Deep dive on ChargePoint ($CHPT)

Deep dive on ChargePoint ($CHPT)

In addition to my Substack newsletter, I also run a Stocktwits room where I post my current holdings, buys & sells, investment models, technical analysis and market commentary for both my Investment Portfolio (long term, strong fundamentals, 20-30 holdings) and my Trading Portfolio (short term, strong technicals, 0-10 holdings). The two options are $15/month for the monthly plan [click here] or $150/year for the annual plan [click here].

You can now signup for my new Substack called Jonah’s Trading Charts which is focused exclusively on the technicals — every day (usually pre-market) I’ll send out an email with my favorite trading charts/setups. You’ll also have access to my trading portfolio with current positions/sizes, entry/exit prices, profits/losses and much more. I’m also doing live charting and live trading 3-4 times per week.

Company: ChargePoint

Ticker: (CHPT)

Website: ChargePoint.com

IPO (deSPAC) date: March 1, 2021

IPO price: $26.13 (SPAC price $10.00)

Current stock price: $14.50

Outstanding shares: 339 million

52 week high: $28.72 on November 17, 2021

52 week low: $8.50 on May 12, 2022

Market cap: $4.915 billion

Enterprise value: $4.761 billion

Headquarters: Campbell, California, United States

Number of employees: 1500+

Average price target from analysts: $23.21 or 60% higher from the current price

Investor Relations [click here]

Q2 2023 Earnings Report [click here]

Q2 2023 Earnings Webcast [click here]

Q2 2023 Earnings Call Transcript [click here]

Q2 2023 Earnings Presentation [click here]

Investor Presentation, September 2022 [click here]

Outline

Introduction

Company Background

Opportunity

Technology

Business Model

Customers

Competitive Advantages

Management

Culture

Financials

Key Metrics

Risks

Ownership

Valuation

Investment Model

Analysts

Technicals

Conclusion

Introduction

I’m definitely bullish on CHPT for the next 5+ years as the world migrates from ICE (internal combustion engine) to EV (electric vehicle) which means as we go from 2-3% EV adoption to 30-50% EV adoption (over the next 10 years) we’re going to see EV charging stations all over the place and right now CHPT is one of the clear leaders in this category. Overall I think EV adoption is good for the planet but it’s certainly not as perfect and as environmental friendly (or grid friendly) as some would have you believe. Right now the world is dealing with an energy crisis (mostly because of Russia) so it will be interesting to see how things unfold over the next 5-10 years from oil exploration & production to more alternative energy projects (mostly solar) to building more nuclear power plants (China is all over this). As a society we’re depleting some of our energy resources faster than we can replenish them and thanks to the Covid disruptions and the Russia/Ukraine war we’re now suffering the consequences with oil and natural gas prices hovering near historic highs.

Now back to CHPT, as you’ll learn in this writeup CHPT is building a global EV charging network, with their current focus on the United States and Europe with more than 200,000+ activated ports. You’ll always read about their business model which is similar to companies like STEM where there’s an upfront hardware component and then ongoing software subscription component which means gross margins start low but climb higher over time. Once the customer has the hardware, the software subscription fee becomes very sticky and very profitable for CHPT.

We’ll discuss valuation later but I do think CHPT is compelling in the mid-teens ($13-16 per share). I started a position in CHPT a few weeks ago and I will continue adding to this position as long as the fundamentals stay strong and the company executes on their strategy. Based on the Q2 results they reported last week, I believe they’re doing the right things and heading in the right direction especially as their supply chain problems are easing up and hardware costs are coming back down which is already helping their gross margins which improved from 17% in Q1 to 19% in Q2.

If we look out 4-5 years I believe CHPT can have 40-45% gross margins which should translate to 15-20% net income margins so even though CHPT is not profitable today, which means they are burning cash and will probably need to raise more capital in the next 4-6 months, I do see them being profitable in 3-4 years at which time we’ll see significant earnings growth. Right now the stock is trading at ~10x FY2023 sales which I think is fair for a company growing revenues at ~100% YoY despite the losses and negative operating margins. Those margins will continue get better in the coming quarters as the software revenues become a larger part of the overall revenues (similar to STEM and other companies with this same hardware/software business model).

As the EV wars heat up between Tesla, General Motors, Ford, Toyota, Volkswagen and all the others… rather than trying to pick which automaker will do the best, I think CHPT gives you a different and perhaps safer/smarter way to play the EV boom that we’re seeing across the globe. Just like Starbucks announced a few weeks ago the installation of CHPT chargers across Utah & Colorado, I believe we’re going to see hundreds of announcements like this. Eventually every shopping center, coffee shop, strip mall, hotel, restaurant, gym, university, apartment/condo building, etc is going to have EV chargers installed so they can attract more customers, keep customers there longer and perhaps even generate additional revenues.

Based on my financial projections I think CHPT can be a $50-60 stock in the next 4-5 years so I’ll use any market pullbacks to increase my position.

Company Background

ChargePoint (CHPT) was founded back in 2007 under a different name, Coulomb Technologies, by five founders, Dave Baxter, Harjinder Bhade, Milton Tormey, Praveen Mandal, and Richard Lowenthal. The latter was the company's first CEO until 2011, when the current CEO, Pasquale Romano, joined the company. Lowenthal moved to a Chief Technical Officer position for a couple of years before officially retiring in 2014.

The founding team led by Richard Lowenthal had a vision that all people and goods could move around the planet on electricity. This ambitious vision required building the necessary infrastructure from the ground. So the team set out to create the first alternative fueling network that would be built around where drivers park, whether at home, around town, or on the road.

Pasquale Romano recalls in one of the earnings calls: "So it led us to the conclusion that this was going to be a parking model, not a pumping model unless you were driving beyond your battery range. We sell to [anyone] who has a parking lot."

After two years of development, by 2009, the company started to offer electric vehicle charging stations to municipalities, utilities, and private companies. These stations were run on a secure, networked system developed and operated by ChargePoint. What made the company stand out right away is it did not own any charging stations; instead, it focused on networking.

"We're a networking company, and our management comes from networking companies like Cisco, Lucent Technologies, and 3Com. We're all about convergent networking, smart grid, and vehicles. We have put in place a payment system. We determined pretty early that utilities didn't want the extra load on the grid, so, from the beginning, we integrated networking and a smart grid. We monitor all the stations from our operations center to make sure they are working and send someone out to fix it as soon as there is a problem." – said Richard Lowenthal, the founder and then CEO of ChargePoint, in one of his interviews back in 2009.

When Pasquale Romano joined the company in 2011, after selling 2Wire, a company he co-founded, for $475 million, there was barely any electric vehicle market, let alone the market for EV charging. That year, global PEV (plugin-in electric vehicles) sales were just 50,000 units, and EVs made up only 0.02% of the total passenger car stock.

It explains why the company initially had trouble accessing any serious capital despite raising almost $33 million (peanuts for such an ambitious goal) in three rounds by 2011. Investors were hard to get around the company with no established market. But Romano brought something special: he had absolute confidence in ChargePoint. He knew that the EV charging market would be huge eventually, worth tens of billions of dollars, and as the company with the first mover advantage, it would benefit immensely. So he laser-focused on pursuing the right connections in the industry.

A significant breakthrough came a year later when the company attracted the attention of big players in the automotive industry. BMW's i Ventures, alongside Toyota Tsusho, Kleiner Perkins, and a few other investors, invested $47.5 million to help the company grow its operations, further extend the ChargePoint Network, and expand the deployment of its next-generation cloud-based charging solutions for electric vehicles.

That was the beginning of a series of investments that landed the company around $1 billion in total funding. Over the years, with available capital, ChargePoint built one of the largest charging networks in the world with a complete product portfolio of solutions for nearly every segment of EV charging: commercial, fleet, and residential.

But even that amount of capital was insufficient for scaling the network further to meet the demand of a rapidly increasing number of new EV models and rising EV penetration in general. In late 2020, ChargePoint announced a merger with a special purpose company (SPAC), Switchback Energy, to become a publicly traded company.

"For thirteen years, we have been singularly focused on our vision to move all people and goods on electricity, and that has never been more relevant than it is today. We've pioneered networked charging and are resolute in our aim to usher in the transition to mass EV adoption by electrifying one parking spot at a time. Today, we are a charging market leader thanks to a winning business model, a complete portfolio, and thousands of brands that have realized that EV charging is essential, good for business, and aligned with their corporate and sustainability goals. Our technology charges all EVs – from passenger vehicles to delivery fleets – so there is no need to choose winners in electric mobility. We see ourselves as an index for the entire category." – said Pasquale Romano, President and CEO at ChargePoint, at the merger announcement.

On March 1, 2021, ChargePoint became the first publicly traded EV charging network, raising approximately $480 million in net proceeds and valuing the company at around $2.4 billion. On the first day of trading, the company closed at $26.13 (+160% from the NAV price of $10.00).

ChargePoint has overseen real growth since 2018: from $62 million to $241 million in 2021. But the company continues to lose money (and the losses are increasing) as it invests heavily in building out its network and introducing new, advanced charging stations. These investments should start paying off in the next three to five years when ChargePoint will become a dominant player in this space and grab a significant share of the total opportunity worth tens if not hundreds of billions by that time.

Opportunity

By now, every major automaker, from a manufacturer of passenger cars to trucks of all sizes and even buses, has committed to electrification. Some call it the biggest race since the invention of the first car with the combustion engine.

Indeed, electrification of mobility is happening at incredible rates. Despite various obstacles, from the COVID-19 pandemic and shift to the work-from-home environment to global supply chain problems, electric car sales keep rising, setting up new records almost every quarter.

According to Global Electric Vehicle Outlook, EV sales doubled in 2021 from the previous year to a new record of 6.6 million. In 2021, the number of vehicles sold in just one week was the same as the total number of all electric cars sold in the entire of 2012. In 2021, 10% of global car sales were EVs, 4x the market share pre-pandemic (2019), and, according to Bloomberg New Energy Finance Electric Vehicle Outlook, almost 50% of all new vehicles sold in the US and Europe by 2030 would be EVs. Today, more than 16 million electric vehicles are on the roads worldwide, and this number keeps growing exponentially. Only in Q1 2022, 2 additional million were sold, up 75% from the same period in 2021. And this is at times when inflation is at several decade highs, and supply chain problems are nowhere near the point of inflection.

There are a number of reasons why EV sales are on the rise. First and foremost, there is an increasing number of various federal, state, and utility programs across the board that offer subsidies and incentives for EVs. Public spending on them almost doubled in 2021 to nearly $30 billion. Because more and more countries have pledged to reduce or eliminate combustion engine vehicles by a certain year (though many of them are already falling behind the initial projections to reach net zero CO2 emissions by 2050), their respective governments do everything possible to incentivize EV purchasing. Luckily for them, there is a large number of EVs available today: from the cheapest option, Dacia Spring Electric ($22,000), to Lucid Air, which starts from $150,000. In addition, with growing gas prices everywhere due to the Russia-Ukraine conflict and rising oil prices as a consequence, it seems that more and more drivers are selecting EVs as their next cars.

But while EV sales are forecasted to grow for all sorts of reasons, much more must be done to support charging infrastructure. According to Global Electric Vehicle Outlook, the global market value of EV charging is projected to grow 20x by 2030 and reach a whopping $190 billion, with a further increase to over $300 billion by 2040.

Yet, the amount of public charging infrastructure initiatives is lacking behind considerably to power the size of the EV market that is expected at least by 2030. Only to meet the levels of pledged numbers, the number of public chargers must increase by a minimum of ninefold.

As a result, governments all over the world try to actively incentivize infrastructure building to support the needed growth in EV charging stations. For example, in the US, under the National Electric Vehicle Infrastructure Program (NEVI), ChargePoint has just completed the first of six highway corridors in Colorado to enable long-distance EV travel across this state.

Here is what Pasquale Romano said about this program on the recent earnings call: "This is a tremendous opportunity to accelerate the build out of charging along highways in our communities in a way that delights drivers and the businesses that want to serve them. As we have commented on previously, this new stimulus [under NEVI program] should begin to manifest in the calendar year 2023, rolling for five years."

Such programs are being formed all around the world, and we should expect to see them coming in the next few years. A company like ChargePoint will greatly benefit because of these programs, which will further help expand its network.

Since most EVs will be charged at the parking lots, governments must also incentivize and facilitate the installation of home chargers in existing parking spaces. We should also see more mandates for EV charging in the new buildings and local communities.

All trends are pointing out the continuous growth of ChargePoint for many years to come. Just to illustrate how massive this opportunity for ChargePoint is: the company made $241 million in 2021, just 2.5% of the total opportunity as of 2021.

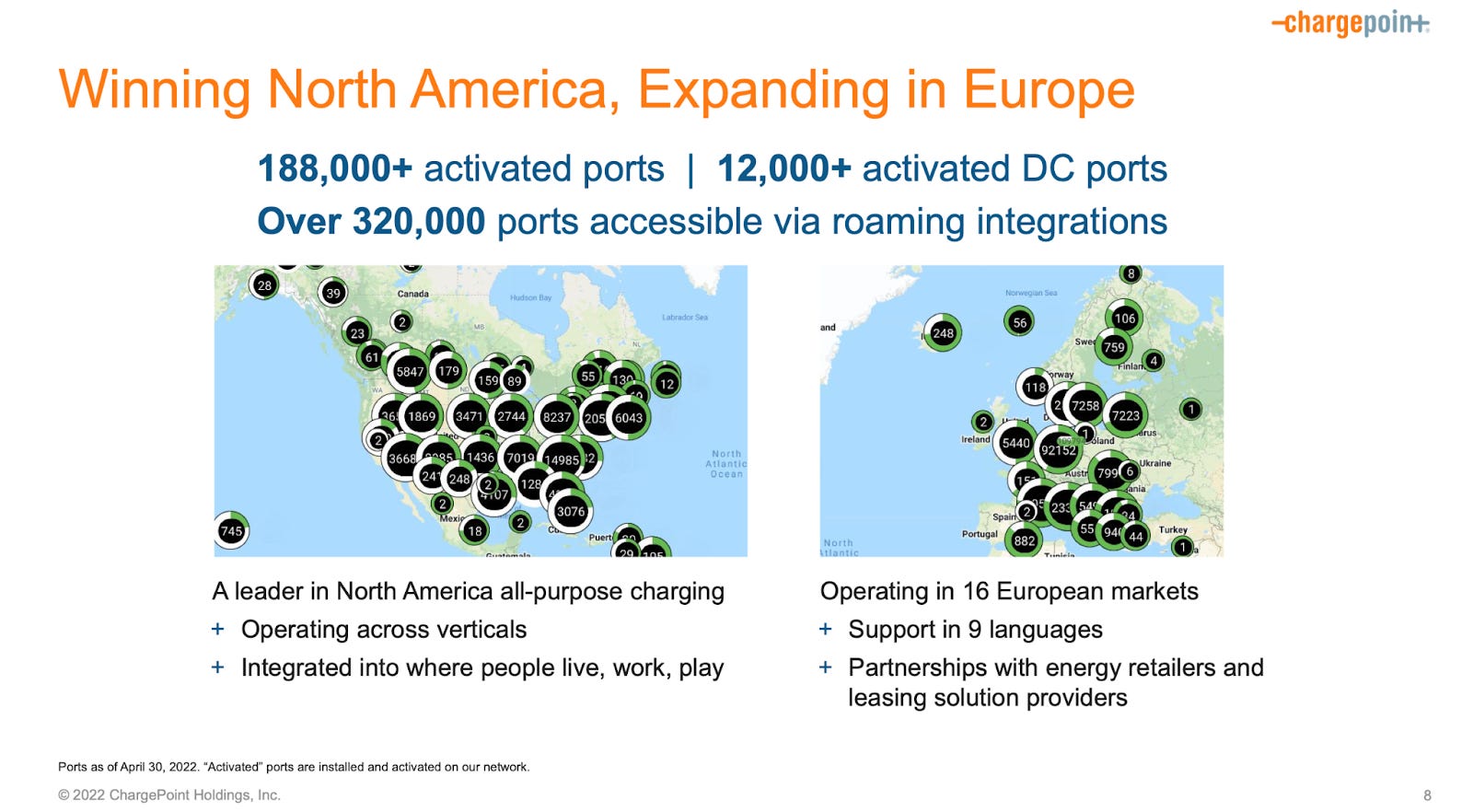

To grab the market share of this fast-growing market, the company tackles a number of areas. To begin with, management believes that drivers will typically charge their EVs overnight at home or during the day at work, in some cases while parked at a shopping center for a few hours – all with Level 2 AC charging. As of Q1 2022, ChargePoint already had approximately 70% market share (7x more market share than the closest competitor) in publicly available networked Level 2 AC charging in North America with over 200,000 activated ports. While there is still a lot of growth in the US and Canada, the biggest opportunity comes from the EU.

ChargePoint began European operations in late 2017 and currently operates in 16 European countries. In the latest quarter, the company reported that 20% of total revenue came from the EU, representing great progress in Europe. ChargePoint delivered $16 million in revenue in the first quarter of 2022, showing 353% year-on-year and 67% sequential growth.

But an even more significant growth is expected in the fleet market in all countries. As fleets are increasing the number of EVs in their car park, more and more fleet companies are turning to ChargePoint. For fleets, it's all about improving their economics. At some point, most fleets will be 100% electric.

ChargePoint also has some early signs of optionality that could eventually open up more revenue streams and increase an overall opportunity: the company generates a lot of data about drivers and how they move. This data might become increasingly valuable at some point to various stakeholders: from governments to utility providers.

To achieve this ambitious growth plan, ChargePoint must continuously invest in the development of charging stations and cloud solutions that are needed to support them. Innovation here is the key.

Technology

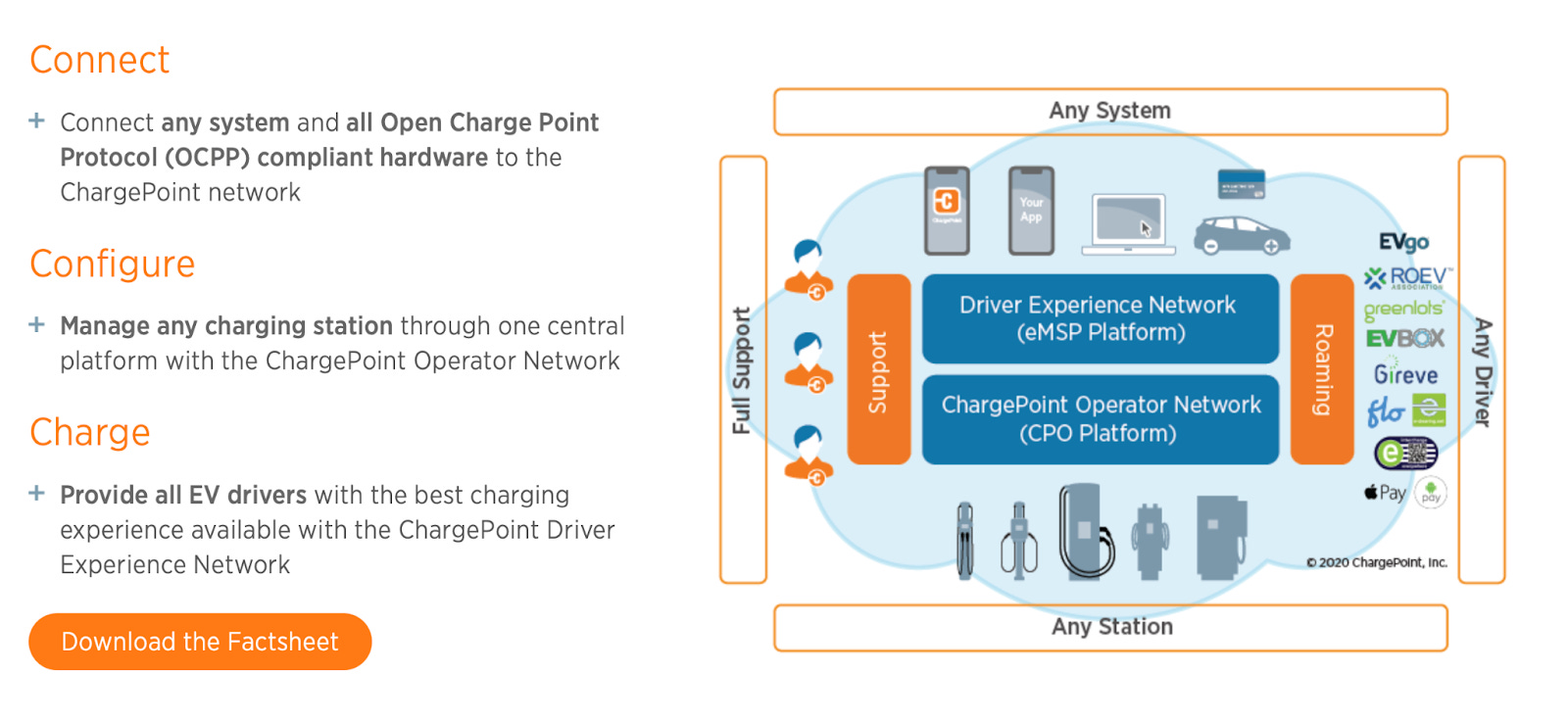

At the core of ChargePoint is its network. It is the world's most open, secure, and robust EV charging network, available in all markets where the company operates.

The openness of this network is what makes ChargePoint unique (unlike Tesla's network, for example): any charging station can be used by any driver and accessed through any system.

Everything else that the company offers is built on top of this network.

Networked Charging Stations

ChargePoint offers two types of charging stations, both designed using cutting-edge hardware technology, which is safe and reliable and that provides drivers with a user-friendly, premium charging experience.

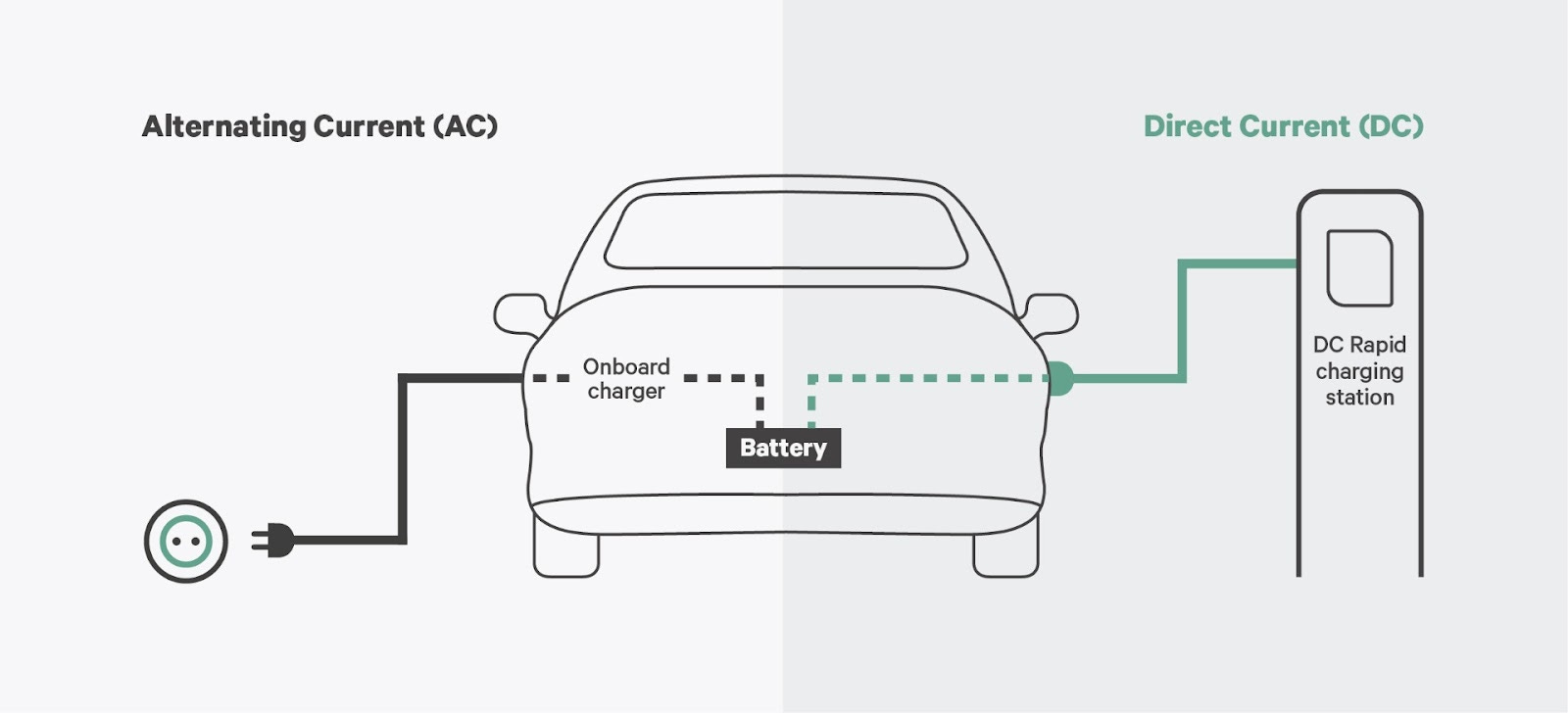

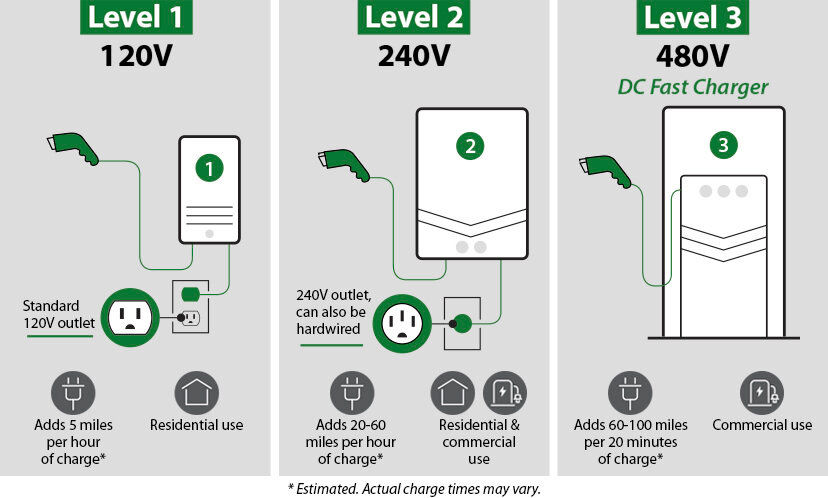

By nature, there are two ways to 'fuel' an electric vehicle: the first is with Level 2 alternating current (AC) power, and the second is with Level 3 direct current (DC) power.

AC power comes from the grid (home or office sockets), while DC power is stored in the batteries inside the EV. Most electronic devices convert the AC power coming from the grid into DC power for their batteries through a converter built into the plug.

The exact mechanism works for electric vehicles: EVs have built-in converters inside, called an onboard charger. This is the most common way to charge an EV.

A DC charger, in contrast, has the converter inside the charger itself. It means that the power can travel from the DC charger to the car's battery without the need to convert it with the onboard charger. DC chargers are usually bigger, more powerful, and can deliver faster charging. They are typically located near highways or at public charging stations to allow a quick charge.

A typical Level 2 AC charger takes 5-6 hours to charge an average battery in the EV, while a Level 3 DC charger takes only 20-30 minutes.

ChargePoint AC stations (Level 2) offer reliable, all-purpose charging for workplaces, multi-family residences, and fleet depots. These solutions allow businesses and property owners to create a new revenue stream while providing a critical service for EV drivers.

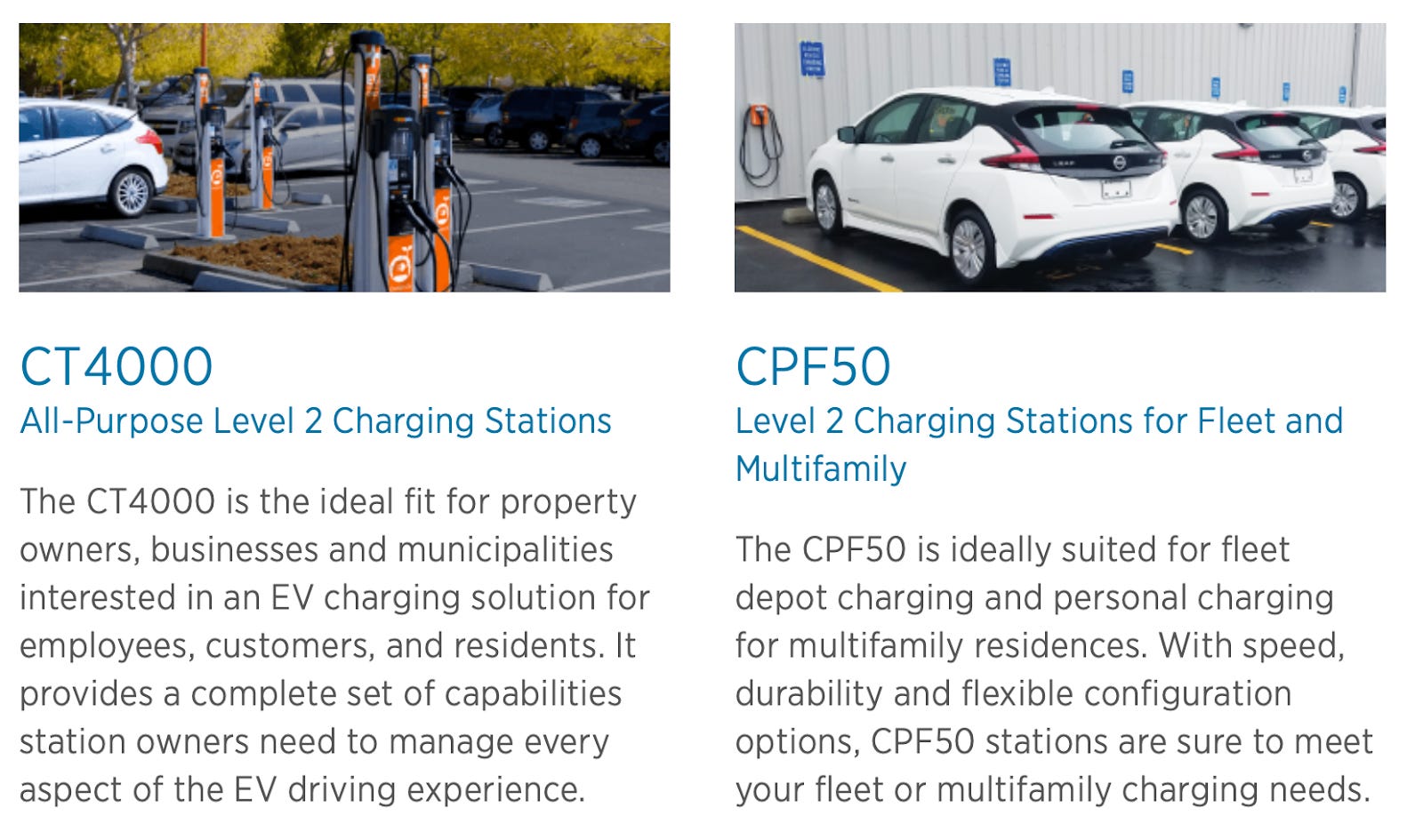

ChargePoint offers two AC stations:

CT4000 (ideal fit for property owners, businesses, and municipalities interested in an EV charging solution for employees, customers, and residents);

CPF50 (ideally suited for fleet depot charging and personal charging for multi-family residences).

ChargePoint DC stations (Level 3) provide high-power charging for commercial and industrial settings. These solutions let property owners, businesses, and government organizations offer fast charging where time to charge is limited (freeway corridors and retail and hospitality locations).

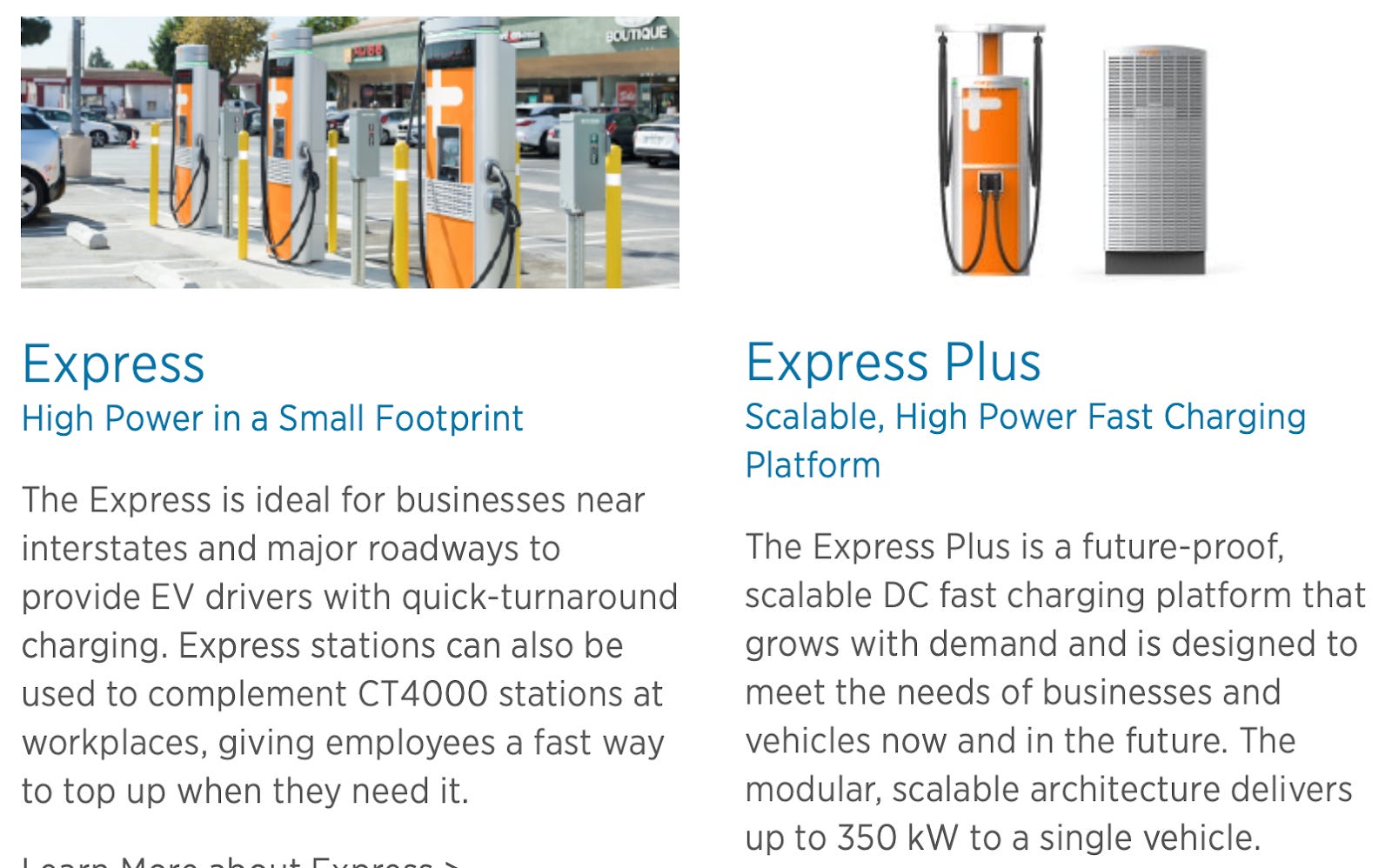

ChargePoint offers two DC stations:

Express (ideal for businesses near interstates and major roadways to provide EV drivers with quick-turnaround charging);

Express Plus (a scalable DC fast charging platform that grows with demand and is designed to meet the needs of businesses and vehicles now and in the future).

ChargePoint's charging solutions can charge most types of EVs, from cars and trucks to delivery vehicles and buses – regardless of the manufacturer. Furthermore, ChargePoint introduced smart cables in all of its new products, allowing it to change connector types dynamically. "[...] has future-proofed us against evolving interface types. So the ability to mix and match connector types on DC and AC is really, I think, benchmark-setting." – said Pasquale Romano, President, and CEO at ChargePoint, on the Q1 2022 earnings call.

The company designs its products in-house and outsources production to several contract manufacturers based in the United States, Mexico, and Europe. Most of the hardware products are manufactured in Mexico.

The company sources various components for the charging stations from a number of global suppliers, most of which are located in Asia. The company also deploys a global supply chain management team that works proactively with these suppliers and coordinates deliveries to distribution hubs that ChargePoint manages in North America and Europe.

Software

The company does not sell charging stations without a subscription to its Cloud Services, which provides access to ChargePoint Network via a unified EV charging management software.

This software enables commercial and fleet customers to manage charging in their parking lots and depots. It comes with a myriad of features, including real-time visibility (insights into driver details, power use, energy costs, driver revenue, and station status), control (price setting based on driver type, session length, energy cost, and time of use), and reporting (insights into station usage, session fees, utility costs, station health, environmental impact and more).

There are some additional features specific to types of customers. For example, fleets can integrate with route planning systems, enabling on-budget deadline scheduling in accordance with energy rate structures and on-site energy storage. It is designed to further integrate with fuel management systems, fleet operations software, and vehicle telematics to enable seamless integration into fleet processes.

Mobile App

ChargePoint offers a free mobile app for all drivers to find stations where they can charge when needed. It requires one account to get access to the entire ChargePoint network and any third-party stations from other supported third-party networks. ChargePoint's network has roaming integrations with more than 350,000 additional ports in North America and Europe.

The app allows drivers to find charging locations, check availability, start sessions, pay for charging, use a ChargePoint account to roam across third-party networks, access preferential pricing and loyalty offers, and track the estimated avoidance of CO2 emissions in comparison to the use of liquid fuel.

Integrations

Ecosystem integrations enable drivers to access charging functionality via in-vehicle infotainment systems, consumer mobile applications, payment systems, mapping tools, home automation assistants, fleet fuel cards, wearables, and residential utility programs.

Business Model

ChargePoint generates revenue from selling hardware (charging stations), software (Cloud Services), and services (extended parts and labor warranty).

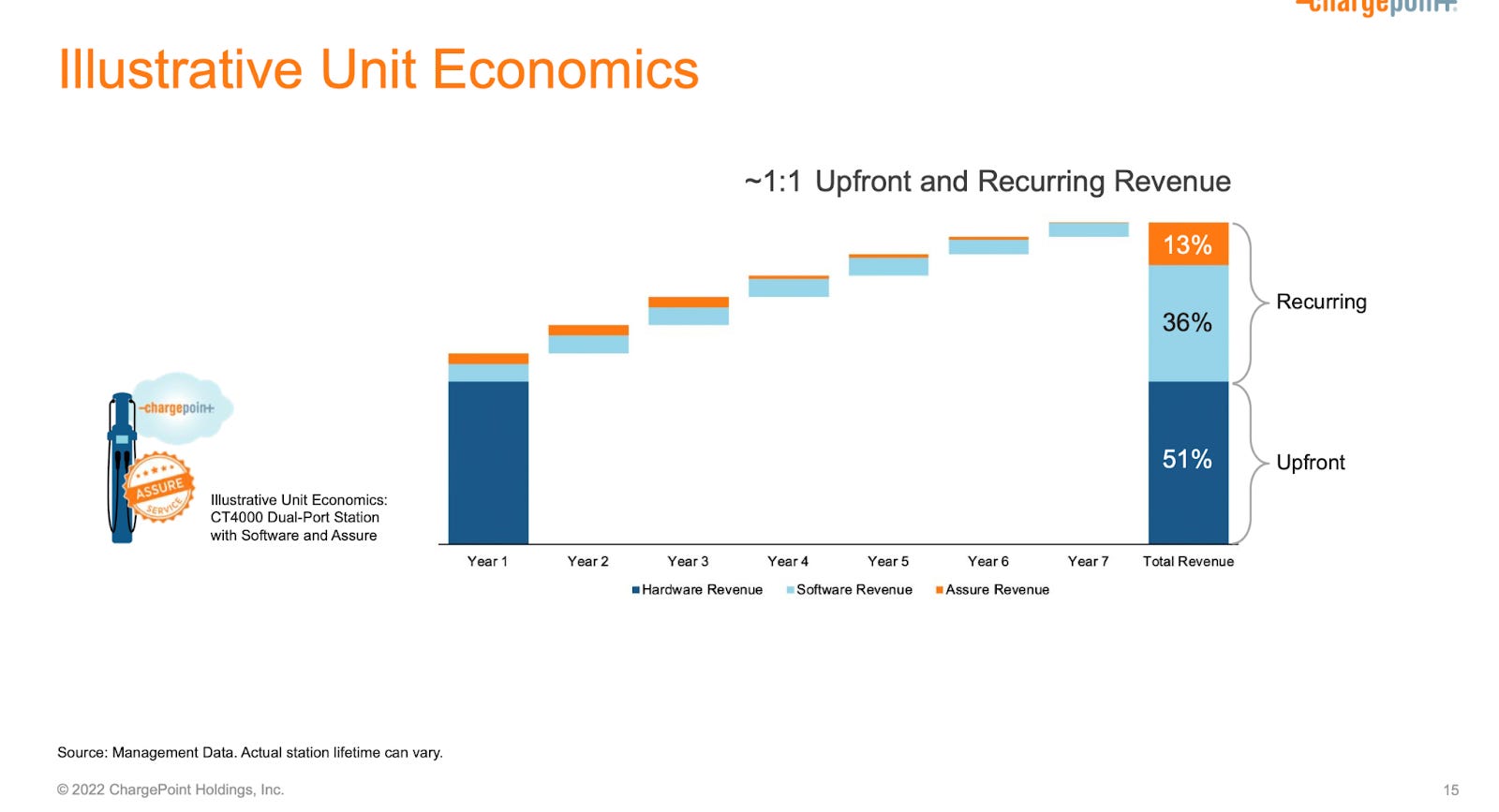

Hardware sales are one-off purchases from residential, commercial, and fleet customers for ChargePoint's Level 2 AC and Level 3 DC products. As of Q1 2022, the majority of revenue comes from the sale of Level 2 AC products. The company generally recognizes revenue from sales of hardware products upon shipment to the customer. Hardware products bear a low gross margin (in the mid-20s) due to the high cost of revenue, which includes contract manufacturer costs, parts, salaries and related personnel expenses (including stock-based compensation), allocated facilities and information technology expenses, as well as warranty costs (comes with all hardware products).

Every hardware product requires a subscription to Cloud Services. The subscription is charged annually and recognized ratably during the contract period. The software subscription is high-margin and recurring, with a typical usage period of a minimum of 7 years. This provides strong financial visibility with predicted revenue.

Separately, the company offers extended maintenance service plans (under Assure name) that include parts and labor warranty. This also comes as an annual subscription, provided in various capacities depending on the type of customer.

Subscriptions revenue also consists of CPaaS (ChargePoint-as-a-Service) revenue which combines the customer's use of ChargePoint's owned and operated systems with Cloud Services and Assure into a single subscription. However, historically revenue from CPaaS has not been material.

The company is trying not to own charging stations and operate an asset-light business model. It also does not profit from electricity or driver access to stations. "We don't own meters. We don't sell energy. So our customers can do whatever they want with the power. They can use it as an amenity. They can use it as a revenue kicker. They can do whatever the hell they want with it. We don't care." – Pasquale Romano, President and CEO at ChargePoint.

This business model does not require heavy CapEx and allows the company to scale faster and more efficiently, basically crowdsourcing the growth of charging stations across the world. What ChargePoint focuses on is product development and innovation, awareness and customer acquisition, as well as lobbying public policy to drive the adoption of EVs.

Additionally, the company derives revenue from fees received for transferring regulatory credits earned for participating in low carbon fuel programs in approved states, charging related fees received from drivers using charging sites owned and operated by ChargePoint, net transaction fees earned for processing payments collected on driver charging sessions at charging sites owned by its customers, and other professional services. These additional revenues have constantly been decreasing over the past few years, from 10% of total revenue in fiscal 2020 to 5.7% in fiscal 2022, due to a continued decrease in regulatory credits transferred.

For the three months ended in July 2022 (Q2 2023), revenue from selling networked charging systems was 78% of total revenue, while subscriptions accounted for 19%. The company experiences a higher demand from customers in the three verticals, resulting in higher volumes of systems delivered across ChargePoint's major product families.

Over the long term, the company expects that software revenue from subscriptions will account for a minimum of 50% of total revenue, which will improve the gross margin. For now, the company is selling hardware for almost a loss to lock in customers for long-term, high-margin subscriptions that will propel the company to profitability.

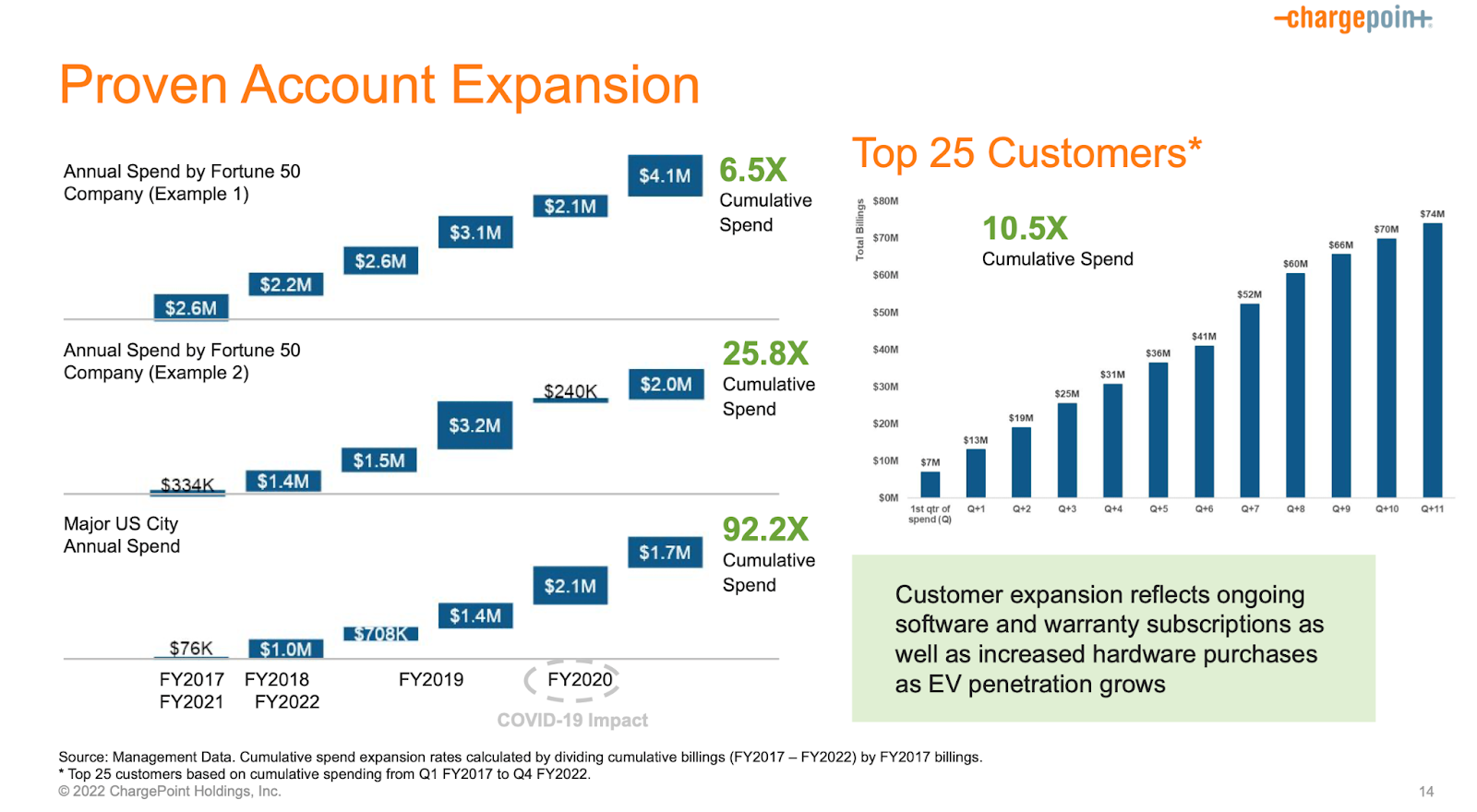

ChargePoint uses a land-and-expand model to drive revenues. Customer expansion reflects ongoing software and warranty subscriptions as well as increased hardware purchases as EV penetration grows. For example, the top 25 customers spent 10.5x cumulative spend, while one particular customer, a Fortune 50 company, spent a whopping 25.8x.

"On the land side, we added over 1,000 new customers this quarter with new customer billings at approximately 30% for the period. Because the orders from new customers initiate a revenue stream that grows consistently into the future, we anticipate most of the revenue generated over the life of customers added this quarter would occur in a future environment in which supply chain conditions will have returned to normalcy, hence the decision to accept the lower margin for the quarter to support the acquisition of new customers and the expansion from the installed base. Supporting the strategy, consistent expansion with existing customers was over 65% of our billings for the quarter." – from Q1 2023 earnings call.

Customers

ChargePoint sells its products and services to three types of customers: commercial, fleet, and residential.

Commercial customers include retail centers, offices, medical complexes, schools, airports, convenience stores, recreation centers, fast fueling sites, and others. These businesses usually own or lease parking.

"ChargePoint believes commercial businesses view charging as essential and invest to attract tenants, employees, customers and visitors, generate direct and indirect income, and achieve sustainability goals." – from the company's 10-K.

The company acquires commercial customers via brand awareness, education, and demand marketing programs through its direct sales force and channel partners.

Fleet customers are organizations that operate vehicle fleets in delivery/logistics, sales/service/motor pool shared transit, and ride-sharing service operators.

"ChargePoint believes these customers choose to electrify their fleets for economic reasons, as the comparative total cost of ownership in favor of electrification." – from the company's 10-K.

The company attracts fleet customers via its direct sales force and a curated set of channel partners that work with fleets.

ChargePoint also offers residential EV charging solutions for owners of EVs living in single-family residences who want the convenience of fueling at home with the ability to optimize energy costs and full integration with the same mobile app they use to charge the vehicle away from home.

The company drives single-family residential sales through direct marketing to the consumer. It also offers landlords and owner associations the ability to provide charging billed directly to the tenant for apartments and condominium settings.

"We are in the early stages of adding recurring revenue for single-family residents, in addition to existing recurring revenue in multi-family." – from Q1 2023 earnings call.

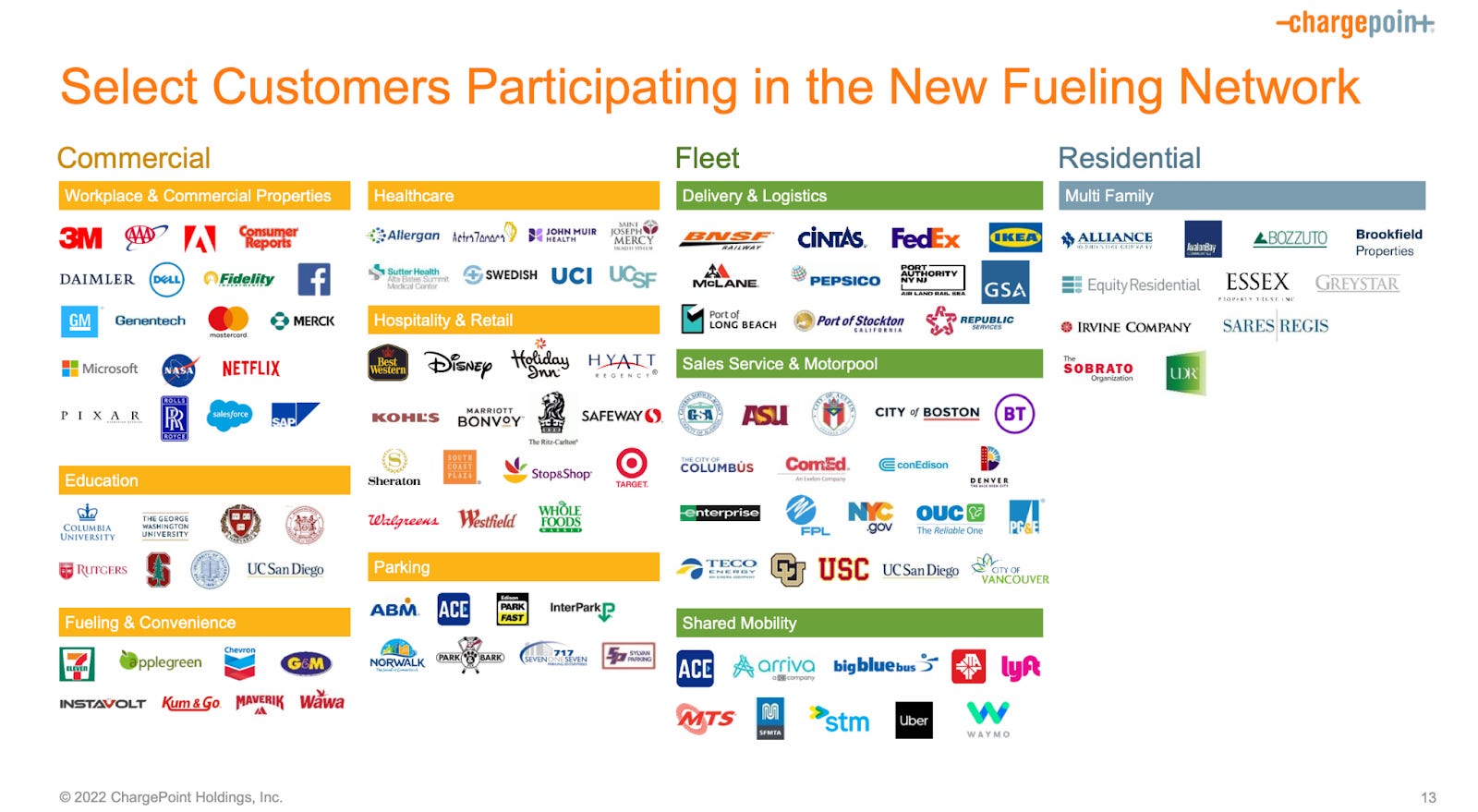

In total, the company has over 5,000 customers (though it does not officially report the exact number) worldwide. However, it states that 80% (up from 76% in Q1 2023) of the 2021 Fortune 50 companies and 53% (up from 52% in Q1 2023) of the Fortune 500 companies are the company's customers.

Among customers are well-known companies and organizations in industries like workplace and commercial properties (3M, Adobe, Facebook, Microsoft, Salesforce, Netflix), education (Colombia University, Harward, Stanford, UC San Diego), fueling and convenience (7eleven, applegreen, Chevron, Maverick), hospitality and retail (Disney, Holiday Inn, Marriott, Target, Whole Foods), delivery and logistics (FedEx, IKEA, Pepsico), shared mobility (Uber, Lyft), and multi-family (Brookfield Properties, Alliance Residential).

Most customers today come from North America, but many of those are present in Europe and actively expanding there, which is reflected in triple-digit growth in revenue from the EU market.

The company does not report churn rates, but these types of businesses usually have a high customer net retention rate as they enjoy the high switching costs and long-term relationships with customers once they install the charging stations.

“Once they're on ChargePoint, as long as we take good care of them and treat them well and give them good value, they'll stay on ChargePoint and continue to expand.” – from Q1 2023 earnings call.

No customer individually represented 10% or more of both the company's accounts receivable and total revenue.

Competitive Advantages

The EV charging market is relatively new and evolving at a very rapid pace. ChargePoint primarily competes with various smaller providers of EV charging stations, especially in Europe, where this market is in its early stage of development and highly fragmented, with many companies providing hardware or software only and few providing both.

In North America, the situation with the competition is slightly different, as the market is more mature. ChargePoint believes its primary competitors include other OEMs, manufacturers, and providers of EV charging station solutions, such as Blink Charging and SemaConnect (in Level 2 AC chargers), Wallbox and Blink Charging (in Level 1 AC chargers), and ABB and Tritium DCFC (in Level 3 DC chargers).

The biggest threat for ChargePoint is not in the charging stations business but in the charging networks. While most smaller companies won't be able to build a similar network to ChargePoint, and we will most likely see a lot of consolidation in the space from bigger players, some of these large players are already building their own networks that could significantly reduce the overall demand for EV charging at other sites.

For example, Tesla is rapidly expanding its charging network worldwide and already has 33,300 charging points. Some oil giants are also entering the space, with BP acquiring one company after another in pursuit of building its charging network (BP Pulse) that now has more than 8,000 charging ports or Shell with its recharge solutions rapidly scaling in the US.

So the competition boils down to building the largest and most reliable charging network, not creating the best charging stations. The charging station is essentially a commodity, and there will always be many substitutes. It will end up being just a pricing game.

ChargePoint was the first one to begin building out the EV charging network and therefore possesses a first mover advantage. Today, it has the largest network in North America, with over 200,000 activated ports worldwide, of which 15,000 are DC ports. But there is more: in addition to its own network, ChargePoint users can now access over 355,000 additional ports (up from 320,000 in Q1 2023) in North America and Europe, bringing the total number of ports accessible to over 550,000. No competitor will be able to match this, possibly ever. And the further the overall infrastructure evolves, the more extensive this network will become.

"First company to get scale has a massive, massive effect and also long-term gross margin advantage just because of the scale." – Pasquale Romano, President and CEO at ChargePoint.

ChargePoint has also created strong network effects that strengthen its value further and distance from competitors. The more EV penetration increases, the more ports site hosts will need, and these hosts usually prefer to scale with the same provider that most drivers choose. In turn, most drivers prefer a network with the most available ports and one which is easy to find (ChargePoint has the top-rated app to find and access charging). This triggers more distribution partners to join, helping to further expand and enhance the ChargePoint network.

Another advantage that ChargePoint possesses is its operational model, under which it does not own any charging stations, unlike most other charging station providers. The company could scale its network more cost-efficiently and much faster.

Finally, while most competitors focus on commercial customers and fleets, ChargePoint has solutions for all types of customers. And these solutions provide everything that any customer needs. "We're in a position to be one-stop shopping, dimensionally across all those sub-verticals. You don't have to go to a bunch of different solution providers to solve your needs for, say, the last mile versus a take-home fleet. It's all integrated into one software platform." – Pasquale Romano, President and CEO at ChargePoint.

Management

ChargePoint has been an executive-led company for over a decade. None of the founders of ChargePoint are with the company anymore.

With the arrival of Pasquale Romano, the current CEO, the company has grown from just a hundred ports in several states in the US to the largest EV charging network in the world, with more than 200,000 ports. It is Romano's belief in the company and his risk-taking abilities that brought ChargePoint this far.

Romano is highly rated by its employees, with a 92% CEO approval rating on Glassdoor based on 106 ratings. Most reviews on Glassdoor mention the strong leadership team.

Alongside Romano, perhaps one of the most experienced leaders in the EV charging space, is indeed a pretty strong team of other executives, many of whom have been with the company for several years.

Some notable members of the leadership team:

Pasquale Romano has served as President, Chief Executive Officer, and a member of the board of directors of ChargePoint since February 2011. Prior to ChargePoint, Mr. Romano co-founded 2Wire, a provider of broadband service delivery platforms, where he served as its President and Chief Executive Officer from October 2006 until July 2010, when it was acquired by Pace. Previously, Pasquale held multiple positions in marketing and engineering at Polycom. In 1989, he co-founded Fluent, a digital video networking company, and served as its Chief Architect until the company was sold to Novell Corporation in 1993. He holds an AB in Computer Science from Harvard University and an MS from the Massachusetts Institute of Technology (MIT).

Rex Jackson has served as Chief Financial Officer at ChargePoint since May 2018. Prior to ChargePoint, Mr. Jackson served as CFO of Gigamon, a developer of network and security visibility solutions, from October 2016 to April 2018 through its go-private transaction. Prior, Mr. Jackson served as Chief Financial Officer of JDS Uniphase, a provider of network and service enablement solutions and optical products for service providers, cable operators and network equipment manufacturers, from January 2013 to September 2015, where he drove the separation of JDSU into two independent public companies (Lumentum Holdings and Viavi Solutions) in August 2015. Mr. Jackson joined JDSU in January 2011 as Senior Vice President, Business Services, with responsibility for corporate development, legal, corporate marketing, and information technology. Prior to JDSU, Mr. Jackson served as CFO of Symyx Technologies from 2007 to 2010, where he led the company's acquisition of MDL Information Systems and subsequent merger of equals with another public company. Previously, Mr. Jackson also served as acting Chief Financial Officer for Synopsys and General Counsel at Avago, AdForce, and Read-Rite. Mr. Jackson holds a BA from Duke University and a JD from Stanford Law School.

Collen Jansen has served as ChargePoint's Chief Marketing Officer since July 2016. Prior to ChargePoint, she served as Vice President of Marketing at Jive Software, a provider of enterprise collaboration solutions, from April 2014 to September 2015. Prior, Ms. Jansen served as Senior Director of Global Consumer Marketing, among other roles, at LinkedIn, the world's leading professional network, from 2011 to 2014. Previously, she served as Vice President of Marketing at Yahoo, a consumer internet company, as well as in leadership roles in public companies and privately-funded startups focused on software. She holds a BS in Business Administration from California State University, Fresno.

Bill Loewenthal (brother of Richard Loewenthal, the founder of ChargePoint) has been ChargePoint's Chief Product Officer since May 2022. He joined ChargePoint as Senior Vice President, Product in July 2018. Prior to ChargePoint, Mr. Loewenthal served as Vice President of Product Portfolio Management at Avaya, a provider of business communication solutions, from July 2017 until February 2018. Since 2010, Mr. Loewenthal held various roles at audio communications leader Poly (formerly Plantronics). His career includes leadership roles in public and startup companies with an emphasis on hardware and software solutions. He was named a top 20 Global Chief Product Officer in the 2022 Product Awards, produced by Products That Count in partnership with Capgemini and Mighty Capital. Mr. Loewenthal holds a BS from San Jose State University.

ChargePoint has a well-experienced and diversified board of directors comprising 11 people, including Pasquale Romano. It is a pretty extensive board for a public company. All board members are owner-oriented, owning shares of the company.

Some notable members of the board:

Secretary Elaine Chao has served as a member of ChargePoint's board of directors since December 2021. Secretary Chao has been confirmed to two Cabinet positions by the United States Senate on a strong bipartisan basis. She served as both the 24th US Secretary of Labor and the 18th US Secretary of Transportation. Secretary Chao has held many corporate and board of director leadership positions in such organizations as News Corp, Ingersoll Rand, Protective Life, Wells Fargo, and Dole Food Company. Secretary Chao was also President and CEO of United Way America, Director of the Peace Corps, and a banker with Citicorp and Bank of America. She earned her master's in business administration from Harvard Business School after receiving her undergraduate degree in Economics from Mount Holyoke College. Recognized for her extensive record of accomplishments and public service, she is also the recipient of 37 honorary doctorate degrees.

Axel Harries has served as a member of the board of directors for ChargePoint since October 2016. Mr. Harries has been Vice President of Product Management and Sales Mercedes-Benz within the Marketing and Sales Mercedes-Benz Cars Executive Board at Mercedes-Benz AG since July 2017. Additionally, beginning in 2020, he has headed the Product Management and Sales Mercedes-Benz at Mercedes-Benz AG as Vice President of Integrated Program, Sales and Inventory Planning with the Production and Supply Chain Management Executive Board. During his 14-year career with Daimler AG, he has held roles in the Commercial Vehicles, Corporate e-Business, and Off-Road Vehicles divisions of the company. He studied product engineering with finance and management accounting at Furtwangen University in Germany. Mr. Harries has extensive management experience in the automotive industry and knowledge of Europe's electric vehicle charging market.

Richard Wagoner has served as a member of ChargePoint's board of directors since February 2017. From 1977 to 2009, Mr. Wagoner held numerous senior positions at General Motors, including Chairman and Chief Executive Officer from 2003 to 2009. Mr. Wagoner currently serves as a director of Invesco, where he has served since October 2013, and Graham Holdings, where he has served since June 2010. Mr. Wagoner previously served as a director of Aleris Corporation from August 2010 until April 2020. Mr. Wagoner holds a bachelor's degree from Duke University and an MBA from Harvard Business School. Mr. Wagoner has extensive experience in the automobile industry, general management, and public company board service.

Culture

ChargePoint has been built around one simple idea: to facilitate the transition to electric mobility by providing a place to charge wherever people go. The company's mission, Move All People and Goods on Electric Power, fully adheres to this idea.

To achieve this mission, the company has created a unique culture where all employees are driven by making electric mobility an easy choice by making EV charging easier for as many people as possible. The company's internal slogan, "we plugin at work," further describes how the company is obsessed with its mission.

ChargePoint is one of those companies that take ESG to another level. By enabling the global shift to mass EV adoption, the company delivers a significant positive climate impact, helping improve quality of life and reducing the cost of living.

To date, the company enabled 4.4 billion electric miles, avoiding more than 178 million (16 million more in just one quarter) gallons of gas, more than 312 million kgs of CO2, and approximately 462 million kg of GHG emissions. ChargePoint has helped to avoid half a billion dollars in gasoline expenses and save around $400 million in the total cost of ownership.

As a result, ChargePoint has been recognized by many distinguished organizations for its contributions toward a more sustainable future. For example, The United Nations Framework Convention on Climate Change honored ChargePoint with a Momentum for Change award at the annual Conference of Parties (COP21) in Paris, France. ChargePoint received this award for its partnership program with BMW and Volkswagen to create Express Charging Corridors along both coasts of the United States.

For its innovative technology, advanced hardware, and best-in-class software, ChargePoint has earned a number of awards and recognitions from Fast Company, Global Cleantech 100, Frost & Sullivan Award, and others.

Most recently, the company has been recognized by Fast Company as one of The 10 most innovative companies in North America in 2022, for gassing up EV charging infrastructure. "In November 2021, President Biden signed the infrastructure bill, which authorized $7.5 billion to build a nationwide electric-vehicle charging network that would be available in public spaces and not proprietary to a particular vehicle. ChargePoint, which has been building an open EV charging network in North America and Europe since 2007, is best poised to take advantage of this investment." – from the press release.

Headquartered in Campbell, California, United States, with operations in Arizona (US), Europe, and India, the company grew to 1500+ employees. North America accounts for around 70% of all workforce, but the company is quickly expanding to Europe and actively hiring there.

ChargePoint has an average rating on Glassdoor of 3.8 / 5 based on 186 reviews, with a downward trend (the company had a 4.4 rating a year ago).

Financials

All information in this section is based on the financial performance of ChargePoint in its most recent quarter (Q2 of fiscal 2023), reported on August 30, 2022.

Note: the company's fiscal year does not align with the calendar year, and the company's fiscal year ends on January 31. For example, references to fiscal 2022 refer to the fiscal year ended January 31, 2022.

"ChargePoint delivered another strong quarter, with continued growth across all verticals and geographies. We posted Q2 revenue of $108 million, above the high end of the guidance provided on our Q1 call. Notably, Q2 is our first $100 million quarter, another major milestone in the company's 15-year history. As consumers embrace the transition to EVs at an accelerating rate, the future of this business is incredibly strong." – from Q2 2023 earnings notes and a call.

Income Statement

Revenue

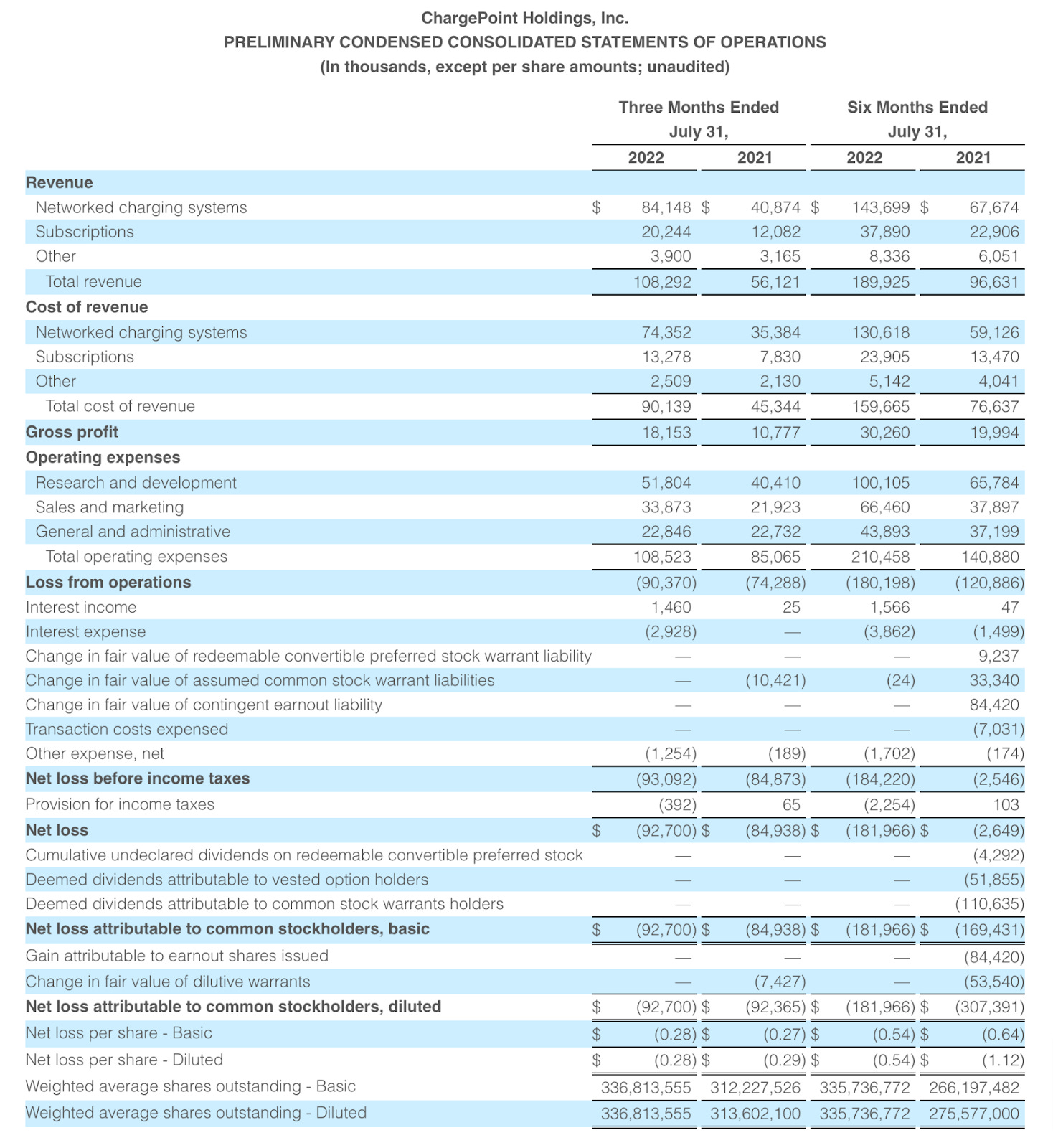

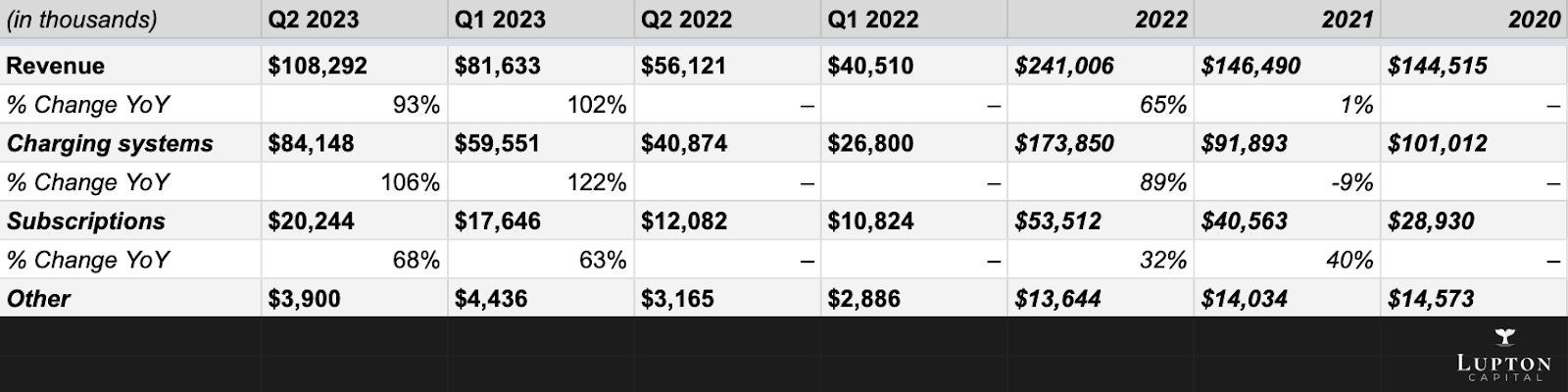

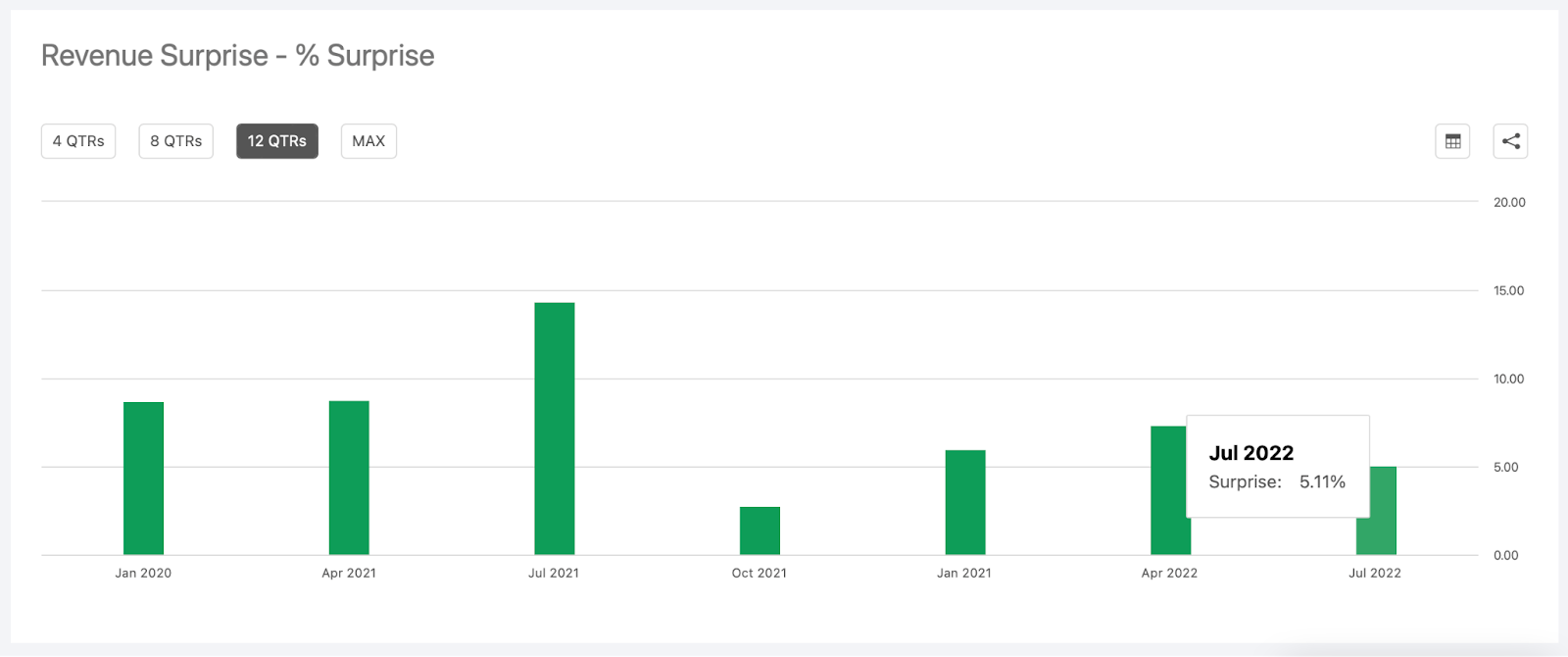

Revenue in Q2 2023 was $108 million, an increase of 93% from $56.1 million in the same quarter a year prior and 33% sequentially.

"Revenue in this quarter was above our previously announced guidance range of $96 million to $106 million." – from Q2 2023 earnings call.

The company has beat the analysts' consensus by $5.26 million (5.11%). Since becoming a public company, ChargePoint has delivered an earnings surprise every quarter.

Network charging systems revenue came at $84 million (or 78% of Q2 revenue), up 106% year-on-year and 41% sequentially. Subscription revenue was $20 million (or 19% of Q2 revenue), up 68% year-on-year and 15% sequentially. Other revenue was $4 million (or 4% of total revenue), increasing 23% year-on-year, down 12% sequentially.

Deferred revenue (future recurring subscription revenue from existing customer commitments and payments) continues to grow, finishing the quarter at $168 million, up from $157 million at the end of Q1 2023.

The revenue split by verticals (types of customers) was the following: commercial – 72% (up from 67% in Q1 2023), fleet – 14% (down from 16% in Q1 2023), residential – 13% (down from 15% in Q1 2023), and other – 1%. Geographically, most of the total revenue (84%) came from the North American market, with the rest from the EU market. Business in Europe is increasing fast. "In the second quarter, Europe delivered $18 million [up from $16 million in Q1 2023] in revenue and grew 254% year-over-year and 11% sequentially." – from Q2 2023 earnings call.

Cost of Revenue

The cost of revenue increased by $44.7 million, or 99%, compared to Q2 2022. It represents 83.2% of total revenue, an increase from 80% in the same quarter last year but a slight decrease from 85% in the first quarter of this year.

Cost of Networked Charging Systems revenue increased primarily due to an increase in the number of Networked Charging Systems delivered, while the cost of subscriptions revenue increased primarily due to increases in customer support headcount and resulting personnel compensation and stock-based compensation increase driven by ChargePoint expanding its network of charging systems.

Gross Margin

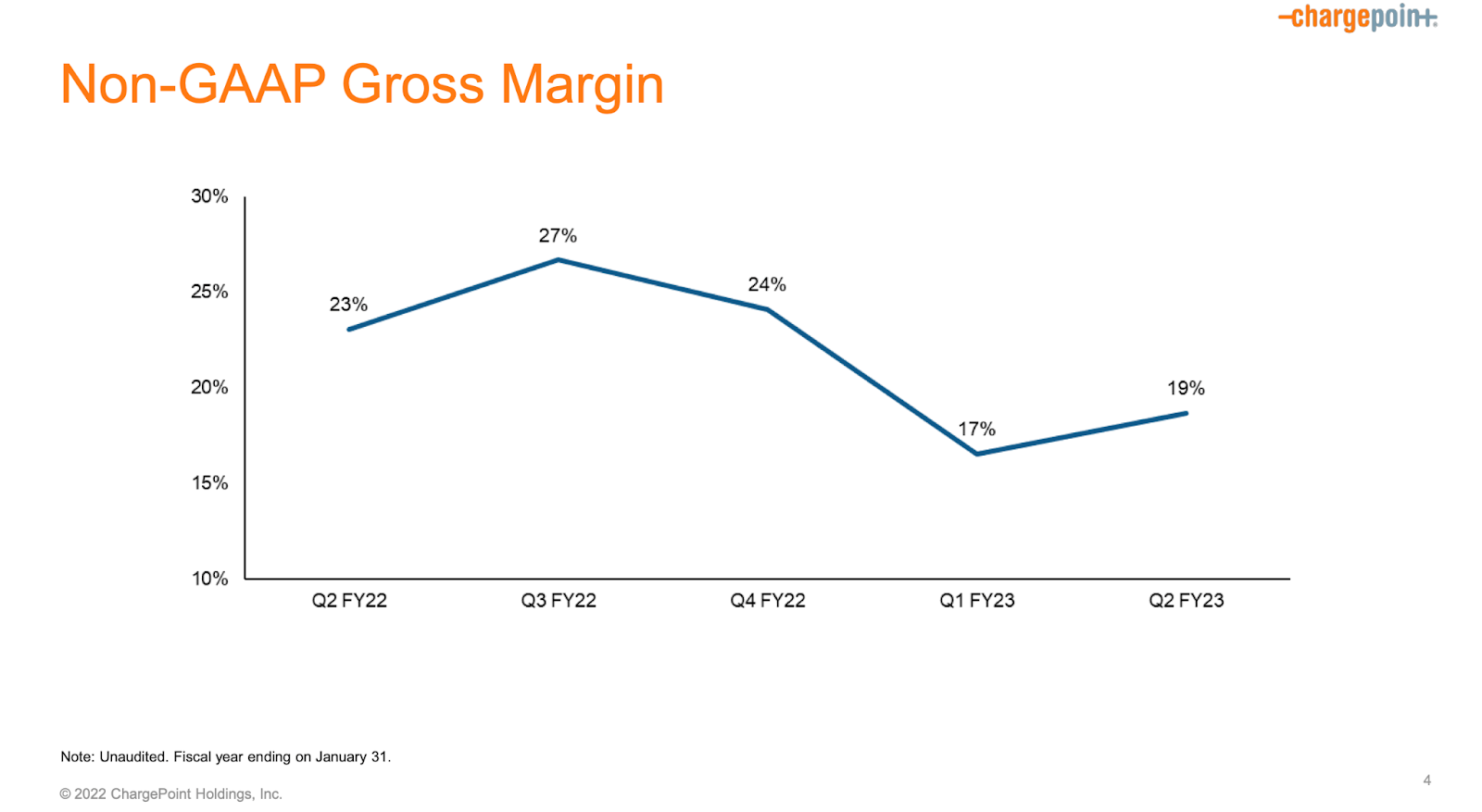

The company reported a non-GAAP gross margin of 19% in the second quarter of fiscal 2023, an improvement from 17% in Q1 2023, which came from $7 million of purchase price variance logistical costs associated with the supply chain.

"We expect continued technology-driven margin improvements for our newer products, lower purchase price variances and improving ASPs to drive recovery in the second half." – from Q2 2023 earnings call.

The GAAP gross margin in Q2 2023 was 16.7%, a decrease from 19.2% in Q2 2022 but an increase from 14.8% in Q1 2023.

The newer, currently lower-margin products performed stronger relative to more mature, higher-margin products due to supply chain disruptions, which affected both cost and supply availability.

The management expected the gross margin to start recovering from Q2 2023 and throughout the rest of the year due to several factors. "First, fewer supplies constraints for mature products. Second, continued technology-driven margin improvements for our newer products; and third, continued efforts to pass on higher component costs. Demand continues to be strong as evidenced by our revenue outperformance, and higher backlog and our price points continue to be well received by the market." – from Q1 2023 earnings call.

The gross profit in this quarter was $18.1 million, $7.4 million more than last year's first quarter and $4 million in Q1 2023.

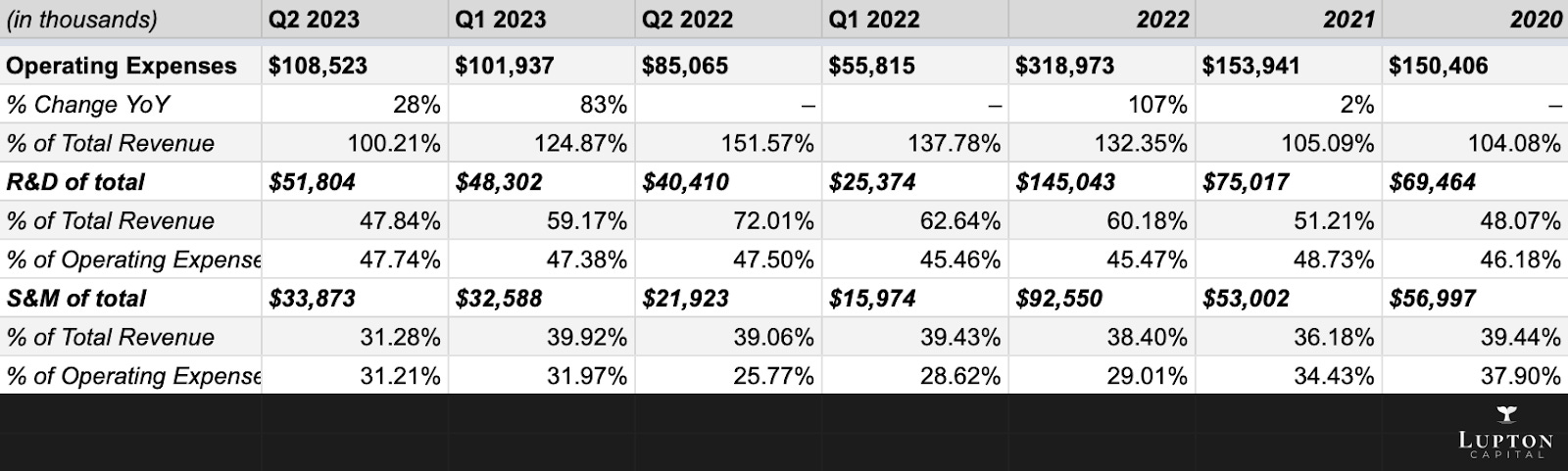

Operating Expenses

Total operating expenses in Q2 2023 were $108.5 million, a 28% increase from $85 million in the second quarter of fiscal 2022.

"70% of our operating expenses are people." – from Q2 2023 earnings call.

It still represents 100% of total revenue, but the company has shown a significant improvement in terms of year-over-year growth. The operating expenses grew only 28% compared to Q1 2022, and they were sequentially essentially flat as the company continues to focus on delivering operating leverage and managing expenses against environmentally driven gross margin challenges.

The company also continues to invest heavily in research and development (specifically in the new fast-charging products), which accounted for almost 50% of total revenue and 50% of total operating expenses.

The management also managed to significantly decrease sales & marketing expenses as a percentage of total revenue and operating expenses. Both numbers are slightly above 30%.

"We expect a particularly strong finish on this metric [operating expenses], which is key to achieving our stated goal of positive free cash by the end of calendar 2024." – from Q2 2023 earnings call.

Profitability

ChargePoint is heavily investing in future growth, with operating losses widening. The company lost $180 million since the beginning of fiscal 2023.

The second quarter GAAP net loss was $92.7 million, which included $26.4 million in stock-based compensation expenses.

The company plans to continue losing money in the foreseeable future to invest in the expansion of its charging network and enhance its charging station products.

No profitability (at least on an Adjusted EBITDA basis) is projected until after 2025.

Guidance

For the third quarter of fiscal 2023, management expects revenue to be in the range between $125 million and $135 million, up 100% year-on-year and up 20% sequentially at the midpoint. The analysts' consensus is $131.5 million.

The management also confirmed its prior revenue guidance for the entire 2023 fiscal year of $450 million to $500 million, representing an anticipated increase of 96% compared to the prior year. An annual non-GAAP gross margin is expected to be in the range of 22% to 26% while operating expenses should come between $350 million to $370 million.

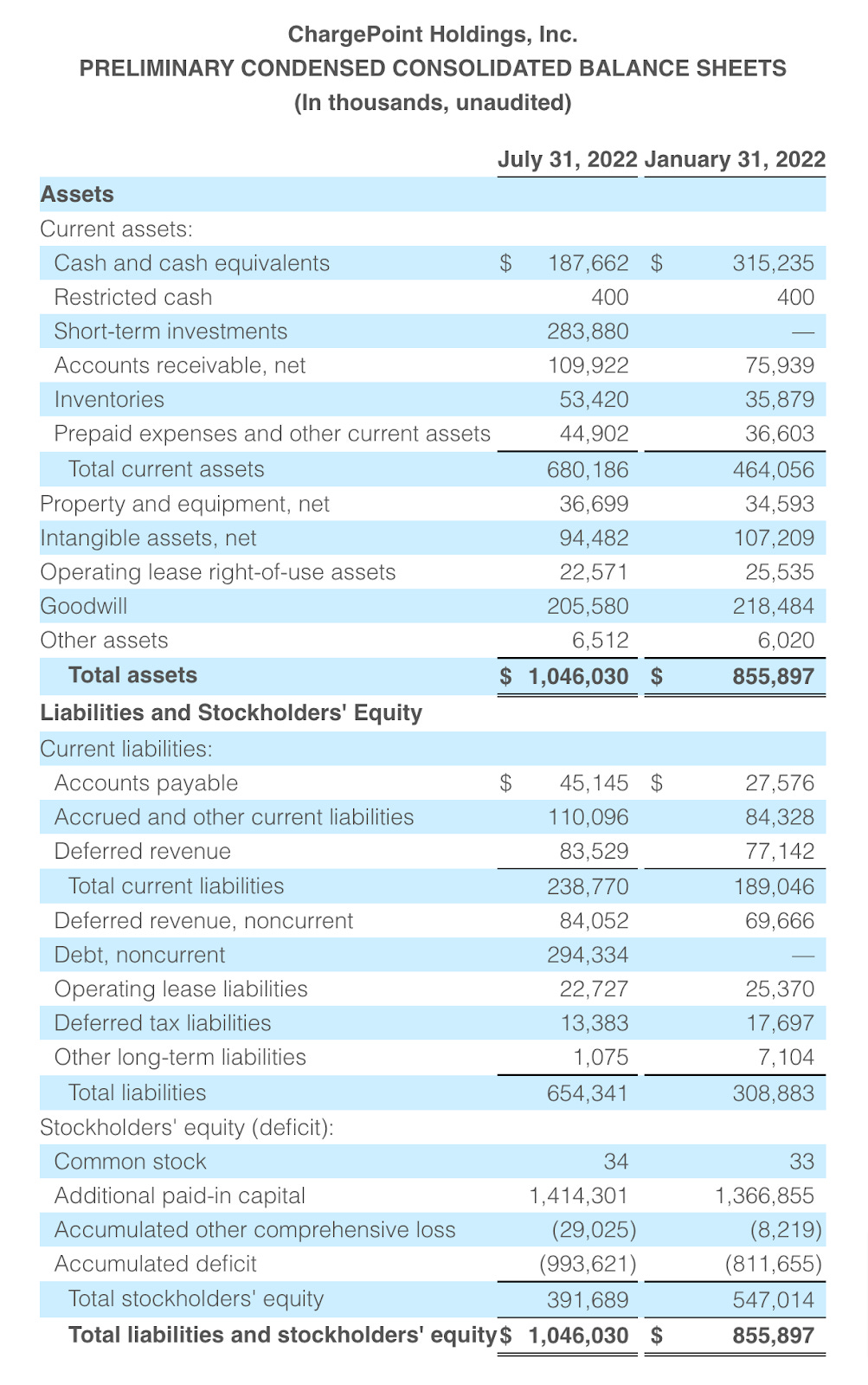

Balance Sheet

ChargePoint ended the first quarter of fiscal 2023 with $472 million (down from $540 million in Q1 2023) in cash and cash equivalents on its balance. Earlier this year, the company closed a $300 million convertible note offering through 2027. The Notes will be convertible at an initial conversion price of $24.03 per share.

The stock-based compensation (SBC) was $26.4 million, a slight decrease from the quarter a year ago but almost a double from Q1 2023. SBC grew to a 24.4% level of total revenue, which is considered overly high.

Since going public in early 2021, the company increased the number of shares outstanding by over 21%.

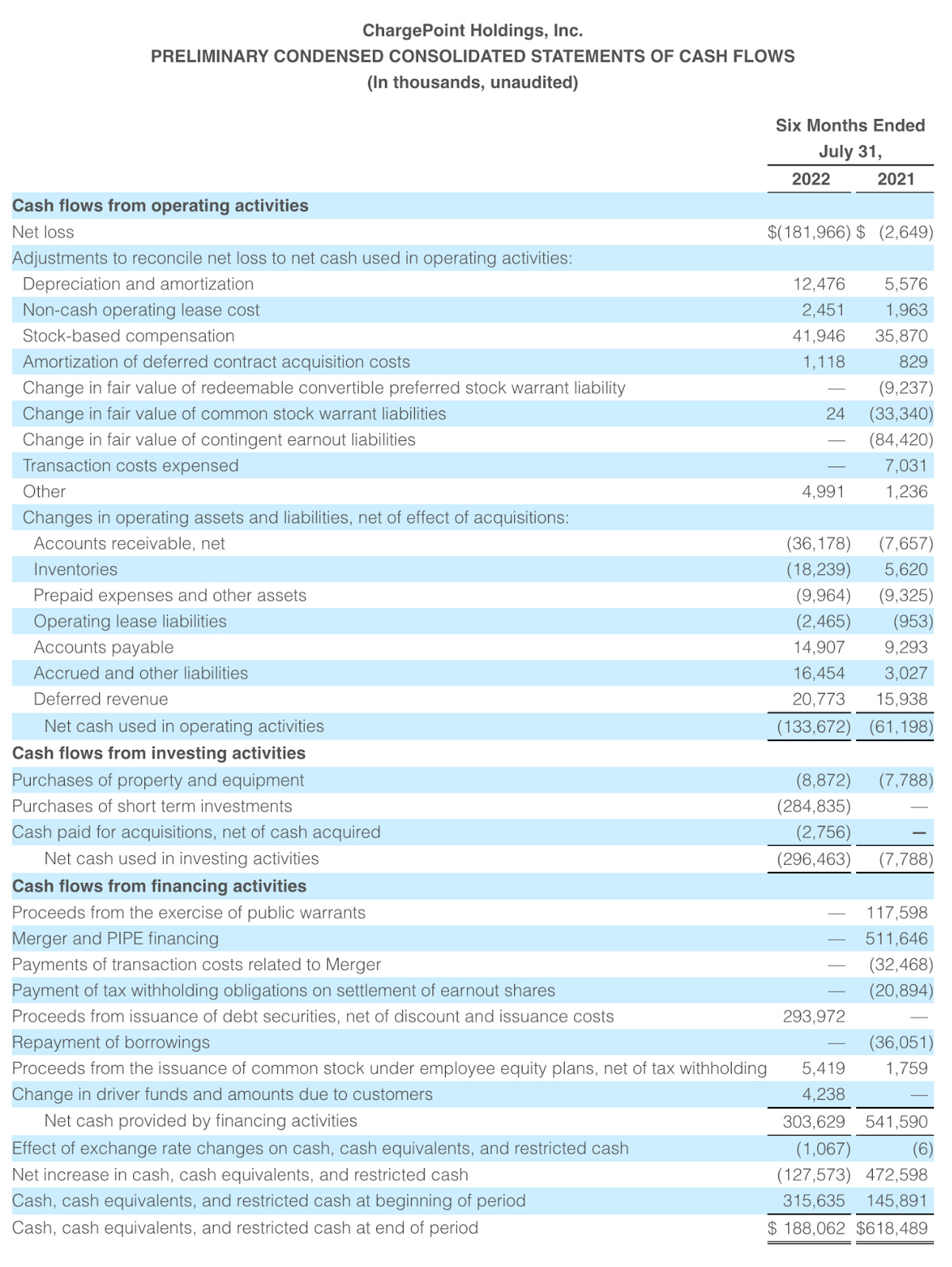

Cash Flow

Net cash used in operating activities since the beginning of fiscal 2023 was $133.6 million in Q1 2023, consisting primarily of a net loss of $181.9 million and non-cash charges of approximately $62 million.

Net cash used in investing activities was $296.4 million at the end of the first half of 2023, consisting primarily of short-term investments of $284.8 million.

Net cash provided by financing activities was $303.6 million at the end of six months of fiscal 2023, consisting primarily of net proceeds from the issuance of debt of $293.7 million.

Free cash flow was negative $131 million in the first six months of fiscal 2023. The company continues to burn cash heavily. However, the management remains committed to becoming cash flow positive in calendar 2024 (fiscal 2025).

Key Metrics

ChargePoint does not officially report any key metrics in its earnings reports. However, the company does provide some additional information (besides revenue and its breakdown by types, verticals, and geography) that can be valuable for investors.

For example, the company reports the total number of active ports. This number is an indicator of existing ports under management, which is the installed base that is paying the company a subscription fee on an annual basis. It can help investors measure the growth of ChargePoint's network and understand the dynamic of customers' expansion and possible future revenues. Additionally, it showcases the development in Europe, the second largest market for ChargePoint, as the company reports a separate number for this market.

"Our installed base of network ports grew to approximately 200,000, a year-over-year increase of 70% and sequential increase of 7%. Of those, over 60,000 [up from 57,000 in Q1 2023] are in Europe and over 15,000 [up from 12,000 in Q1 2023] are DC fast. And I will remind you that ports under management is one way to track our progress in our commercial and fleet verticals as each of these ports generates an annual software subscription. We do not include home chargers at single family residences in this count, where we continue to have strong demand as well." – from Q2 2023 earnings call.

Risks

As a company that still invests in growth and heavily burns cash, ChargePoint is exposed to a number of risks, some of which are critical and require special attention from all investors considering investing in this company.

Debt

The company will undoubtedly need more cash at some point to scale its network further. Becoming the key player in this space will require spending hundreds of millions for many years ahead.

The company will need to rely more on debt leverage in order to obtain the necessary capital. As of Q1 2023, the company already had a debt of $300 million, which can eventually convert into shares, leading to significant dilution.

More debt is expected.

Dilution

Since going public, the company increased its total number of shares outstanding by over 21%. It is an extremely high number for such a young company and such a short period. And because more capital will be needed, more dilution will follow.

Profitability

The company is currently unprofitable, and its projections to become profitable in calendar 2024 (fiscal 2025) are moving farther away.

At the time of the IPO, management suggested that fiscal 2022 revenues would be $346 million, while the company ended the year with $241 million in revenue (approximately 43% less).

The company may not reach profitability at all.

Growth

Despite operating in an industry that is still early-stage but growing exceptionally fast, the company may not sustain its current rapid growth in the future as more and more players will enter the market.

Competition

Covered in detail in the Competitive Advantages section.

The competition should only intensify in the coming years as the market for EV charging develops.

Tesla possesses a hidden threat should the company decide to open up its charging network for non-Tesla vehicles.

Europe expansion

Since Europe is expected to significantly contribute to ChargePoint's revenue in future years, the company substantially depends on its success in this market, and to succeed, it will require a lot of capital.

Fleet expansion

The company's growth is also dependent upon success in the fleet vertical. This particular market is even more competitive and has several specifics like a high customer dependency on the expected increase in the arrival rate of new vehicles.

Supply chain

Supply chain problems are breaking down ChargePoint's projections and harming its growth. These problems are expected to persist throughout the entire 2022, at the very least.

Government

The company heavily depends on government mandates, incentives, and programs, which significantly lower EVs' effective price and infrastructure needed to support the EVs.

Any reduction in rebates, tax credits, or other financial incentives would significantly harm the charging infrastructure development.

Innovation

The EV charging market is characterized by rapid technological changes. The company will need to continuously invest in R&D to develop products to stay competitive. Right now, the company spends almost 60% of its total revenue on innovations, which will most likely not decrease in the near future.

Ownership

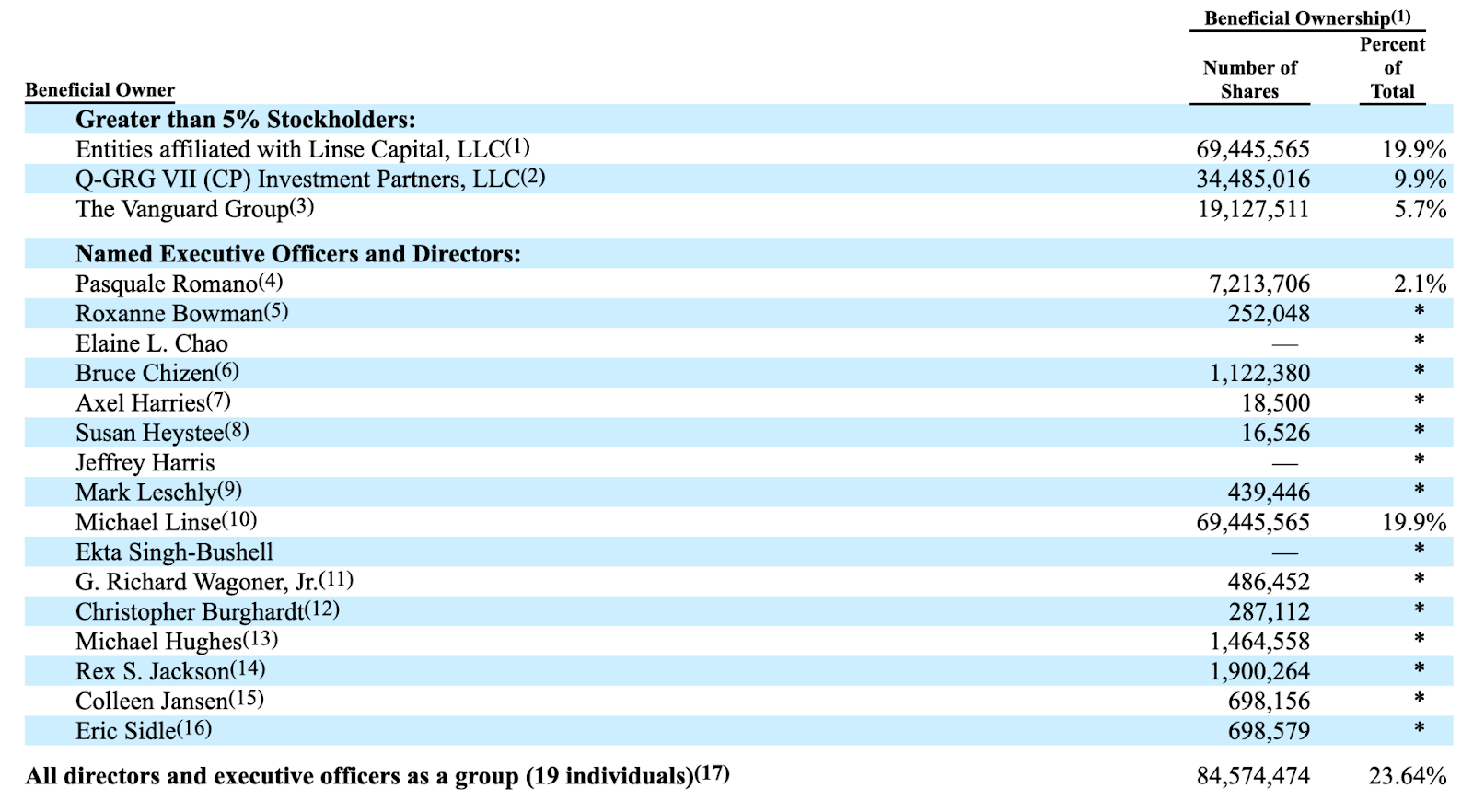

According to the latest proxy statement (DEF 14A) filed on May 2, 2022, the ownership structure of the company looks the following way:

The beneficial ownership percentages in the table above are based on 336,668,226 shares issued and outstanding as of Q1 2023.

The largest insider shareholder is the company's board member, Michael Linse. Through Linse Capital, a growth equity firm focused on transportation, energy, and logistics industries, which was the early investor in ChargePoint, he holds more than 20% of the company.

The company's CEO, Pasquale Romano, owns approximately 2.1% of ChargePoint, while the rest of the directors and executive officers as a group (17 individuals excluding Michael Linse and Pasquale Romano) hold less than 2.5%. In total, 25% of the company belongs to insiders.

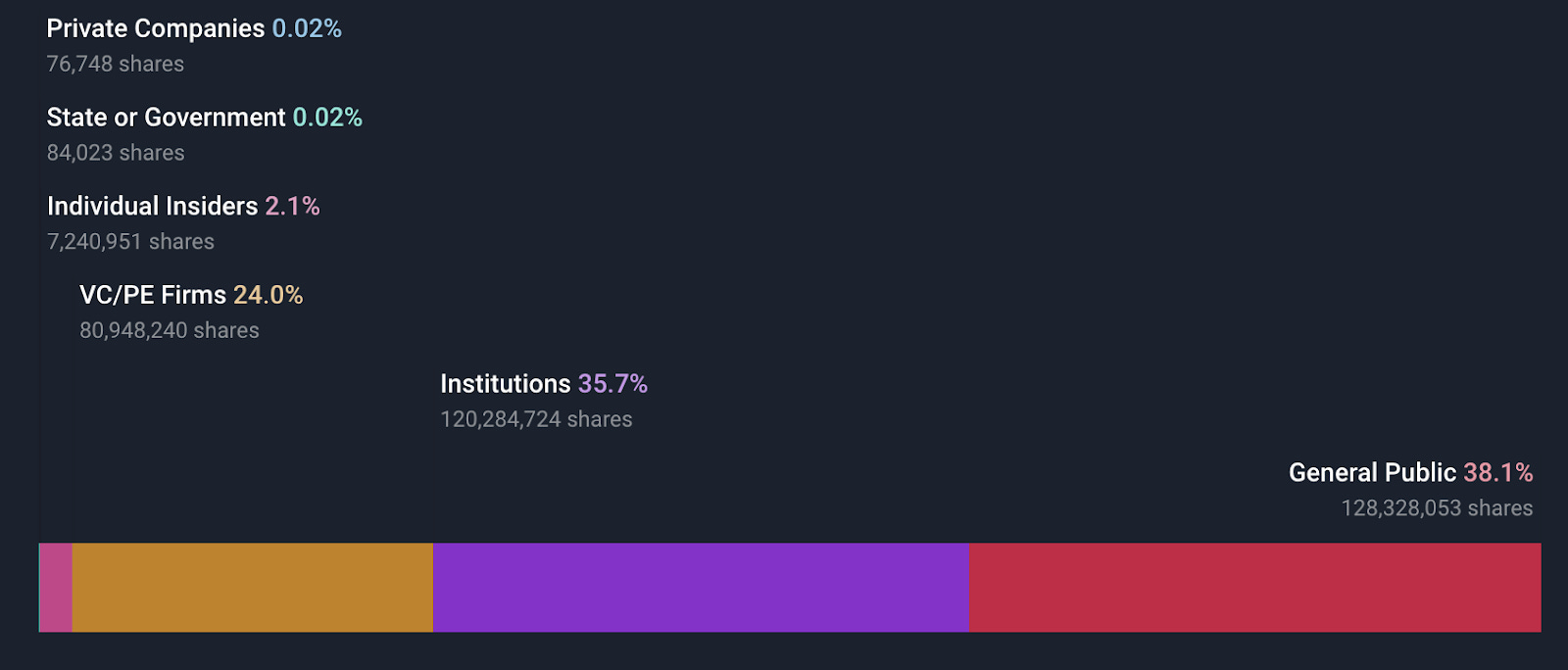

The largest outside shareholders are Linse Capital, Q-GRG (10%), and The Vanguard Group (5.6%). According to SimplyWallSt, all institutional investors right now own no more than 35%, while VC/PE firms have about 24%.

ChargePoint is still popular among retail investors who invested heavily during the SPAC craze in late 2020.

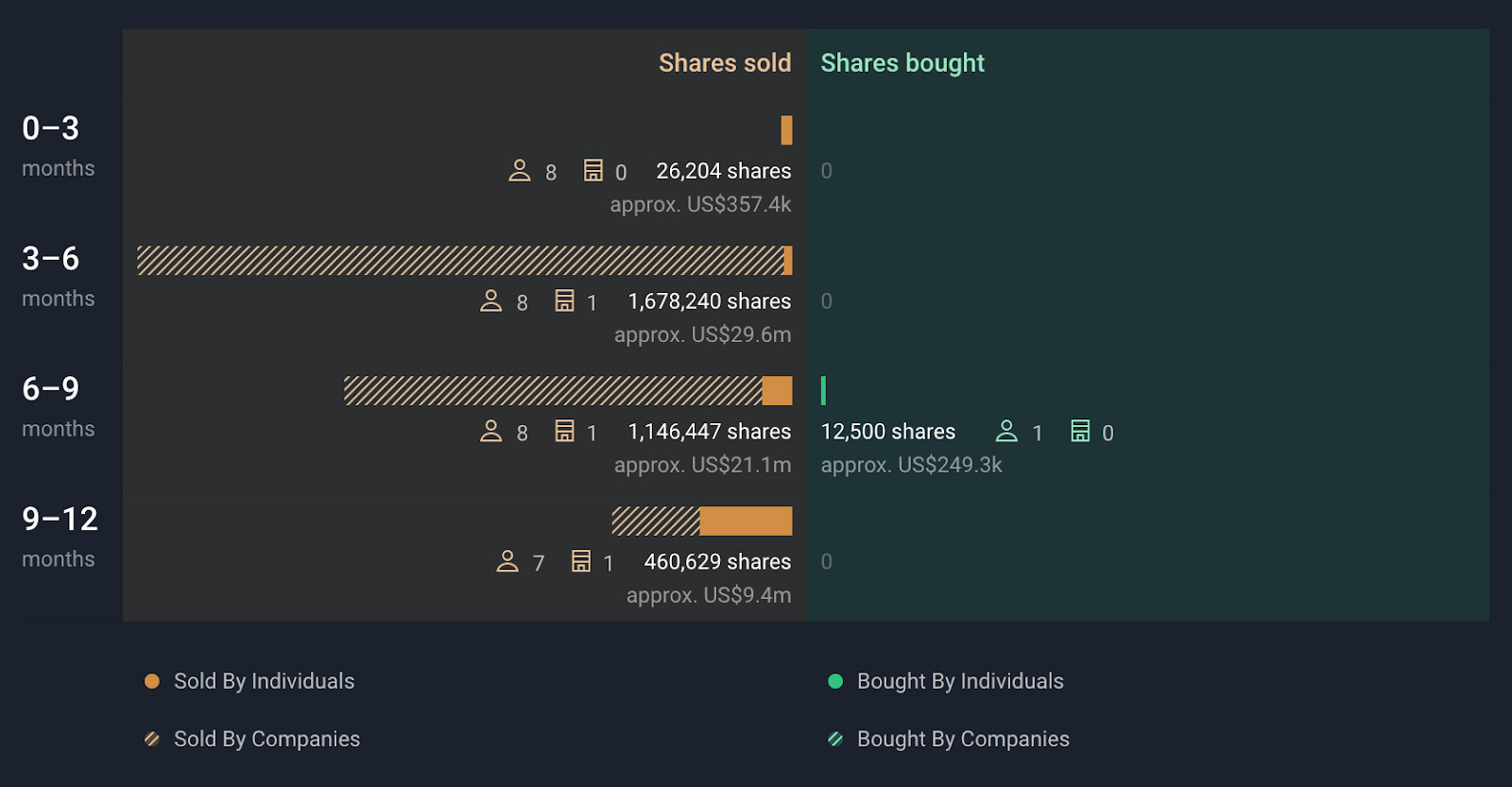

However, since the publication of this DEF 14A form, the company has seen substantial selling from both insiders and institutional investors.

There was just one insider purchase recorded since the company went public. A board member, Susan Heystee, has purchased 12,500 shares worth approximately $250,000.

Valuation

I don’t think CHPT is necessarily cheap at 10x FY2023 sales but I also don’t think it’s expensive when you consider the current growth rates (~100% YoY) as well as the expected growth rates over the next 4-5 years. The consensus from analysts is quite bullish as they’re looking for $2+ billion in revenues in FY2027 (which is calendar year 2026) which is almost a 10x increase from FY2022 (which was last year).

Since CHPT is currently losing money and has negative EBITDA margins it’s kind of hard to talk about valuation metrics when P/S (price to sales) is basically the only one we can use. We could talk EV/GP (enterprise value / gross profit) but I think that one is pretty useless unless you’re just comparing a bunch of unprofitable software companies to one another.

In cases like CHPT, assuming you are interested in owning this stock for the long term (3+ years), I think it’s better to look out 3-5 years and start thinking about where EBITDA, net income and free cash flow might be and then what kind of multiple the market might be willing to put on each of these.

Investment Model

These are my rough estimates for CHPT over the next 4-5 years, overall they are slightly more bullish than the analysts. Obviously I’m making alot of assumptions but that’s all you can do with these forecasts since nobody knows the real numbers. Generally speaking I think the analysts tend to lean conservative for hypergrowth companies like CHPT so I don’t mind being a little bit higher than them on my numbers. Over time I’ll tweak my estimates based on CHPT’s performance and guidance. There are plenty of risks and obstacles over the next few years that could jeopardize their growth rates but also lots of tailwinds and even some legislation that should help them.

The four numbers on my spreadsheet that have the greatest potential to be wrong are the annual revenue growth rates, the net income margins, the P/E multiples and the share count. Those potential P/E multiples might look high if you’re not used to investing in high-growth companies but I assure you if CHPT if growing earnings in the triple digits in FY2027 they’ll probably get a 60-90x multiple on those earnings especially if earnings growth the following year is also expected to be strong. This is why I’ve started adding another year to my spreadsheets because the P/E multiple in the second half of FY2027 will start to reflect the expected earnings growth in FY2028 so it’s important to look ahead at those numbers to give a reference point.

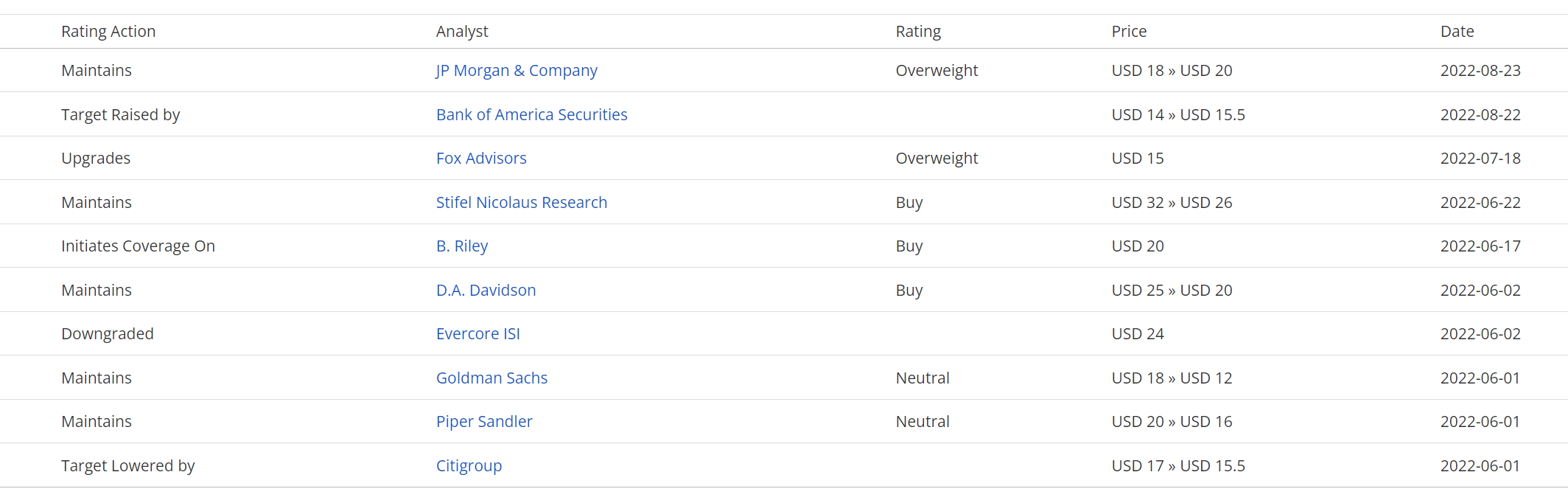

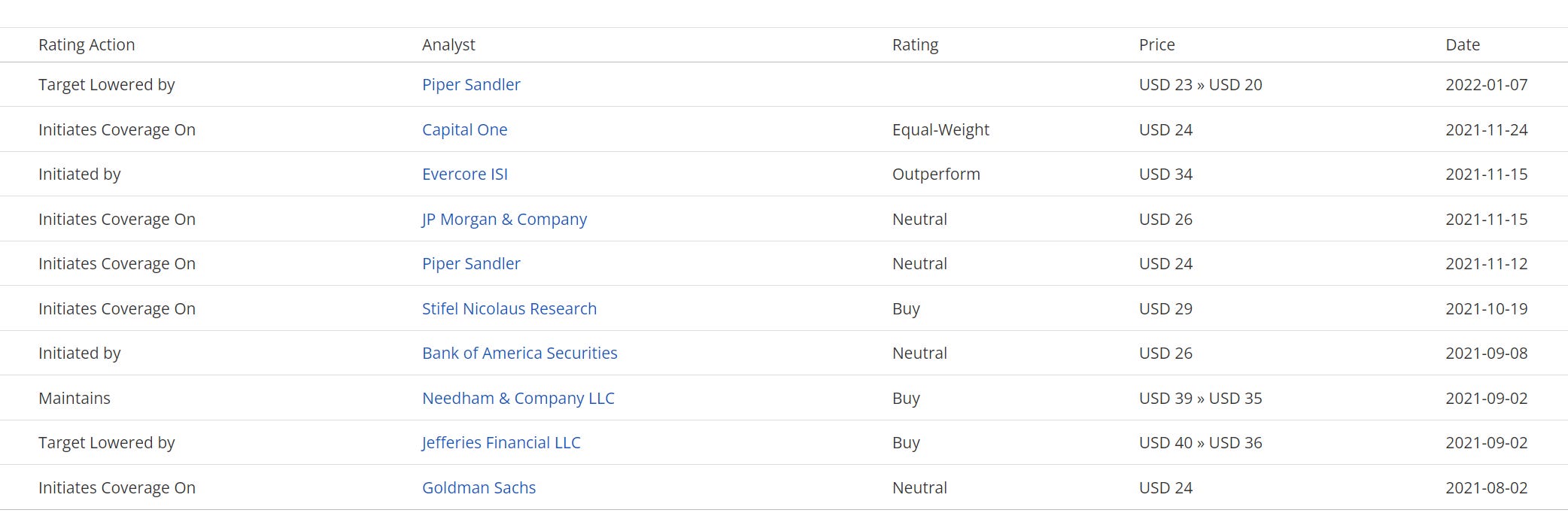

Analysts

If I look at the last 12 months, there’s approximately 14 analysts that have a rating and price target on CHPT but unfortunately some of them have not updated it in many months and only a few of them updated their rating and price target since the Q2 earnings report this past week. Most of the price targets are now in the low to mid $20s which represents 60-80% upside from the current $14.50 price. I could definitely see CHPT trading in the high $20s by end of next year assuming they’re on track to do $750-800 million of revenues in FY2024 and $1.1-1.2 billion the following year.

Here’s what the analysts are saying:

August 31st: Oppenheimer analyst Colin Rusch says ChargePoint posted strong results as it continues to work through supply chain headwinds. The analyst is encouraged to see ongoing revenue growth at the company despite limited commercial vehicle availability and government funding yet for electric vehicle infrastructure. Both of those elements could drive growth in excess of current expectations, Rusch tells investors in a research note. At the same time, ChargePoint is leveraging its "best-in-class software offerings" into a growing recurring revenue base, says the analyst. Rusch keeps an Outperform rating on the shares with a $40 price target.

August 31st: JPMorgan analyst Bill Peterson reiterates an Overweight rating on ChargePoint with a $20 price target saying the company reported revenue well above consensus and above the high-end of guidance on "broad-based strength with Commercial being particularly strong." While ChargePoint continues to see margin headwinds related to inflationary pressures and supply constraints, dislocations appear to be improving directionally the company is also able to pass along price increases, particularly in North America, which is also positive for margins, Peterson tells investors in a research note. He continues to think ChargePoint's "leadership across verticals (Commercial, Fleet and Residential) is underappreciated."

August 22nd: BofA analyst Ryan Greenwald raised the firm's price target on ChargePoint to $15.50 from $14 and keeps a Neutral rating on the shares ahead of the company's Q2 results. Management has established a track record of beating quarterly sales guidance and this trend should continue, Greenwald tells investors in a research note. The analyst increased sales forecasts saying the signing of the Inflation Reduction Act is poised to provide support to electric vehicle charging infrastructure buildout that is likely to lead to a more redundant network nationally.

June 22nd: Stifel analyst Stephen Gengaro lowered the firm's price target on ChargePoint to $26 from $32 and keeps a Buy rating on the shares as he is lowering his targets across his EV charging infrastructure coverage to reflect higher interest rates. Among the group, ChargePoint remains his favorite EV charging name based on its capital-light business model and growing recurring subscription revenue stream.

June 17th: B. Riley analyst Christopher Souther initiated coverage of ChargePoint with a Buy rating and $20 price target. The analyst likes the company's "dominant" market share, established brand, and growth strategy. ChargePoint has more than a 70% market share in networked Level 2 charging in North America and 5,000 commercial and fleet customers globally, Souther tells investors in a research note. He expects the commercial business to drive margins and says ChargePoint has cash for further investments.

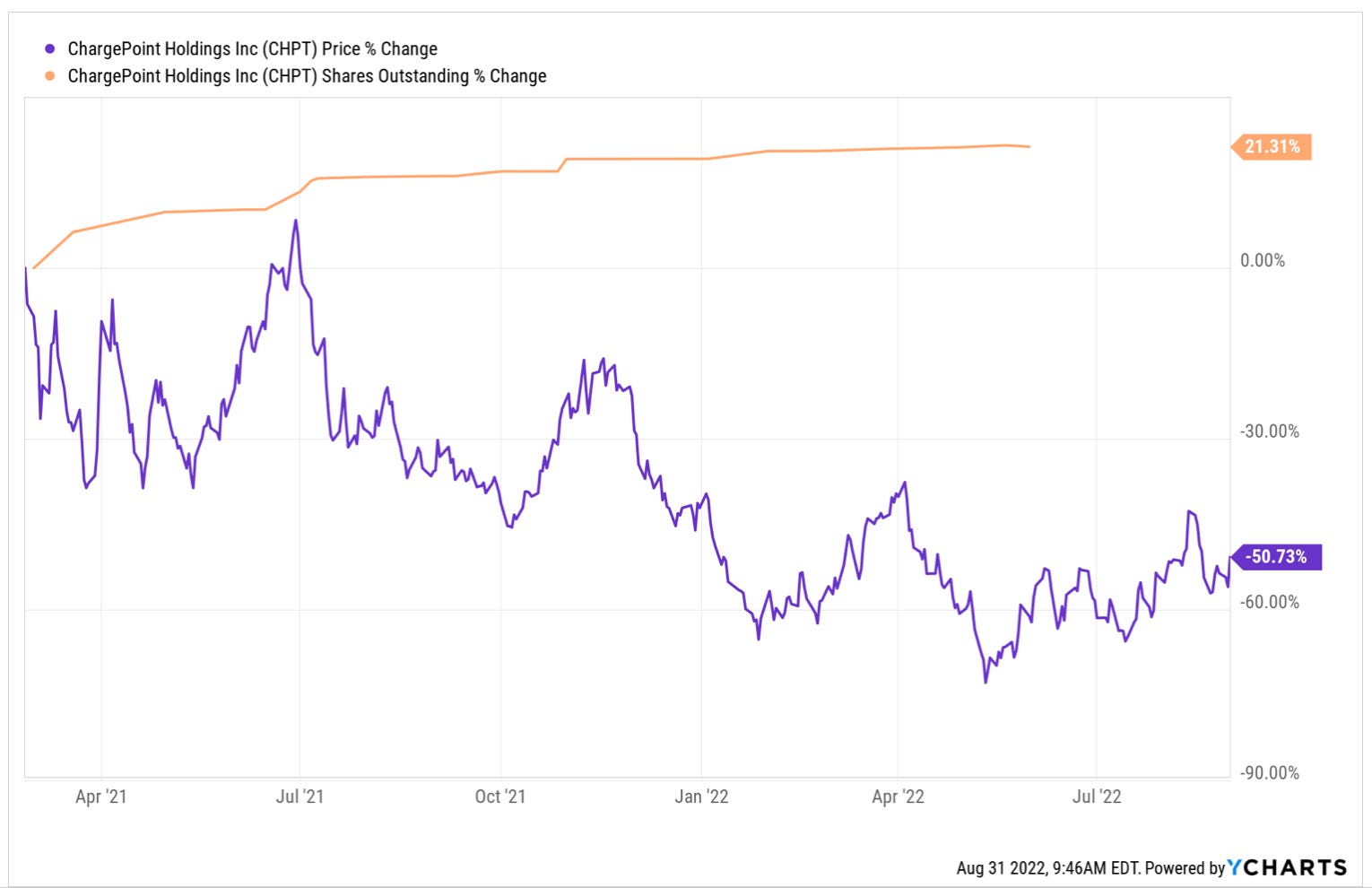

Technicals

If you look all the way to the left on this chart you’ll see where CHPT used to be a $10 SPAC and then after it announced the merger with ChargePoint it shot all the way up to $49 before falling more than 82% into the May 2022 lows. CHPT is still in a clear downtrend however we could see a nice breakout in the coming weeks if we can push through that downward sloping resistance line. It’s hard to say at what price we’d breakout because the timing matters but it would likely be $16-17. If we did breakout we’d want to see this resistance line hold up as support on any pullbacks and retests.

That bottom support line is connecting the May lows to the June lows which is around $13.50 right now but will increase everyday. From a technical standpoint you would not want to see CHPT break below that support line because then it’s likely going to retest the June lows. I think it’s very unlikely we go lower than that given the strong Q2 results from this past week. Based on this wedge pattern forming, the next couple weeks are very important for CHPT.

CHPT has been above the 200d SMA in the past couple weeks but wasn’t able to hold it. As of Friday’s close (which wasn’t pretty) we’re back below the 10d EMA, 21d EMA and 50d EMA but just above the 100d SMA. If you were looking to start a position in CHPT this week and wanted to limit your downside you could always set your stop loss just below the 100d SMA or set your buy limit order just above the 100d SMA in case we do pullback and retest it. If we go lower and can’t hold the 100d SMA then the next area of obvious support would be that support line I mentioned earlier. That would also be a nice place for a big add to my position in hopes of a substantial bounce. Since I’m hoping to own CHPT for the next few years while increasing my position on any pullbacks, it’s doubtful that I’m going to use stop losses anytime in the near future. If CHPT goes down to $13.50 I’ll be adding the whole way although if we didn’t bounce there and the broad markets were looking pretty gross I might reduce my position and hope for a retest of the June lows.

Conclusion

To recap, I’m obviously bullish on CHPT at current prices. Not sure who was buying this stock last year at $45+ but now that it’s pulled back 80% while the fundamentals have continued to improve (despite still losing money), I think CHPT is a growth stock that you should consider for your long-term portfolio (assuming you understand the risks).

I currently have a 2% position in CHPT but I’d be very open to increasing that to 3% in the next few weeks if the stock pulled back and I could lower my cost basis. Just like STEM is one of my favorite stocks in the alternative energy storage space, CHPT is one of my favorite stocks in the EV space and like I mentioned above… rather than picking which EV automaker is going to be the winner over the next 4-5 years, I think I’d rather use a stock like CHPT for my EV exposure because they benefit from overall EV adoption regardless of which brand you are buying and driving.

Since CHPT is a relatively new position for me I’m still learning more about this company and will continue to do my due diligence in order to maintain the conviction needed to own the stock going forward. I would suggest listening to the recent earnings call, there’s a ton of great info/data about the company, the opportunity and the strategy — management seems very capable and competent.

We all know that most SPACs ended up being complete disasters but so far it looks like CHPT could be one of the real gems.

If you have any thoughts or comments regarding CHPT or something we missed in our writeup, please feel free to reach out.

Regards,

Jonah Lupton

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.