Part 1: Deep dive writeup on On Running ($ONON)

I also run a Stocktwits room where I post my current holdings, daily activity, investment models, market/macro commentary, daily Zoom sessions and performance for both my Investment Portfolio (long term, strong fundamentals, 20-30 holdings) and my Trading Portfolio (short term, strong technicals, 10-20 holdings). My investment portfolio is up 26.8% YTD and up 562% since early 2020. The two options are $15/month for the monthly plan [click here] or $150/year for the annual plan [click here]. Prices will be going up next week but you can lock in for the next 12 months with the annual plan.

Earlier this year I launched Trading Charts which is focused exclusively on my trading portfolio. Every morning I send out an email with 10-30 of my favorite trading charts/setups for the day. You’ll also have access to my current trading portfolio with current positions, position sizes, entry prices and stop losses. I also do live charting/trading webcasts every morning and every afternoon over Zoom.

Company: On Holding

Ticker: (ONON)

Website: On-Running.com [click here]

IPO date: September 15, 2021

IPO price: $24.00

Stock price at the time of writing: $22.47

Outstanding shares: 317.52 million shares

52 week high: $29.18 on March 22, 2022

52 week low: $15.44 on October 11, 2022

All time high: $55.87 on November 17, 2021

Market cap: $7.10 billion

Enterprise value: $6.95 billion

Headquarters: Zurich, Switzerland

Number of employees: 1,700+

Average price target from analysts: $26.16 — 16.4% upside from current price

Next earnings report & call: TBA (likely in late March)

Investor Relations [click here]

Q3 2022 Press Release [click here]

Q3 2022 Earnings Call Transcript [click here]

Outline

Introduction [part 1]

Company Background [part 1]

Opportunity [part 1]

Products [part 1]

Business Model [part 1]

Customers [part 1]

Competitive Advantages [part 1]

Management [part 2]

Culture [part 2]

Financials [part 2]

Risks [part 2]

Ownership [part 2]

Valuation [part 2]

Investment Model [part 2]

Analysts [part 2]

Technicals [part 2]

Conclusion [part 2]

Introduction

**Disclosure: I started a small 0.5% position in ONON a couple weeks ago because I felt the valuation finally made sense given my/consensus estimates for the next few years. ONON should be reporting earnings later this month and assuming the numbers/guidance are good I’ll probably add to my position.

To be completely honest I had never even heard of ONON until a couple years ago but then I started seeing their sneakers everywhere and now when I walk into my gym it’s one of the most popular brands along with Nike, Hoka and NoBull. If I had to guess I’d say around 1 out of 8 people (~12.5%) are wearing ONON sneakers.

I bought a pair of ONON sneakers last year but I actually regret buying the particular style that I did. I wish I had gotten one of their sneakers with a bigger sole for more support and cushion. Overall I think ONON has very solid sneakers, they’re not the best running sneaker or the best training sneaker but they’re a a great all-around option. I’m kind of a sneaker-head with 50+ pairs in my closet so I have my favorites for everything whether it’s for lifting weights, running errands, traveling, going out with friends, etc and ONON is always a solid choice and relatively comfortable once you break them in.

Personally I think Hoka makes the best sneakers for cardio especially since I’m a bigger guy and need more support/cushion — I have 3 pairs of the Bondi X and love them for walking/running on the treadmill. My favorite everyday sneaker in the APL TechLoom Wave and my favorite leg day sneaker is the NoBull high-top. I could go on and on but I’ll spare you anymore pain :)

For many years Nike, Adidas, Reebok, UnderArmour, Brooks, Asics and a few others dominated the sneaker category but that’s all changed the past few years with up and coming brands that are taking more and more market share from the OGs like Nike. Given how fast some of these newer brands are growing and therefore could pose a legit threat to Nike in the future, I would not be shocked if they actually acquired a company like ONON which has a market cap of $7 billion but that’s nothing compared to Nike’s (NKE) massive $188 billion market cap. Given the premium multiple (P/E) that NKE trades at, even if they paid a nice premium for ONON it might not even be that dilutive in the first year and would bring some big growth and excitement to a brand that might be facing more competition than ever before.

Not only do I like ONON because I’m a fan of their sneakers and see them everywhere now but the fundamentals are very strong as well. ONON is not a cheap stock like CROX (trades at 12x earnings) but it shouldn’t be because ONON is about to finish off a year in which they grew revenues by more than 50% and even though that level of growth isn’t sustainable, analysts still think ONON can grow revenues by a 30% CAGR over the next 4 years.

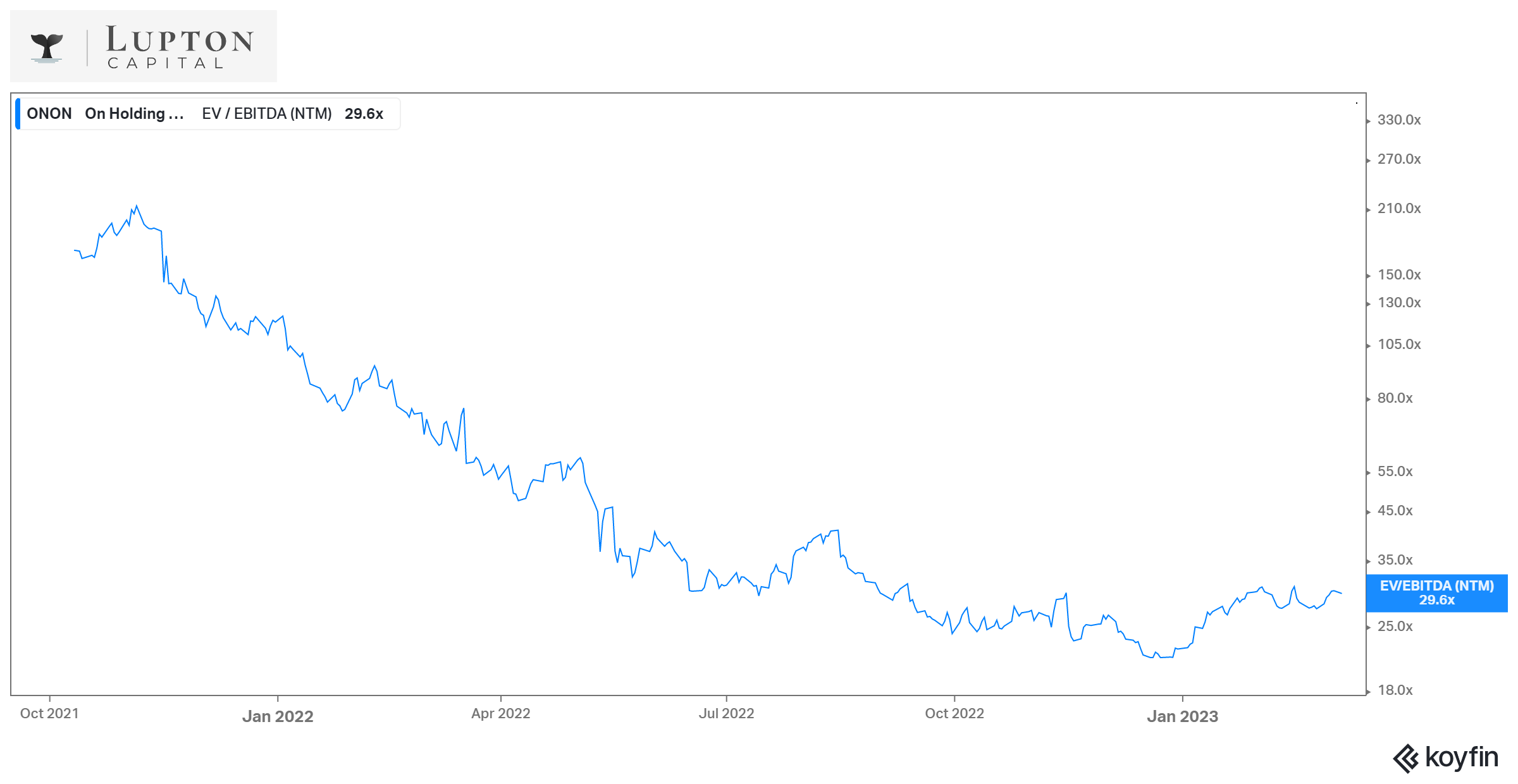

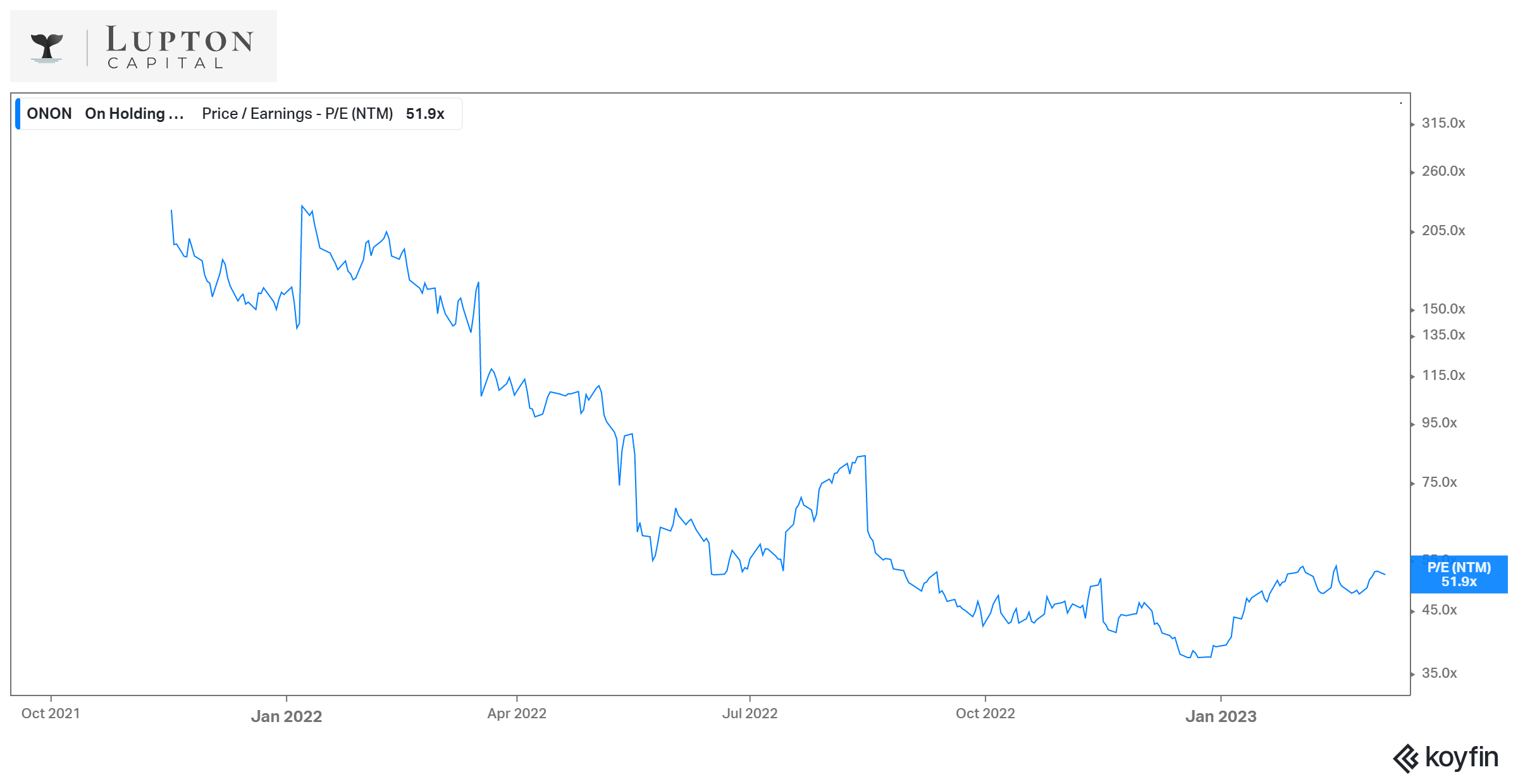

That would take revenues from approx $1.13B in 2022 to approx $3.18B in 2026 while expanding net income margins from 8.5% in 2022 to 13.1% in 2026 which means ONON is going to have some significant EPS growth over the next few years which justifies their current valuation and multiple. If you look at NTM EV/EBITDA and NTM P/E multiples for ONON they are very reasonable for a company with 30% top line growth and 50% EPS (net income) growth.

I’ll get deeper into the valuation and my 4-5 year investment model in part 2 of this writeup but just for fun let’s compare ONON to NKE. Based on 2023 estimates, ONON is trading at 48x EV/NI with 35.4% revenue growth (est.) and 42.1% net income growth (est.) which would be a PEG ratio of 1.14x — now compare that to NKE which trades at 34x EV/NI but is only expected to grow revenues by 6-8% with flat to possibly negative net income growth. Even if we’re overly generous and pretend NKE squeaks out 6% net income growth this year, the PEG ratio is still considerably higher than ONON but a factor of 5x.

If you looking to invest in the footwear industry and skew towards value investor than I’d stick with CROX however if you’re looking for a reasonably valued growth stock in this sector you should be considering ONON instead of NKE.

I’m not sure where ONON goes in the short term because there are many factors at play including macro, inflation numbers, yields, etc however if ONON hits the consensus estimates from analysts, my price target for end of 2026 or early 2027 is $50-60 depending on whether you’re looking at earnings or free cash flow and what kind of my multiple you apply to both.

With ONON still down 60% from the ATH, I think the stock looks relatively attractive at these levels but as we know any stock can always go lower on a bad earnings report, worse than expected macro or just a broad market selloff.

What I will say is that ONON has way more upside over the next few years than NKE which is a mature, low growth, high multiple stock. If I was a long/short fund manager I’d even consider being long ONON and being short NKE as a pair trade which would really crush it if NKE ended up buying ONON — if this happens I want the credit haha.

If you own a pair of ONON sneakers, let me know what you think of them and I hope you enjoy this writeup. As always feel free to give me some feedback.

Company Background

On Holding (On) was founded in 2010 in Switzerland with the goal of revolutionizing running. The main brain behind the brand is Olivier Bernhard, a retired professional athlete, three-time world and six-time Ironman champion.

Having a successful career in running, Bernhard personally experienced a problem with running shoes that, in most cases, were uncomfortable and led to injuries. He wanted to create a running shoe with a totally different feel, never experienced by any runner before.

Bernhard began by experimenting with pieces of garden hose that he glued to the outsole of his prototype. When he first made the prototype, he felt something he had never experienced before as an athlete wearing shoes of well-known brands. He seemed floating above the ground like he was running on clouds.

Caspar Coppetti and David Alleman soon joined Bernhard. Together, they created On and called this experience – the experience of ‘running on clouds,' when shoes absorb impact, reduce strain, and adapt to the runner's running style. They also help prevent injury so runners can run pain-free.

In 2010, On’s revamped prototypes won the ISPO BrandNew Award from the leading global sports platform ISPO which honors the most innovative products and services in the sports industry.

So what the trio wanted to create is the most high-performance running shoe ever, with two distinct features: cushioned (soft) landings and powerful take-offs.

As a result, they invented a completely new cushioning technology, which they called CloudTec. This patented technology has been at the heart of every On pair produced ever since.

“When people stepped into the shoes something switched “On.” They found themselves moving. Sometimes further. Sometimes faster. Sometimes in entirely new ways.”

The company took off, and soon enough, the trio realized they needed more management capacity to scale and professionalize the business. In 2013, they brought on Marc Maurer and Martin Hoffmann.

The five partners have been leading the company collaboratively since then, with Caspar and David acting as Executive Co-Chairmen, Olivier as Executive Board Member, Martin as CFO & Co-CEO, and Marc as Co-CEO. The three founders spend considerable time on innovation and product development, while Marc and Martin are focused more on operational and administrative matters.

In addition, each partner owns some strategic missions that contribute to both On's operational and long-term success. This truly collaborative approach sets On apart and is an integral part of the company's culture and success.

Despite the immediate success, very few backed the company in its early days. Not many believed that On could keep pace with the giants of the running shoe industry. But one, a New York-based private equity firm called Stripes, became a big believer in On, investing in the company an undisclosed amount in Series A round in 2017.

"We rediscovered our passion for running through our diligence and are thrilled to be partners with the On team as they continue to build the next iconic athletic brand!" – Stripes about On.

A big breakthrough for the brand and the business came in 2019, when Roger Federer, one of the best tennis players who ever played this game, became an investor in the company. After his retirement in 2022, Federer started to spend a lot of time with the company in its On Lab, working on his namesake sneaker franchise and his tennis competition shoe.

"Our partnership with Roger has never been an athlete endorsement deal. Instead, he has long been a partner, investor, and co-entrepreneur of ours. He plays a truly instrumental role in the development of the Roger line and the Roger Pro tennis shoe, acting as a role model to all of his own teammates at the same time." – the company's statement.

However, Federer's endorsement helped the company to bring more partnerships with other athletes, especially from running. These partnerships propelled the brand further among the community, cementing On as the most innovative brand in the space.

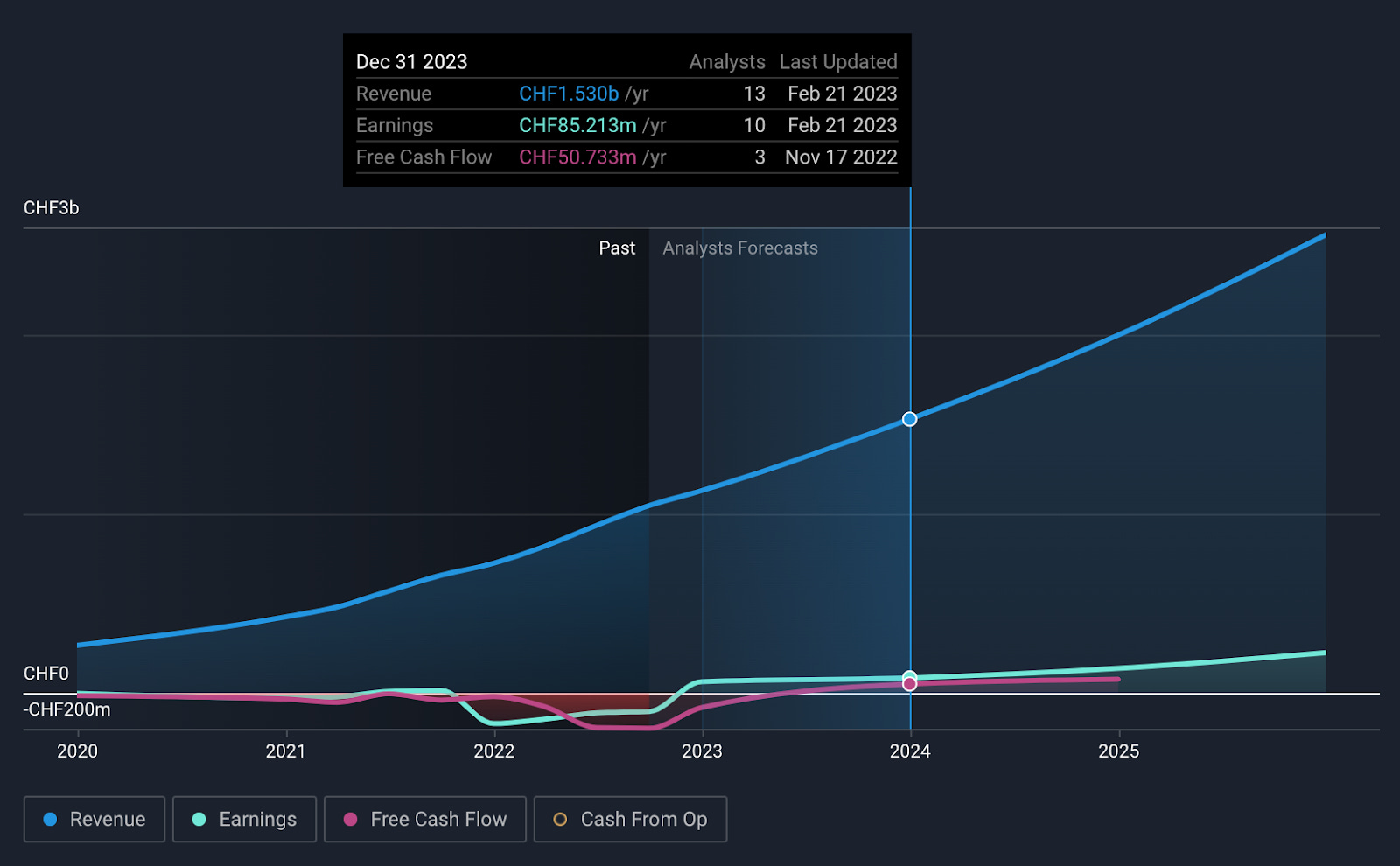

Since then, sales have skyrocketed. The company generated CHF 267.1 million (approximately the same amount in US dollars) in 2019, CHF 425.3 million in 2020 (+59.2% YoY), and CHF 724.6 million in 2021 (+70.4% YoY).

These results partially helped the company to have a tremendously successful IPO in late 2021. The stock opened at $35.40 (up from the initial price of $24) and ripped to $55 (47% higher) on the debut day, valuing the shoemaker at a whopping $11.35 billion. The company raised an astonishing $746.4 million.

On exceeded CHF 1 billion in sales in 2022, an incredible milestone for the company that has been around for just a little over ten years. The company is expected to double its net sales from 2021 to 2023 while it is already profitable and will soon start generating free cash flow.

Today, On is one of the sport’s fastest-growing brands (if not the fastest). More than 7 million people (including Olympians and world champions) from 50 countries purchased a pair of On's shoes. Yet, it is just the beginning for On.

"From day one, we've defied the doubters to take the world of running by storm. And we're just getting started." – On's founders.

The opportunity ahead is as ample as ever. With the shift to sportswear fashion and with the rise of sports lifestyle, the company has a long runway in what looks to be a crowded space. But On has something other big brands like Nike and Adidas don't – a strong product proposition centered on innovation and product quality. The company will win millions of legs in the coming years and far beyond those that wear sports shoes for running.

Opportunity

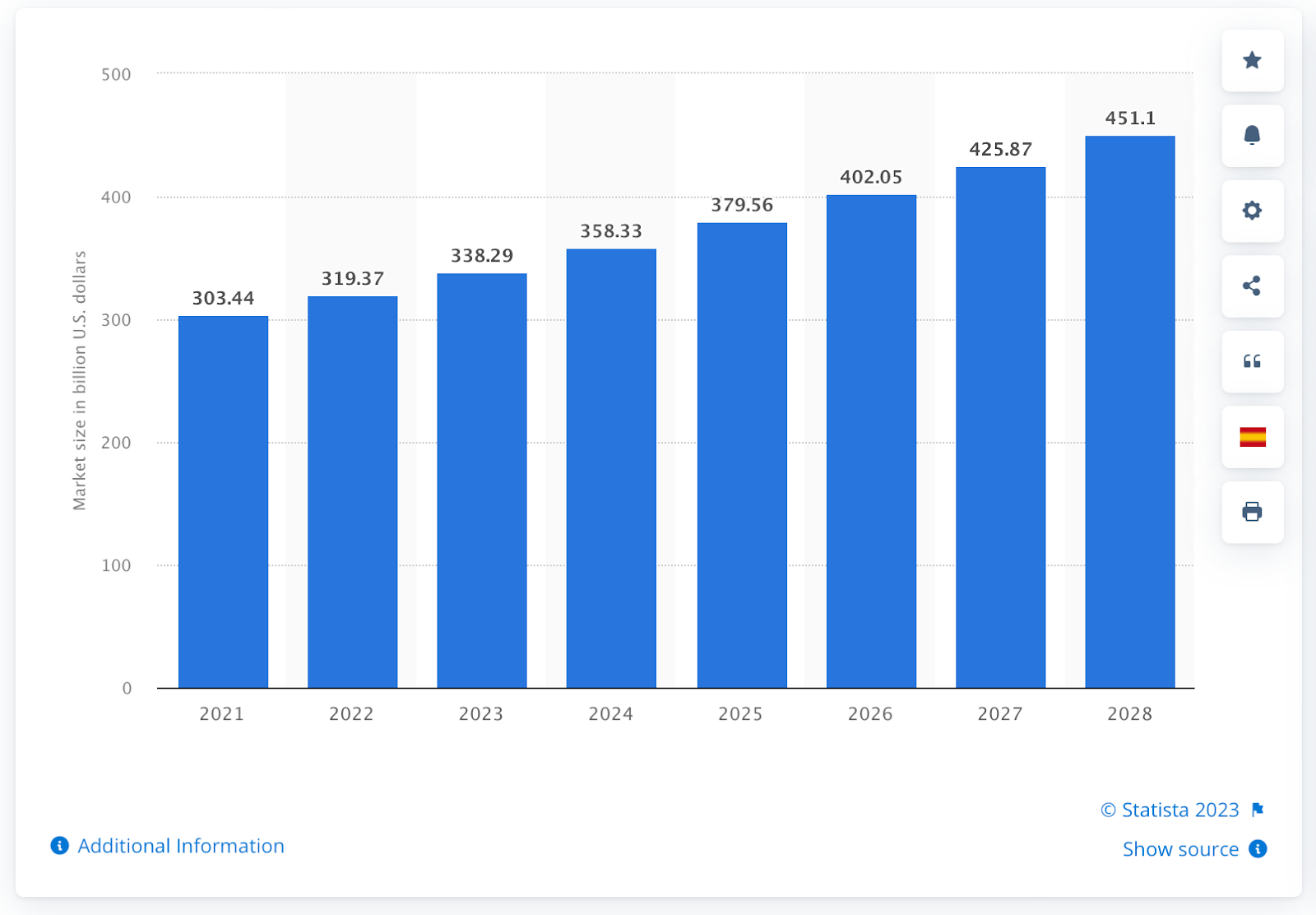

On is operating in a massive $300+ billion global activewear market, which includes footwear, apparel, and wearables. According to Statista, this market will further grow to over $450 billion by the end of this decade.

The market growth is due to more people getting health conscious and progressively getting into physical movement, especially females, who increasingly participate in various sports, including running. In the United States, women’s sportswear products generated more than $35 billion in 2021, more than men’s and children’s sportswear combined.

At the same time, fashion trends, specifically the shift to sportswear fashion, are further helping the growth of the activewear industry. For example, sneakers, a large part of the footwear category, are now integral to our culture and contribute to the increasing consumption rate. According to Statista, 64% of US millennials and Generation Y reported buying athletic shoes in 2021 as part of their personal style and not for sports activities.

The retail segment is estimated to lead the market due to a large number of consumers preferring to buy offline vs. online to avoid misfits, delays in delivery, and other complications related to buying clothes and shoes, like replacements and refunds.

With its combined DTC and wholesale strategy to meet runners wherever they are, On is well-positioned to drive the market share of this sizable, multi-billion opportunity.

The company's roots have been in running since its beginnings. For many years, On has been innovating and investing a lot of resources into developing the best running shoes, launching new models, and improving the key technologies behind them.

But running shoes is just one of many footwear categories, so the company began expanding to other categories. The first category was fitness, which offers various shoes beyond the track. So-called 'Active Life Shoes' were designed for everyday wearing.

Sports shoes started to gain traction among tens of thousands of customers so much that they began showing interest in other categories, boosting the total addressable market immensely.

First were hiking and outdoor shoes. These shoes were designed for any weather and terrain. Then came out the travel collection, designed for comfortable long-distance traveling when a lot of walking is needed.

The company has just launched tennis shoes in collaboration with Roger Federer. Two models, The Roger Pro and The Roger Clay, are now available for purchase. Roger Federer made his final appearance on the court in one of these pairs.

According to the company, more partnerships with other tennis players are on the horizon. The tennis category should become the next big sports category for On and pave the way to more sports like basketball, soccer, and others. The market for each is extensive on its own.

Perhaps, the largest opportunity in the footwear category lies not in sports shoes of any kind but in everyday shoes for personal style wearing, like sneakers. This is the largest market within the footwear category, and it is where the real money is. On is tirelessly working on this front, both in product launch and marketing efforts, trying to make the brand trendy among fashion heads.

A great example of these efforts is the plan to develop a tennis sneaker family with Roger Federer to re-invent how age-old tennis sneakers are made. The company wants to create something Nike did with basketball sneakers: people wear them far outside the basketball court.

While the footwear category is by far the most popular among customers and currently generates the majority of net sales (>90%) for the company, the apparel category is twice as large as footwear, according to Fortune Business Insights. Moreover, the apparel category is projected to dominate the market further due to the rising popularity of the utilization of sports apparel for fitness and day-to-day wearing.

On has been in the apparel business for just a couple of years. The apparel category generated less than 5% of total net sales in 2022. The company is only implementing the learnings from its apparel business but plans to scale this category aggressively starting in 2023. The company recently added many great talents to the apparel department to innovate on the products in this category.

“Our product innovations aren't just confined to footwear. The potential of our apparel business has never been greater. We're doubling down on apparels and have recently made a number of key investments to strengthen our design and development team.” – from the company's statement.

The company is only building the foundation for future success in this category by investing in internal capabilities, product assortment, and customer experience for apparel. The apparel category should become a meaningful part of On's business over time.

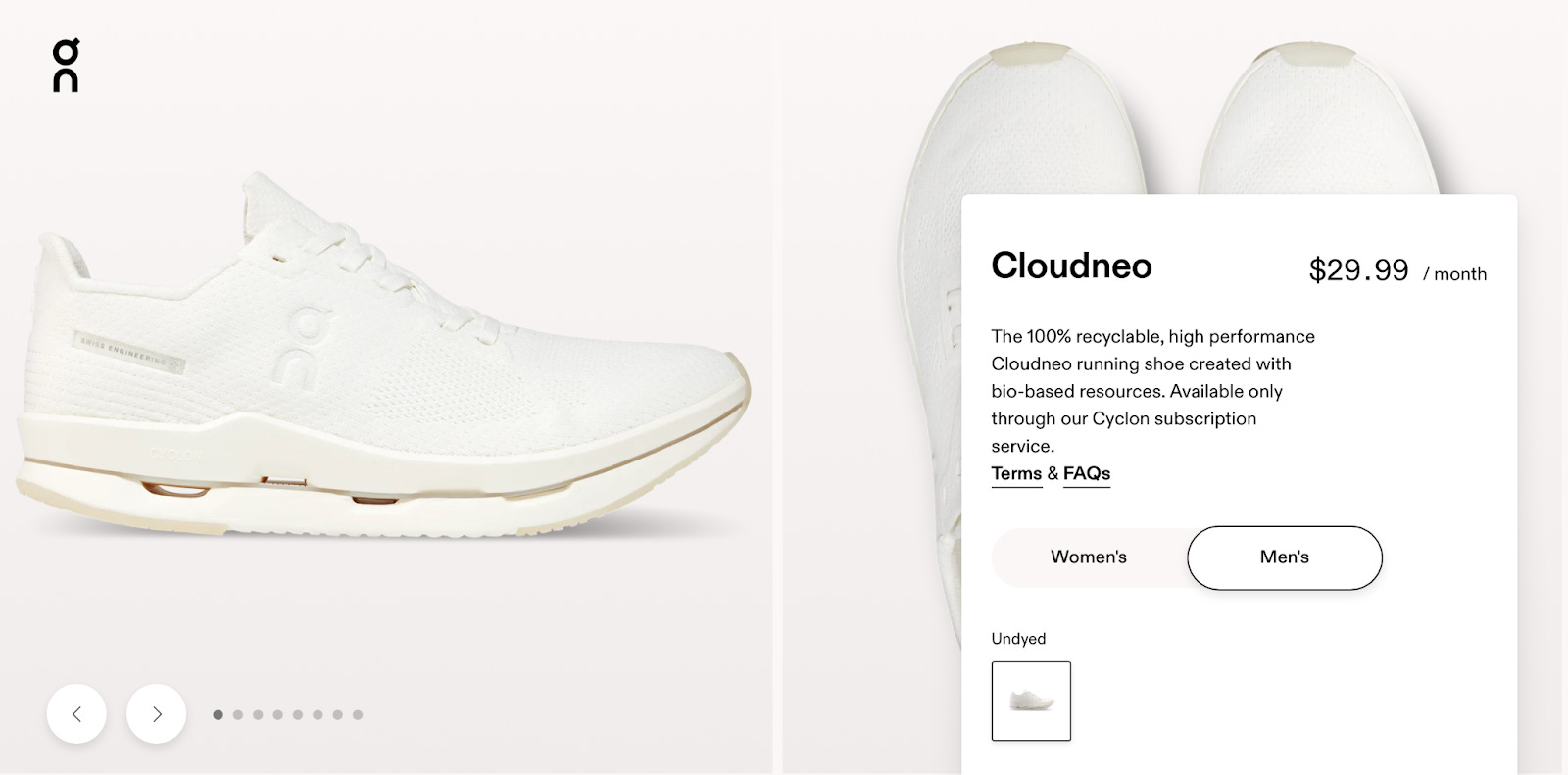

On did many other tests in 2022 apart from apparel. The company plans to scale many of them starting in 2023. One particular is looking exceptionally promising – running shoes on subscription. It is called Cyclon.

Under this award-winning (Cyclon has won the 2021 ISPO Award for Product of the Year and Sustainability Achievement) circular subscription service, customers receive a pair of running shoes every six months. But these shoes are not regular – they are fully recyclable. Cloudneo – is the company's first fully recyclable running shoe made from castor beans.

The subscription starts from $29.99 per month. After six months, the customer can return the worn shoes back to the company, and the company will send over a new pair. The price of a 6-month Cyclon subscription is the same as the industry average price for high-performance running footwear.

On keeps innovating not only on the product side but also on the side of how to sell its products.

“Our strategy connects us with consumers when and where they want to shop, either via our own physical and digital stores, wholesale partners or immersive digital platforms.” – from the company's statement.

Wholesale has been the bread and butter for the company so far. In 2022, almost 70% of all net sales came from sales in physical stores. The company has established strong relationships with some of the most trusted retailers in running specialty, the outdoors, and fashion, such as FootLocker, JD, and Nordstrom, among hundreds of others. As of Q3 2022, On had 9,050 wholesale doors selling its products worldwide.

“Wholesale is vital to our strategy. It provides access to new customers faster. But we want to drive DTC sales more.” – the management comments.

While wholesale is vital for the business today, DTC is the future of it. DTC offers much higher margins than wholesale, as well as greater consumer engagement and an optimal environment to showcase the brand.

To start with, the company began opening its own locations. On plans to selectively build physical stores to showcase its brand and products, further strengthening the local community and brand reach. These stores are designed to create an enriching customer experience through technology and personalized customer service. The first flagship store was opened in 2020 in New York, United States.

Management has the intention to open a flagship store in all key locations around the globe, including stores in London and Tokyo that are opening soon.

The retail store strategy is the key growth pillar, especially in China, where the company already operates eight owned retail stores in Shanghai, Chengdu, Shenzhen, and Beijing.

China is still a tiny part of On's business (~5% of total net sales in 2022), but the company is looking to build it into one of the main ones very soon. Management expects China to be a continued growth driver for the company for the years to come.

The retail stores also continue to be a showcase of the opportunity the company has in apparel. For example, the existing store in Shenzhen reached a 30% apparel share in Q3 2022, the highest of any other store.

The company has ample opportunity to not only acquire new customers but also drive repeat purchases, and the digital channel is the best way to achieve it.

In September 2022, the company began piloting a fully redesigned website designed to deliver a richer, more immersive shopping experience. The pilot and A/B testing was launched in the UK and has already shown excellent results. The global rollout will be in the coming months.

On also partners with external digital platforms such as China's WeChat e-commerce mini program. Chinese consumers can now seamlessly shop for On products without ever leaving the WeChat ecosystem.

Furthermore, On introduced Onward, the first-ever platform to shop and trade in preowned gear for On's customers and products. Onward is currently available in the US.

The company is firing on all cylinders, and it is just at the beginning of many of its opportunities. Generating $1 billion in net sales in 2022 is a massive achievement for the company, but it is still less than 1% of the overall opportunity.

Products

Innovation is in the On's DNA. Under the guidance of its founders, On's products are engineered in Switzerland by in-house research and development teams that work on the innovation, engineering, design, development, and testing of all of the company's products.

At the heart of every footwear product is an award-winning CloudTec technology, which is a completely unique cushioning system. CloudTec reacts according to unique movements, compressing horizontally and vertically to cushion just where it should. CloudTec is tailor-made for every shoe.

CloudTec is not the only technology developed by the company. For example, Speedboard is working in harmony with CloudTec to convert the kinetic energy of each landing into a powerful take-off, offering more speed for the same effort.

The material, shape, thickness, and curve of the Speedboard change to provide different results based on different running needs, from comfort to all-out speed.

When it comes to offroad running, the company developed Missiongrip, which offers traction for any trail, providing support for the ups and downs. A specially selected grip-rubber compound keeps the person in control regardless of what the trail is underneath.

Finally, the superior performance the company wants to create is impossible without suitable foam. The company engineered superfoam, Helion, which combines rigid, stable sections with more flexible foam elements along the same molecular chains, something that was previously only possible with two separate materials.

The company holds a number of critical patents for its technologies, and it is continuously working on new technologies to advance its existing lines of products and create new ones, both in footwear and apparel.

When designing products, management takes diverse viewpoints from scientists, athletes, designers, storytellers, product developers, digital innovators, talent scouts, and business operators – an approach that defines On and separates it from the rest of the competition.

The company is continuously working on new digital and physical experiences that constantly create value for the fans and give On an edge over the competition.

“I'm thrilled to see how our newest performance product like the Cloudmonster, the Cloudrunner and the CloudGo are resonating with runners in a major way, becoming the fastest-growing product lines at our retail partners. These styles are now driving volume for us, not only in running specialty doors, but also in general sporting goods channels like big sporting goods.” – from Q3 2022 earnings call.

On is focusing a lot of effort on sourcing renewable raw materials, such as recycled polyesters and polyamide, organic cotton, vegan leather, and PFAS-free membranes. In Q3 2022, the company (in collaboration with LanzaTech, Borealis, and Technip Energies) unveiled the first-ever shoe made from carbon emissions with clean cloud material.

“This makes on the first company in the footwear industry to use carbon emissions as a primary raw material for a shoe's midsole, a huge milestone for the sports industry and something that seemed almost impossible when we first started developing it 5 years ago.” – from the company's statement.

This is a significant moment in On’s journey to move away from petroleum-based resources, something competitors don't even consider.

Technology can be seen and felt also in performance-infused apparel and accessories.

In general, the company offers products in the following categories:

Road Running

Trail Running

Active Life / All-Day Wear

Hiking and Outdoor

Travel

Tennis

Most products are available for both men and women, and there are several collections for kids. More and more kids are starting to wear On's alongside Crocs.

The company is trying to mimic the same strategy that Crocs has successfully used to attract millions of kids to wear the Crocs.

In each product category, the company also offers various apparel and accessories designed primarily for athletic use. Apparel includes pants, jackets, hoodies, sweatshirts, bras, shorts, tops, and t-shirts. Accessories mainly include socks and headwear.

On does not own or operate any manufacturing facilities. All of its products are supplied by third parties. The company is very selective about its suppliers and works with around 16 companies, five of which produced approximately 85% of all products in 2021.

All of the footwear is produced by seven suppliers in Vietnam across 12 production sites, while apparel and accessories are sourced from nine other suppliers located in Vietnam, China, Portugal, Germany, Lithuania, and Turkey.

The company has production and quality control staff in each country from which it sources products to monitor manufacturing at supplier facilities.

With the recent supply chain problems, management made a decision to invest in warehouse capacity to avoid any future possible challenges with the supply chain. During Q3 2022, the company secured the capacity with a third party to build a highly automated fulfillment center in Atlanta, the United States. This warehouse will provide additional capacity as of early next year and will replace the existing East Coast warehouse by 2025.

Business Model

On operates a pretty much straightforward business model. The company generates revenue primarily from selling its products (shoes, apparel, and accessories). The company does it through two distinct channels: Wholesale (WHS) and Direct-to-Consumer (DTC).

WHS involves selling the products in volume to wholesale customers (large retailers) and international distributors. These organizations then resell the goods with their margin. The DTC sales include selling to end customers directly through On’s e-commerce platform and through its own retail stores.

DTC sales usually carry better margins than WHS, as the company does not need to sell its products at a discount to wholesalers. Despite generating over 65% of its net sales through the WHS channel, On still has best-in-class gross margins at ~60% (but may fluctuate like in 2022 when it was 55% due to air freight costs). To compare, Nike's gross margin is 45%, Under Armour's is 42%, and Adidas' is ~50%. With further growth of DTC sales and business optimizations, the gross margin will return to 60% and may further expand.

Gross margin expansion is possible due to further SG&A leverage, which should come when the automation in the newly secured warehouse in Atlanta kicks in. It will help the company significantly decrease handling costs and dependency on manual labor. Automation will facilitate gross margin growth in the coming years.

The company operates in more than 60 countries, with key markets being the United States, Brazil, Australia, Germany, the United Kingdom, and China. The company first launched its products in Germany in 2011, then entered the United States in 2013, the same year as Japan, and then China, Brazil, and Australia in 2018. The company recently established its operations in Spain and Italy and is looking to enter South Korea and the Middle East in 2023. In all of these markets, the company owns subsidiaries.

As of nine months of 2022, net sales in North America were CHF 496.4 million (58% of all net sales), CHF 274.7 million in Europe (32% of all net sales), CHF 58.6 million in Asia-Pacific (~7% of all net sales), and CHF 25.7 million in the Rest of the World (~3% of all net sales).

The company turned profitable in 2022, delivering both Adjusted Net Income and GAAP Net Income. As of Q3 2022, Net Income and Adjusted Net Income were CHF 84.1 million, while adjusted EBITDA increased to CHF 103.5 million.

Most analysts expect the company to accelerate both revenue and earnings in 2023 and beyond while starting to generate positive free cash flow.

The formula for growth is pretty straightforward as the business model itself: drive more sales (especially through the DTC channel), maintain high gross margins, and leverage operating expenses.

Customers

On's primary customers have been from the inception and still are runners inspired by an emerging run culture that elevates running into a lifestyle.

The company has built a global community of hard-core runners that have become not only loyal customers but also brand advocates. Word-of-mouth has been a huge driver of the company’s success. These strong relationships that the company has with its critical base of customers are something that no other brand has.

But the customer base is growing beyond just runners, and many fans own several pairs of shoes: one for running, the other for everyday use. In fact, 43% of e-commerce customers have already purchased two or more items, and this number keeps increasing. In total, the company sold over 17 million products to date.

It also reflects in the company's Net promoter score. On has a market-leading NPS of 66, compared to 30 for Nike, 36 for Under Armour, and 28 for Adidas.

The secret is in the quality of products. On produces far superior shoes than any other competitor, and the level of innovation is simply unmatched even by large retailers with tens of billions in revenue.

Because of the premium quality, the company can afford not to discount its products. During the holiday season (which was in a very challenging environment), the company sold 94% of shoes online at full price, pinpointing the brand's strength and the customers' willingness to buy at any price.

On has also seen a record number of visitors coming to its website, with almost 10 million monthly sessions recorded in 2022. Instagram followers just crossed 1 million, and engagement is as high as ever. The company keeps attracting new consumers every single day.

Due to its fragmented customer base, no single customer accounts for more than 10% of total net sales.

Competitive Advantages

On operates in a highly fragmented and extremely competitive market of footwear, apparel, and accessories. The company competes with wholesalers and direct retailers of sports footwear, apparel, and accessories and with other apparel sellers that do not specialize in the sports segment.

Alongside main competitors are Nike, Adidas, Puma, Under Armour, Lululemon, Jordan, New Balance, Reebok, Columbia Sportswear, and Asics. These are the largest companies in the sports segment, with Nike holding the biggest market share and making 50 times more in sales than On.

However, most likely, the main competitors for On are Hoka (which belongs to Deckers Brands, the parent company for UGG, Teva, and other footwear brands) and Brooks. These brands target the same customers and offer similar products. Most online reviews of sports footwear are of these two brands.

Hoka offers low-profile and max-cushion shoes for road, trail, and all-terrain. Similar to On, Hoka has enhanced cushioning coupled with a unique midsole.

Brooks takes a step further, targeting a full range of running and fitness footwear for all types of runners, but especially those who run long distances. Brooks also offers a comfortable, yet responsive midsole foam, and its shoes will last longer than probably most others. Another significant differentiator of Brooks shoes is that they are available in narrow, medium, and wide widths.

So Brooks is for really hard-core runners, while Hoka and On are balancing somewhere in the middle.

What really sets On apart from these two companies and all other competition is its approach to creating truly innovative products. Innovation is what the brand is known for and why millions of people choose On for other alternatives.

The desire to make better products lies in constant experimentation. The company never stops innovating, constantly creating new products or introducing new experiences, including the buying experience (subscription).

And there is quality. On shoes offer true premium quality, and while Hoka and Brooks are sold at the same price, they don't provide the same luxury feel, let alone the big brands like Nike, Adidas, or New Balance – their products are of completely unmatched quality.

When customers are buying On's shoes, they know they are getting not only the most innovative shoes on the market but also the highest quality that will last longer than others. Customers appreciate this and choose On, creating a competitive advantage that is hard to replicate.

Having said that, On still risks having competitors flooding the market with products seeking to imitate its products (even with patents that the company holds for its key technologies), therefore, making the competition always relevant and, perhaps, making it the company's biggest risk.

Hope you enjoyed part 1 of this ONON writeup — part 2 should be out in the next day or two.

Have a great week 😊

~Jonah

PS: don’t forget to check out my other Substack at tradingcharts.luptoncapital.com and my Stocktwits room [click here]

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.