$AEYE - AudioEye

This free newsletter is sponsored by:

Every week I will partner with a company as a sponsor which keeps this newsletter free for non-paying subscribers. Every sponsor has been personally vetted by me. I'm excited to introduce our first partner and share a free stock offer — Public.com

If you're interested in investing but don't want to be alone, Public is the place for you. Public.com has created a social layer for investors, so you can own the companies you believe in and share your stock ideas within a community of investors.

Free mobile app, no account minimums, and $0 commissions on standard trades

Ability to form chat groups with your friends, like mini-investing clubs

74% of the community are longer-term investors, not looking to day trade

No more PFOF — Public.com recently decided to stop earning revenue from Payment for Order Flow and instead routes your trades directly to the exchanges

My subscribers can start with $10 in free stock by downloading the app here.

*Offer valid for U.S. residents 18+ and subject to account approval. Free stock for new accounts only — Public.com/disclosures

Down below is the writeup I sent to my paid subscribers earlier this week.

If you’d like to become a paid subscriber and get the writeups right away, please go to https://jonahlupton.substack.com/subscribe — the cost for paid subscribers is $10 per month or $100 per year. Paid subscribers also get early access to many of my CEO interviews.

Follow my current investment portfolio [click here]

Signup for my Stocktwits daily chat room [click here]

Signup for Fintrics for help with fundamental analysis [click here]

Watch my recent CEO interviews on YouTube [click here]

Follow me on Twitter [click here]

$AEYE - AudioEye

Introduction to AudioEye [watch here]

Website: AudioEye.com

Stock Price: $27.18 (price when writeup was sent to paid subscribers on March 16th)

Market Cap: $290 million

Enterprise Value: $275 million

Headquarters: Tucson, Arizona

Founded: 2005

Founders: Jim Crawford and Sean Bradley

CEO: David Moradi [click here]

Funding: $17.3 million [click here]

Employees: 100+

Phone: 866-331-5324

Email: info@audioeye.com

AudioEye Investor Presentation [click here]

AudioEye 2020 and Q4 Earnings Report [click here]

AudioEye 2020 and Q4 Earnings Call Transcript [click here]

AudioEye 2020 and Q4 Earnings Call Webcast [watch here]

AudioEye on Vimeo [click here]

AudioEye on Twitter [click here]

AudioEye on Facebook [click here]

AudioEye on LinkedIn [click here]

AudioEye on Instagram [click here]

2018 revenues: $5.6 million (actual)

2019 revenues: $10.8 million (actual)

2020 revenues: $20.5 million (actual)

2021 revenues: $31.8 million (estimate)

2022 revenues: $45.4 million (estimate)

$AEYE — AudioEye

Introducing the AudioEye portal and toolbar [click here]

INTRODUCTION:

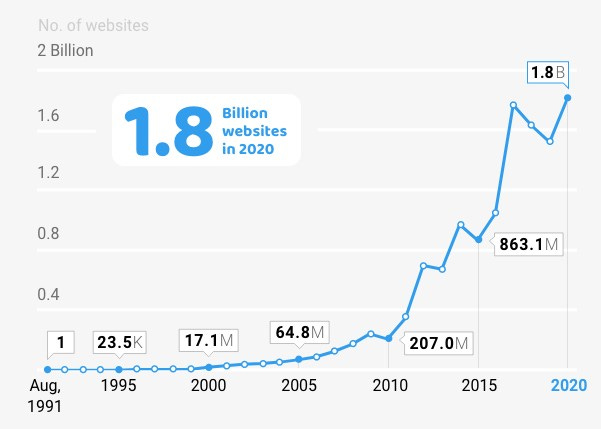

Did you know there are 1.8 billion websites?

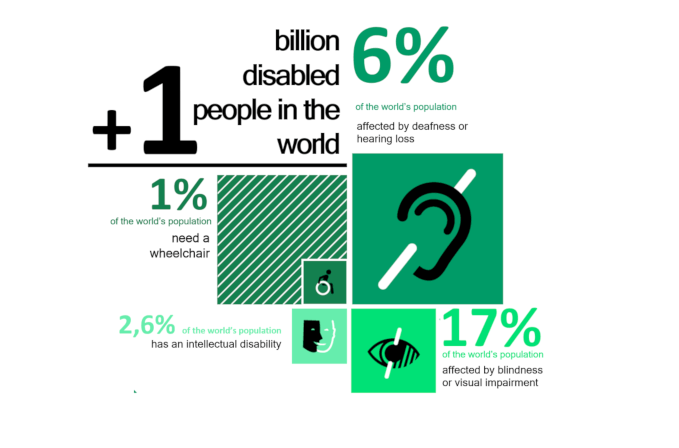

Did you know there are more than 1 billion people with disabilities?

I bring up these two mind boggling statistics because they are related when it comes to AudioEye (now referred to as $AEYE).

$AEYE has created a suite of products to help companies keep their websites more accessible and compliant for people with disabilities. As our lives have shifted towards digital-first everything it’s critical that these 1 billion people are not neglected or left behind — AudioEye can be part of this solution.

OVERVIEW:

Founded in 2005 as an R&D company, $AEYE began as an audible player plugin, enabling websites to be read out loud, creating a better experience for people with disabilities.

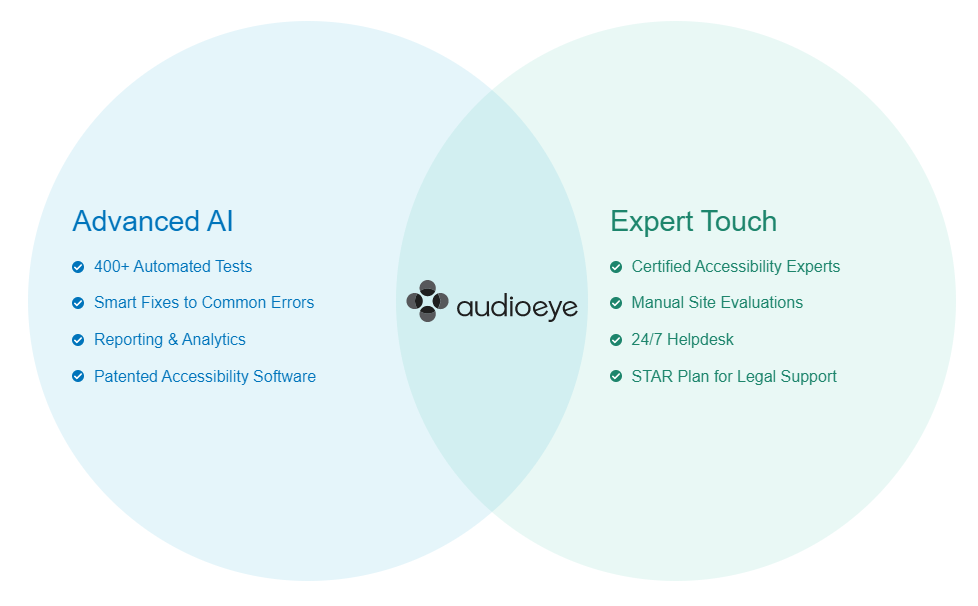

Over the past 15 years $AEYE has continued to be a leader in breaking barriers to digital accessibility through product innovations, including 400+ accessibility tests, AI-powered remediation and IAAP certified expert advisors (International Association of Accessibility Professionals).

Using advanced voice recognition and artificial intelligence $AEYE gives individuals the opportunity to have fair and equal access to websites. This is called “digital accessibility” and I want everyone to watch this video so you understand the challenges that many people are facing [watch here].

$AEYE’s platform when connected to voice recognition and artificial intelligence engines, can provide for a fully Audio Internet (TM) experience complete with voice navigation and voice-driven transactions. Everything the Internet can do AudioEye can do better without the use of a visual display, mouse, or touchpad. It offers technology that makes digital content more accessible and more usable, for more people.

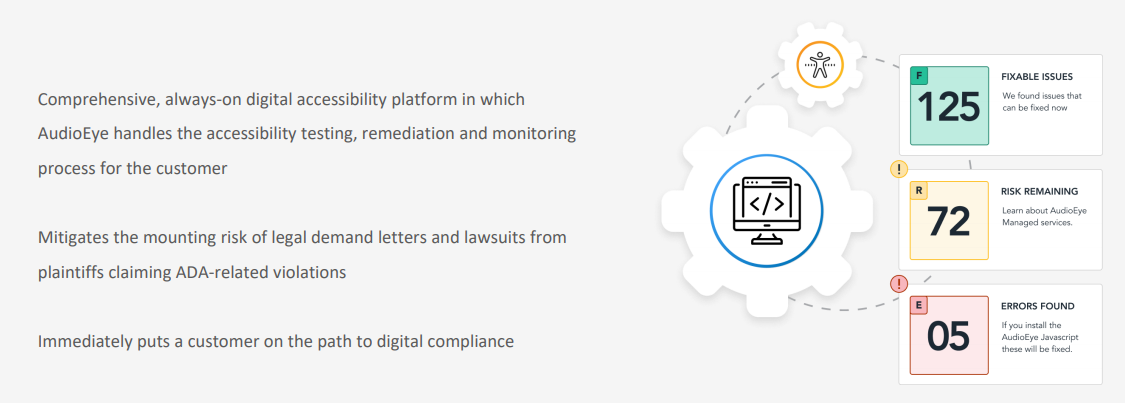

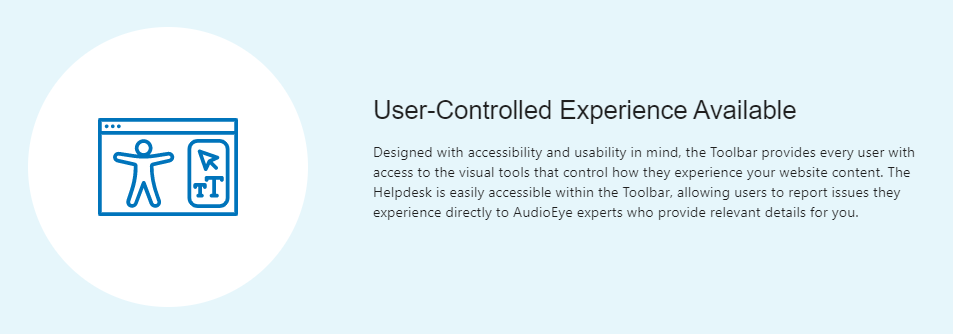

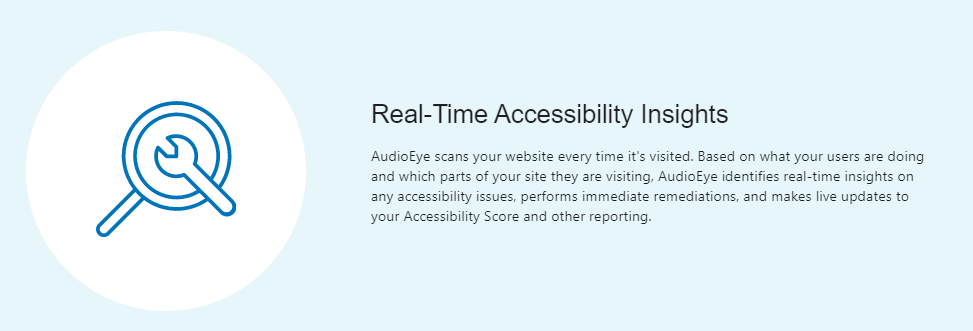

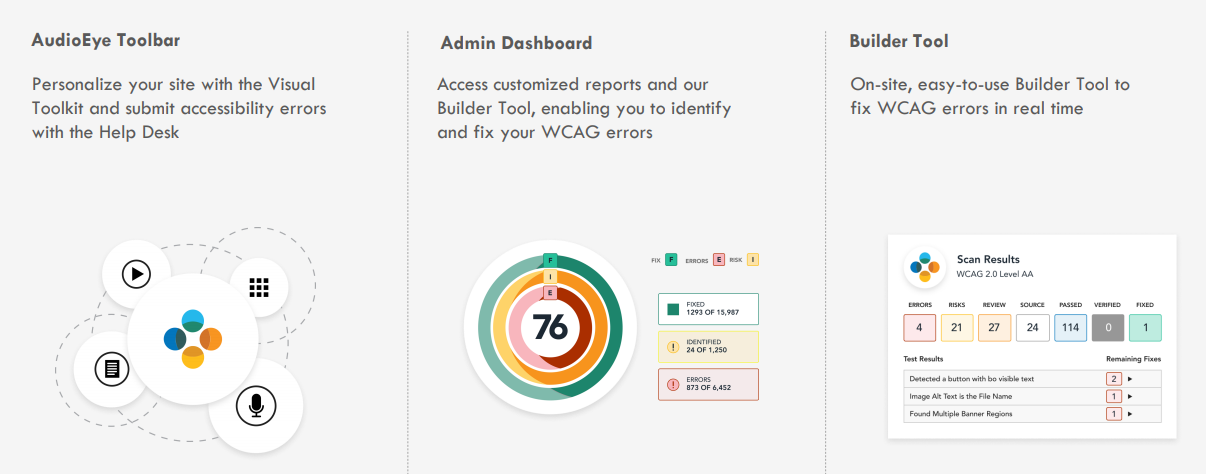

After developing the technology to provide digital accessibility, $AEYE launched a software product that enables companies of all sizes to monitor and analyze their websites for accessibility problems, suggest fixes and help them stay compliant for the Americans with Disabilities Act (ADA).

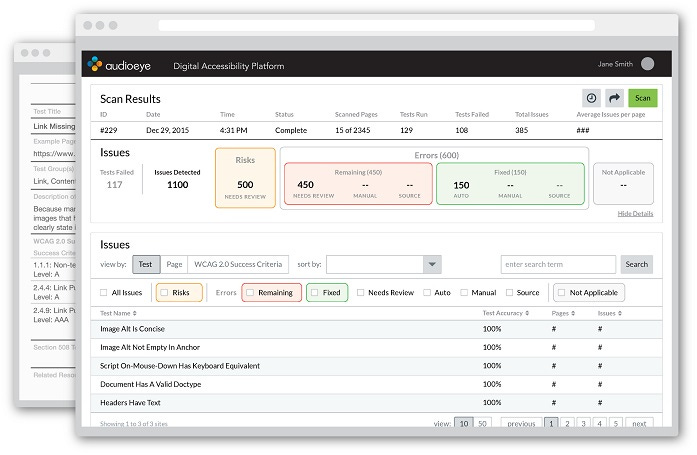

$AEYE provides a dashboard where companies can see their accessibility score, potential risks, remaining problems, fixed problems and more. $AEYE is the AI-powered software automation tool that companies should be using to ensure a better experience for more people while protecting themselves from expensive lawsuits.

$AEYE stands out among its competitors because it not only provides a better, more accurate solution but it’s easily installed into the code base of any website without fundamental site architecture changes.

$AEYE catches 3x more errors/mistakes than their closest competitor.

PROBLEM:

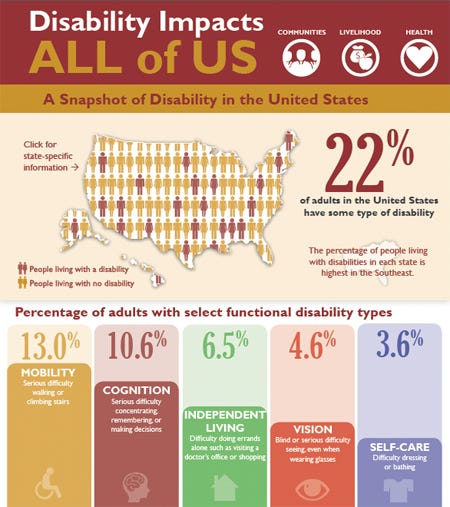

There are more than 1 billion people across the globe including more than 65 million people in the U.S. living with disabilities — these disabilities vary in severity but many of these people are at a big disadvantage when it comes to using the internet.

Every company should want to keep their website accessible for everyone. This means whether a potential user/customer has a reading disorder, sight impairment, color blindness, loss of motor skills or something else — they won’t feel discriminated against when they come to your website. Providing better accessibility for these people will not only improve their experience but also increase their loyalty and the likelihood of repeat business in the future.

As a company you also don’t want to be accused to discriminating against people with disabilities and then dragged into an ugly, expensive lawsuit so using $AEYE is a great way to feel confident that your digital assets are up to the ADA standards while providing some legal protection.

There were more than 3,500 digital accessibility lawsuits filed in 2020 alone so don’t let your company be next.

PRODUCT | SOLUTION:

$AEYE has made it very easy for companies to install their software into their websites. You don’t have to be very tech savvy to install the code — $AEYE has detailed instructions on their website plus they have “accessibility experts” available by chat and phone to assist you. I actually spoke to one of them today because I had a few questions while doing this writeup.

BUSINESS MODEL:

$AEYE is really a B2B SaaS company (software-as-a-service) that gives SMB’s and larger enterprise companies a chance to increase the ROI on their websites by making them accessible to more people.

$AEYE believes that artificial intelligence and automation is not only important for their customers but also allows $AEYE to generate higher gross profit margins (currently 73%) and net operating leverage going forward.

Most companies don’t want to worry about their website accessibility 24/7 not to mention the laws/regulations are always changing and new content is constantly being added to websites so $AEYE can provide some piece of mind that everything is being monitored, flagged and fixed.

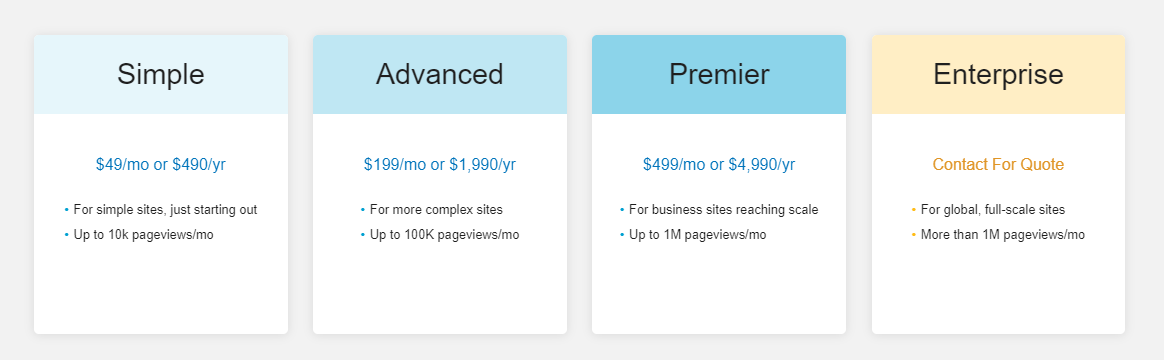

PRICING:

Like most SaaS companies $AEYE has multiple pricing tiers based on the company’s needs and the complexity/size of their website(s). Most SMB’s would obviously start on the $49/month plan with much larger companies paying $199 or $499 per month.

From the recent earnings call the CEO seemed very excited about the number of larger customers they have onboarded over the past 3-6 months and the strong likelihood that many of those customers move to more expensive (premium) plans in the near future. $AEYE also has a very high customer retention rate (approximately 90%) which goes to show good value at a reasonable price. These companies do not want to build their own digital accessibility product internally so $AEYE is a worthwhile expense.

We’ll talk about this a little later but $AEYE has begun partnering with companies to help get better distribution (ie installations) which probably means they are giving up a small chunk of the revenues per customer however they are getting more installations.

As of the end of 2020, $AEYE had 32,000+ customers which represents a 370% increase of the end of 2019. This is monstrous growth in the customer base and I guarantee we haven’t even begun to see the revenue potential from this growth.

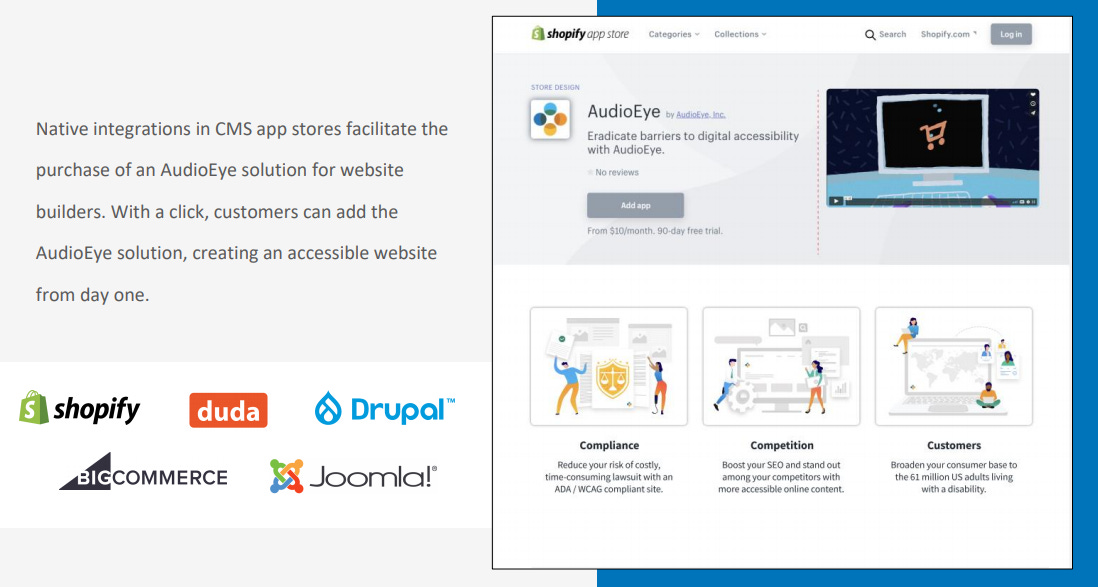

INTEGRATIONS:

You can see all the integration partners here: [click here]

One of the reasons I’m super bullish on $AEYE over the next few years is because of all their installation partners such as WordPress, Shopify, BigCommerce, HubSpot, Drupal, and many more. These are literally the largest CMS (content management system) companies, website builders and ecommerce platforms in the world. These companies together probably account for 80-90% of all the active websites — just WordPress alone accounts for more than 500 million websites globally.

If you go to this page on the AudioEye website [click here] they list all the integration partners with links to installation instructions for each.

Knowing how easy $AEYE is to install through any of these platforms is a huge advantage going forward and means the number of potential $AEYE customers around the world is essentially endless.

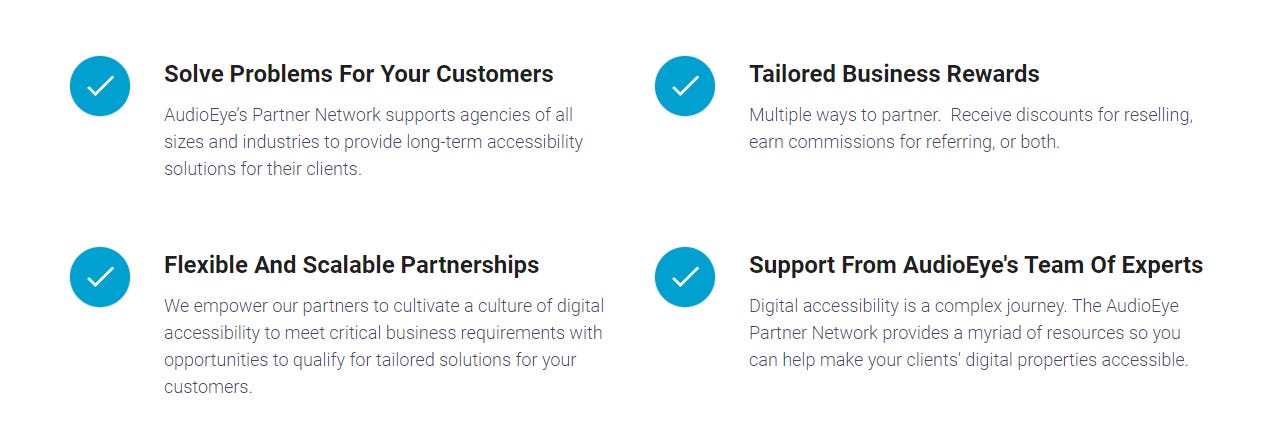

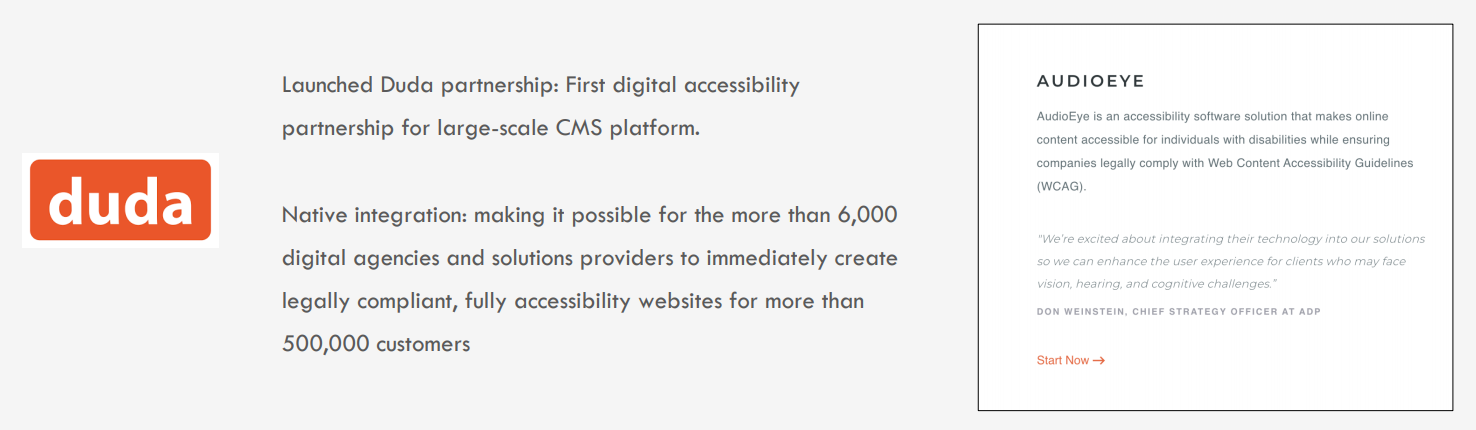

PARTNERS:

As I mentioned earlier, $AEYE has been partnering with different types of resellers and referral partners. One of the examples on the recent earnings call was with a digital design/marketing agency that would be deploying $AEYE across many of their customer websites. Since $AEYE has great margins (as is common with SaaS companies) they are able to strike these types of deals while keeping those installations very profitable.

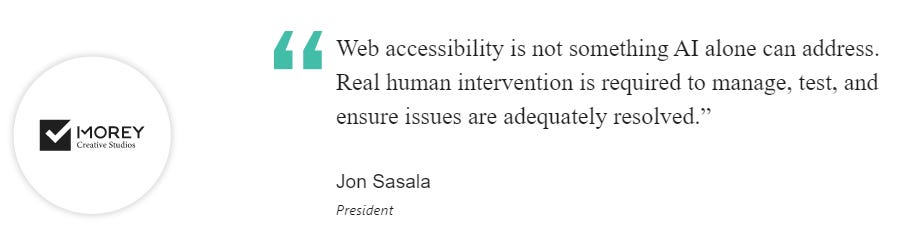

Here’s a video with one of their partners, Morey Creative Studios, that recommends $AEYE to their customers [watch here] in order to keep them accessible and compliant. In this video they mention being a HubSpot partner as well - $HUBS is now a $21 billion company and uses a very similar reseller model with the same types of agencies that $AEYE wants to work with.

This is a link to the Partner Network Program Guide that $AEYE created to show their referral/reseller partners what to expert [click here]

Here are some case studies and success stories [click here].

CUSTOMERS:

$AEYE already has a very solid customer list including the FCC, Square, Fox Media, ADP, Samsung, Uber, and thousands more. As I stated earlier, $AEYE had 32,000+ customers at the end of 2020.

Lots of SaaS companies are forced to focus on SMBs or large Enterprises but $AEYE has already shown an ability to work with both groups including government agencies. I believe $AEYE will continue to see strong customer growth over the coming years given the simplicity and affordability of their product offering.

Any company that chooses not to use $AEYE is basically saying they don’t care about people with disabilities — so part of my investment thesis is that we’ll see both societal pressures around these issues as well as tighter government regulations with more severe fines and penalties for companies that don’t comply.

REVIEWS:

I looked at a few different sites to gauge the sentiment around the company from both customers and employees and overall they look good.

$AEYE as a product got 9.3 out of 10 [click here]

$AEYE as a company (including the CEO) got 3.5 out of 5 [click here]

Below are some customer reviews/endorsements off the company’s website — it always adds more credibility when the endorser is willing to give their full name plus the company they work for:

MARKET OPPORTUNITY:

Clearly the TAM is enormous for a company like $AEYE since there are 1.8 billion websites and millions of them could benefit from $AEYE’s software which not only provides voice assistance but also provides the “visual toolkit” to allow for adjustments to fonts, colors, etc.

$AEYE is bringing on new customers at a wild pace although it’s unfair to assume they can keep up the 370% clip that they saw in 2020. The goal now is convert those new customers onto more expensive plans.

I think the biggest opportunity for $AEYE is working with their referral/reseller partners in order to get access to their client base as well as the CMS platforms for easy integration.

We need to see more partnerships like this one…

FINANCIALS:

There are only a few analysts that cover $AEYE so we can use their estimates which are below — although $AEYE already provided full year 2021 revenue guidance of $30-32 million (which is probably conservative but CEO’s would rather under-promise and over-deliver).

As you can see revenue growth has been slowing down in recent years as the numbers get larger but this is quite common with SaaS companies. $AEYE increased revenues by 90% in 2020 and reported 73% gross margins in Q4. It’s safe to assume those gross margins will carry into 2021 however on the Q4 earnings call last week management said they expect further gross margin expansion.

Looking at the 2021 guidance $AEYE management is forecasting 50-55% revenue growth although this number seems low if we know the company just increased their customer base by 370%. I don’t know how many of those customers are paying yet or could be upgrading but 50-55% revenue growth seems very light and I’d be surprised if they didn’t end up doing $34-35 million which would be closer to 68% YoY revenue growth. Obviously I don’t know this for a fact but it’s an educated guess based off their customer growth over the past 12 months and their ability to monetize/upsell those customers into paid plans.

VALUATION:

Even though I really like the $AEYE mission and their product offering, the main reason I’m in this stock is for the financials (revenue growth + gross margins) and the valuation. Over the past few days $AEYE has been trading in the $26-$29 range which puts the market cap around $300 million.

Just a few weeks ago the stock was trading in the low $40s so we’ve already gotten a 36-38% pullback which makes the current risk/reward much more attractive in my opinion.

If we use the midpoint of $AEYE’s revenue guidance for 2021 ($31 million) and divide the current enterprise value ($275 million) by $31 million we get approximately 8.8x EV/Sales. I believe this is a very fair multiple to pay for a company that should grow at least 55% this year with perhaps 60-70% as a possibility. This is also a company with very strong gross margins (73%) and has already said they will keep increasing.

$AEYE is expected to be profitable next year with 8.4% net income margins which could be a nice catalyst for the stock price. It’s always nice to see a company with strong revenue growth, expanding margins and free cash flow — these are the types of companies that deserve to trade at a premium and right now 8.8x EV / 2021 Sales is not a premium. I think $AEYE should be trading closer to 14x EV/Sales which would put the stock price in the low to mid $40s which is approximately 60% higher from here.

I think $AEYE could/should have 60% upside over the next 12 months.

TECHNICALS:

Unlike some of my other recent writeups which are/were SPACs with limited trading history, with $AEYE we’re able to see a nice chart that goes back to last summer.

As you can see the stock recently pulled back from the $40s, bounced off the 50d EMA (exponential moving average) and is now trying to find some support. If we do see anymore pullbacks from growth stocks and/or small caps, I’m hoping the 50d moving averages will provide that support especially for a company with strong fundamentals like $AEYE, a reasonable valuation and the likelihood of profitability on the horizon. This combination of factors gives me confidence in owning $AEYE at these levels with limited downside risk.

FINTRICS:

As some of you may know I launched a website last weekend called Fintrics which crunches dozens of financial metrics such as revenue growth, gross margins, free cash flow, etc plus some technical indicators to try and predict 12-month price targets. I looked up $AEYE this morning and got a 12-month PT of $39 — personally I think this is low because I’m confident that they’ll beat their $30-$32 million guidance for 2021 in which case the analysts will need to raise numbers.

MANAGEMENT:

The management team continues to get stronger because $AEYE added Rob Ulveling as Chief Business Officer (most recently at Pinterest) and Zach Okun as Chief Product Officer (most recently at Facebook) — both of these new hires bring a wealth of sales and product experience from world-class organizations and validate that $AEYE is on the cusp of massive growth potential.

Let’s be honest, you don’t leave Pinterest and Facebook unless you think $AEYE provides an exciting growth opportunity with more financial upside (likely from stock options).

Sach Barot, the current CFO, has announced he’ll be leaving $AEYE in May but I’m confident they’ll find a strong replacement.

David Moradi, current CEO is also the CEO of Sero Capital (the largest shareholder) but this is only temporary, because as far as I can tell they are looking to bring in a permanent CEO to replace David.

It appears the founders of $AEYE are no longer actively involved with the company however given that the company is already 15 years old it’s very possible they have moved onto new adventures. The current Board of Directors is primarily made up of the largest institutional shareholders which is fine with me — they have a vested interest in the success of $AEYE.

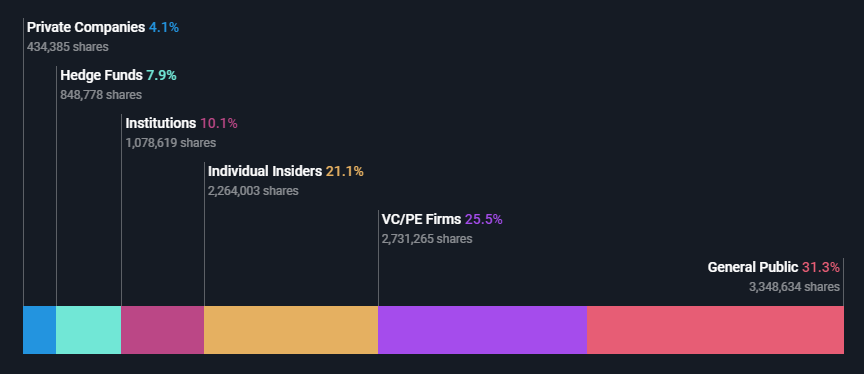

SHAREHOLDERS:

Nice diversity across different types of shareholders from insiders to early investors to institutions to retail.

In terms of largest institutional shareholders there are some high quality names that I recognize like Vanguard and Royce. I was not familiar with Sero Capital but here is there website [click here]. Looks like they take larger stakes in a smaller number of companies. This means they have strong conviction in $AEYE and are willing to make a concentrated bet. Unlike most of my other recent writeups, we rarely see individuals in the top 25 shareholders but just means these executives/insiders have more skin in the game.

CONCLUSION:

Five things got me interested in $AEYE back in January when I first started my position. Over the past couple months I have been adding to that position and $AEYE now represents a 4.5% holding in my personal portfolio.

The five things that got me excited about $AEYE were:

1) Valuation = SaaS company with recurring revenues, 60-80% revenue growth, 70-75% gross margins

2) Mission = make all websites accessible for people with disabilities

3) TAM = 1.8 billion websites, 1+ billion people with disabilities, only 2% of websites are ADA compliant

4) CMS integration partners = including WordPress, Shopify, BigCommerce, HubSpot, Joomla, Drupal, etc.

5) Reseller/ & referral partners = like the website design companies and digital marketing agencies

I don’t think it’s a question as to “if” bigger companies starting using AI-powered ADA compliance software but “when” — either companies start making their websites and digital assets/properties more accessible for people with disabilities or we’ll see more government enforcement. I’ll never understand the daily frustration that people with certain disabilities have to deal with but knowing that companies like $AEYE are trying to provide solutions makes me feel better. There’s no longer any excuse for a company to have an inaccessible or unusable website when we know $AEYE has an option for as low as $49 per month.

I’m glad that the companies in that image below are leading this effort — now we just need the rest to follow.

As stated above, I currently have a 4.5% position in $AEYE and I will continue adding around these prices because I think the valuation at less than 9x EV/Sales is very fair with limited downside risk unless we got a significant pullback in the markets — in which case most high growth stocks would suffer short term losses.

Just as a reminder, my investment strategy for my personal portfolio as well as my Social Capital fund is to find stocks with market caps under $5B that I believe can 5x over the next 5 years — typically this is happening from sustained revenue growth above 40% with minimal multiple contraction or it’s happening with less 30% or less revenue growth but some multiple expansion.

It’s very hard to know where P/S multiples will be in 5 years but I’ve done enough analysis on $AEYE to believe they can average at least 40% revenue growth over the next 5 years which makes them a great candidate to be a 5-bagger during that time frame. I also think it’s possible we get some multiple expansion just like I think it’s possible they get acquired. There are a few companies that would make ideal acquirers for $AEYE because those acquirers already have a large customer base and established reseller network.

I hope you enjoyed this writeup on $AEYE — if you’re looking for a high-growth SaaS company with great margins, nice product offering, expanding margins, and fair valuation then I’d encourage you to take a hard look at $AEYE for your portfolio. I’m planning to be in this stock for a while so feel free to ask me any questions.

I’ve already spoken to the Investor Relations team at $AEYE and we’re trying to finalize a date for me to interview the CEO — hopefully within the next couple weeks.

Disclaimer: The stocks mentioned in this newsletter are not intended to be construed as buy recommendations and should not be interpreted as investment advice. Stocks mentioned in this newsletter should only end up in your own portfolio after you conduct your own research and due diligence. Many of the stocks mentioned in my newsletter have smaller market capitalizations and therefore can be more volatile and should be considered more risky. I encourage everyone to do their own research and due diligence before buying any stocks mentioned in my newsletter. Please manage your own portfolio and position sizes in accordance with your own risk tolerance and investment objectives.