Deep dive writeup on Dutch Bros ($BROS)

In addition to my Substack newsletter, I also run a Stocktwits room where I post my current holdings, buys & sells, investment models, technical analysis and market commentary for both my Investment Portfolio (long term, strong fundamentals, 20-30 holdings) and my Trading Portfolio (short term, strong technicals, 0-10 holdings). The two options are $15/month for the monthly plan [click here] or $150/year for the annual plan [click here].

You can now signup for my new Substack called Jonah’s Trading Charts which is focused exclusively on the technicals — every day (usually pre-market) I’ll send out an email with my favorite trading charts/setups. You’ll also have access to my trading portfolio with current positions/sizes, entry/exit prices, profits/losses and much more. I’m also doing live charting and live trading 3-4 times per week.

Company: Dutch Bros <> Dutch Bros Coffee

Ticker: $BROS

Website: DutchBros.com

IPO Date: September 15, 2021

IPO priced: 24.2 million shares at $23 [click here]

Total shares outstanding: 165 million [click here — page 89]

Quiet period expiration: October 9, 2021

Lockup expiration: March 13, 2022

Current stock price: $46.00

52 Week High: $81.40 on November 1, 2021

52 Week Low: $32.42 on September 15, 2021

Market Cap: $7.5 billion

Headquarters: Grants Pass, Oregon

Number of employees: 8,500+

Analysts: 8 of 9 have a BUY rating (88%)

Average price target: $70.13

Investor Relations [click here]

Form S-1 filing [click here]

2021 Q3 earning report [click here]

2022 Q1 earnings presentation [click here]

2021 Q3 earnings webcast [click here]

2022 Q1 earnings call transcript [click here]

Barclays Investment Conference [click here]

INTRODUCTION:

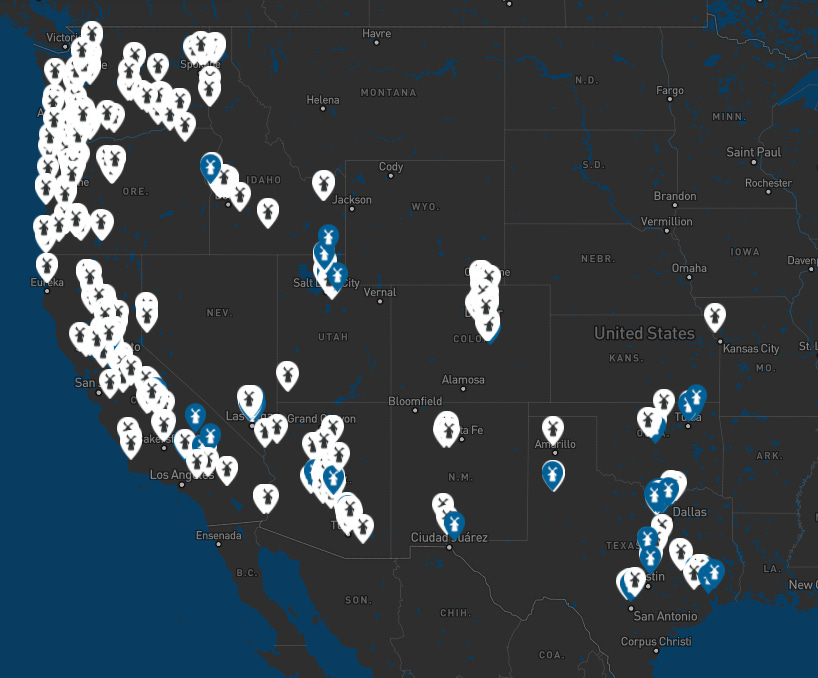

Dutch Bros ($BROS) is an Oregon-based company that operates and franchises drive-thru coffee shops. Initially an exclusive West coast operation, the company has started expanding across the US and today has +500 stores (aka shops) in 12 states which includes Oregon, Washington, California, Nevada, New Mexico, Arizona, Colorado, Idaho, Utah, Oklahoma, Kansas and Texas.

To say that the company’s products are “sticky” would be an understatement – sugary drinks and coffee are extremely addictive. Additionally, the company has managed to garner significant brand recognition (particularly amongst millennials and the “hipster” crowd) and is seen as the “next Starbucks” in some circles.

Before you get into the writeup, I recommend watching this video from 2015 which gives you a good idea of the culture that $BROS has created for their employees and their customers — it honestly looks like a fun place to work.

OVERVIEW:

Founded in 1992 initially as a pushcart operation by brothers Dane and Travis Boersma (third generation dairy farmers), $BROS offers its name brand hot and cold espresso based beverages and cold brew coffee products as well as its branded Blue Rebel line of energy drinks, teas, smoothies and other beverages mostly through company operated shops and online channels. Most of its operations are drive-thru (more on that later). The company has historically served the West coast however, post IPO it has begun to ramp up its expansion efforts into the Midwest.

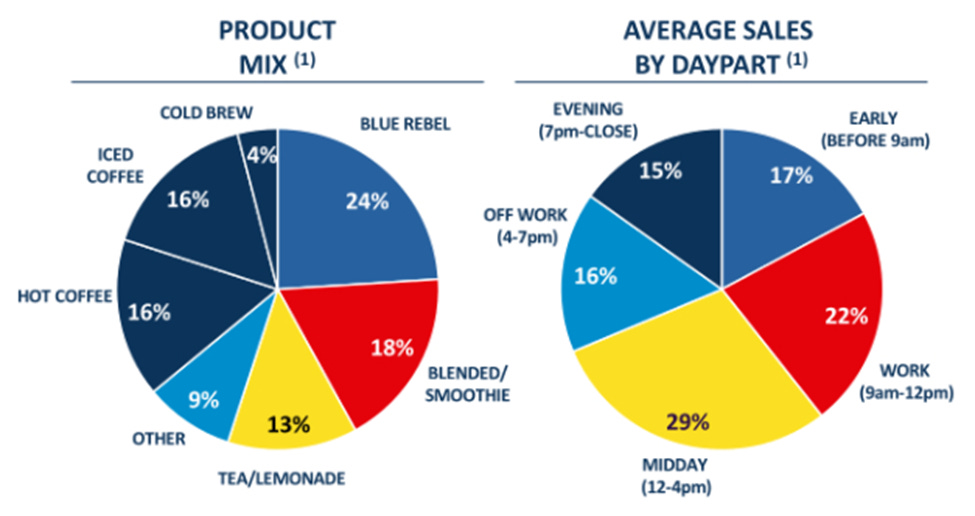

According to the company, there are more than 9,000+ unique drink combinations at $BROS and even though the company is best known for their hot, cold and blended espresso beverages… this makes up less than 32% of total beverages sold meaning they have sufficient product diversification across their menu with mass appeal.

By its own admission, the company has a stated goal of getting to 4,000+ stores which means they’ve reached less than 15% of their full brand penetration. As a shareholder and someone that loves coffee, it would be exciting to see $BROS expand to the East Coast and begin penetrating the densely populated metro markets that many of us live in.

$BROS has a massive opportunity to embed its coffee and branded products in the same way that rival Starbucks has done by driving expansion across the globe. The company began trading on the New York Stock Exchange on September 15th, 2021, after completing its IPO. The company issued 24.2 million shares at a price of $23 (raising $550M+), just above the expected range of $18-$20 which shows that demand for this particular offering was strong.

The company had significant buzz coming into its IPO and as a result the stock shot up more than 50% within the first few hours of trading (high of $40.10) and was up more than 100% in the first week of trading (high of $62.00). That means the stock is currently down 22% from the first of trading and down 41% from the post-IPO highs back on November 1st.

The Dutch Bros IPO was the largest in the Oregon’s history.

BUSINESS MODEL:

The $BROS business model is pretty similar QSRs (quick service restaurant) where they own/operate a portion of the locations and then the rest are run by the franchisees.

$BROS locations are very tiny — which is a significant advantage in terms of cost of operations, rent, utilities, etc. $BROS reminds me of Chick-Fil-A in terms of how efficient they operate and of course their impeccable customer service.

The $BROS shops range on average from 850 square feet to 950 square feet — of course some are smaller and some are larger. By contrast, the average Starbucks ($SUBX) locations range on average between 1500-2000 square feet and the average Dunkin Donuts runs 1200-2600 square feet. In terms of revenue per square foot, $BROS does some impressive numbers.

According to its S-1 filing, it costs $BROS on average $1.3 million to set up a single location which is pretty wild considering the size. I’ve heard that Starbucks and Dunkin Donuts can now run you $2-3 million each although that typically includes the franchisee fees.

$BROS also has number of franchises from which it earns fees. As of Q3, 52% of total shops were franchises (262) versus 48% being company owned (241). Franchise fees are $50,000 for the first shop and $30,000 per location for additional shops. Franchisees pay a 5% royalty on sales to $BROS corporate and an additional 1% that goes to the Dutch Bros Marketing program. Additionally, franchisees are required to spend at least 1% of their quarterly revenue on local marketing and charitable causes. The company has however decided to no longer franchise additional locations. To quote the company “Moving forward, all locations are company-owned and regional operator positions are offered exclusively to those within the company who have shown outstanding employment history and exemplify the culture”.

$BROS has segmented its approach and believes it can significantly grow its market share around three addressable markets where beverages are sold:

general coffee category

convenience store category

quick service restaurant category

This segmentation seems a bit of a reach — feels like this might be doing this to give the perception of a larger TAM but in reality their primary market is plenty big.

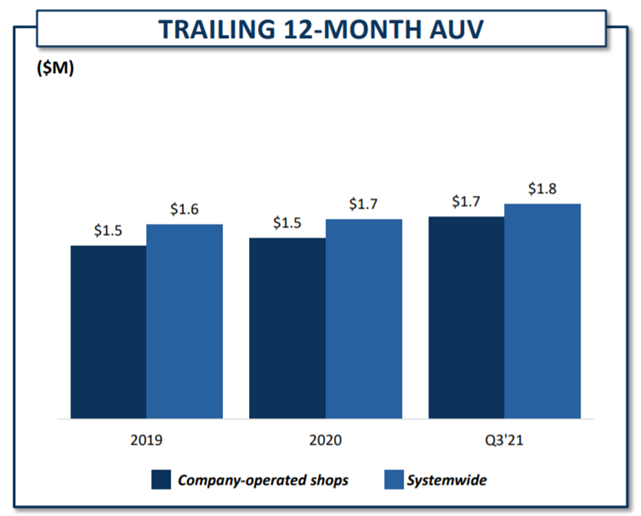

As far as the product mix, customers can choose from a range of warm and cold beverages, as well as customize drinks to their liking. $BROS average unit volume (AUV), as of Q3 2021 was $1.8 million with an average customer bill of $7.50.

They have managed to consistently stay above $1.7 million since 2020. As the company expands it will be interesting to monitor the growth (or contraction) of this AUV figure.

KEY METRICS:

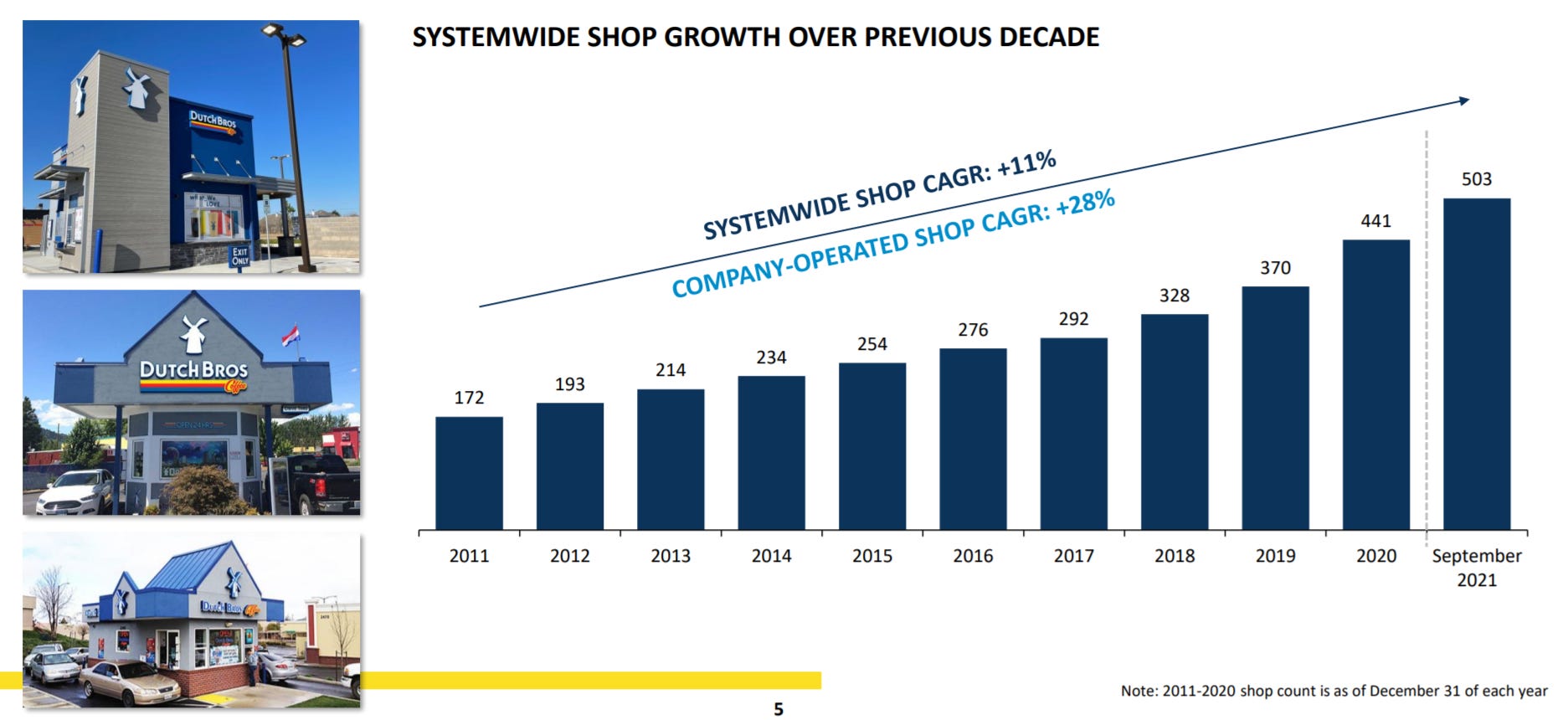

For a business like $BROS, a few key metrics drive most of its business. The first would be the rate at which the company is able to rollout new locations — $BROS has been around since 1992 but most of their growth has happened in the past decade. Since 2011, $BROS has grown their shop count by an average of 11% per year.

It has also grown its company operated stores by 28% during the same 10-year period. This contrasts with Starbucks which has grown its system-wide store chain by roughly 9.9% per year over the last decade. Comparing the store growth rate of $BROS to Starbucks may not be an apt comparison because the bases from which they are starting is obviously different. To put things in perspective, $BROS is up to 500 stores in the U.S. versus Starbucks at 15,000+ stores in the US.

That said, it is still a positive sign to see that $BROS is not lagging their largest competitor in terms of new store openings.

Another key metric is the AUV per store. As stated earlier, each BROS store does roughly $1.8 million in AUV per annum. Quite commendably, when Covid hit, the company was still able to maintain its AUV above $1.7 million. The lack of fall off during Covid can be seen as a testament of the stickiness of the product. As I stated from the very outset, selling sugar and caffeinated products can be a wonderful business. Also, $BROS managed to optimize its online ordering and app platform to mitigate any possible shortfall. By contrast the AUV for a Starbucks is estimated at $540,000 and for a Dunkin Donuts, it’s estimated at just over $1 million per annum. Again, a lot of context has to be placed around these numbers but as mentioned before, it is quite impressive to see $BROS operating in the same ballpark (if not ahead) of the big boys. For me a cause for concern on the $BROS thesis would be if I saw a massive gap between its comparable performances with the larger players.

The final key metric I think that merits examination is employee retention. Anyone who’s ever worker for, or knows anyone who runs a quick-service operation understands the challenge of retaining employees and reducing employee turnover. These jobs, are by their very nature, high turnover jobs. The costs involved in recruiting and training new employees are not immaterial in running a quick service business. According to $BROS S-1 filing, 40% of employees of company-operated shops stay with the company for at least one year. This is a pretty good retention rate when measured against industry giants like Starbucks (65% annual employee turnover) and Dunkin Donuts (60% annual employee turnover)

GROWTH DRIVERS:

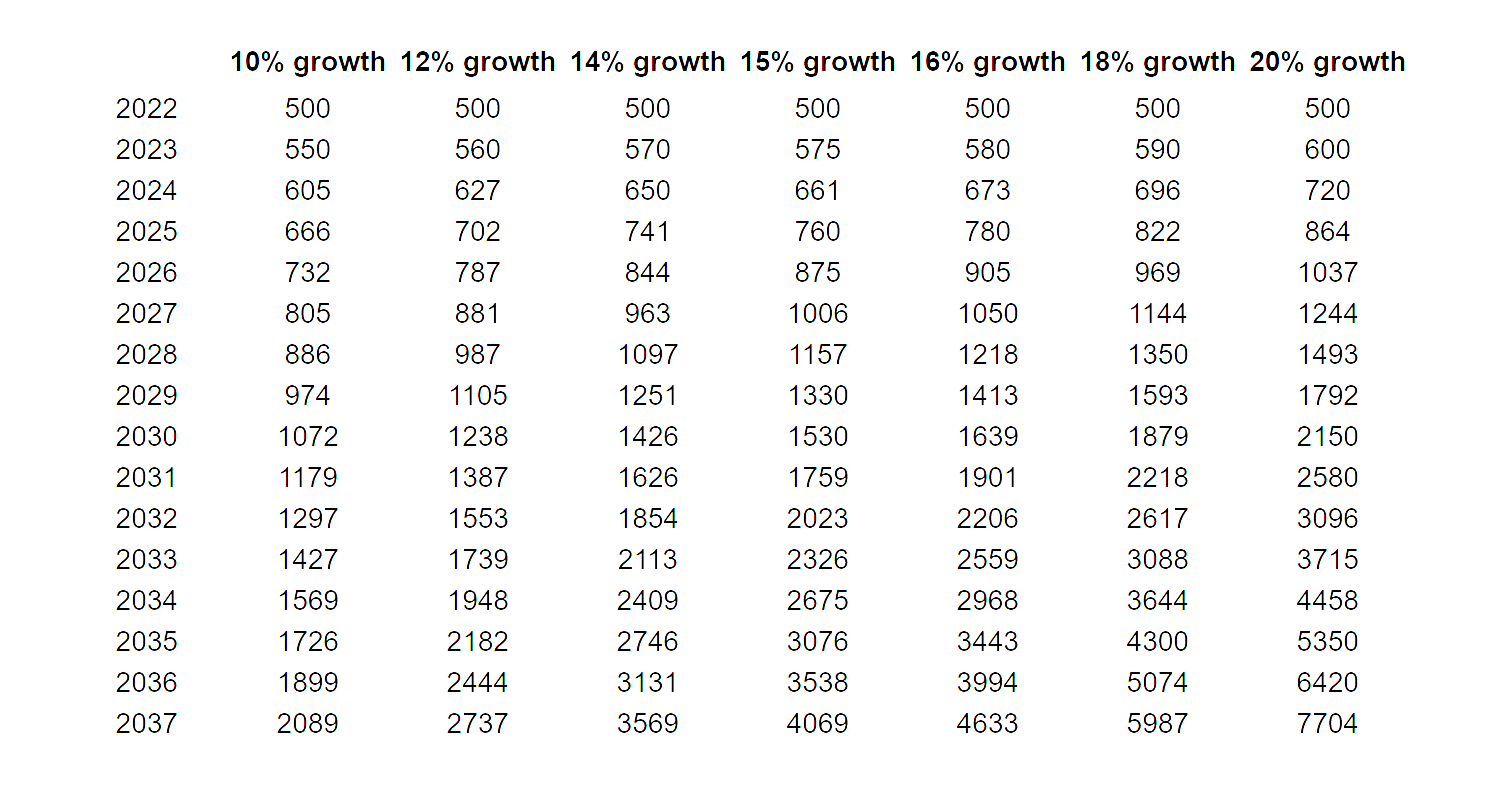

For me, the biggest growth driver for $BROS will be its ability to add new customers to its existing customer base as it expands eastwards and across the US, and maintain its attractive unit economics and customer loyalty in the process. By their own admission, central to their future success will be opening new stores – scaling up to 4,000+ shops over the next 10-15 years as management has stated would represent an 8x increase from the current ~500 stores. Based on this chart below that I created, it would take them approximately 15 years to get to 4,000+ shops if they were able to grow the # of shops at 15% per year. I think it’s fair to assume the current cost of opening a $BROS shop will not only increase over the years because of inflation and other cost pressures but it might also get more expensive as they move east. If we assume the average cost per new shop will average $1.45 million over the next 15 years then $BROS will end up spending approximately $5 billion to open up the next 3,500+ locations. Given their proven operational track record and high ROI from locations I doubt they’ll have any problem financing this growth — but we can still stick it in the “risk” column.

The company says they have 250+ sites identified for new stores which should cover 2022 and 2023 roll outs. Opening a new store is one thing, but ensuring the unit economics are sustainable is another. In other words, growth can help or hurt $BROS if they aren’t able to maintain an adequate AUV per shop and of course there’s always the risk that new geographic markets don’t love the $BROS crafted beverages as much as their current geographic markets (although I find this unlikely).

$BROS takes significant pride in both promoting talent from within but also finding future shop operators from their current employee base then putting them through management training (which they call Dutch Bros Leadership Pathway Program) in order to groom them to run their own shop one day. Based on the CEO’s comments on the last earnings call, they have 200+ people in the regional operator pipeline (with an average of 6.5+ years of tenure at $BROS)… this group can support the next 750-1,000 company owned shops that are opened. The CEO also stated since 2018 every single shop manager position (more than 200+) were filled with internal candidates — not sure I’ve ever seen a culture this strong or one that bent over backwards to make sure new management positions were only be filled by current employees and not hires from outside the company — this is very unique. I suspect this is the main reason why $BROS has such a low turnover or churn across their entire company.

$BROS also cites menu expansion as another growth driver. I can agree with this as there is really no limit to the variation of sugary and caffeinated drink combos people are likely to try and become addicted to. Most beverage businesses live or die by their ability to innovate drink combos and this would be no different for $BROS. One of the advantage that $BROS has in this area is that they allow customers to customize beverages which leaves customers with a certain degree of “control” of their beverage choices. The ability to build your own beverage certainly is a sticky attraction — I mentioned above there’s 9,000+ possible drink combinations.

$BROS also seems to have gained massive traction with its mobile app. The company credits the launch of its Dutch Bros Rewards app in 2021 with driving brand awareness across its jurisdictions and even outside of areas that it serves. Within the first two months of its launch, the app attracted approximately 1.6 million members and as of 2021 Q3 that number is now up to 2.7 million members (including me since I recently signed up even though I don’t live near a $BROS).

As far as I can tell (and I’m trying to confirm this), I’m 99% sure that $BROS still doesn’t allow mobile ordering. Even on the Q3 earnings call this question came up in the Q&A from one of the analysts and the CEO confirmed that they are working on this and hope to have it live in the next 3-6 months.

TBH, this is freaking insane — it’s now 2022 and $BROS has 500+ locations and a market cap of $7.5 billion — how in the world have they not introduced mobile ordering yet? I suspect it gets a little trickier when you business model is drive-up windows but they company needs to find a solution. When you’re competing against the big boys like Starbucks and Dunkin Donuts it’s simply unacceptable to have have mobile ordering already available to customers. I’m an early fan of $BROS but this is really disappointing and the management team deserves some serious criticism for being late to this party.

So basically the mobile app is for paying for orders, receiving rewards and tracking those rewards — plus finding locations, hours, etc.

It still blows my mind that a company of this scale could overlook something this important — makes me wonder what else management has underinvested???

CUSTOMERS:

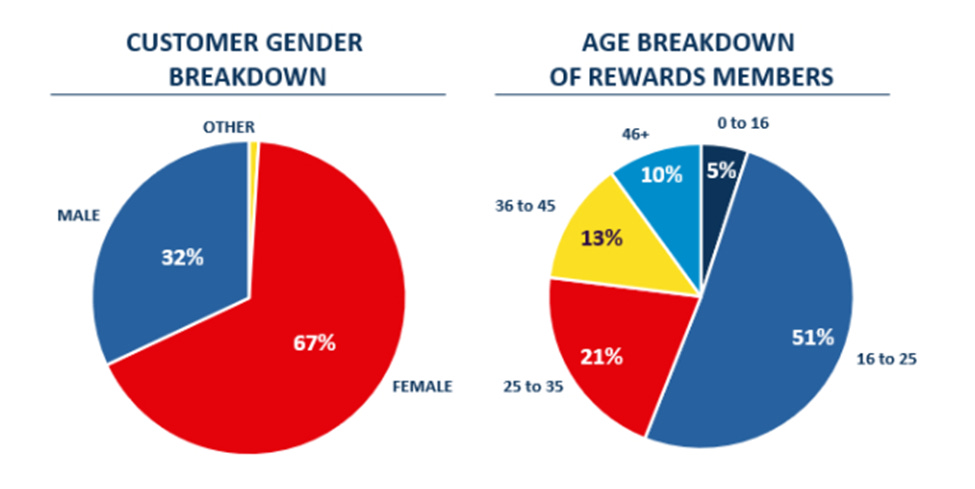

As stated from the outset $BROS has managed to develop a solid following with the millennial and GenZ crowd and to my surprise 67% of $BROS customers are females. I suspect this is not the case for other coffee chains however since $BROS is known for their hand crafted drinks and sugary concoctions, I can see where the females would gravitate towards this more than males.

Additionally, its rewards program skews mostly to a younger audience with the majority of customers accessing rewards between the ages of 16-25. Intuitively this makes sense since this crowd is not generating as much income as the older cohorts and thus rewards to offset purchase costs would matter a lot more to them. $BROS does not break out any additional customer information as I would have like to have seen information around frequency of purchase and other forms of customer behavior.

Here’s a POV (point of view) video if you’re wondering what the ordering process is like at $BROS

MANAGEMENT:

The company is, for the most part still founder-led. It’s also good to see that for the most part, the executive leadership team has significant experience in the coffee and quick service industry. Unfortunately Dutch Bros website does not have a photo panel of its management team but here are some quick points.

Executive Chairman and Co-founder:

Travis Boersma – founded the company in 1992 with his late brother Dane and is still involved in the day to day operations particularly in maintaining the culture and strengthening relationships with operators and franchisees.

President & CEO

John Ricci - Ricci has served as president and chief executive officer at Dutch Bros Coffee since January, 2019. Mr. Ricci has nearly 15 years of leadership experience in the beverage industry. Prior to joining Dutch Bros, he served as president and CEO of Adelsheim Vineyard, president of Stumptown Coffee Roasters, and CEO of Jones Soda Co.

Chief Financial Officer

Charley Jemley - Charles Jemley has served Dutch Bros as chief financial officer since January 2020. Mr. Jemley has over 30 years of restaurant finance and restaurant real estate development experience. Prior to joining Dutch Bros, Mr. Jemley had a 16 year career at Yum Brands and 12 year career at Starbucks Coffee Company. At Yum Brands, Mr Jemley completed his career as the Chief Financial Officer for the Yum China business, serving in that role from 2004 to 2006 and based in Shanghai, China. From there he joined Starbucks to lead its China expansion, serving as Vice President of Finance. Mr. Jemley returned to the United States in 2008, spending the majority of his 12 year career at Starbucks leading Finance for Starbucks International and Channel businesses.

Chief Marketing Officer

John Graham - John Graham joined Dutch Bros Coffee in August of 2020 as chief marketing officer. He brings more than 20 years of experience in marketing and general management with a focus on strategic leadership, brand building and people development. Prior to joining Dutch Bros, Mr. Graham served as CEO of Triton Strategy Partners, LLC, chief marketing officer at Align Technology and GlaxoSmithKline Consumer Healthcare and had a 15 year career at Johnson & Johnson. At Johnson & Johnson, Mr. Graham completed his career as vice president of corporate equity after having worked in the U.S., Australia and China across the company’s consumer, medical device and pharmaceutical sectors.

Chief Operating Officer

Brian Maxwell - Brian Maxwell currently serves as chief operating officer of Dutch Bros Coffee, where he is responsible for the executive team’s performance in implementing initiatives and service to the franchise family. After starting as an original “broista” in 1992, Mr. Maxwell began his 22 year career at Dutch Bros headquarters in 1999 as vice president of growth and franchise coordinator, envisioning and constructing the organization’s franchise system. Mr. Maxwell dedicated seven years to overseeing the expansion of Dutch Bros, helping take the company from 12 locations to 100. He continued to oversee growth until 2009, when he stepped into the general manager position before taking on his current role in which he leads the retail team to deliver on strategic growth plans in real estate expansion and overall store performance

FINANCIAL PERFORMANCE:

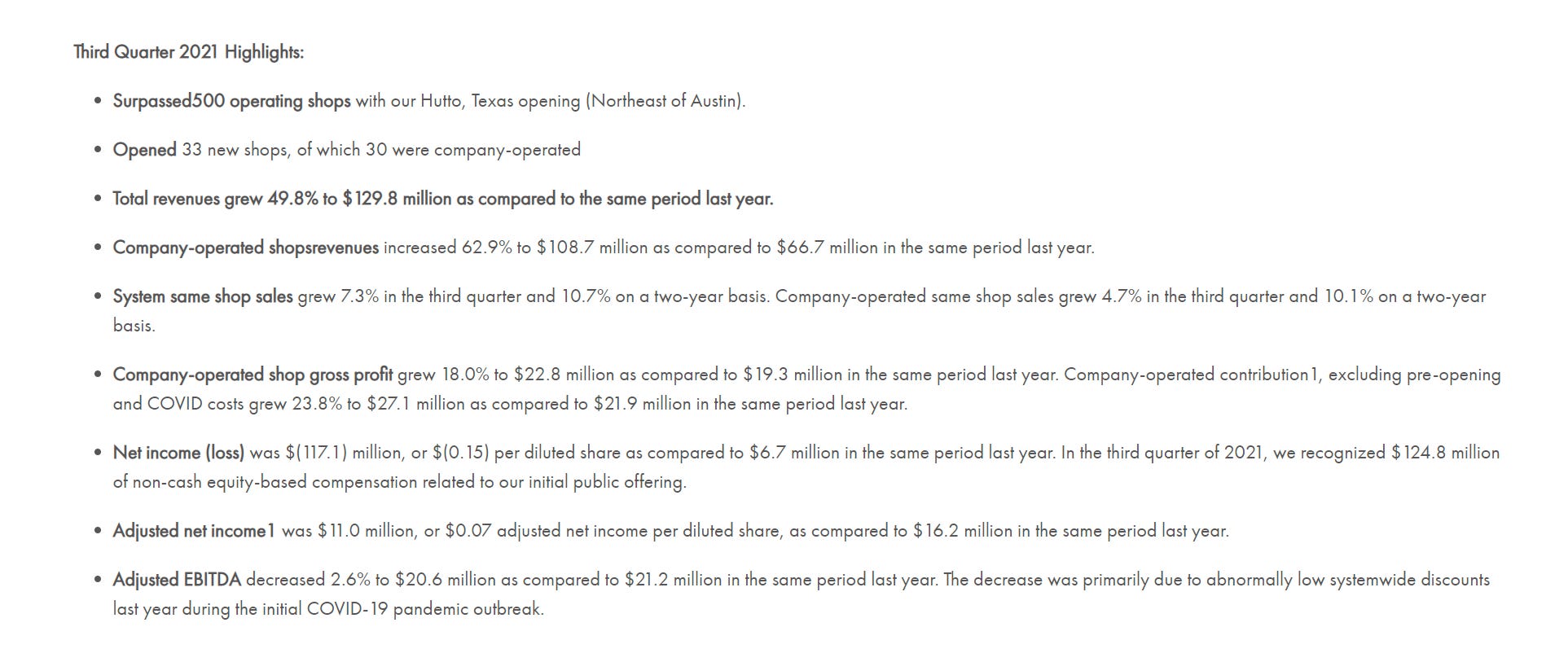

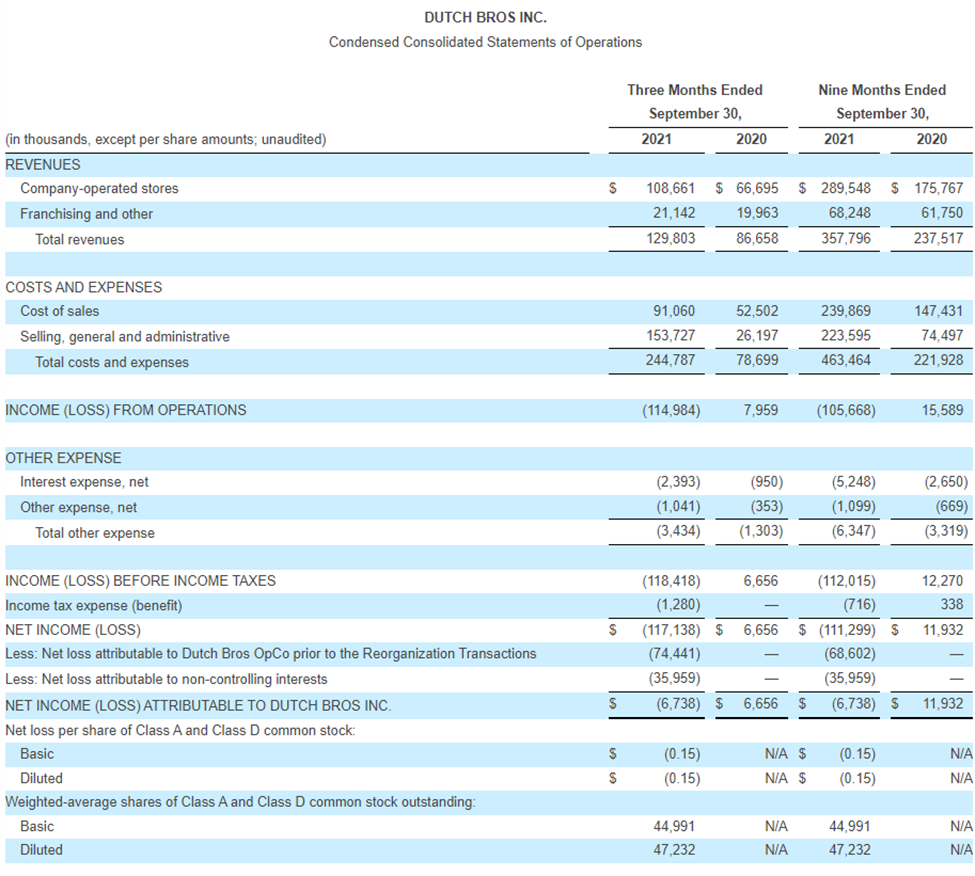

In the mostly recently reported quarter, 2021 Q3, $BROS grew total revenues 49.8% YoY to $129.8 million. For the 9-months ending September 30th, the company recorded total revenues of $357.8 million (up 51% from 2020 when it recorded 9-month revenue of $237.5 million). In terms of Q3, revenues from company owned stores was up 62.9% YoY to $108.7 million which means those company owned stores are doing 82.7% of all the revenues.

Net income for the quarter was -$117.1 million however if you take out the one-time non-cash equity based compensation related to the IPO ($124.8 million) then $BROS actually had adjusted net income of $11.0 million in 2021 Q3 so it’s fair to say that $BROS is a profitable company although compare that to $SBUX which did $1.1 billion in profits last quarter and we can see how small $BROS is compared to their $150 billion competitor from Seattle.

The reason I like $BROS (and it’s not a cheap stock) but they have impressive top-line growth and with only 500 shops it’s pretty clear this could be a growth story for many years to come. For the upcoming year, $BROS is expected to grow approximately 3x faster than $SBUX however the multiple is much higher so I’d say if you want more beta and volatility in your portfolio then it might be worth considering $BROS however if you’re looking for an established global company in the QSR space with more predictive revenues & earnings then $SBUX might be the better fit for you. I have a ton of respect for what $SBUX has built however I consider myself a growth investor and therefore $BROS checks off more of the boxes for what I’m looking for especially if they can accelerate their growth into the Midwest and eventually the East Coast.

It will be interesting to see how $BROS handles inflation and any increases to their commodity and labor costs… will they be able to pass these onto their customers?

VALUATION:

Since topping out at $81.40 back on November 1st, $BROS price has declined by ~43% making its valuation more attractive at these current prices however $BROS is still not a cheap stock so you should be mindful that the current multiple could certainly contract some more especially in the current macro climate with the Fed threatening to raise short term rates even sooner than originally expected.

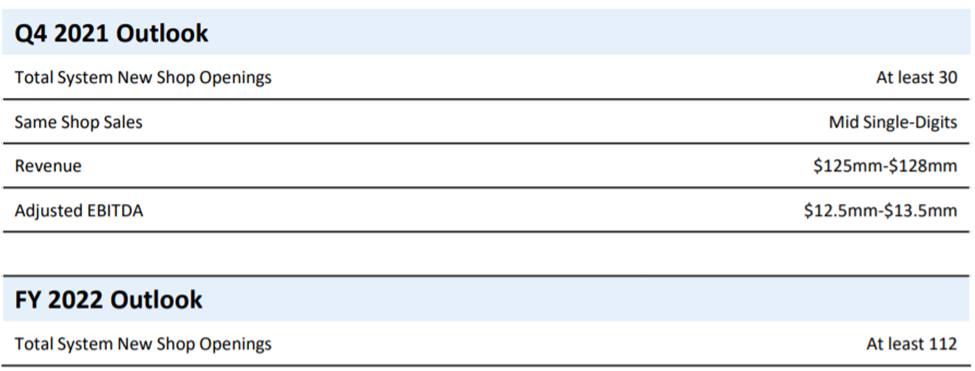

Above are the current 2021 Q4 estimates from $BROS however for the rest of this valuation section I’m going to be using 2022 estimates from the chart below since I prefer to look forward when investing in companies.

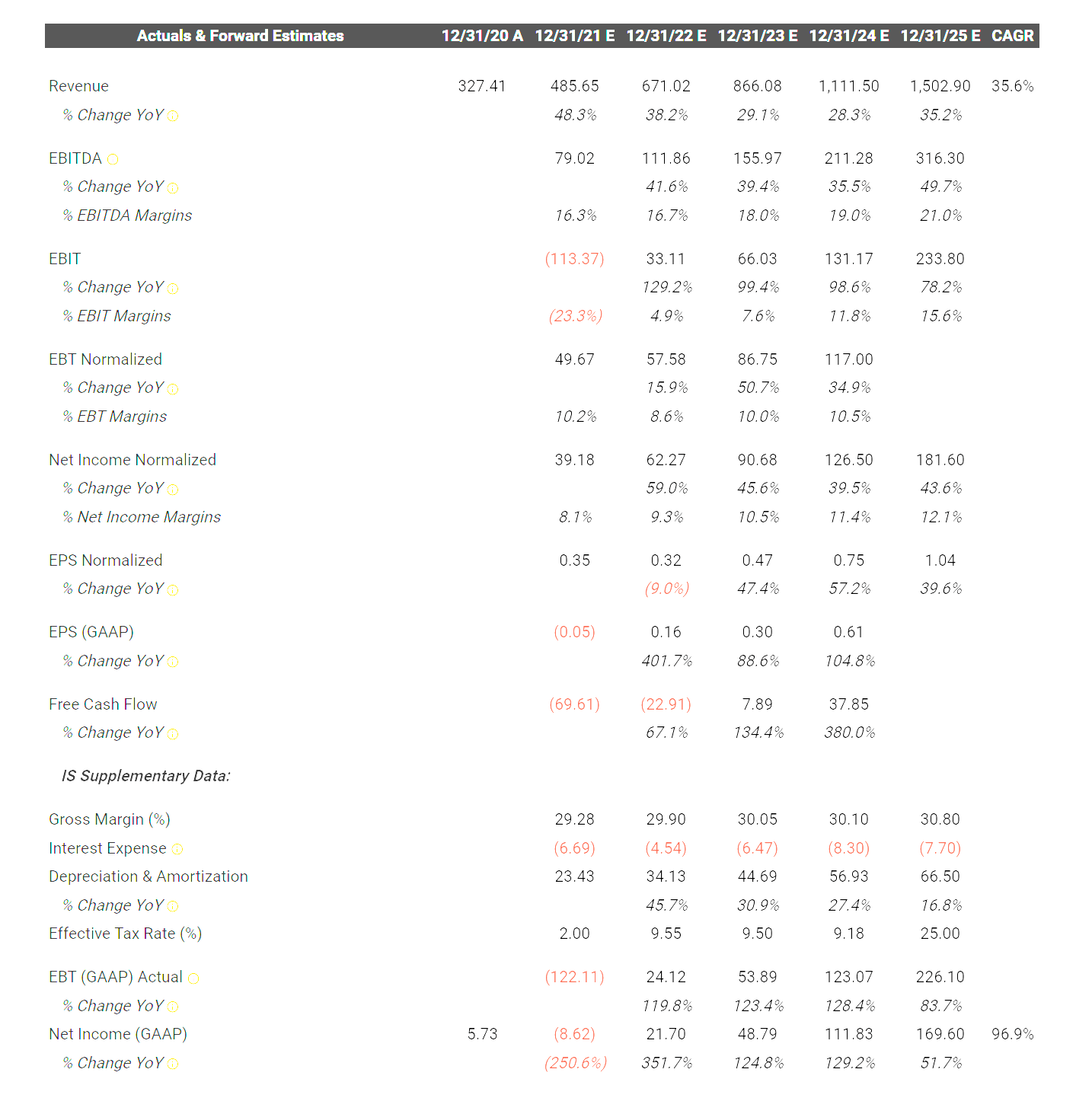

Currently $BROS is trading at 11x 2022 revenues (est.) and 120x 2022 earnings (est.) — in all fairness $BROS is still in their hypergrowth phase so it’s probably not a great idea to determine whether or not $BROS belongs in your portfolio based on these metrics alone, especially P/E.

If we’re comparing to $SBUX which is expected to grow much slower (~12%) they are currently trading at 5x 2022 revenues and 28x 2022 earnings.

For what it’s worth if you look at the chart below $BROS earnings growth is expected to accelerate over the next few years. You’re definitely paying a premium for that $BROS growth but you’re getting much faster top line growth (3x faster than $SBUX) and faster earnings growth once we look past 2022 where $SBUX is growing EPS at 15% and $BROS is growing EPS at 45%.

Based on the current consensus estimates, if we look out 3 years, $SBUX is currently trading at 30x 2025 earnings and $BROS is currently trading at 41x 2025 earnings — now they look a little more comparable however $BROS is the more exciting growth story if they can continue to execute as a public company.

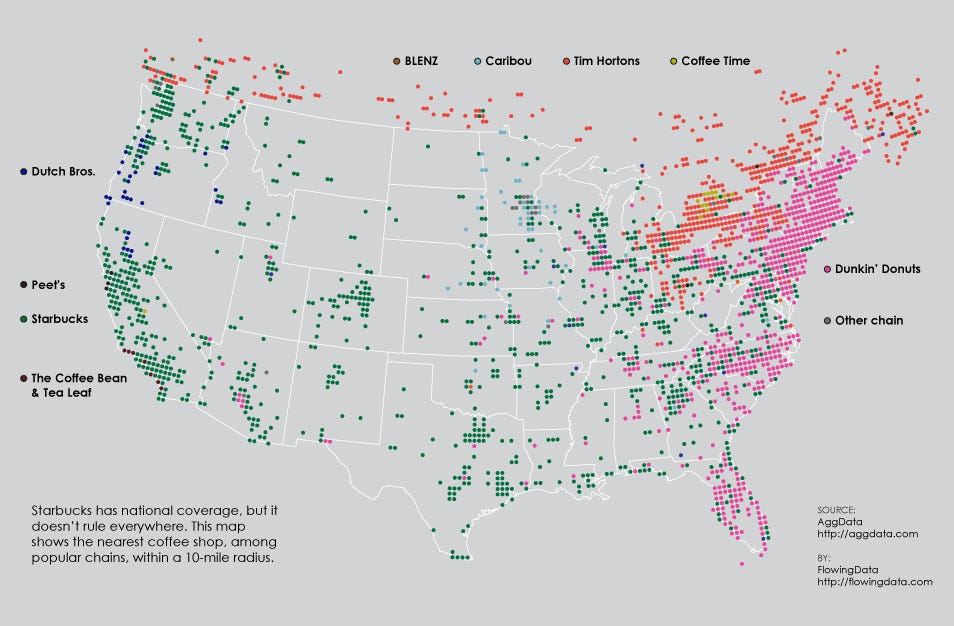

COMPETITION:

The question of who $BROS is competing with seems fairly obvious from the chart above but also because we see these other coffee chains all over the place.

It’s very hard to say which chain has the best coffee… I’m sure you know plenty of people that prefer Starbucks over Dunkins’ and others that prefer the exact opposite. Relative to this discussion, I have friends that live in the PNW and the SW who love their Dutch Bros and say it’s the best coffee they have ever had. From doing my research and having an overall idea of the coffee market, I’m still not sure how many people really prefer their coffee chain versus going there out of convenience. Whether you live in the city or the suburbs, you probably visit your favorite coffee chain because it’s the closest to your house or office. If you had to drive an extra 10 minutes to a different coffee store, I doubt you’d do it on a consistent basis which means the success of these companies is not just having a great product but also having the best locations.

I stumbled across a website called Roasty Coffee [click here] that offered key qualitative insights on both company’s products ($BROS and $SBUX). Naturally this is all subjective, so please view it as such but, according to the website, $BROS scores higher in terms of affordability but Starbucks scores higher in terms of quality. In terms of customer experience, these companies are very different because most $SBUX locations have seating areas so you can come in, sit down, relax, meet some friends, do some work, etc. — $BROS is 99% drive throughs so they’re not providing the same experience and ambiance however I’m hoping this changes over time.

RISKS:

Though $BROS has a substantial following in a limited number of jurisdictions, and prior to the end of Q3 has been profitable, the company is far from a proven entity as it begins to roll out its operations across the US.

I see a number of risks that could affect this business. The company lists 19 itself in its S-1 filing but for the purpose of this writeup, I’d like to focus on what I think the three biggest risks are.

Moat – I can appreciate that moats are built over time, and aren’t always visible, but the durability of any $BROS moat is yet to be seen except that customers do seem to love them and come back on a consistent basis. It is yet to be seen if $BROS customer loyalty will transfer as it heads eastward. To say that it is in an intensely competitive market would be an understatement. Others have tried to take on the major outlets like Starbucks and have run into the scaling problem. To quote BROS: “We may not be able to compete successfully with other coffee shops….intense competition in the food service and restaurant industry could make it more difficult to expand our business and could also have a negative impact on our operating results”

Labor costs – the “Great Resignation” has had a particularly negative impact on the quick service restaurant industry — I’m sure we’ve all seen a tremendous number of “Help Wanted” signs at many small businesses. Though $BROS has a fairly high employee retention rate and employees seem very happy, there’s been a bit of shift in the power dynamic of service staff versus employers recently. This coupled with the rise in state and federal minimum wage means $BROS staff costs are likely to be under pressure as it scales.

Supply chain – this is more of a near term risk because of the prevailing supply chain issues making business difficult across the globe, but as $BROS scales and opens new company operated stores… the logistics and supply chain management will become more critical to their success. Managing a supply chain of coffee beans, flavored syrup and other ingredients across 12 states is vastly different from doing it across 40+ states. If $BROS is planning on maintaining a store opening CAGR of 15% per year (17% since 2018), it will have to ensure its supply chain can keep up with the pace of expansion.

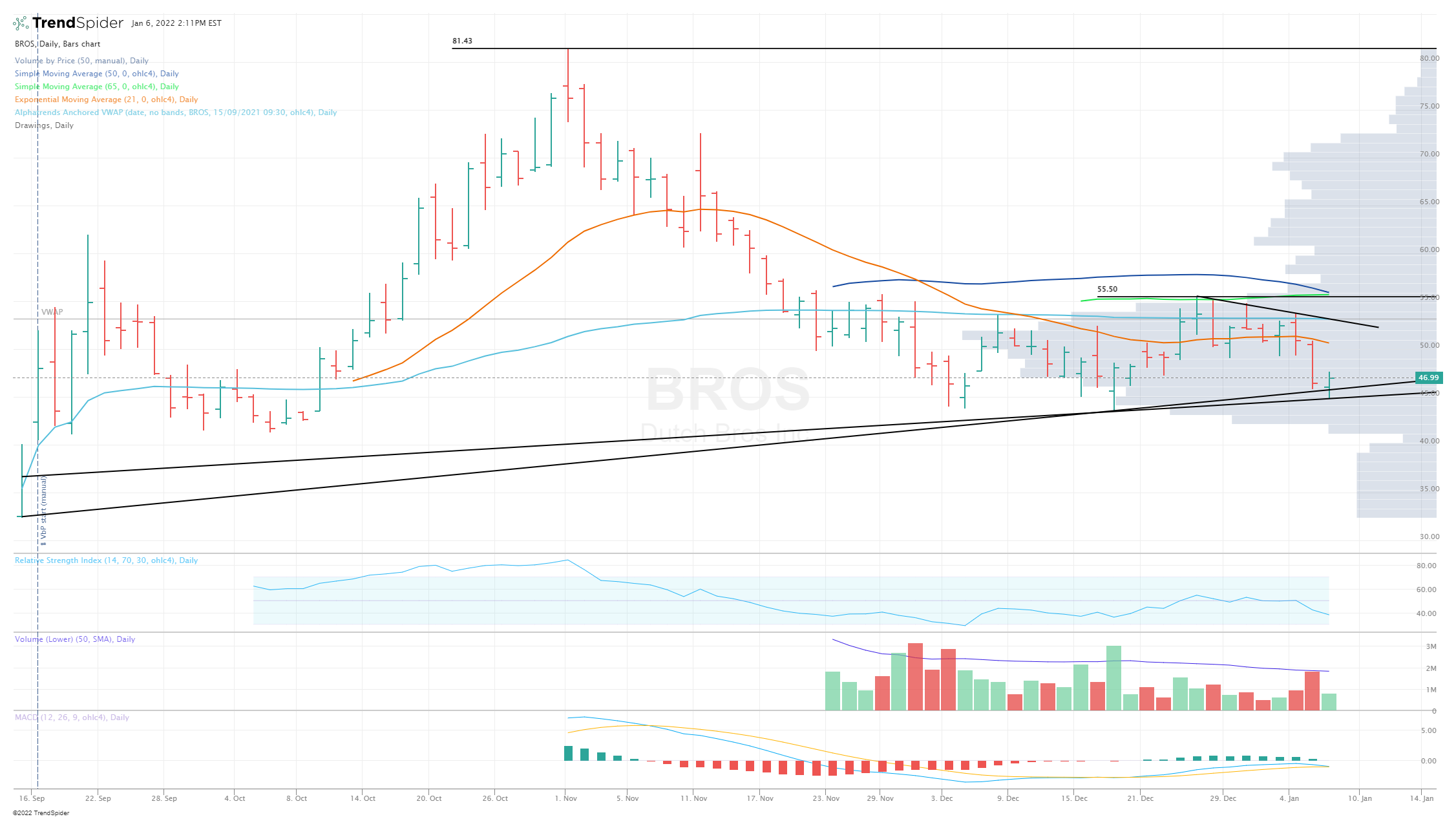

TECHNICALS:

When I look at the technicals the first thing that stands out to me was the bounce today (January 6th) off that support line going back to the IPO — just depends whether you anchor that line at the lows on the IPO day or the closing price on the IPO day. I think this trendline is notable which means if we can’t hold it then I’d reduce my current position by 30-50%.

If $BROS can’t hold above the trendline back to the IPO, then the next support area would be $43.55 which was the low on December 17th. If we can’t hold there then I’d likely reduce my position again.

The last level of support would likely be the IPO day in the low to mid $30s. Hopefully $BROS doesn’t go that low but anything is possible in the short term. Even though I’d reduce my position if we can’t hold the first two support levels, I’d probably increase my position if we got down into the mid $30s. That would be a very attractive entry point in my opinion given the growth story that is underway at $BROS.

Since $BROS has only been public for a few months we don’t have the longer term moving averages like 100d, 150d and 200d however we do have the 10d, 21d, 50d and 65d. Right now $BROS is trading below all of them although most growth stocks right now.

If you’re looking to get into $BROS, I think you can play it a couple different ways. You can buy here with a partial or full stop loss under the trendline…or… you can wait until $BROS reclaims the 10d or 21d moving average…or… you can wait until the 5d EMA crosses over the 8d or 10d EMA which usually signals that a new base has formed and momentum has turned bullish. If you’re looking at the MACD at the bottom of the chart, you’re looking to own stocks when the blue line is above the orange line. As you can see right now those lines are right on top of each other which means the short term direction is very unclear. You might want to wait a few more days to see whether we turn up or turn down.

SHAREHOLDERS:

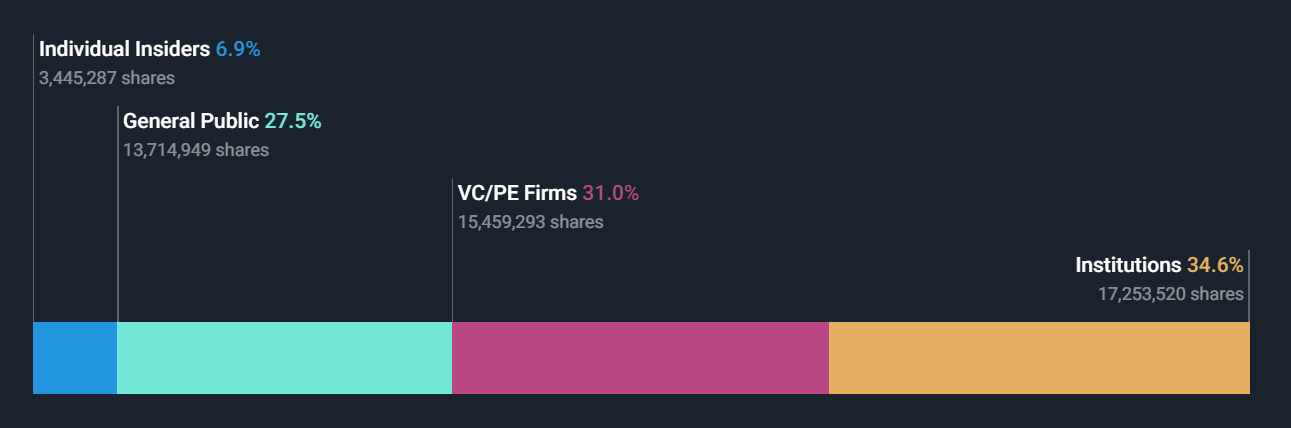

For a recent IPO, the current shareholder base is nothing new. We have early investors owning 30-40% of the outstanding shares many of which will probably sell down their stakes over the next 6-18 months. For a recent IPO, I like seeing that 1/3 of the float is already owned by institutions including some high quality funds if you look down at the second chart.

I’m a little surprised that insiders (ie founders & key employees) only have 6.9% of the shares however they were privately held for 30 years so it’s possible the original founders were forced to sell down their equity over the years in order to fund their growth.

The top 25 shareholders are as follows:

TSG Consumer Partners [click here] is a $10 billion private equity group that owns close to 1/3 of the outstanding shares so it’s very likely they’ll need to eventually sell down this stake, just hard to know exactly when.

As I mentioned at the very beginning, according to IPOScoop.com $BROS lockup expiration is currently scheduled for March 13th — I think it’s fair to assume that after this date some of the early investors on this chart will be sellers which means we’ll get an announcement that the company is doing an offering.

Given that $BROS currently has less than $30 million on the balance sheet (after they paid off their debt with the IPO proceeds) it would surprise me if $BROS didn’t also raise some capital in that secondary offering. If I had to guess I'd say that insiders would sell ~$250-300 million while $BROS raised $200-250 million for their balance sheet to fuel their 2022 and 2023 growth plans.

From my experience a 3% capital raise (3% of their $7500B market cap = $225M) in one of these secondary offerings is pretty standard. Since $BROS is already profitable ie not burning cash every month/quarter it’s possible they might do a smaller capital raise — perhaps in the $100-150 million range. When that secondary comes the stock would probably be down 4-5% which is typically a nice time for adding to your position assuming you’re still bullish longer term.

ANALYSTS:

Overall, analysts appear to be quite bullish on $BROS — I guess they realize that people love coffee :)

Of the 9 analysts covering $BROS — JP Morgan, Stifel Nicolaus, Piper Sandler, Cowen, Bank of America, William Blair, Robert Baird and Jefferies have a BUY rating (aka OUTPERFORM or OVERWEIGHT) and 1 analyst from Barclays has a HOLD. The average price target amongst these 9 analysts is $70.13 with the highest at $85 and a lowest at $53.

In case you’re wondering, I gave this info from StockTargetAdvisor.com

CONCLUSION:

I’m going to assume that most of the people reading this writeup from the West Coast are very familiar with Dutch Bros and the people from the Midwest and East Coast are not very familiar with Dutch Bros.

Just like most of you were probably not familiar with $DLO $GLBE or $OLPX, I’m hoping that $BROS is a name that has you interested.

Starbucks ($SBUX) went public in June 1992 at $17 per share however if you adjust that price for all of the stock splits over the past 30 years it takes it down to just $.27 which means $SBUX is up ~411x since the IPO. That means if you invested $10,000 in the $SBUX IPO you’d have $4.1 million today (assuming you didn’t sell any).

I certainly don’t expect $BROS to perfect anything close to $SBUX but there’s definitely an exciting growth story here that is worth paying attention to. This company is far from perfect… my two biggest knocks on $BROS are “only drive-ups” and ”no mobile ordering” but it’s very possible both of these are fixed in the next few quarters. I don’t know $BROS exact expansion strategy through the Midwest and into the Eastern states… it’s possible they will stay in the suburbs and stick with drive-ups only however if they want to be in downtown markets they might need to adjust this. However I will say that most of the Dunkin Donuts in downtown Boston are always packed and there’s rarely more than 1-2 tables to sit down so it’s possible that $BROS could stick with this approach and make it work.

As of today, $BROS is a 2% position in my portfolio, there’s a chance I’ll do some small adding in the next few weeks but mostly I’ll hold off until we get through that lockup expiration and then see if there’s a secondary offering which drops the stock 4-5% in which case I’ll do some buying.

Over the past 20 years of being an investor I’ve probably own $SBUX less than 200 days even though it’s been one of best performers and growth stories in the entire market. Americans love their coffee, we are addicted and it’s part of our daily routine. $BROS appears to have a very loyal customer base that chooses them over many other options. They’ve definitely found a way to stand out in a crowded market. I’m just hoping they can keep that magic going as they expand across the country and hoping one day I’ll see them in Boston.

If you do live near a $BROS and go there frequently, please let me know what you think of the brand, products, pricing, customer experience, mobile app/rewards and so on. Whether it’s good or bad feedback, I’d love to hear your take on the company.

If you need a laugh, I stumbled across this video… seems like $BROS has a reputation for hiring very high energy people and not every customer is on their level haha

Hope you enjoyed this deep dive writeup on $BROS — if you have any thoughts, comments or questions please feel free to reach out at jonah@luptoncapital.com

Best regards,

Jonah Lupton

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletters. Please manage your portfolio and position sizes in accordance with your own risk tolerance and investment objectives.