Part 1: Deep dive on Block ($SQ)

Part 1: Deep dive on Block ($SQ)

In addition to my Substack newsletters, I also run a Stocktwits room where I post my current holdings, daily activity, investment models, technical analysis, live charting, live trading and market commentary for both my Investment Portfolio (long term, strong fundamentals, 20-30 holdings) and my Trading Portfolio (short term, strong technicals, 10-20 holdings). The two options are $15/month for the monthly plan [click here] or $150/year for the annual plan [click here]. Prices for both plans are going up at the end of February so you have 4 more weeks to lock in at the current prices.

You can now signup for my new Substack called Jonah’s Trading Charts which is focused exclusively on technicals/charts and great trading/breakout setups. Every morning I do a live charting session at 5:30am and then send out an email with my 10-20 favorite trading charts/setups for the day. You’ll also have access to my current trading portfolio with current positions/sizes, entry/exit prices and gains/losses/win rate. I also do live charting/trading sessions most days at 10-11am and 3-4pm.

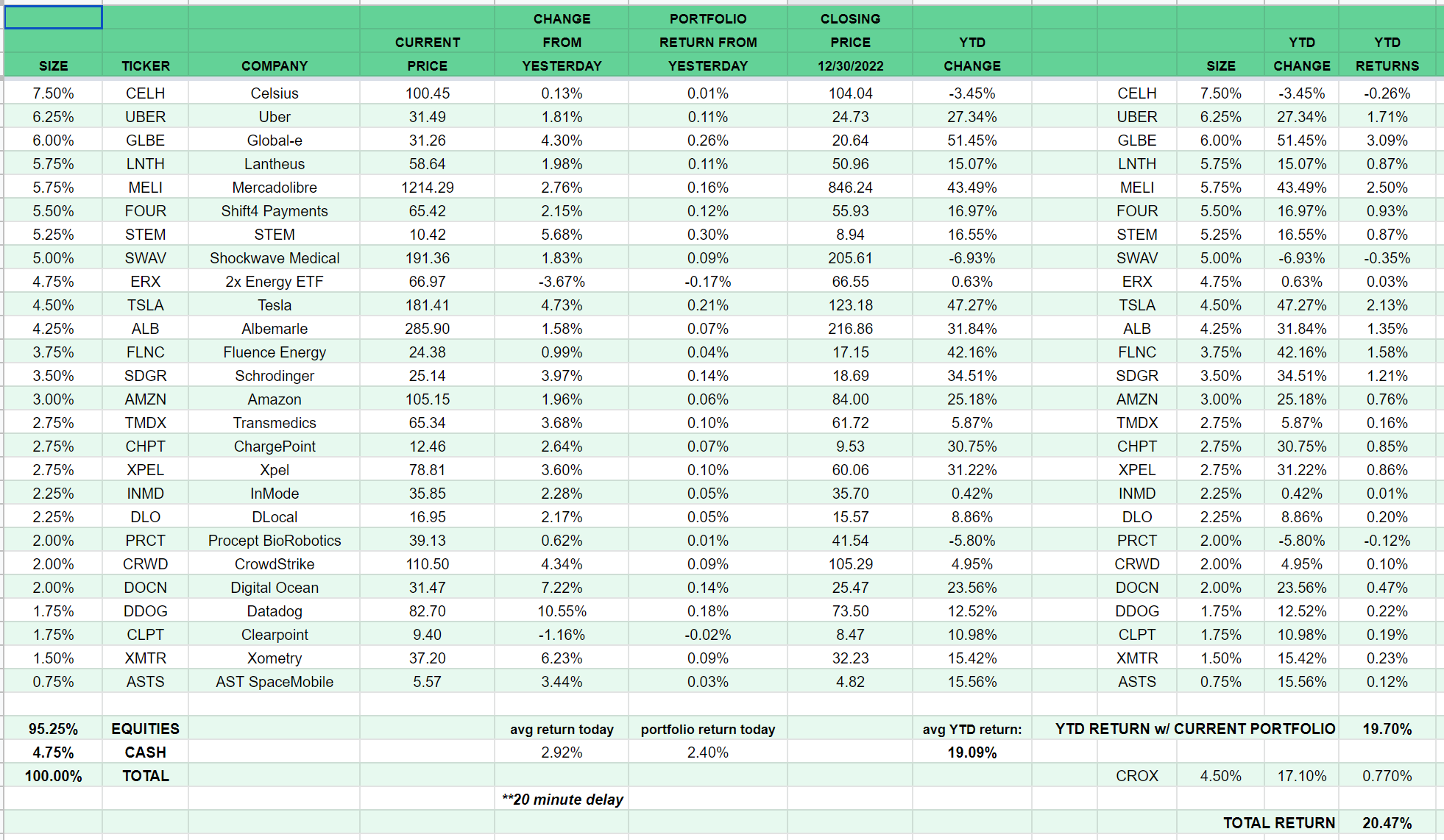

Here is my current investment portfolio, going forward I’ll keep it behind the paywall for paid subscribers only.

Company: Block (formerly Square)

Ticker: (SQ)

Website: Block.xyz and Square.com

IPO date: November 19, 2015

IPO price: $9.00

Current stock price: $83.90

Outstanding shares: 600.1 million

52 week high: $149.00 on March 29, 2022

52 week low: $51.34 on November 03, 2022

All time high: $289.23 on August 05, 2021

Market cap: $50.348 billion

Net cash/debt: -$165 million

Enterprise value: $50.513 billion

Headquarters: San Francisco, California, United States

Number of employees: 14,000+

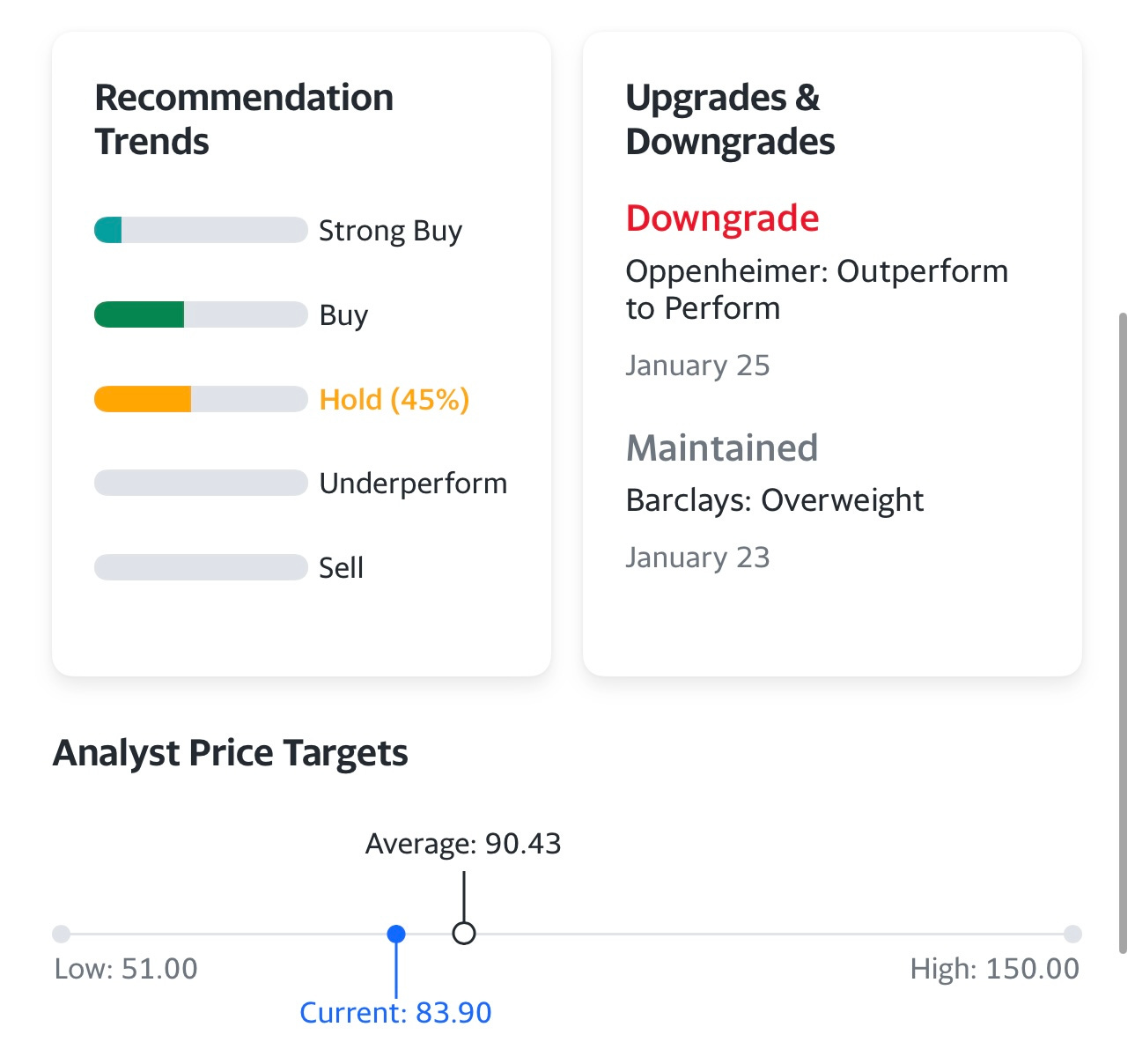

Average price target from analysts: $90.43

Investor Relations [click here]

Q3 2022 Shareholder Letter [click here]

Q3 2022 Earnings Call [click here]

Block Investor Day 2022 [click here]

Next earnings date/call for Q4 2022 is February 23, 2022

Outline

Introduction [Part 1]

Company Background [Part 1]

Opportunity [Part 1]

Technology [Part 1]

Business Model [Part 1]

Customers [Part 1]

Competitive Advantages [Part 1]

Management [Part 2]

Culture [Part 2]

Financials [Part 2]

Risks [Part 2]

Ownership [Part 2]

Valuation [Part 2]

Investment Model [Part 2]

Analysts [Part 2]

Technicals [Part 2]

Conclusion [Part 2]

Introduction

As you could see from the screenshot up above showing my current investment portfolio, I don’t currently have a position in SQ however it’s definitely on my watchlist and I’m encouraged by the recent price action in the stock.

Despite SQ being up 63.4% from the lows just 3 months ago, SQ is still down 70.9% from the all time high in 2021. SQ has been flirting with the 200d ema for the past week, getting back above it today after the FOMC meeting.

We’ll dig into the charts more in Part 2 of this writeup which should be out in the next couple days.

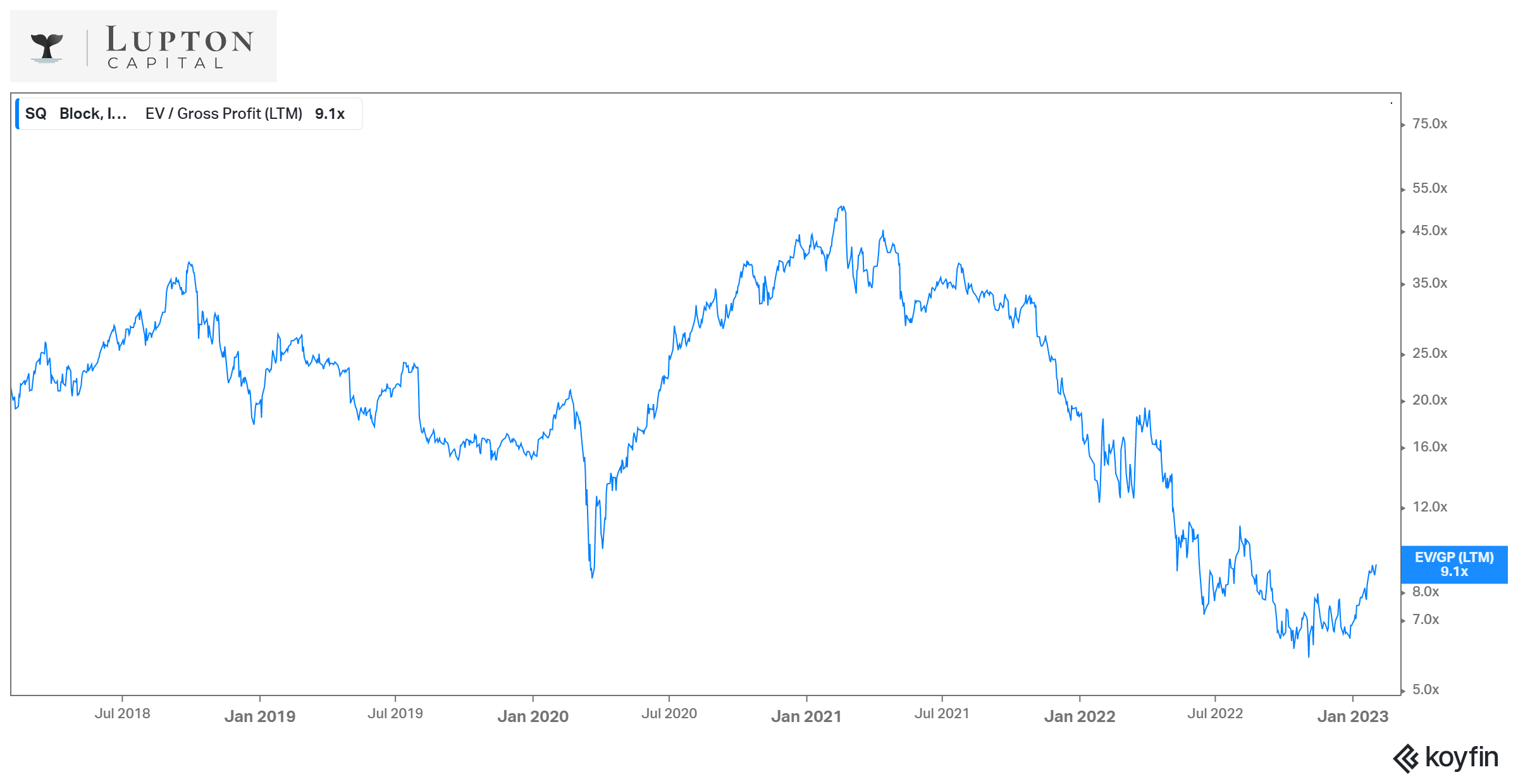

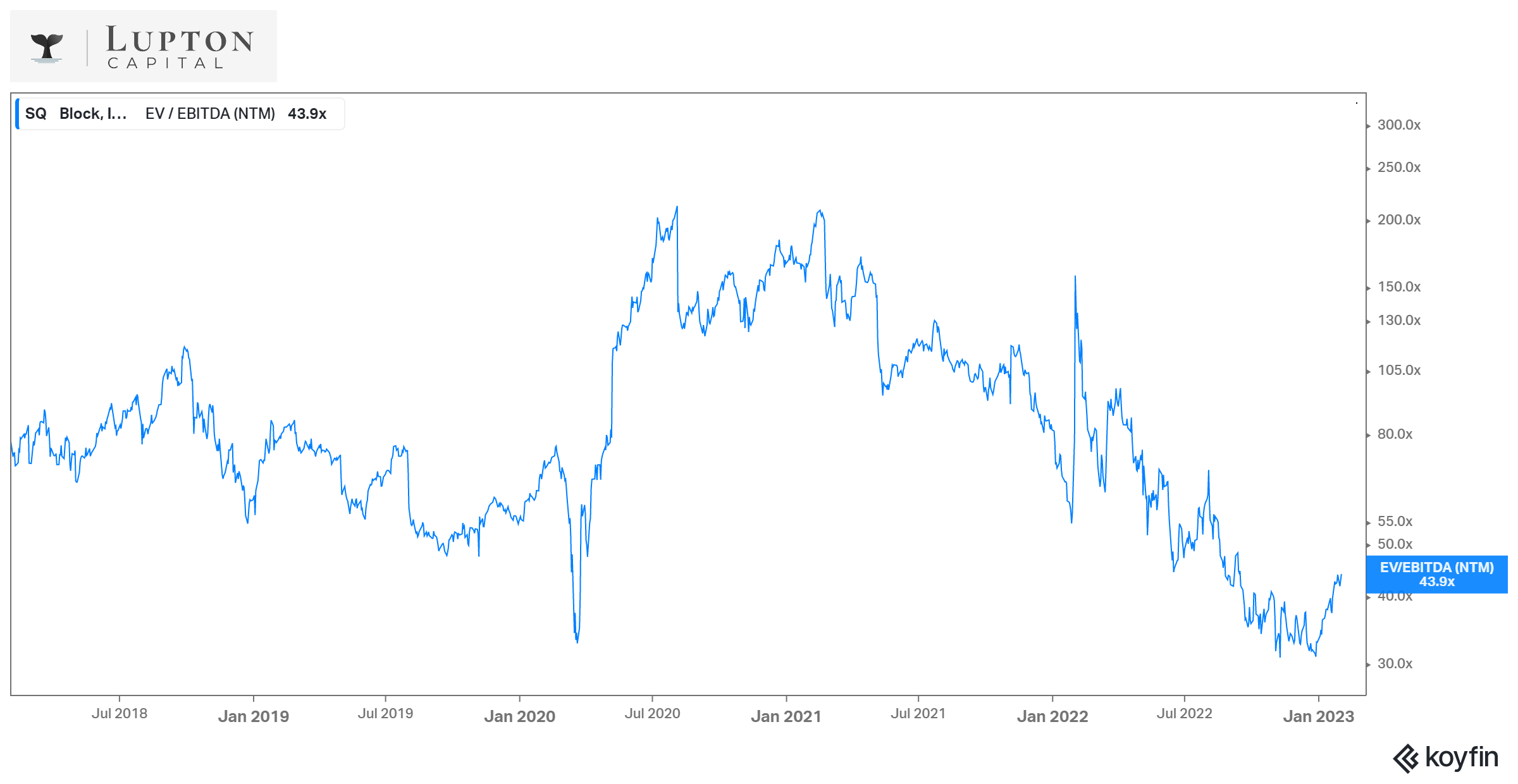

If you look at the chart above and the chart below you can see how much the SQ multiples have contracted over the past two years. In early 2021, SQ was trading at more than 50x LTM EV/GP and more than 200x NTM EV/EBITDA versus today those multiples have shrunk to 9.1x LTM EV/GP and 43.9x NTM EV/EBITDA. I’m not saying that SQ is cheap but it’s a hell of alot cheaper than it was 24 months ago despite growing revenues by almost 100% during that time — although some of this growth was from crypto trading which miniscule margins.

SQ is already up 33.5% YTD, similar to many other long-duration growth stocks so buying it here would kind of feel like chasing however given that SQ is still 22% below the VWAP from the ATH, if the markets continue to grind higher (especially the Nasdaq) then it’s possible SQ could run up into that VWAP before they report earnings on February 23rd. If I did start a position in SQ in the next couple days, with a stop loss below the 200d ema (if I wanted to keep it tight) or below the 10d ema (if I wanted to keep it a little looser) and it did rally into earnings (in three weeks) then I’d probably trim the position because I’d be worried that expectations had risen too much and the stock could be setting up for disappointment.

Personally, after the big rally in growth stocks today (after the FOMC meeting and Powell press conference) I’m getting a little concerned about how many stocks are up 50% or more over the past few months. I know that inflation is coming down and the FOMC is almost done hiking but there’s still alot of questions about the economy in 2023, where $SPX earnings will come in and what the right $SPX multiple might be given current growth rates and Treasury yields (2Y & 10Y). With $SPX now above 4100 and $SPX earnings expected to below 220 this year, we’re now talking about a 18.6x multiple on $SPX which is kind of frothy given flat to low single digit EPS growth.

I guess what I’m saying is that SQ and many other growth stocks might be solid companies with a bright future but now is not the time to be chasing them, especially into earnings without a profit cushion to play with.

Given the move in SQ over the past few months, if you were looking to build a position in SQ please don’t be in a rush. It’s alright to start with a partial position now and then either wait for a near-term pullback (which may or may not happen) or wait until you see Q4 earnings in a few weeks which will likely include 2023 guidance. Currently the revenue consensus for 2022 is $17.47 billion and then 20.0 billion for 2023 which would be a 14.5% increase. That’s a far cry from the 40-60% YoY growth that SQ was putting up in 2016 through 2021. Technically SQ did have a 91% revenue CAGR during those 5 years but 2020 and 2021 included the revenues from crypto trading so the numbers are kind of skewed.

SQ might never be a high-growth company again but that doesn’t mean it’s not investable. If SQ can maintain 15-20% revenue growth over the next 4-5 years (which is right inline with current estimates) while expanding gross margins from 34% (2022) to 42% (2026) and expanding net income margins from 4% (2022) to 12% (2026) then SQ shareholders should do very well. If we throw these numbers into my investment model (which I’ll share in Part 2) and we assume 1.9% annual stock dilution (that’s the current LTM number) and a P/E or FCF multiple in the mid-30s then my price target for SQ in 3-4 years is $225-250 which is still below the all time high but that’s still 160-200% higher than the current price. If SQ is able to grow revenues and/or increase margins even faster than the upside should be more substantial. Based on current analysts estimates, SQ is going to generate more than $10 billion of FCF over the next 4 years. Granted that doesn’t include SBC (stock based compensation) but that FCF can be used for acquisitions and/or stock buybacks when the time is right.