their balance sheet (~$378 million) to cover those losses which means the $220+ million they’re getting from the Nimbus acquisition could be used to reduce the share count by close to 10 million shares. Another option would be to use that cash to start a venture fund and get more aggressive with their investments within the biotech industry to hopefully produce more wins/acquisitions in the future. SDGR also uses their software and data analytics for their own R&D purposes so they could pour more money into those efforts which could lead to lucrative licensing deals for any successful outcomes/discoveries.

I don’t invest in biotech stocks because it’s just too risky, especially the ones that only have 1-2 drugs on the market or perhaps the smaller ones that are still going through the FDA trials. Of course biotech cans produce massive winners if you know how to pick them but it can also produce massive losers which is the part that scares me. However, even though I don’t want to invest in biotech directly, I feel like SDGR is a less risky way to get exposure to the industry since they work with every single one of the largest biotech/pharma companies. SDGR fits into that “picks & shovels” investment narrative, in many ways this is what also led me to ClearPoint Neuro (CLPT) which is another position of mine (although slightly smaller in terms of position size as well as market cap). CLPT created a hardware and software system that allows drugs/therapeutics to be safely administered/delivered to certain parts of the brain and they now work with 40+ biotech companies which means any big wins for them is also a win for CLPT because upon FDA approval those approved drugs/therapeutics will be delivered via the ClearPoint system thus increasing their hardware and software sales.

I’ve never worked in the pharma/biotech industry but I have plenty of friends that do so I know how competitive it gets. Not only are we talking about a multi-trillion industry where companies are spending BILLIONS a year on R&D but they are always looking for any little advantage they can find and SDGR’s physics-based computational platform gives them an advantage which is why they’re all using it (1600+ customers around the world).

In addition to that SDGR is able to invest in some of these smaller biotech companies as they are raising early rounds of capital and as we saw with Nimbus, sometimes these small investments ($1-5 million) can turn into massive windfalls ($100-500 million). I’m not sure exactly how much SDGR invested in Nimbus but I know their first investment into the company was back in 2010 as part of Nimbus’s $3.5 million seed round [click here for more details].