$DM - Desktop Metal

$DM - Desktop Metal

Signup for my Stocktwits room [click here]

Signup for Fintrics [click here]

Subscribe to my YouTube channel [click here]

Follow me on Twitter [click here]

$DM — Desktop Metal

Stock symbol: $DM

Prior SPAC symbol: $TRNE

Stock price: $12.15

Market cap: $3.0 billion

Enterprise value: $2.5 billion

Sector: Industrials / Manufacturing

Website: DesktopMetal.com and DesktopHealth.com

Founders: A. John Hart, Christopher A Schuh, Ely Sachs, Emanuel M. Sachs, Jonah Myerberg, Ric Fulop, Rick Chin, Yet-Ming Chiang

CEO: Ric Fulop

President: Steven Billow

CTO: Jonah Myerberg

CFO: James Haley

CPO: Arjun Aggarwal

Board of Directors [click here]

Founded: 2015 [click here]

VC Funding: $430+ million [click here]

SPAC merger announced: August 2020

First day as public company: December 10, 2020 [click here]

Auditor: Deloitte & Touche

Law firm: Latham & Watkins [click here]

Headquarters: Burlington, MA

Employees: 200+

Phone: 978-224-1244

Email: press@desktopmetal.com

Investor relations: investors@desktopmetal.com

Investor presentation, March 2021 [click here]

2020 Q4 earnings conference call, March 2021 [listen here]

2020 Annual report, Form 10-K [click here]

Patent portfolio [click here]

TechCrunch article about $DM going public via SPAC, August 2020 [click here]

13 things you should know about $DM, December 2020 [click here]

Could $DM be the next $10 billion company, August 2020 [click here]

Baron Growth Fund highlights $DM in recent investor update [click here]

$DM completes acquisition of EnvisionTEC, February 2021 [click here]

$DM launches Desktop Health, March 2021 [click here]

$DM qualifies 316L stainless steel for use in production system [click here]

The future of metal manufacturing, November 2020 [click here]

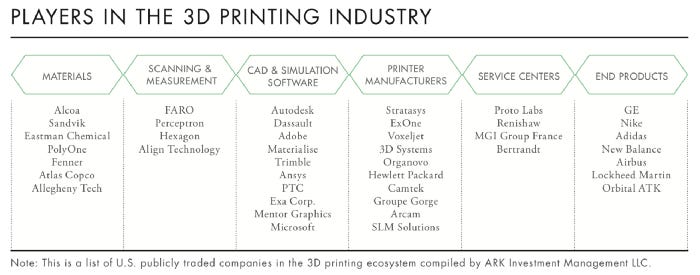

White Paper from ARK Investments on 3D printing, October 2016 [click here]

2021 Big Ideas from ARK Investments, 3D printing starts on slide 85 [click here]

Additive manufacturing and why it’s the next frontier, October 2019 [watch here]

CEO discusses why $DM is coming public via SPAC, August 2020 [watch here]

CEO discusses completion of the SPAC merger, December 2020 [watch here]

CEO talking about 3D printing on Voices of Wall Street, December 2020 [watch here]

CEO talking about the future of additive manufacturing, February 2021 [watch here]

$DM on Facebook [click here]

$DM on Twitter [click here]

$DM on Instagram [click here]

$DM on YouTube [click here]

$DM on LinkedIn [click here]

$DM — Desktop Metal

“Today we help companies print parts but someday we’ll help companies print products” ~Ric Fulop, CEO of Desktop Metal

INTRODUCTION:

Before you consider investing in $DM it would be a very wise idea to listen to the recent 2020 Q4 earnings call because Ric Fulop (CEO) will explain what $DM does and all of the benefits of additive marketing and the market opportunity ahead better than I ever could [listen here].

I first heard about $DM back in 2015 when one of my friends Wayne Chang invested in the $15 million Series A-Round. The idea of using massive 3D printers to make metal parts seemed wild and almost impossible but Ric and his all-star team at $DM pulled it off.

$DM was one of the fastest startups to reach a $1 billion valuation (unicorn status) and you’d be hard pressed to find a better roster of early investors. In the case of $DM those early investors included several angel investors like Wayne Chang and Jason Calacanis plus VC firms such as Kleiner Perkins, NEA Associates, Google Ventures, Lux Capital, Founder Collective, GE Ventures, BMW Ventures, Saudi Aramco, Lowe’s Ventures and many more.

Given that $DM is only 6 years ago and about to hit their hypergrowth phase I would argue that investing in $DM right now would be similar to investing in the Series F-round if they had opted to stay private instead of going public via SPAC in the summer of 2020.

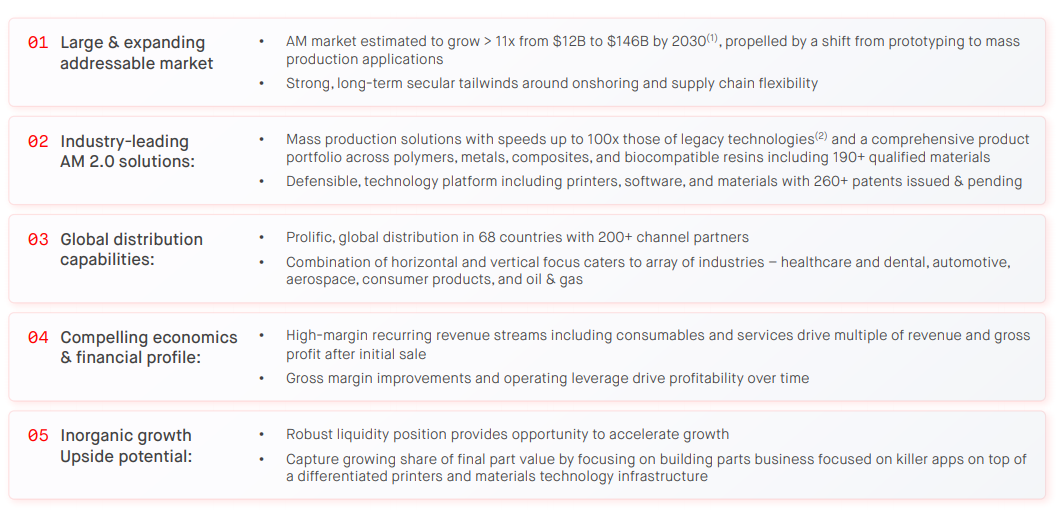

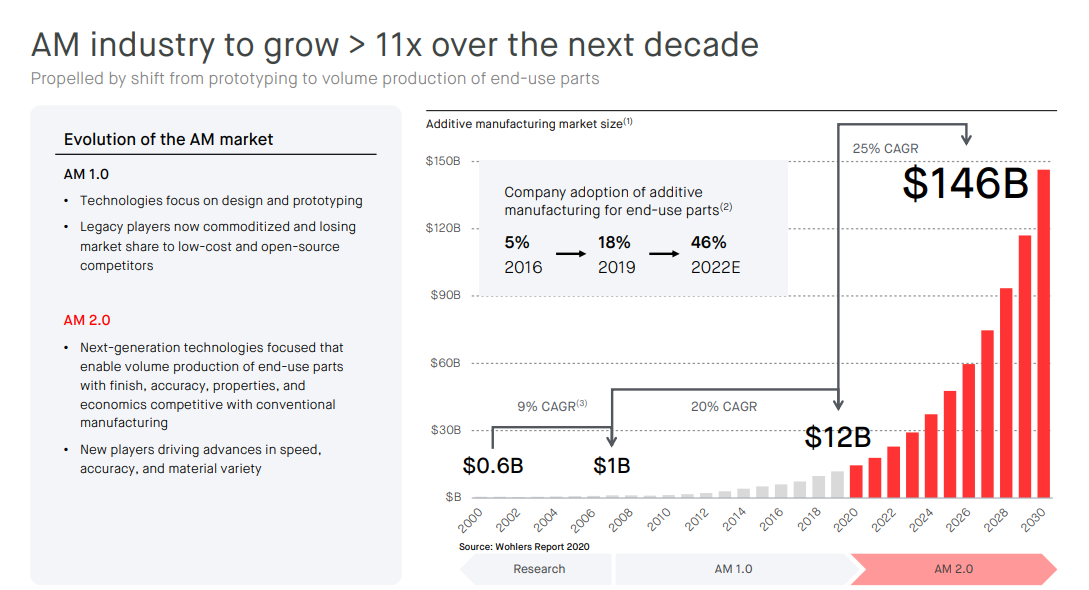

$DM raised $160 million at a $1.5 billion valuation in January 2019 so having the valuation less than double in 2 years seems very reasonable for current shareholders — I’m using the current enterprise value of $2.8 billion. As you’ll learn through this writeup, $DM has enormous potential in this new industry called “additive manufacturing 2.0” which I’ll be referring to as AM to make things easier.

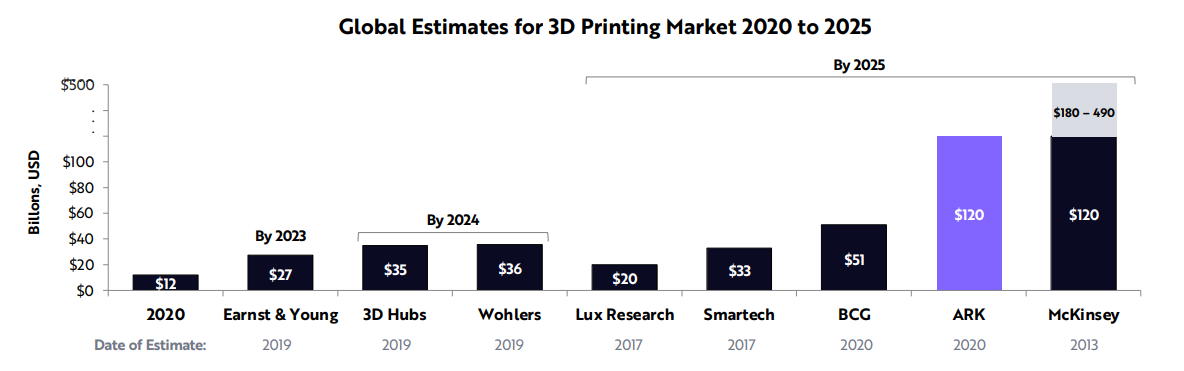

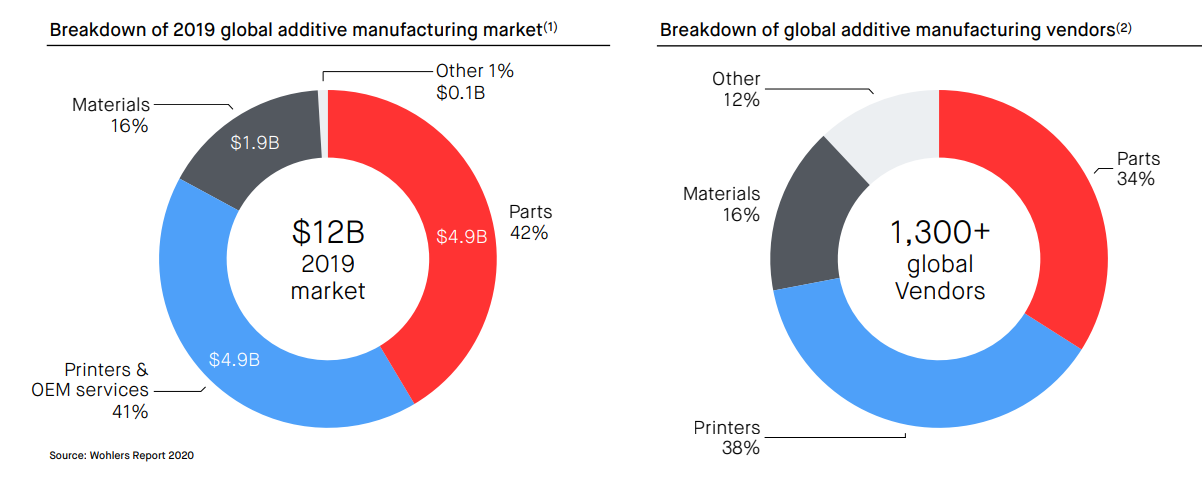

Right now the global manufacturing industry is valued at $12 trillion however additive manufacturing only accounts for $12 billion of this. Based on research from both ARK investments as well as Bill Miller (the famed investor from Miller Value Partners) they believe the additive manufacturing industry will reach $146 billion no later than 2030 with recent comments suggesting it could happen as early as 2025 thanks to recent advances in the hardware, software and compounds being used [click here - slide 85].

Very rarely do investors have the opportunity to jump into a new industry near the beginning and ride the massive growth trends for a decade or longer. In several interviews with Ric Fulop he mentions that investing in additive manufacturing in this decade is similar to investing in the semiconductor industry in the 1970s. My ears perked up when I heard this. If you missed the last decade in software or cybersecurity or solar or electric vehicles, I would not suggest missing 3D printing and additive manufacturing as well. Many experts are calling this the fourth industrial revolution.

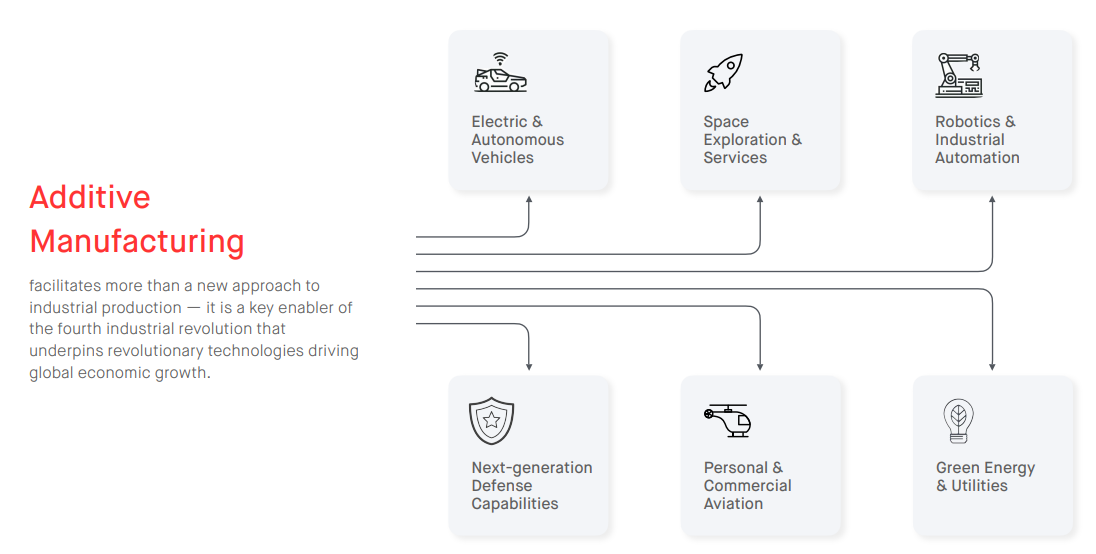

If the additive manufacturing industry really does grow to $146 billion or bigger by the end of the decade and $DM is able to position themselves as one of the leaders for metal, ceramics, aluminum, polymers and other materials/composites not to mention the opportunity in healthcare, dentistry and orthro then it’s possible we could be looking at a 20-bagger or more over the next 10 years. The question is “do we have the conviction and patience to hold that long?” I think I do but only time will tell.

OVERVIEW:

Desktop Metal aka $DM is pioneering a new generation of additive manufacturing technologies focused on the production of end-use parts. $DM offers a portfolio of integrated additive manufacturing solutions for engineers, designers and manufacturers comprised of hardware, software, materials, and services.

$DM solutions span use cases across the product life cycle, from product development to mass production and aftermarket operations, and they address an array of industries, including automotive, aerospace, healthcare, consumer products, heavy industry, machine design and research and development.

The reason that $DM calls this additive manufacturing 2.0 is because they want to highlight the distinction between the legacy 3D printing companies/methods and how far their new technology has evolved. $DM has created high-speed, high-capacity binder jetting systems which are 100x faster than the legacy systems with a cost that is 1/20th of the legacy systems which puts them on par with traditional manufacturing methods that require injection molding, die casting, extrusion, milling or stamping.

$DM believes they are creating a massive shift within the manufacturing industry because now companies can create more complex parts in a faster, cheaper, more efficient and more environmental friendly way.

Using $DM production systems also allows companies to produce their parts locally rather than having to import them from other countries and deal with shipping delays, freight charges, exchange rates, unnecessary transportation emissions and of course expensive tariffs.

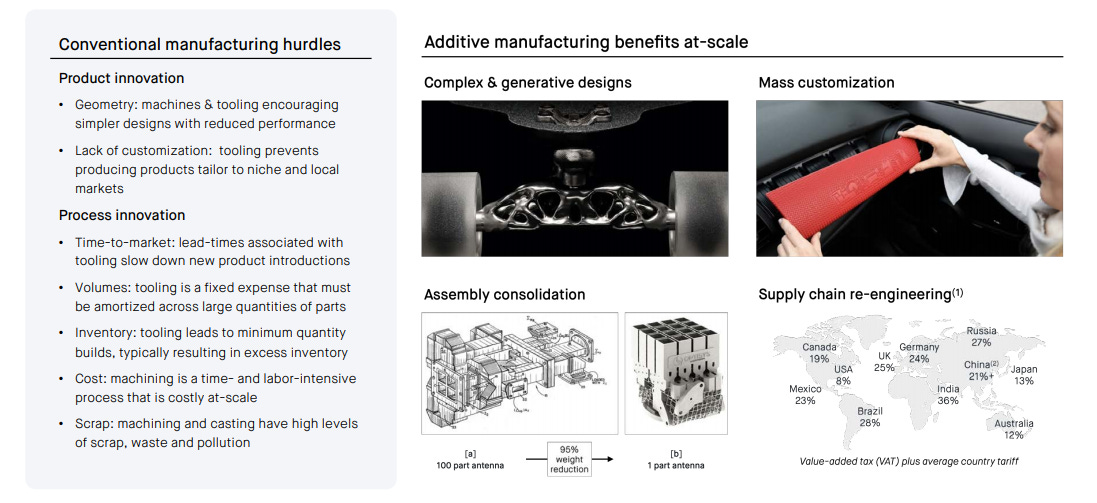

Additive manufacturing eliminates the need for tooling which is expensive, time consuming and not agile because making any design changes would require starting all over. If you’ve ever watched Shark Tank you’ve heard plenty of stories of entrepreneurs spending hundreds of thousands of dollars on tooling, casts, molds, etc.

Now imagine you are a large global manufacturer with dozens of facilities and hundreds or thousands of parts that need to be made every month with constant design changes to improve performance, efficiency, speed, costs, etc — now you’re in the tens of millions of dollars in tooling, casts, molds, etc.

If you are outsourcing this stuff you are dealing with long lead times, minimum volume production runs, time sensitive designs/programming and significant material waste not to mention high shipping costs.

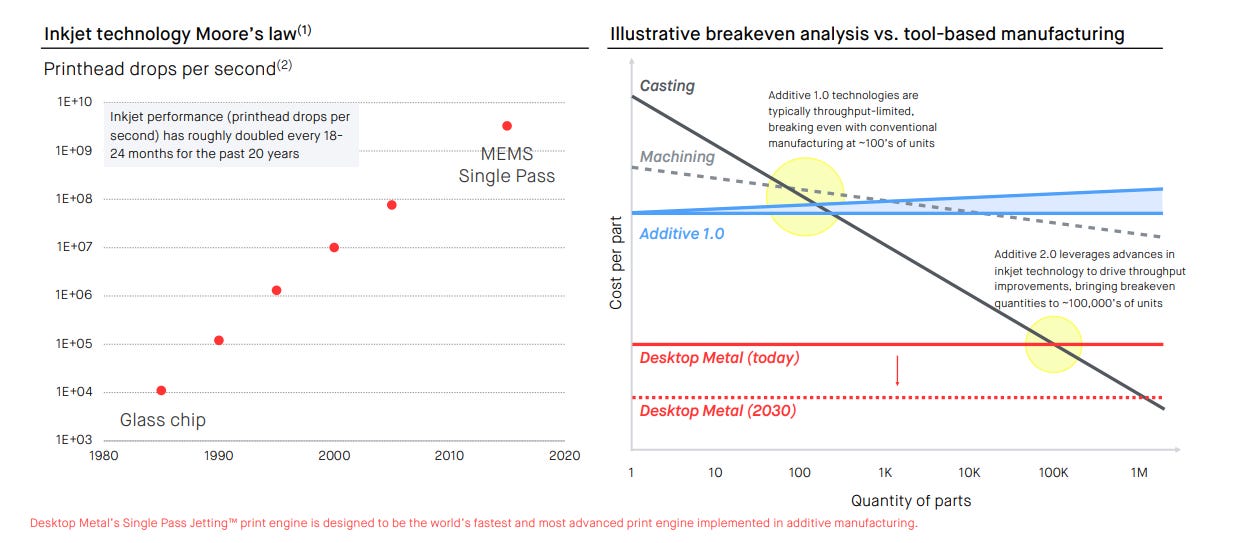

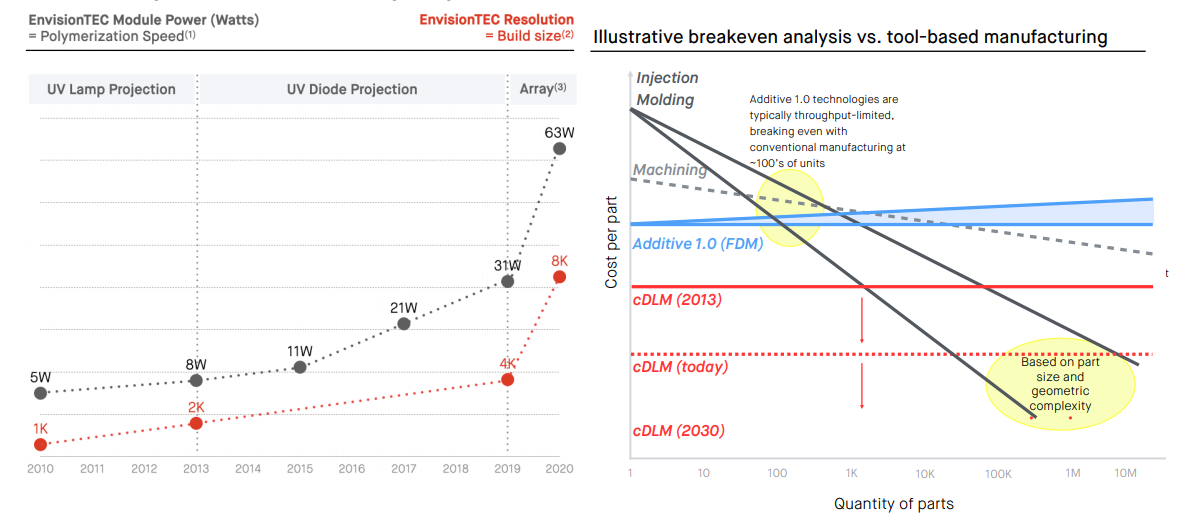

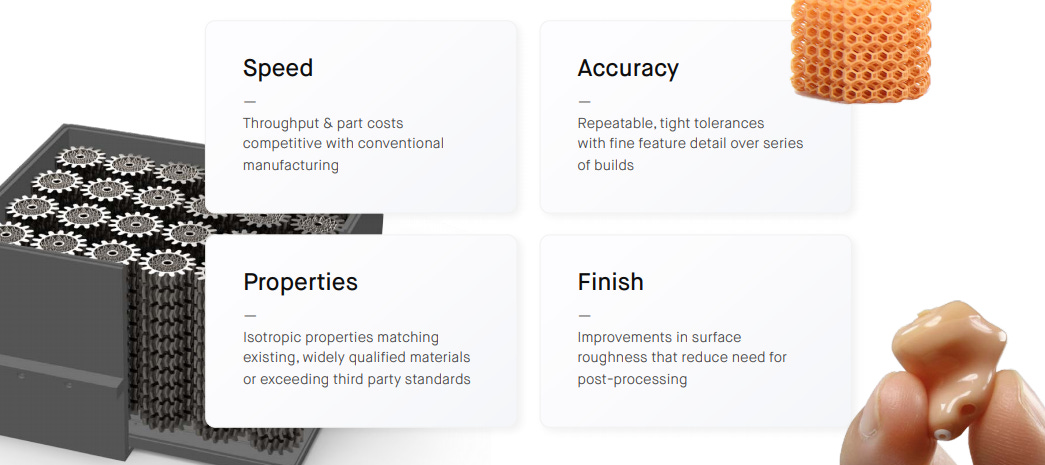

When 3D printing was first getting started most people thought it would only be used for small batch manufacturing or prototypes however given the improvements in technology, increased speed and accuracy, the variety of composites available and now with amazing finishes… finally 3D printing and additive manufacturing can be used for large batch manufacturing because the costs are comparable with traditional manufacturing and it’s a no-brainer on small batch manufacturing as you can see in the chart below.

To summarize this chart is to say that additive manufacturing via production systems like $DM is more cost effective on batches under 100,000 units and within the next decade that number could increase to 1 million.

ARK Investments has said the combination of 3D printing (ie additive manufacturing) and artificial intelligence will enable better designs that are not possible in traditional manufacturing methods. This allows companies to create end parts and products that are stronger, lighter, safer and more durable.

Not only is 3D printing replacing segments of traditional manufacturing but it’s giving designers and engineers capabilities that they never had before. I think the universal slogan for 3D printing should be “if you can dream it, we can build it”

CURRENT PRODUCTS:

Hopefully you listened to the 2020 Q4 earnings call where Ric discusses some of the differences between their different systems [click here].

Rather than go through each of the products and composites I’m going to suggest visiting the $DM website for more information, descriptions, use cases but mostly because of the videos that really make all of this come alive.

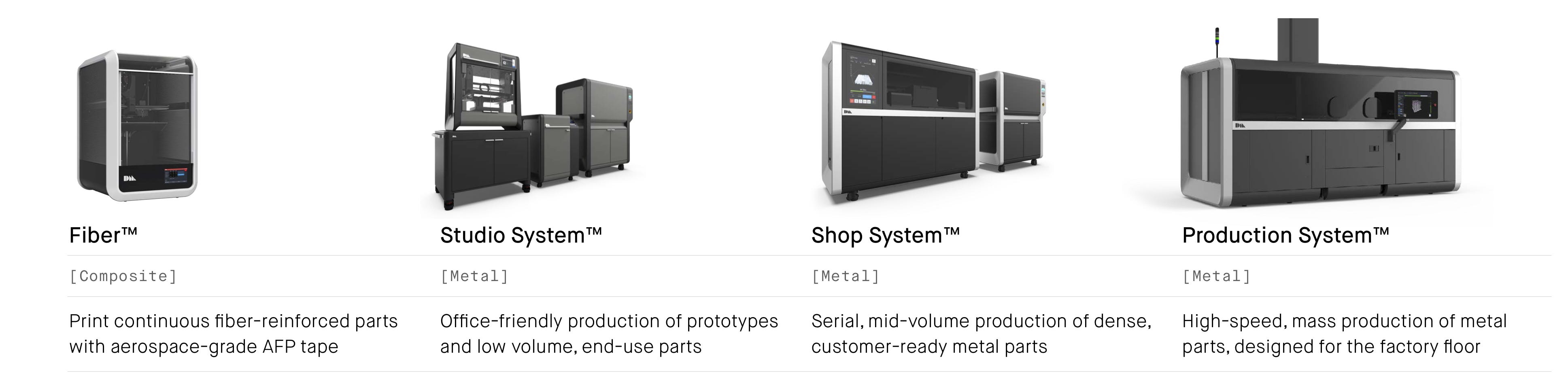

Fiber to print continuous fiber reinforced parts with industrial grade tapes made from different metals and composites available from carbon fiber to stainless steal to copper [click here]

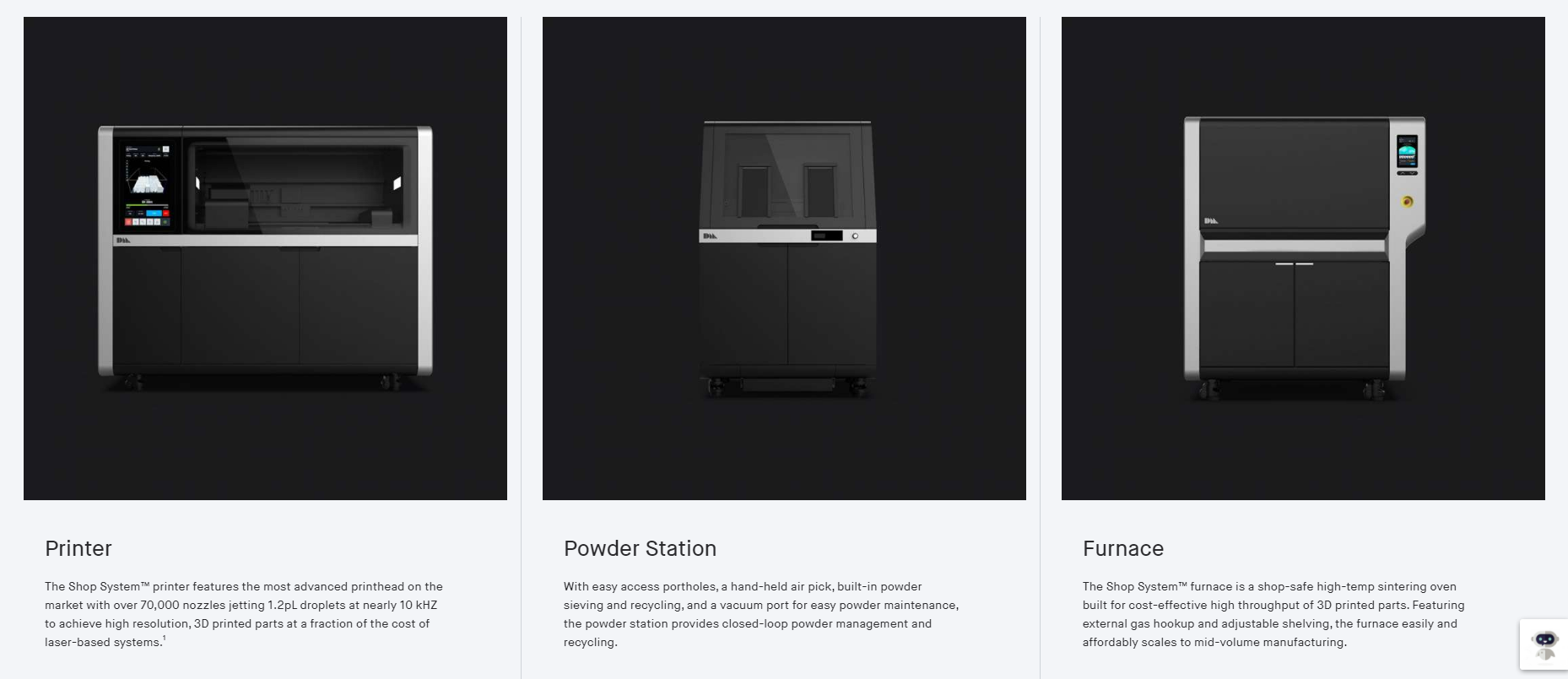

Studio system for small volume manufacturing to make prototypes and replacement parts [click here]. Here’s a customer talking about the studio system and how they are using it in their daily workflow/needs and why $DM’s studio system can do things that traditional machining methods can’t do plus the $DM shop system speeds up wait times on parts/assemblies from weeks/months down to days [watch here].

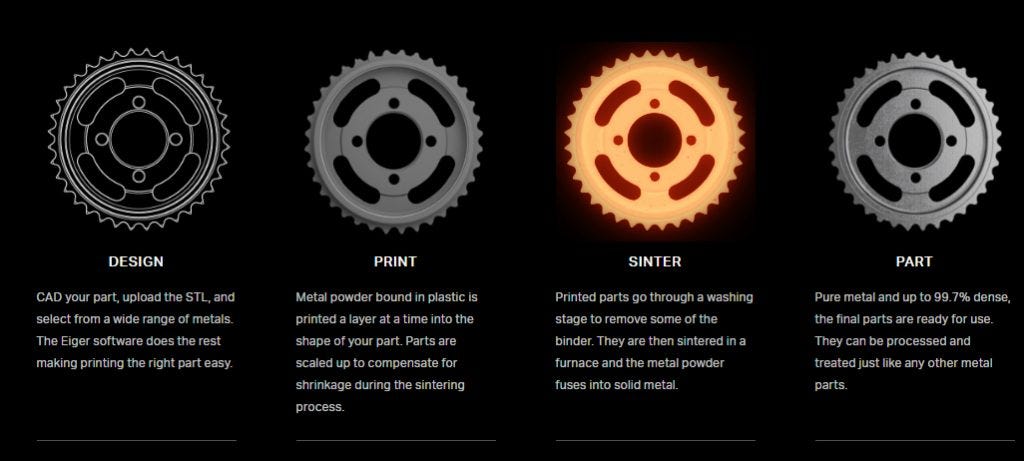

I recommend scrolling half way down the page [click here] to the section “how it works” where you can see the process… prep > print > sinter.

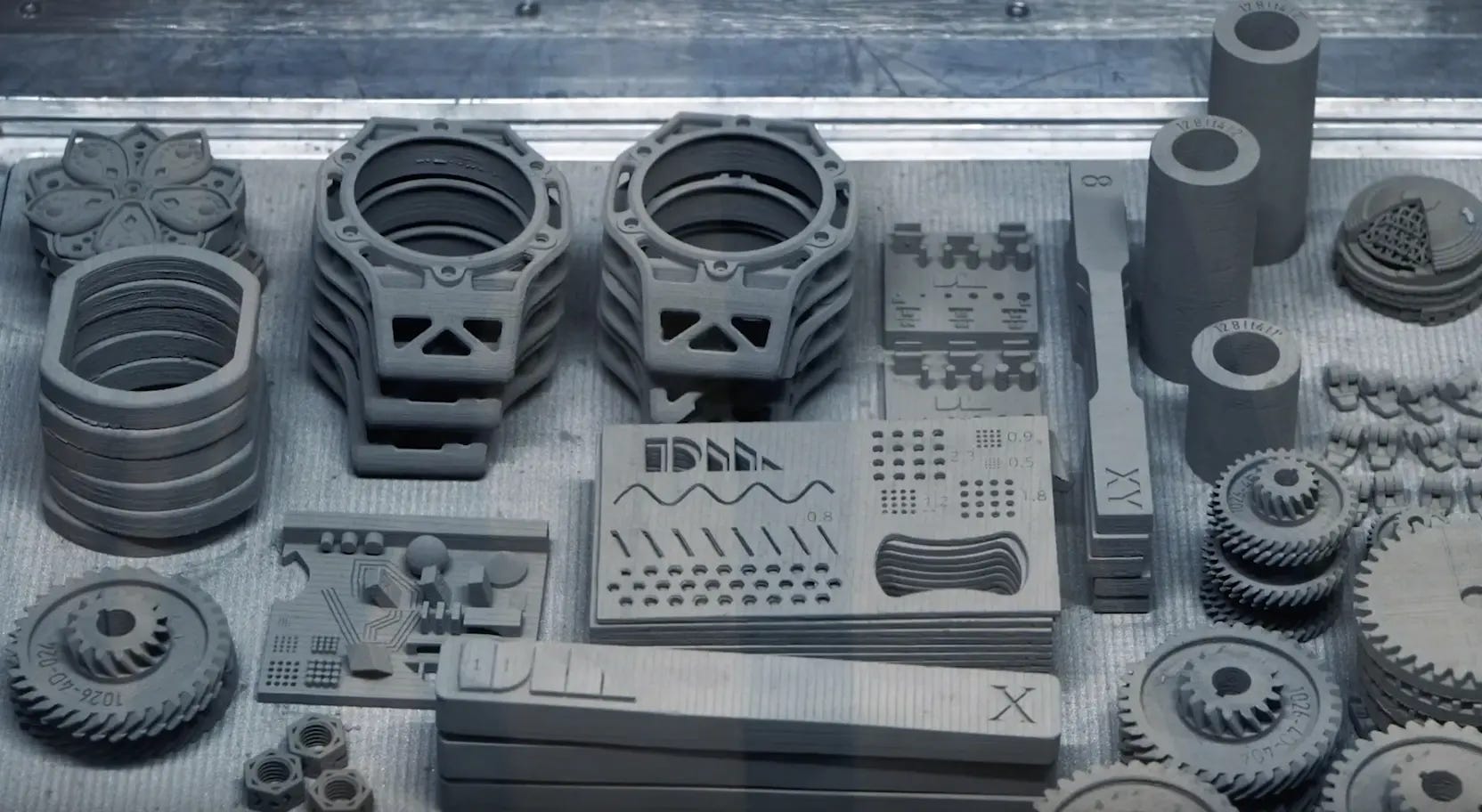

At the bottom you will see a library of just some of the thousands of different parts/products that can be created using the $DM studio system.

Shop system for medium volume manufacturing for machine shops and job shops to make fully dense end-user metal parts [click here]. Here’s a video with the CTO of $DM explaining the Shop system and what it can be used for [watch here]. The big takeaway is that the binder jetting technology is able to use less expensive powders compared to laser printing systems which makes $DM system more cost effective for the customers because cheaper powders means cheaper parts.

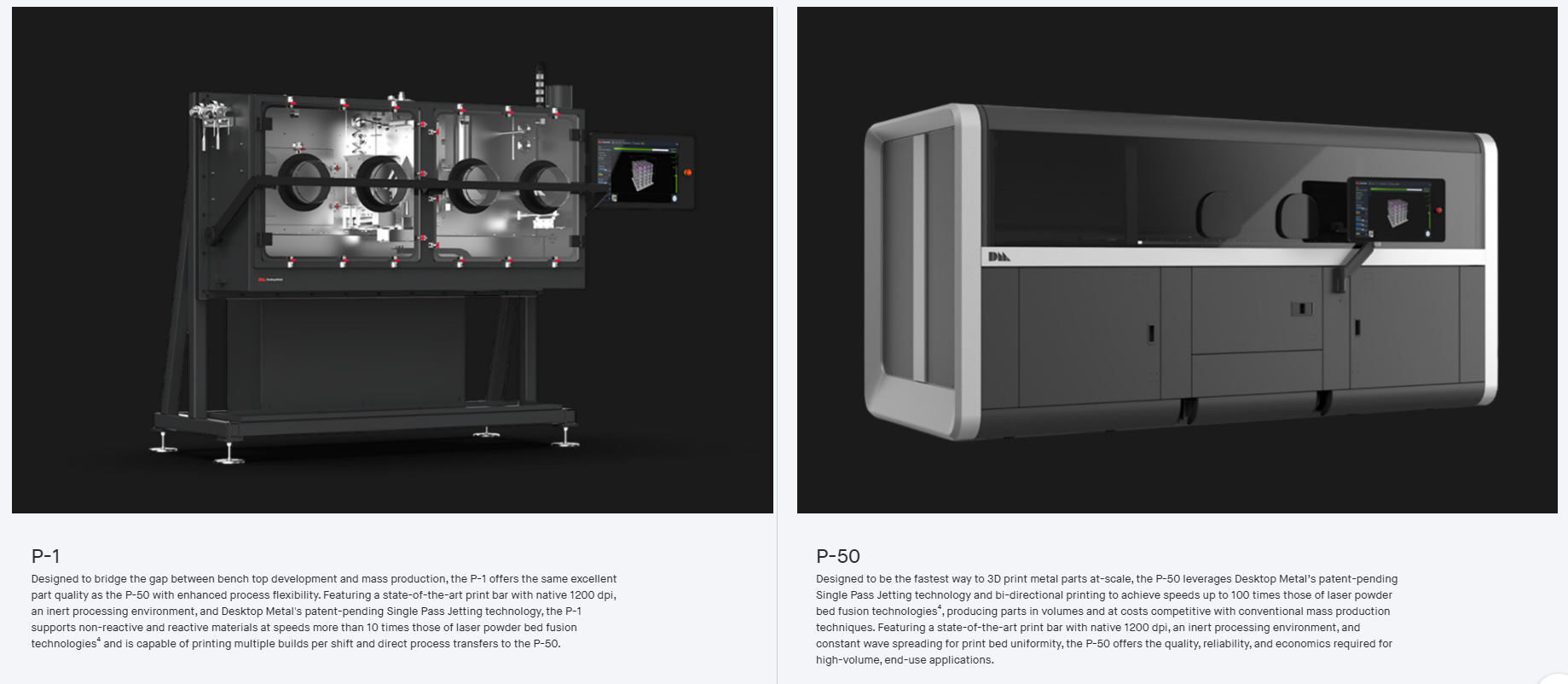

Production system for high speed, high volume, mass production manufacturing [click here]. When you watch the videos of metal parts being made… going from the dry powders to printing to sintering it’s hard not to be in total awe. I especially like the video that shows the side-by-side time comparison between the single jetting system from $DM versus the older laser-based systems.

This gives you an idea of how 3D printing will be used and where the big growth opportunity still remains (hint: end use parts)

PRINTING PARTS:

In one of the webinars with the CTO of $DM he said the “all in” costs including equipment, depreciation, materials, labor and electricity is approximately $1-3 per cubic centimeter.

Some of the materials available for use with $DM equipment include fiber composites (ie carbon fiber), 17-4 PH stainless steel, 316L stainless steel, H13 steel, 4140 steel and copper [click here for more details on each material plus data sheets]

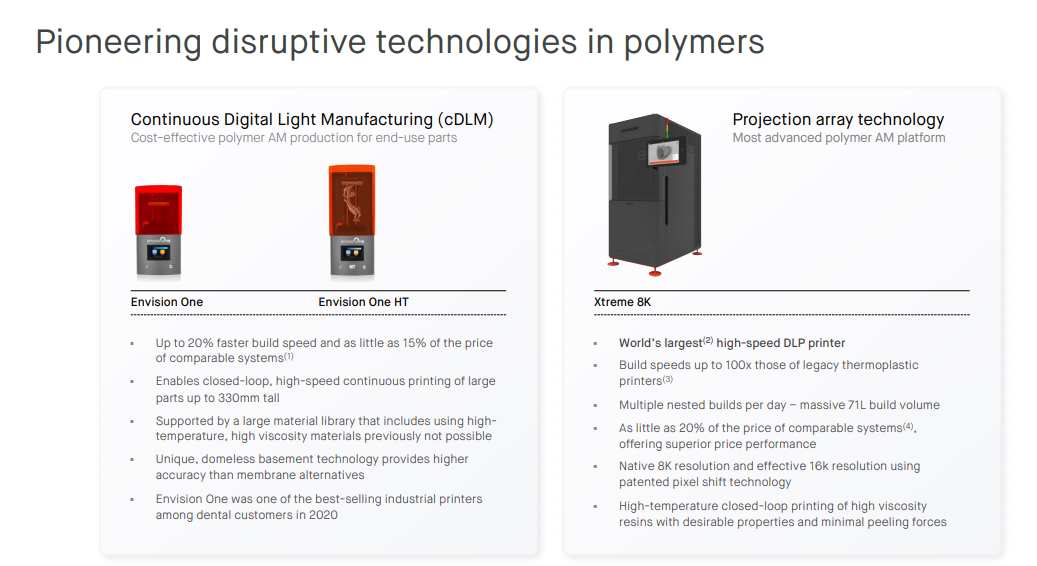

ACQUISITION OF ENVISIONTEC:

This acquisition is big news for $DM shareholders because it expands their TAM, capabilities, and product portfolio to include photopolymer 3D Printing, digital biofabrication and digital casting.

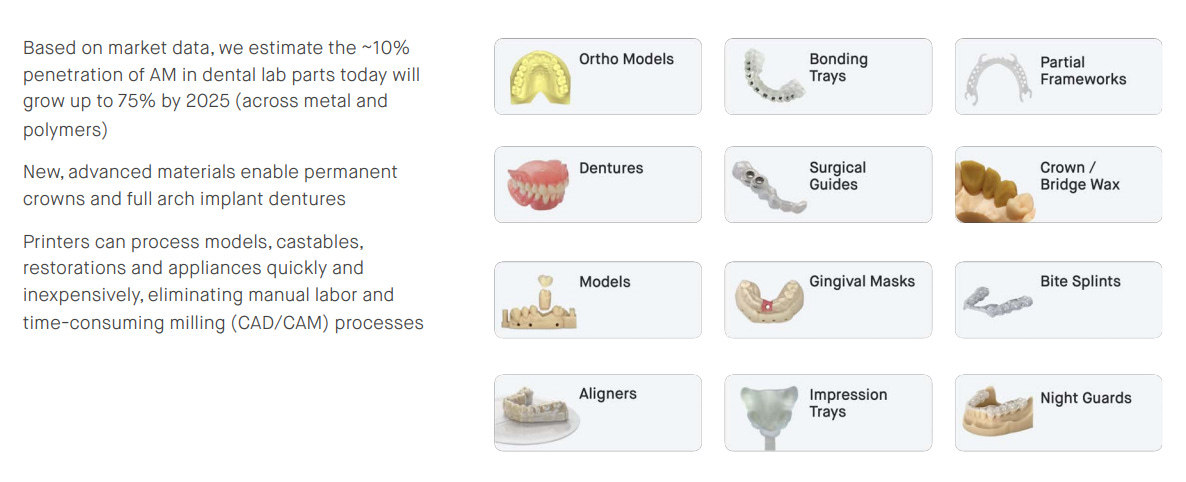

These new technologies help open up markets such as healthcare, dentistry, ortho and jewelry which are all massive opportunities for 3D printing and additive manufacturing. This acquisition led to the launch of DesktopHealth.

EnvisionTEC will operate as a wholly owned subsidiary of Desktop Metal and be led by the company’s founder Al Siblani.

EnvisionTEC has one of the strongest IP portfolios in the photopolymer 3D printing market with 140+ issued and pending patents. EnvisionTEC has 190+ qualified materials and 5,000+ customers across a broad range of industries including automotive, aerospace, medical devices, jewelry, and biofabrication but their biggest market is probably dental with 1,000+ customers using their 3D printing technology for parts and end-use products.

This acquisition makes $DM the leader in both metals and polymers.

Similar to the graph I showed earlier on volume manufacturing for metals, here is one for polymers and as you can see 3D printing for polymer based parts/products is much cheaper than traditional injection molding or machining methods.

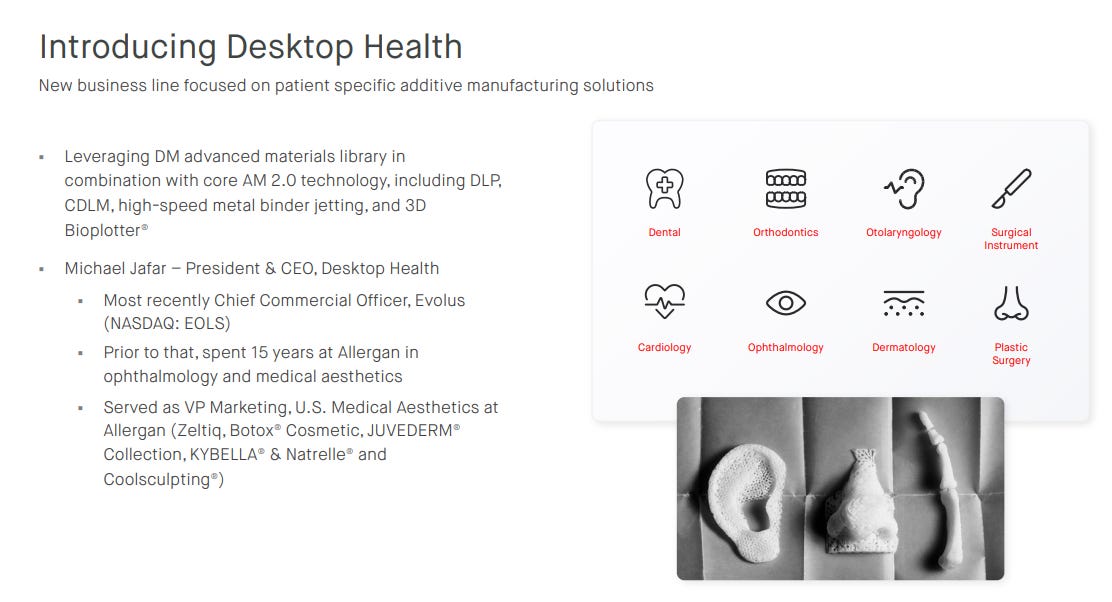

DESKTOP HEALTH:

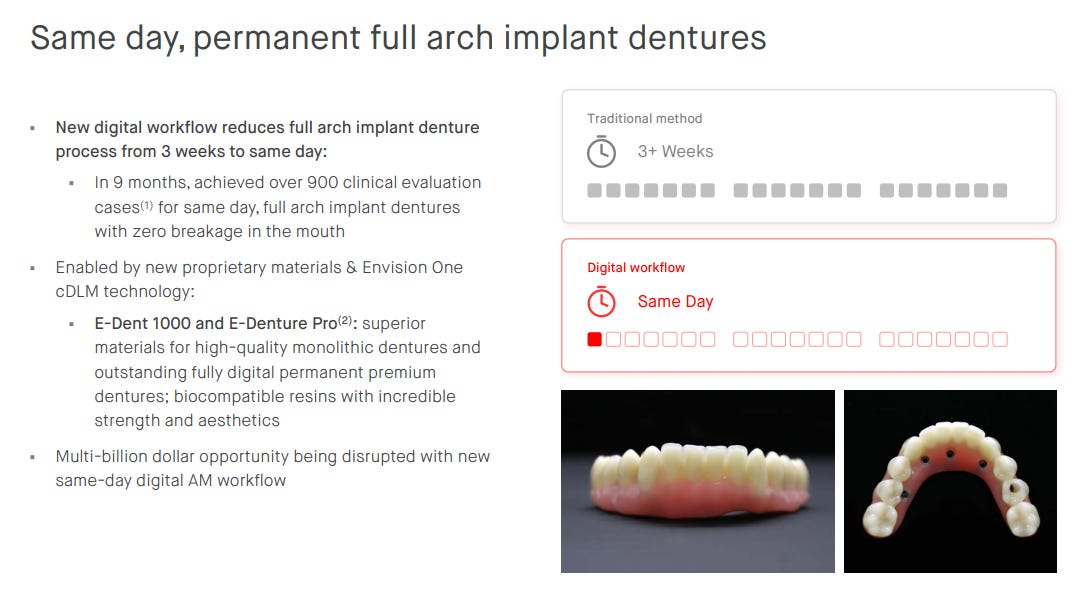

$DM has stated that Desktop Health is going after a $30+ billion TAM where many of the parts and products used in healthcare, dentistry, ortho and other areas could and should be using 3D printing because it’s faster, cheaper and more customizable. Ric mentioned on the earnings call [listen here] that many dental products could be custom designed and printed in hours/days versus weeks by using their 3D printing systems.

Next month I’m going back to the dentist to have customer mouthguards made for both daytime use and nighttime use because I clench my teeth when I’m stressed, working out and sleeping. These mouthguards are going to cost me $650 each which seems outrageous plus they’re going to take several weeks because of the conventional process with molds that is current used. I have a feeling these products will eventually be done using 3D printing with special polymers.

BUSINESS MODEL:

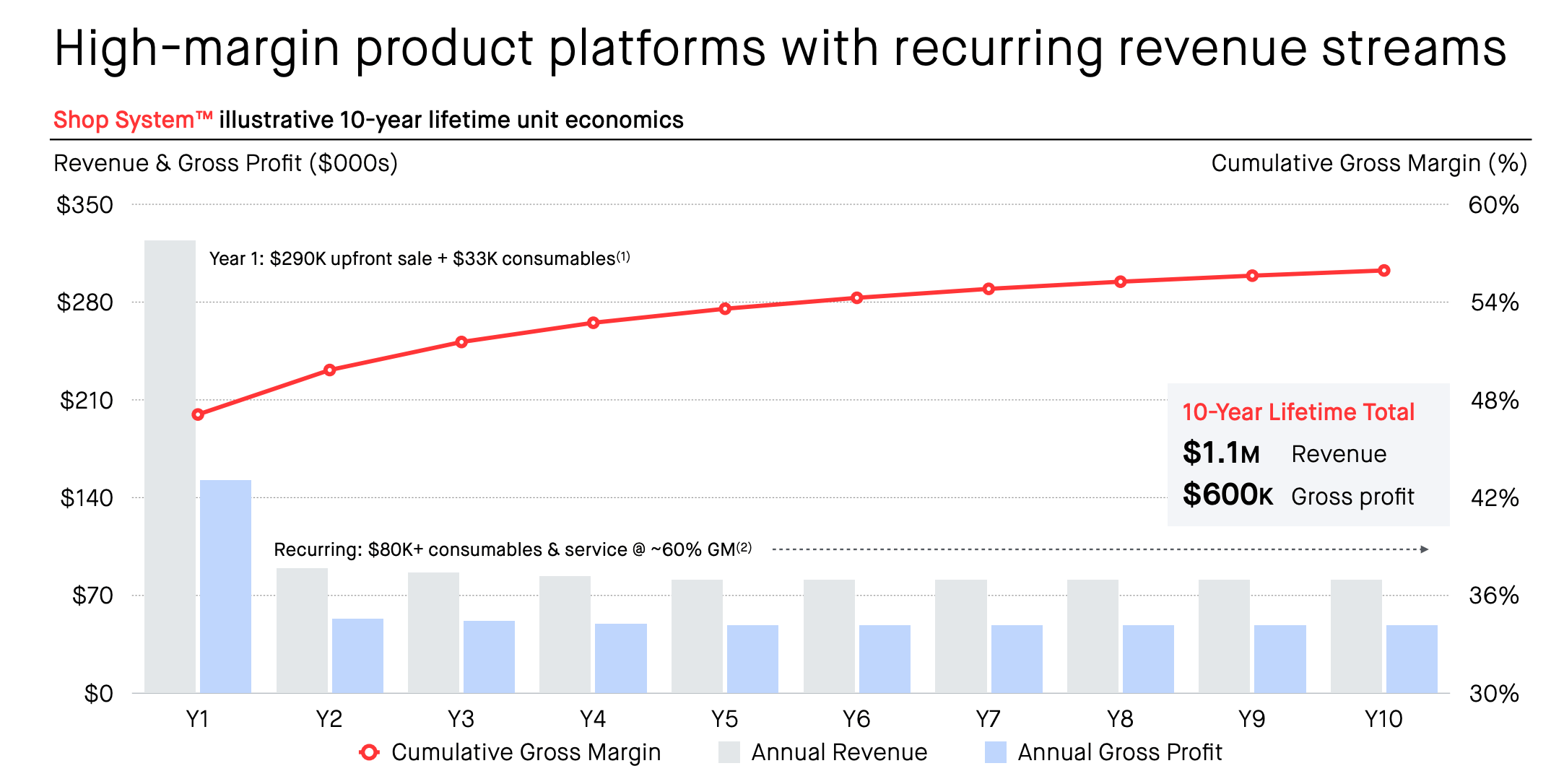

On the earnings call Ric Fulop even referred to the $DM business model as the well documented “razor blade” model where a company sells the customer a product and then that customer has to keep buying refills/services in order for that product to continue functioning. This was true with $TMDX (TransMedics). This was true with $CLPT (ClearPoint). This is also true with $DM (Desktop Metal).

$DM sells the machines to the customer (at a profit) and then continues to make money off that customer from consumables (software, binders, powders, warranty, etc).

As you can see from the example below, selling the P-50 system to a customer would bring in $2.2 million upfront but another $4.3 million over the next 10 years from the consumables (ie razor blades) for a total of $6.5 million of which $3.8 million is gross profit for a 10 year gross margin of 55%. These margins are much better than traditional manufacturing companies and it’s because of the consumables component.

GROWTH STRATEGY:

$DM is already working with some of the largest manufacturers in the world from automotive to aerospace to medical to consumer goods and many more. These companies are already transitioning aspects of their manufacturing process over to additive manufacturing because of the cost savings, customization and flexibility especially on small batches. Now with the help of 200+ distribution partners around the world we’re going to see shipments of their different models ramp up over the next few years. In all of my research it seemed like the big hurdles were speed, accuracy, different metals/composites and cost — $DM has gotten all of this figured out which is why I believe now is the time when we see additive manufacturing hit that inflection point which could lead to a decade of outstanding growth for companies like $DM and others in this space.

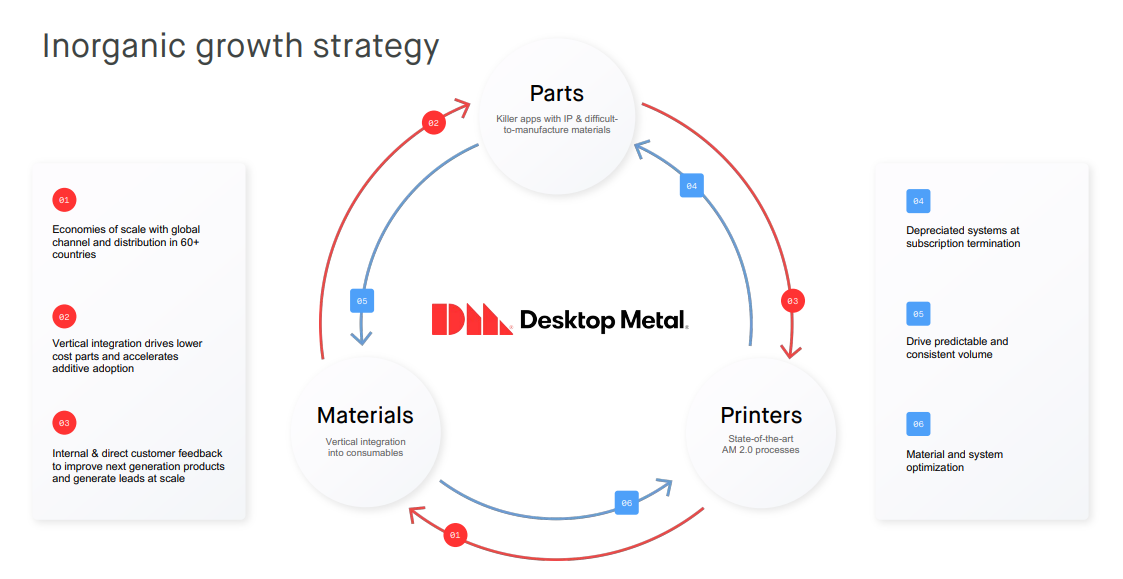

This image below is just another way to think about the business model and how one piece of the growth engine feeds into the next piece. Better machines/printers means better parts which means more materials being consumed because customers are happier with the final part/product. More parts also means more cost savings for the customer which means they order more machines/printers to scale up their manufacturing even more which just keeps the cycle going around and around.

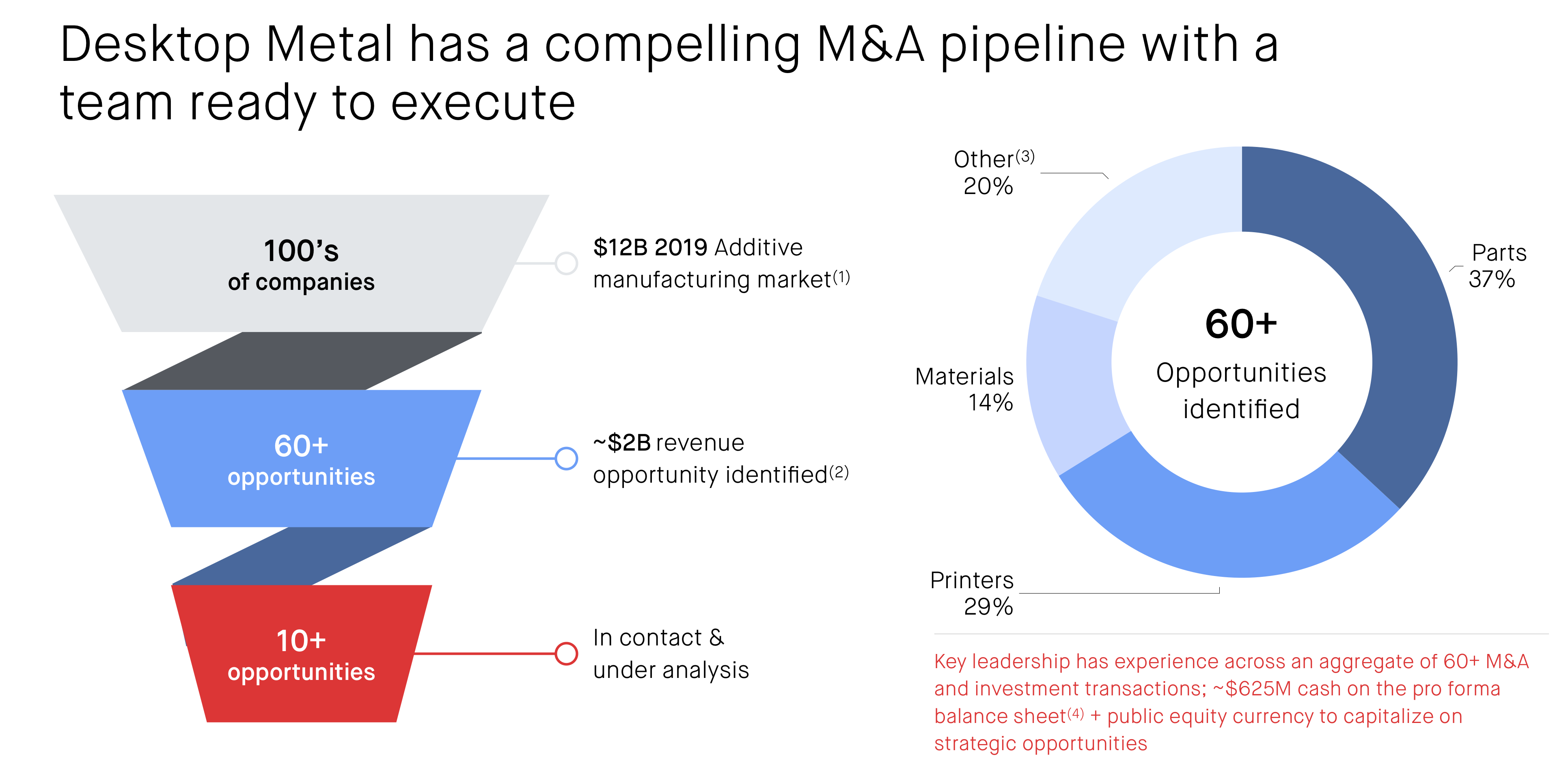

$DM has shown us with the acquisition of EnvisionTec that they are willing and able to do M&A in order to beef up their platform, product library and patent portfolio. $DM might have started in metals but now they are expanding into different composites and polymers which continues to expand their TAM by getting into new industries and geographies. I believe one of the reasons that $DM came public via SPAC in 2020 is because they saw significant acquisition opportunities on the horizon and knew those deals would be easier to complete as a public company (using stock as currency) rather than a private company. As the $DM stock price continues to increase it should make deals easier to pursue because the economics will be more favorable. Typically you don’t want to see companies doing M&A deals when their stock price is undervalued because then they are being forced to overpay for an asset unless it’s a small bolt-on acquisition and they can just use cash off the balance sheet.

CUSTOMERS:

As I mentioned earlier, $DM already has an impressive list of customers using their products. I assume some of these customers might still be waiting on the higher end models depending on how many they are expecting but I will ask Ric this question when I interview him in a couple weeks.

Several of these customers (Koch, GE, BMW, Ford and others) were also early investors in $DM so they know the company/products very well. Whenever you see future customers jumping into the early investment rounds of a company like $DM it should give you a sense of security knowing those companies not only did their due diligence on the technology, patents, etc but that they also see a massive opportunity within their respective industries.

I can’t help but wonder how many car parts and airplane parts might someday be made through 3D printing and additive manufacturing.

If you’d like to read some case studies on how these customers are using $DM’s machines/technology to optimize their manufacturing processes you can do so [click here]. I recommend starting with this video from Ford [watch here] where they talk about the integration of 3D printing as the “factory of the future”.

TAM / MARKET OPPORTUNITY:

I might never be an expert in 3D printing or additive manufacturing despite spending more than 40+ hours over the past couple weeks going through investor presentations, SEC filings, white papers, case studies, earnings reports, industry reports and watching hours of videos, interviews, webinars, and customer reviews — I still don’t know everything that I want to know about this industry or the future of additive manufacturing however it doesn’t take a rocket scientist to look at the chart below and appreciate the tremendous growth opportunity that lies ahead for companies like $DM.

Whether you listen to Ric Fulop (CEO) or Cathy Wood (ARK Investments) or Chamath (Social Capital) or Ron Baron (Baron Capital) or Bill Miller (Miller Value Partners)… each of them are considered to be the best investors of our generation and each of them predicts additive manufacturing is going to be a $100-200 billion industry by the end of this decade and each of them is invested in $DM either personally and/or through their funds.

Now that $DM is not only doing metals but also getting into different composites and polymers with the fastest and most efficient machines on the market, I like the potential upside with $DM. They also have the most robust patent portfolio of any other company in this space which should/could be a competitive advantage moving forward.

FINANCIALS:

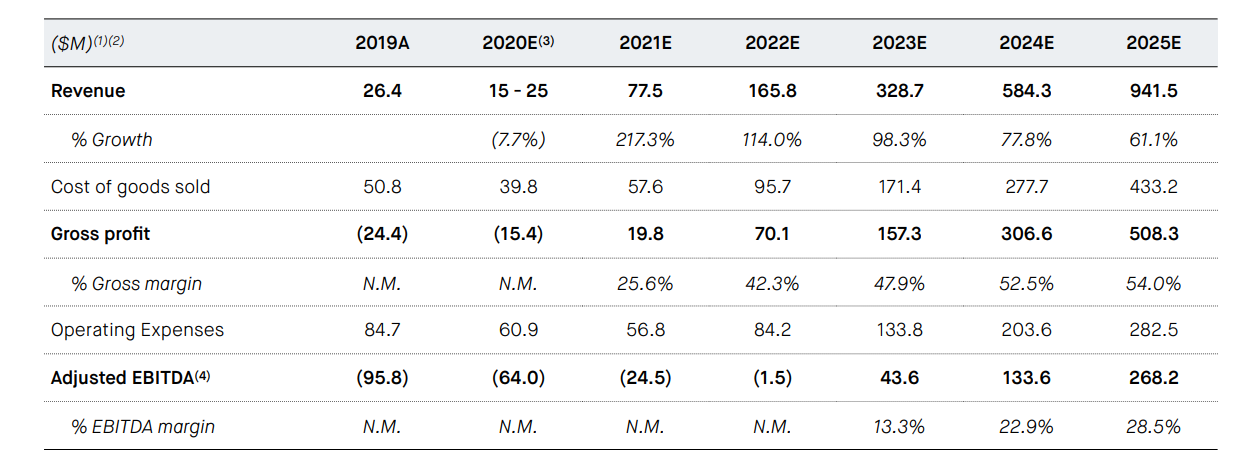

$DM is going to put up massive YoY growth numbers in 2021 but this is obviously not sustainable — this is because 2021 in the year when many of their products start shipping in higher volumes.

I think it’s more important to look at 2022 when revenues could reach $200 million and then start forecasting for the next 3-5 years. $DM stated in their SPAC investor presentation that they believe they can get close to $1 billion of revenues in 2025.

If you work backwards and assume $100M in 2021, $200M in 2022 then 70% CAGR for 2023, 2024 and 2025 you get to $980M+

If $DM can get to $980+ million in revenues in 2025 then we’re probably talking a $12-16 billion company which would be a 50% CAGR on stock performance over the next 4+ years.

A few things stand out when I look at the financials for $DM:

1) Revenue growth is spectacular and should remain strong for the next 5-10 years as the 3D printing and additive manufacturing markets do a potential 12-bagger through the end of this decade. Based on my numbers above I believe $DM’s revenues could be up close to 900% over the next 4+ years through 2025, if $DM can pull this off the stock should do quite well.

2) $DM is still losing money and probably won’t be profitable for another couple years however this is quite common with early stage, high-growth stocks that need to focus on growth, customer acquisition, market share, R&D and so forth. If you believe $DM has the potential to be a 5-bagger over the next 4-5 years then you shouldn’t be overly concerned with short term losses. They also have no debt and a very strong balance sheet with $500+ million of cash from the SPAC + PIPE. Like I mentioned in the very beginning… investing in $DM right now is quite similar to investing in their Series F-round if they were still private. You need to have this mindset in order to invest in these transformational companies with very ambitious goals and long runways of growth ahead.

3) Gross margins are not the best however we discussed this above because short term margins don’t look amazing because the numbers you see below are mostly for the printers however over the life of the machines the customer will be using all of those consumables which are much more profitable for $DM and bring the 10-year gross margins up to 55% so that’s what I’m focused on. As $DM gets more printers deployed over the coming years and some of those consumable numbers become a larger % of the total revenues I expect we’ll see these gross margin numbers creeping higher.

These were the numbers from the SPAC investor presentation but they are already outdated and too conservative considering Ric’s recent comments plus the acquisition of EnvisionTEC.

Here is the entire SPAC investor presentation [click here]

CURRENT VALUATION:

If you want to value $DM based on trailing revenues then of course the stock looks crazy expensive but that’s not how I value stocks. I don’t care what the last 12 months looked like because those numbers are already baked into the current price. Investors should always be looking 12-24 months into the future when doing their valuations, especially if they are longer term investors.

If we assume $DM can do $200+ million next year then the stock trading at 12.5x 2022 EV/Sales is pretty fair considering the revenue growth and the LTV of those customers with the “razor blade” business model. Don’t forget that the 10-year revenue value of a machine is 3x the initial customer purchase price because of all those consumables.

I’m not going to post a $DM chart in this writeup but feel free to go look at one — the stock was trading close to $35 a couple months ago at which point the valuation was definitely stretched but now that the stock has pulled back to $12, this feels like a really great entry price, especially for longer term investors who are willing to add on any dips/pullbacks.

**In full disclosure $DM was trading at $14.00 last Tuesday when this writeup went out to the paid subscribers. Unfortunately growth stocks have been getting hammered the past few days including $DM but now I think the risk/reward is even more compelling.

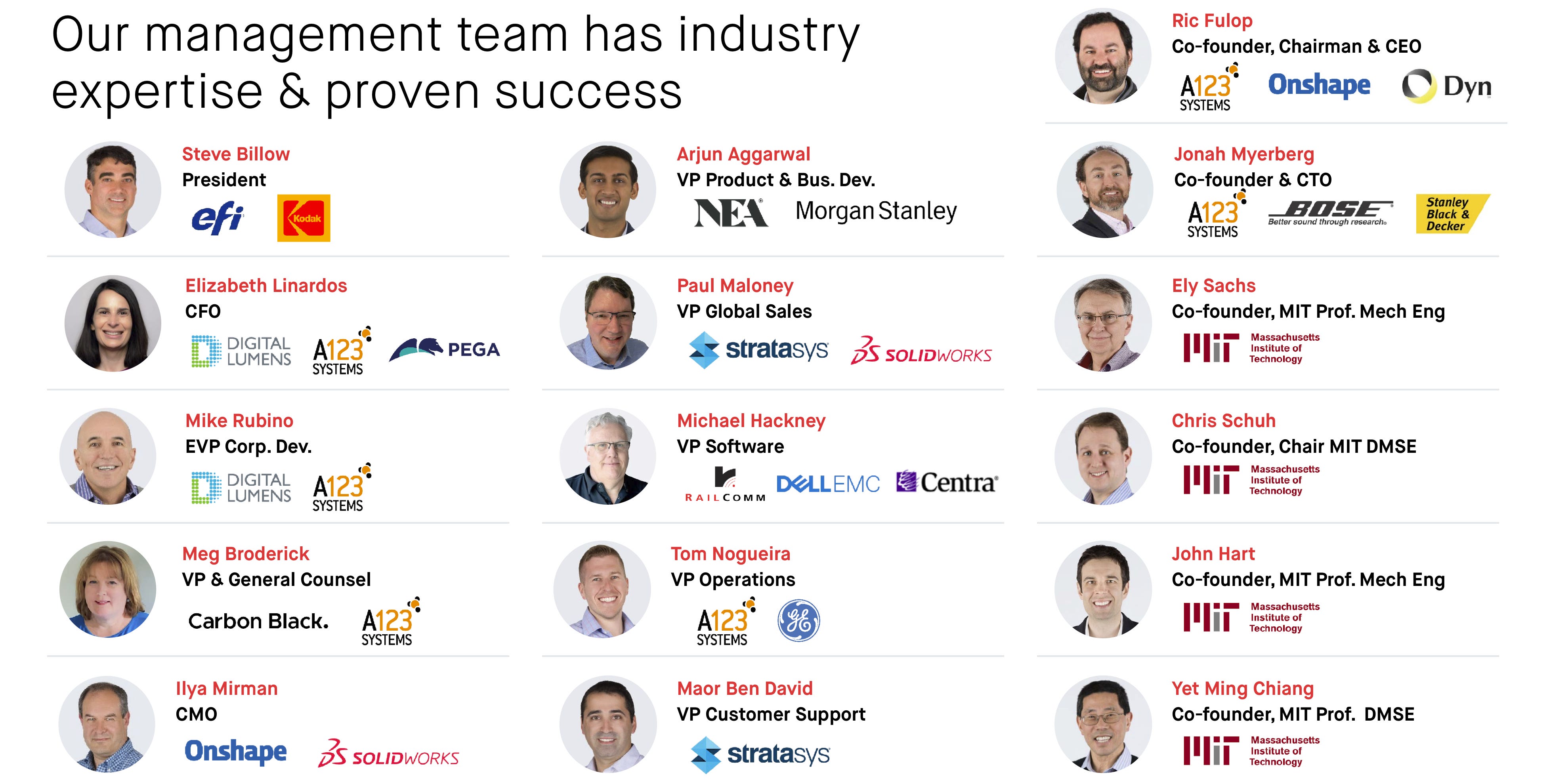

MANAGEMENT and BOARD OF DIRECTORS:

There’s a lot of talent and experience on this team. I know the 3D printing market is getting more competitive but you’d have a hard time finding a stronger, smarter team than this one.

See the entire team [click here]

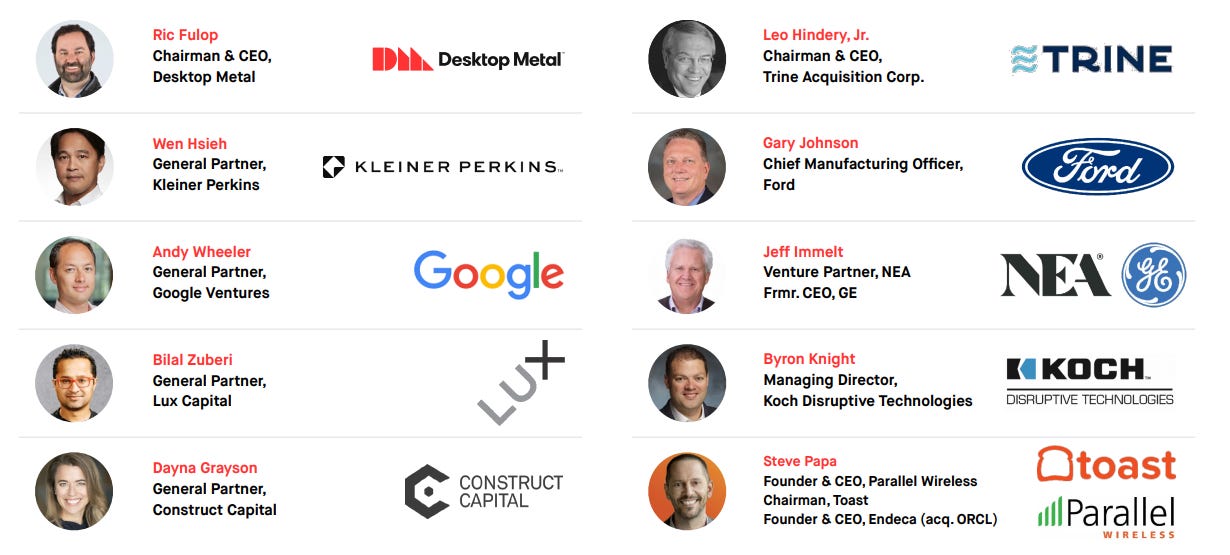

Here’s the Board of Directors, feel free to dig into any of them and you’ll realize this is an incredibly accomplished group of entrepreneurs and investors.

SHAREHOLDERS:

ARK Invest has a 2.6% weighting to $DM in their 3D Printing ETF [click here]

If I was going to list out the major risks with $DM I’d start with the competition from other 3D printing companies however if I was going to list out the major risks with the stock price I’d start with how many of the early stage VC’s are still large shareholders and when they might need to start selling their shares in order to return that capital to their LPs (limited partners). Some of these investors might be locked up for 6-12 months after the IPO date (or when $DM officially started trading) however that 6-month lockup is coming soon so we could see some pressure on the stock from these VCs selling. I’m not saying it’s going to happen or how much pressure there might be on the stock but it’s something to keep in mind.

CONCLUSION:

I’m clearly a big fan of $DM as well as the 3D printing industry but additive manufacturing more specifically. I really didn’t know much about this industry prior to doing my due diligence on $DM so I can now say that my perception has changed. 3D printing is no longer about making toys and junky little knick knacks in small batches. This new 3D revolution has taken the next step forward thanks to companies like $DM where large volume, high-speed manufacturing is now possible thanks to better hardware, better software, better materials and real economies of scale.

This industry certainly has it’s competitors so it won’t be an easy journey for $DM but I believe they have positioned themselves very well to capitalize on what appears to be a massive growth trajectory in additive manufacturing especially with the acquisition of EnvisionTEC and future M&A deals to come.

I spoke to Ric last week and he agreed to do an interview with me after they report Q1 earnings in early May — even cooler is that we’ll be doing the interview at the Desktop Metal headquarters in Burlington, MA which will allow me to take a tour of the facility and see some of these machines up close and personal. I look forward to sharing some great pictures and videos with everyone from that trip.

**I have a 6.5% position in $DM in my personal portfolio**

If you have any questions about $DM or any other stocks I have covered in the past, please feel free to reach out and I’ll do my best to answer them for you.

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Stocks mentioned in this newsletter should only end up in your own portfolio after you conduct your own research and due diligence. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletter. Please manage your own portfolio and position sizes in accordance with your own risk tolerance and investment objectives.